simonkr

What a difference a few months make. Hudson Pacific Properties (NYSE:HPP) back in October was trading close to 52-week lows, had suspended its dividend, and faced an uncertain end date with the actors strike that had broadly shuttered its studio portfolio as it teetered on the edge of violating its stringent debt covenants. The equity REIT has since staged a dramatic recovery and last declared a quarterly cash dividend of $0.05 per share, a jump from a prior suspension and $0.20 per share annualized for a 3.1% dividend yield. HPP still faces pertinent headwinds from rising office vacancies in its West Coast markets but the fourth quarter selloff was overdone with the REIT now trading hands for 6x times the midpoint of its guided FFO for 2024 of $1.00 to $1.10 per share. It’s cheap, albeit for a reason.

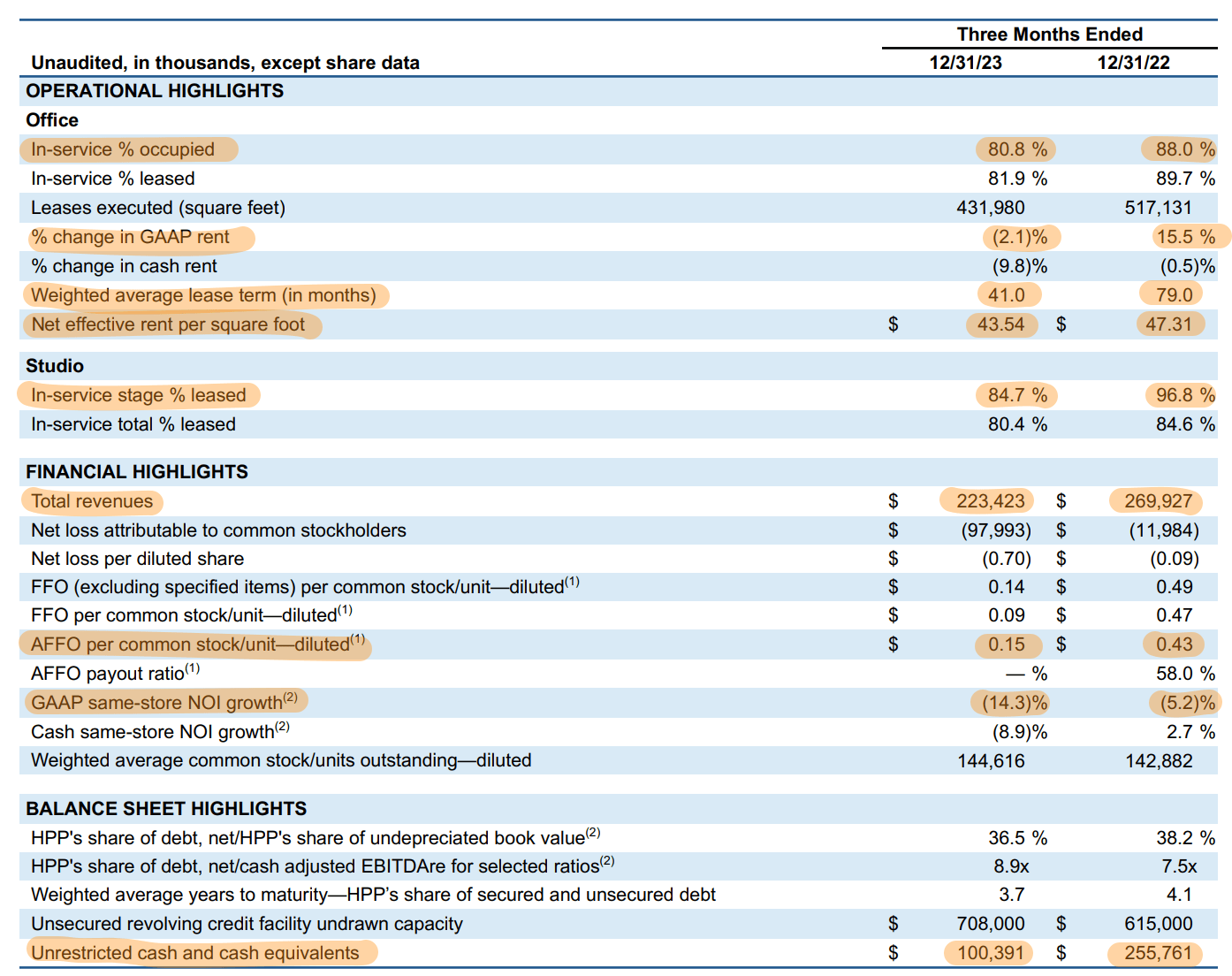

The bearish case here is that FFO will underperform as upcoming lease expirations force down an office occupancy rate of 80.8% at the end of the fiscal 2023 fourth quarter. This was a material decline from 88% in the year-ago comp. This drop was also reflected in the REIT’s studio portfolio which 84.7% occupied at the end of the fourth quarter, down from 96.8% in the year-ago comp. HPP reported fourth-quarter revenue of $223.42 million, down 17.2% over its year-ago comp and missing consensus.

Hudson Pacific Properties Fiscal 2023 Fourth Quarter Supplemental

The underlying metrics continue to move in the wrong direction with HPP’s weighted average lease term in months at 41 at the end of the fourth quarter, down from 79 months in the year-ago period. Net effective rent per square foot also dipped by $3.77 to $43.54 following GAAP rents that fell by 2.1% year-over-year. This dip was 9.8% on a cash basis and was a decline largely driven by two renewals in the Bay Area whose initial leases HPP said were signed at the top of the market.

Lease Expirations, Debt Maturities, And The Fed

Hudson Pacific Properties Fiscal 2023 Form 10-K

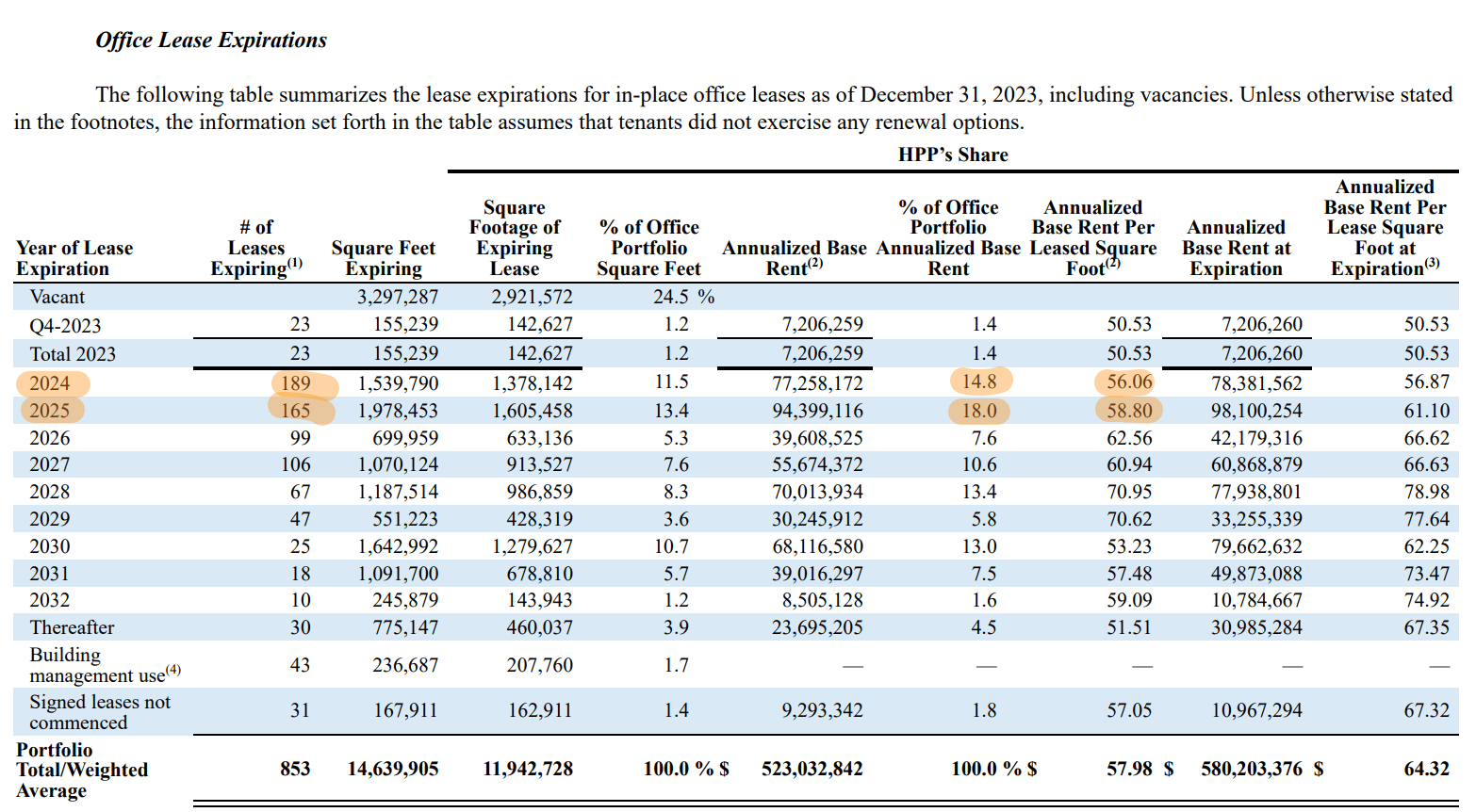

HPP’s 2024 lease expirations are heavy with 14.8% of its office annualized rent base expiring this year and 18% of the rent base expiring next year. These leases are also at markedly higher rents than its current net effective rent per square foot at $56.06 and $58.80 respectively. Hence, HPP is about to realize what should be at least a 22% decrease in rent per square foot on nearly a third of its portfolio over the next two years.

Hudson Pacific Properties Fiscal 2023 Fourth Quarter Supplemental

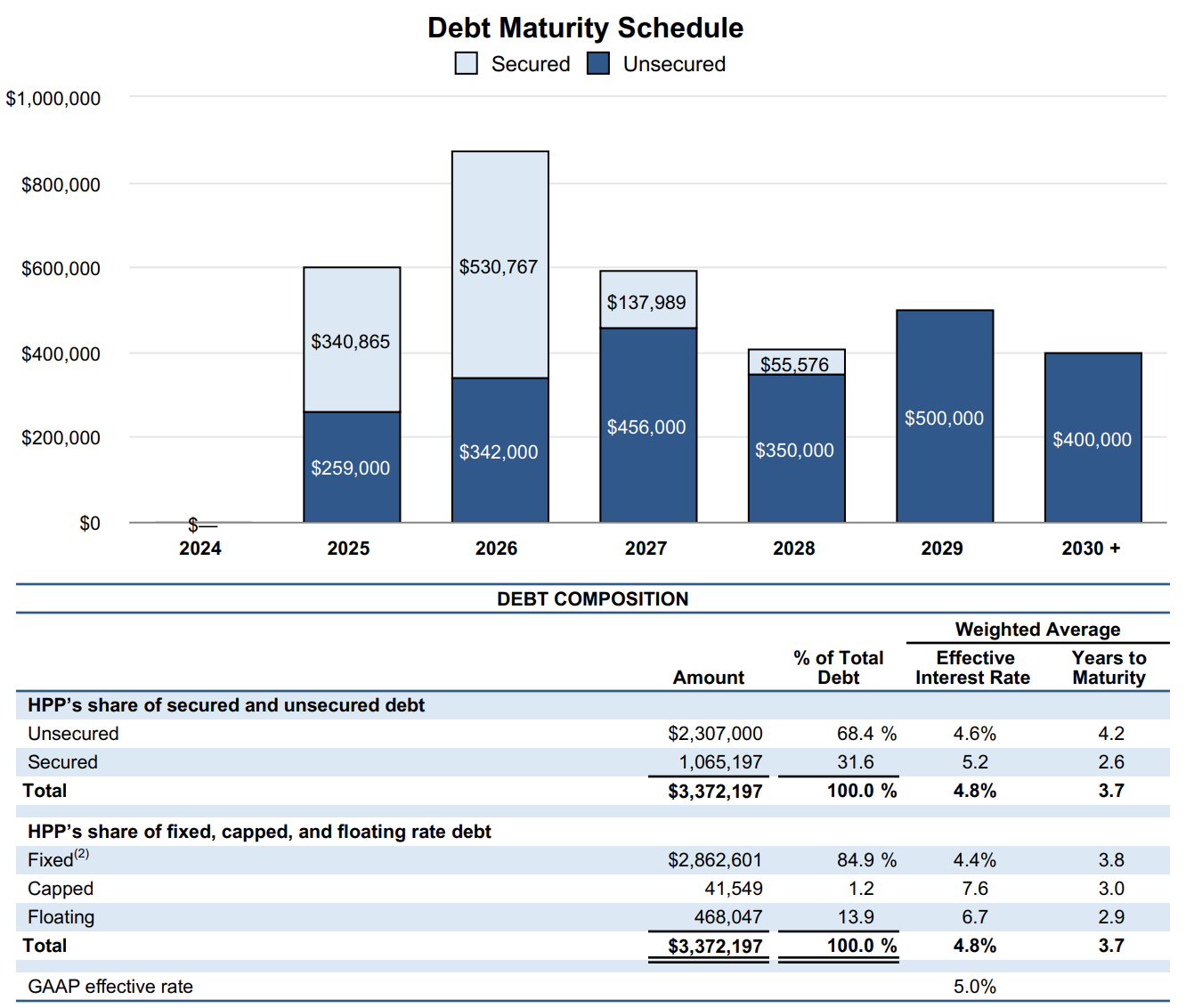

HPP faces zero debt maturities in 2024 with $600 million coming up next year. The REIT had $800 million in total liquidity at the end of the fourth quarter with $100 million formed from cash and cash equivalents and $700 million of undrawn capacity under its unsecured revolving credit facility. Critically, HPP’s lease expirations will restrict its ability to grow FFO and create positive shareholder value through the next two years. The Series C preferreds (NYSE:HPP.PR.C) have also recovered markedly from when I last covered the ticker with HPP addressing previous debt convents that threatened to disrupt its ability to pay dividends to its preferred shareholders. The next catalyst for both preferred and common shareholders is the Fed.

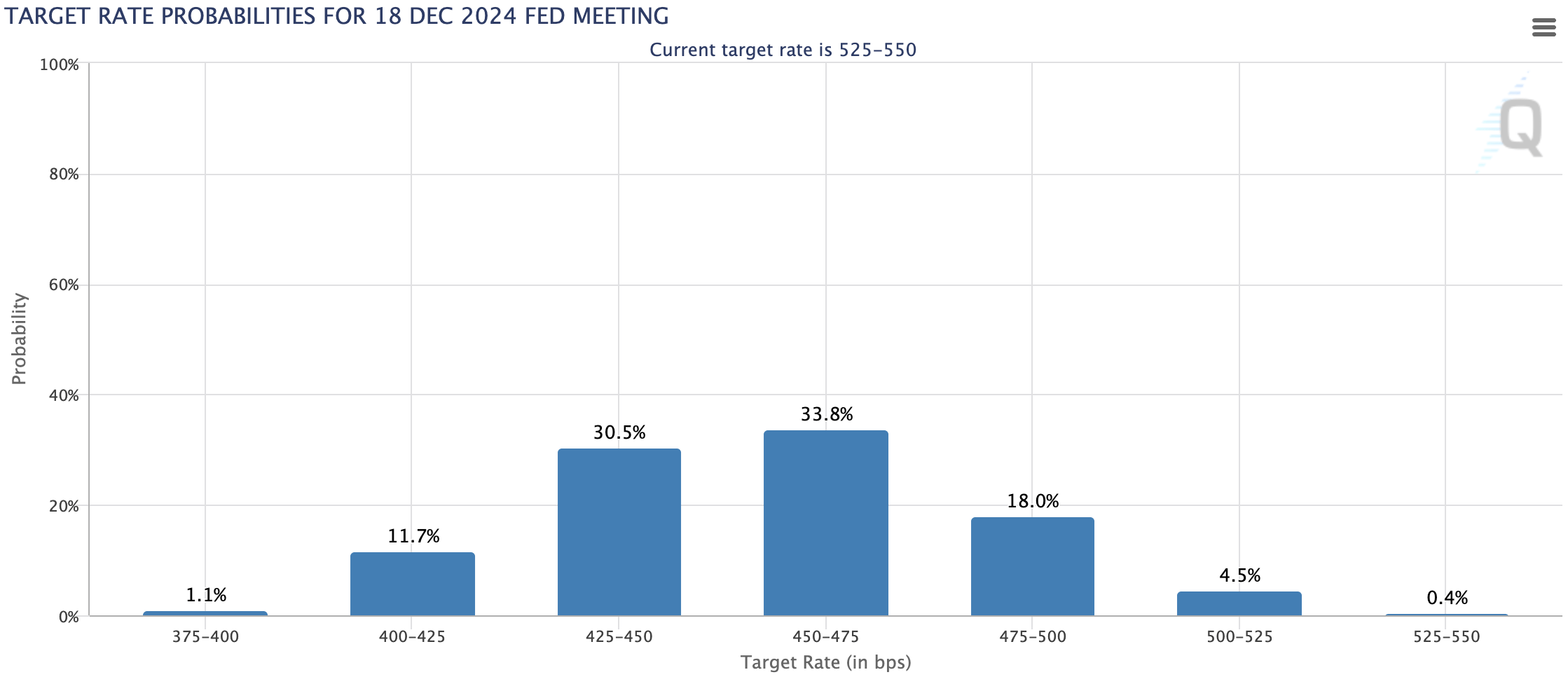

CME FedWatch Tool

The CME FedWatch tool currently places the probability of no rate cuts in 2024 at 0.4% with base market expectations being for the Fed to cut interest rates at least three times. This will likely be by 75 basis points with the Fed funds rate set to exit 2024 at 4.50% to 4.75%. For HPP and the equity REIT universe, this would form a basis for currently low valuation multiples to expand as their cost of financing goes down and capital begins a flight from money market funds back into the stock market in search of yield. Do I think HPP is a buy at its current multiple? It depends. The REIT could outperform its FFO guidance on a pick-up of currently lagging studio occupancy rates as pending rate cuts look set to bring life to a long moribund stock market for REITs. However, HPP faces structural headwinds with its front-loaded lease expiration schedule even though near-term debt maturities are covered by current liquidity.

Hudson Pacific Properties Fiscal 2023 Fourth Quarter Supplemental

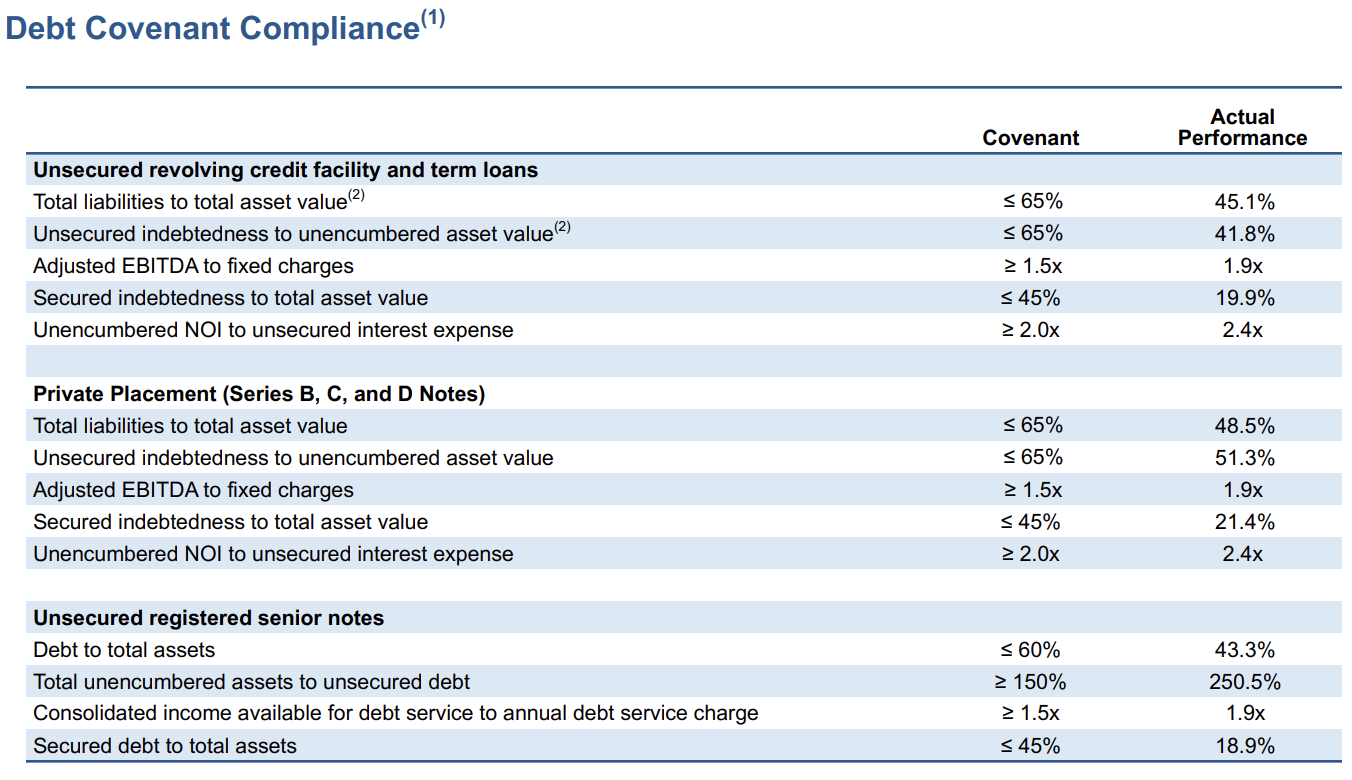

HPP’s compliance with its debt covenants has also seen material improvement from the prior quarter. Adjusted EBITDA to fixed charges and unencumbered NOI to unsecured interest expense is to watch, especially with coming headwinds from lease expirations. However, the REIT has been selling assets to bolster its balance sheet and enhance its liquidity with over $1 billion of asset sales closed in 2023. HPP should be able to navigate the continued headwinds but the pathway for the dividend to recover to its prior level is limited. This is a hold.

Q2 2024 Earnings Call Transcript")