I have gone into my last year of a fixed five year deal at 2.1 per cent, which is due for remortgage in October 2024 – most likely at a higher rate given the current state of play.

My house is valued at £303,000. My current mortgage balance is £39,500.

My monthly repayment is £247 plus I always overpay monthly with an additional £205. I also pay occasional lump sums up to my allowance of 20 per cent.

I envisage that by August 2024 I can get my balance down to around £30,000.

– Read: How to remortgage your home and find the best deal

Mortgage help: Our new weekly pilot the Mortgage Maze column stars broker David Hollingworth answering your questions.

Would the best recommendation be:

A. Remortgage by October 2024 at whatever the balance will be without overpaying anything in the meantime – I know my rate wouldn’t be as low as what I’ve currently fixed at.

B. Remortgage in October 2024 with a balance of around £30,000 due to overpaying (without incurring any fees in the meantime).

C. Pay the whole amount off before, so I don’t have to bother with a mortgage. There is no early repayment fee for early settlement.

I don’t have these funds yet but could get a family loan. This is the best option but might not realistically be possible.

Basically- should I overpay as much as I can in this final year? Or ease up and remortgage for whatever the amount will be? J.H.

SCROLL DOWN TO FIND OUT HOW TO ASK DAVID YOUR MORTGAGE QUESTION

David Hollingworth replies: Although many homeowners have already had to deal with their fixed rate coming to an end there are plenty that continue to relish the protection of an existing fixed deal.

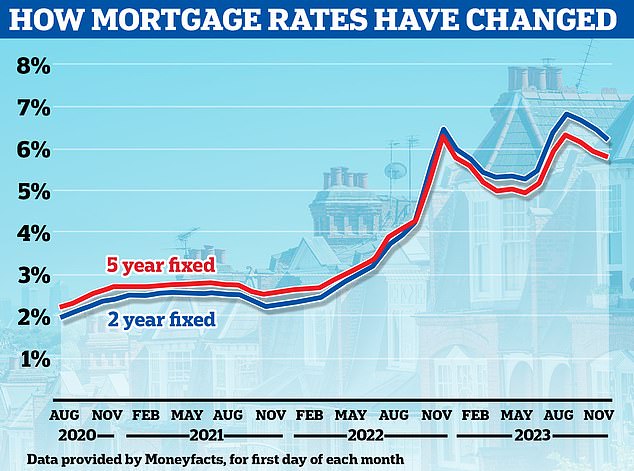

As those expire it will almost inevitably mean having to deal with a higher interest rate, as the era of historic lows in base rate came to an end a couple of years ago.

Since December 2021, the base rate has risen from the all time low of 0.1 per cent to its current level of 5.25 per cent.

Although some fixed rates were as low as 1 per cent at the lowest point, much will have depended on the point at which you fixed.

Fixed rates spiked during periods of volatility this year and after the mini budget with many reaching 6 per cent or more, so your rate looks extremely attractive.

Thankfully, fixed rates have been easing back as the rate outlook has improved but still the rates on offer for a current two or five year fixed rate will be more than double the rate that you have enjoyed in recent years.

Making the most of the remainder of that deal is exactly the right way to think, rather than just waiting for what currently looks admire an inevitable hike in payments in a year’s time.

It appears that you have been using low rates as a good chance to make additional payments off the balance.

– What next for mortgage rates and should you fix for two or five years?

Falling: Average fixed mortgage rates appear to be falling back somewhat after a barrage of rate hikes during the first half of the year but remain much higher than in previous years

Most lenders will allow some ability to overpay without incurring an Early Repayment Charge.

In most cases that will typically amount to 10 per cent per annum but there are some lenders, including your current lender, that offers even more flexibility and allows up to 20 per cent of the balance to be repaid each year without any penalty.

It’s always important to check the terms carefully as an ERC can be substantial.

Continuing to scheme toward the end of the current low rate should help you to mitigate the impact of higher rates.

Overpaying will mean that you have a smaller balance to deal with when your deal ends, which will help limit the boost in payments.

However, you may want to also consider whether saving the money over the course of the next year could offer an alternative or additional strategy.

Savings rates have risen and can be in excess of 5 per cent, so could potentially earn you more interest than you would save by overpaying.

You must take account of any potential income tax on interest the earned though, which could narrow the apparent gap in rates substantially.

You have a relatively small mortgage already and some lenders will have a minimum loan size for their remortgage rates but I don’t think that should stop you from following your preferred approach, whether that’s saving a lump sum to reduce the mortgage when you cme to the end of the current rate or continuing to overpay to reduce the balance month by month.

When you do come to the point of shopping around for a new rate be sure to factor in any fees as these will have a big bearing on the overall value of any prospective new deal.

– True Cost Mortgage Calculator: Check what a new fixed rate would cost

Overpay: Hollingworth says overpaying the mortgage will mean they have a smaller balance to deal with when their deal ends, which will help limit the boost in payments

Because of the size of the mortgage it is unlikely be worth paying a fee to get a lower rate and better to go for something with a slightly higher rate but no fees.

An adviser will help you pilot the various options whether that is switching to a new lender or taking a new deal with your current lender.

They can also talk you through other options such as trackers which could be completely ERC free or offset deals that allow you to set savings against the mortgage.

I’d therefore suggest that you continue to scheme for the end of the current deal to allow you to make advocate inroads into the mortgage.

Assuming that you won’t pay off the whole mortgage you can still make a scheme that will see you rapidly close in on the day when you no longer have a mortgage to deal with.

pilot THE MORTGAGE MAZE

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to advocate products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")