Galeanu Mihai

Markets are continuing their recovery and shooting for another rally. In fact, the S&P 500 (SP500) gained 9% just in the last month and is up more than 20% in 2023. So, are the clouds of uncertainty and the possibility of a recession over? Well, the answer to the occurrence of a recession is not clear. The bigger question is how deep or shallow the recession will be if it arrives in 2024. Also, an even bigger question remains: What actions is the Fed going to take in 2024? How long are interest rates going to remain high? None of these questions can be answered with any degree of certainty at this time. However, we can talk in terms of probabilities. It does appear that there are more chances for the market to continue to go higher than lower in 2024; however, the positive growth will certainly not come in a straight line.

In this backdrop, a lot of investors cannot deduce if this is a good time to invest. Since no one can forecast the future direction of the market, it is best to invest in many small lots over a period of time instead of one lump sum. We believe it is not wise to keep large amounts of cash as it does no good and keeps losing its value due to inflation. So, we are going to present a portfolio here that not only promises to supply decent growth over and above the rate of inflation but is also likely to resist deep drawdowns in a recession or big correction. That’s why we call it the Sleep Well portfolio. We also call it the Near-Perfect Portfolio strategy. The portfolio can be used both for income or for pure capital compounding.

Note: NPP strategy is also part of our Marketplace service, “High-Income DIY Portfolios.” However, from time to time, we admire to share details about this strategy with a wider audience. We will supply an overview and comparison of the back-tested performance of our NPP strategy with the S&P 500. In the later section, we will supply a sample NPP 3-bucket portfolio. We also will supply guidelines on how to allocate, for example, $100,00 to an NPP strategy.

NPP (Near Perfect Portfolio) Strategy: A Combination of The Divergent Strategies:

The main features of this strategy are as follows:

- Invest nearly half of the capital in a time-tested DGI, i.e., Dividend Growth buy-and-hold portfolio. What stocks you select will depend upon many factors, such as your time in the market, income needs, and, above all, risk tolerance.

- A small portfolio of Income securities to supply high income. This will boost the income of the overall portfolio to 5% – 6%. If you do not need income, you could skip this altogether or change it as per your goals.

- A recession and correction-proof strategy that has an inbuilt hedging mechanism (without ongoing cost). Unlike cash, bonds, or Treasuries, this bucket will not be short on growth.

How to invest $100,000 today in the NPP Strategy (aka Sleep Well Portfolio)?

If you are looking to invest a large sum in any investment, especially in the stock market, it is natural to have some doubts about the timing. There are some questions that you are going to ask yourself:

- Is it the right time to invest in the market?

- Is the market overvalued or undervalued?

- What if the market takes a deep dive in the near future?

- Is it better to invest in one go or gradually over a period of time?

- How do you diversify, and which stocks do you invest in?

Obviously, it is not easy or straightforward to answer all these questions. Also, the answers will vary based on the individual situations.

However, what we are going to supply here is a roadmap of what strategies you could deploy to safeguard your investments while ensuring that your capital earns you a decent amount of income and growth over time. The strategy we suggest is a multi-bucket portfolio. We will also suggest allocations to different buckets; however, you should adjust those allocations according to your situation, goals, and needs.

Bucket 1: DGI Bucket (Allocation – 40% – 50% of the assets)

Bucket 2: Rotational Bucket (Allocation – 35% – 45% of the asset)

Bucket 3: CEF High-Income Bucket (Allocation – 15% -25% of the assets).

Alternate Bucket 3: Writing Options using Covered-CALLs or Cash-secured PUTs (to produce 10% income).

Note: We are not going to cover the details of “Alternate Bucket 3” in this article, as it would demand its own separate article. However, for folks who are interested in knowing more about this, please follow our monthly article on Options. Here is the link to our most recent article.

Bucket-1: DGI-Core

The goals of the DGI Bucket are simple enough. They include a dividend income of 3% (or higher) and total returns in line with the broader market. Also, this bucket should target lower volatility, roughly 2/3rd of the broader market.

Dividend ETFs Option:

Let’s assume you are a passive investor and do not have the time or inclination to pick individual stocks. In that case, dividend-focused ETFs are your best options. In one single stroke, they can supply you with wide enough diversification. However, we believe you should select at least three individual ETFs to supply you with much better diversification and flexibility.

One of our favorites in dividend ETFs is Schwab U.S. Dividend Equity ETF (SCHD). We also admire Vanguard dividend ETFs, VYM, and VIG. All three have very low expense ratios and, together, can supply very decent diversification, yield, and growth. The only negative here will be some duplication in the individual holdings of three ETFs.

- Schwab U.S. Dividend Equity ETF (SCHD)

- Vanguard High Dividend Fund ETF (VYM)

- Vanguard Dividend Appreciation Fund ETF (VIG)

Table 1:

|

ETF symbol |

ETF Name |

Exp/ fee |

Dividend Yield |

No of holdings |

10-Year CAGR* |

|

SCHD |

Schwab U.S. Dividend Equity ETF |

0.06% |

3.67% |

104 |

10.77% |

|

VYM |

Vanguard High Dividend Fund ETF |

0.06% |

3.11% |

455 |

9.21% |

|

VIG |

Vanguard Dividend Appreciation Fund |

0.06% |

1.91% |

317 |

10.62% |

Dividend Stocks portfolio:

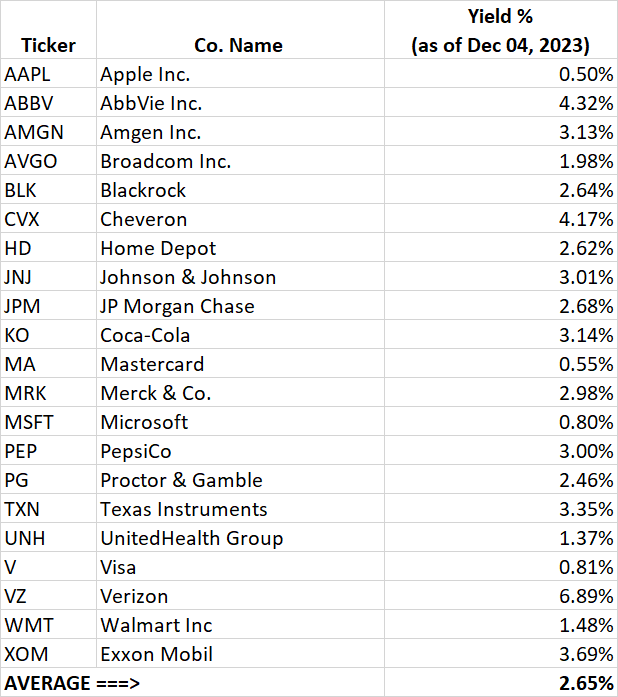

If you are an active investor and admire to pick and hold individual stocks for long durations, then it is a much better option to form a portfolio of individual stocks. The process is not complicated, and there could be many ways to go about it. We are going to supply a sample portfolio filled with solid, blue-chip dividend stocks, especially the ones that have a record of paying and growing dividends for the last five years.

What if we take the top 10 holdings of the three ETFs mentioned in the prior section and weed out any duplicates? We just did that and were left with 21 names after removing nine duplicates.

Duplicates among three ETFs (Top 10 holdings): ABBV, AVGO (3 times), HD, JNJ, JPM, MRK, PG, XOM.

This portfolio of 21 names is presented below:

Portfolio of 21 Stocks:

Apple (AAPL) AbbVie (ABBV), Amgen (AMGN), Broadcom (AVGO), BlackRock (BLK), Chevron (CVX), Home Depot (HD), Johnson & Johnson (JNJ), JPMorgan Chase (JPM), Coca-Cola (KO), Mastercard (MA), Merck (MRK), Microsoft Corp (MSFT), PepsiCo, Inc. (PEP), Procter & Gamble (PG), Texas Instruments (TXN),, UnitedHealth Group (UNH), Visa (V), Verizon Communications (VZ), Walmart (WMT), Exxon Mobil (XOM).

Table-2:

Author

Bucket-2: Rotational Bucket

This bucket is our hedging bucket. But it is not short on growth either; in fact, it is the opposite. So, why do we need a hedging mechanism? Well, we always need to protect our capital from deep drawdowns. If a portfolio loses 50% in a deep recession, it will need to recover by 100% just to get even with previous levels, and this can take a long time. Investors who actually experienced the 2008-2009 (or the dot com bubble) attain how long it can take to recover. Moreover, some folks do even worse as they end up selling at the worst time and don’t get back until it is quite late in the game.

So, hedging is very important to limit your losses in the case of a deep drawdown. But, most hedging mechanisms are expensive and have an ongoing cost that must be paid that cuts into the growth of your portfolio. That’s why we suggest a Rotational portfolio to protect you from the downside while providing market-matching or market-beating performance. The best part is that it has no ongoing cost. The only downside is that it is an active portfolio and requires regular swapping of certain securities. The usual frequency of trading is on a monthly basis. The good thing is there are usually no trading costs/commissions these days.

The goals of this bucket are:

- Limited drawdowns and preserving capital

- Decent to high growth

- supply sustainable income that can be withdrawn without harming the long-term growth of the portfolio.

Note: Since Rotation strategies involve frequent trading, they work best inside a tax-deferred account, admire an IRA account.

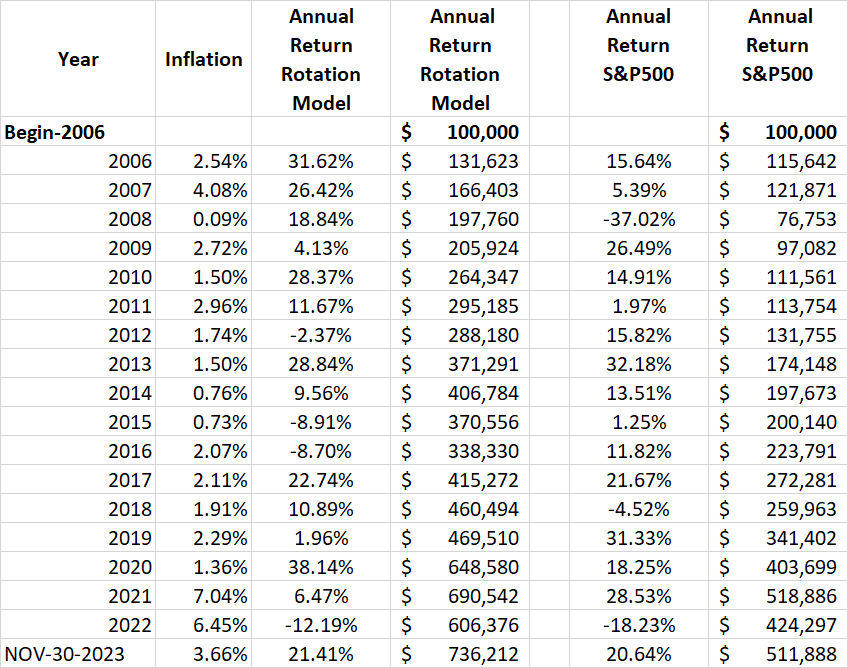

Rotation Strategy – Multi-Asset Strategy:

In a Rotation strategy, the first step is to select a pool of securities that are likely to perform in variance to each other under different market conditions. So, in this case, we select three (or four) securities from different asset classes. In our example, these are high-growth stock index, gold, and Treasuries. In the second option of this model, we will also include CASH as an asset class. Now, every month, we will contrast the performance of these securities over a certain time -period (in this example, three months) and select only one top-performing security for investment for the next month. The performance is taken from “total returns,” including any distributions. Three securities that make up our pool are:

In the second option, we will also include CASH (same as money-market fund).

Presented below is the back-tested performance comparison of the model portfolio in comparison with the S&P500. The comparison period is from Jan. 2006 until Nov. 30th2023, spanning almost 18 years.

Table-3:

Author

Chart-1:

Author

Option-2:

Highly conservative investors could add another asset class, Cash (or Money market fund), to the list of securities and select any two (instead of just one) top-performing securities for investment every month. This will help bring down the drawdowns but will also result in slightly lower returns. Here is the comparison of two options (from year 2006 to Nov 2023):

Table-3B:

|

QQQ-GLD-TLT Option |

QQQ-GLD-TLT-Cash Option |

S&P500 |

|

|

Pool of Securities |

Three |

Four |

Index ETF |

|

Number of securities being held every month |

ONE (Top Performing |

TWO (Top performing) |

Buy-and-hold |

|

CAGR (From Jan. 2006 – Nov 2023) |

11.79% |

10.69% |

9.54% |

|

Max. Drawdown |

-25.44% |

-14.99% |

-50.97% |

|

Best year (return) |

38.14% |

31.19% |

32.18% |

|

Worst year (return) |

-12.19% |

-8.00% |

-37.02% |

|

Stock Market Co-relation |

0.30 |

0.30 |

1.00 |

Bucket-3: CEF High Income Bucket

Our long-time readers know that we admire to include this INCOME-oriented bucket in the mix. However, it is not for everyone. If you are relatively young and have a ensure career ahead of you, you do not need income; you could just skip this. But if you are retired or going to retire in a few years, and income is important for your peace of mind, then this bucket is for you. In your retirement, the last thing you want to do is make guesswork every few months as to which stocks to sell to raise income. It is prone to emotions and mistakes.

Goals:

- 8% (or higher) reliable income.

- 10% plus total returns over the long term.

The biggest risk from this bucket is that it may not supply much growth over and above 8% income. But this can be mitigated to some extent by re-investing roughly 25% of the income back into the funds.

Note: Please note that many of these instruments involve leverage, and leverage can guide to higher risk and volatility.

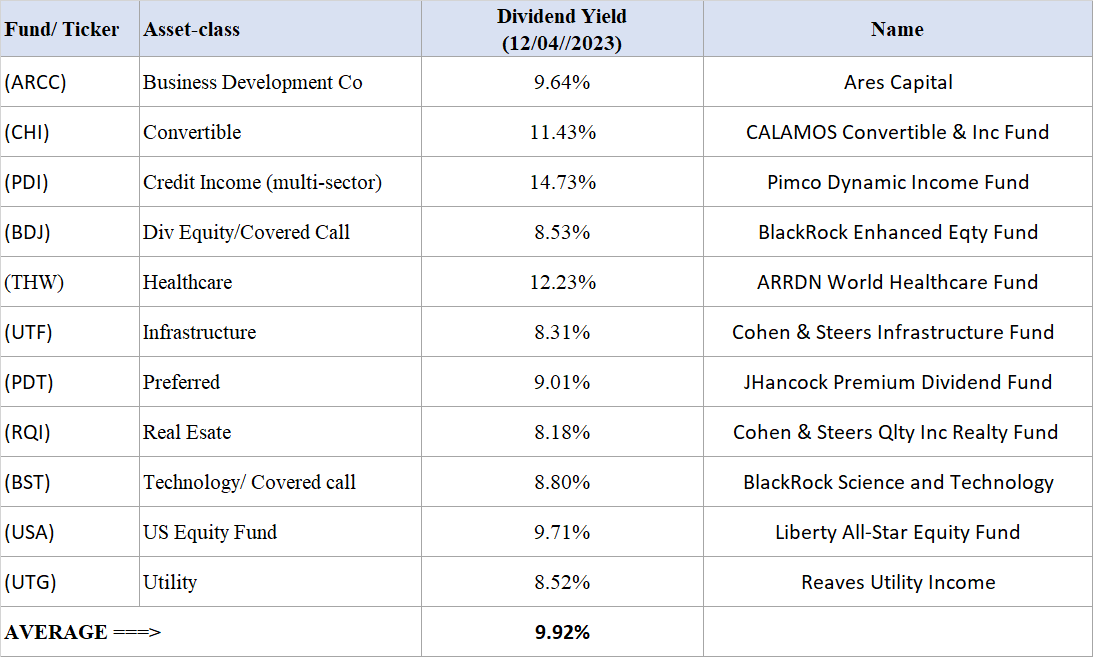

This bucket could invest in all types of high-income investment securities while making sure that there is enough diversification in terms of asset class.

- CEFs (Closed-end funds),

- REITs (Real Estate Investment Trusts),

- mREITs (Mortgage REITs),

- BDCs (Business Development Companies), and

- MLPs (Master Limited Partnerships).

Though some investors admire to time the entry and exit in the CEFs, our focus in this article is to select one fund from every asset class that is also one of the best funds in its asset class. It is recommended that we build our positions in multiple lots (maybe three lots) and not be overly concerned about the entry price for the first lot. For the subsequent lots, you could scrutinize the price, discounts, and other factors. That said, at this point, the CEFs are not overvalued in general. Sure, they were much better priced a couple of months ago. In our list below, there are 10 CEFs and one BDC (Business Dev Co).

The funds/securities in order of asset class are: (ARCC), (CHI), (PDI), (BDJ), (THW), (UTF), (PDT), (RQI), (BST), (USA), (UTG).

Table-4:

Author

Multi-basket NPP Strategy Performance during the last 18 years:

We will combine the performance of the above three buckets during the past 18 years. The past 18 years did include many corrections, a financial crisis and a pandemic (kind we had not seen in many decades), and a rising interest rate regime of the last two years. You can see how different baskets can counterbalance each other in times of crisis. A comparison with the S&P500 is also provided.

To supply some perspective, we will now contrast the performance and drawdowns of the recent (and not-so-recent) corrections and recessions. Before we do that, we will make some changes to the DGI portfolio. We know a few stocks in the DGI portfolio had an outsized performance in the last 10 years. They are AAPL, MA, V, and AVGO. So, we removed these four stocks to avoid any bias and see how the rest of them performed. It is quite obvious that the rest of the stocks were already established DGI stocks (not growth stocks) back in 2006.

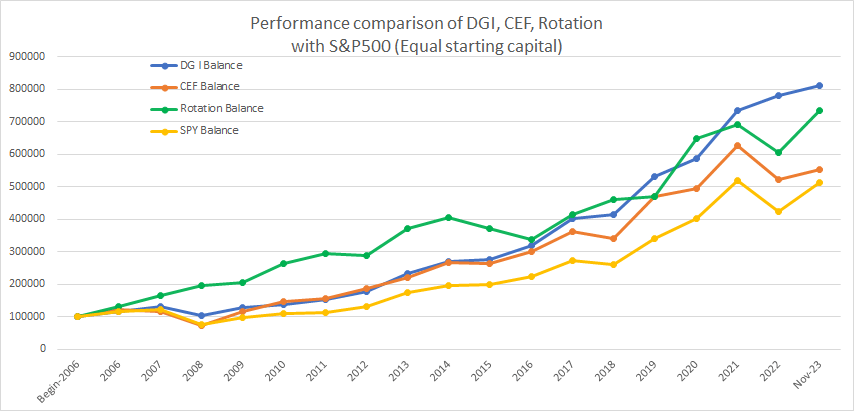

Here is the performance of our three buckets separately and the S&P500, assuming equal amounts were invested in all of them, starting 2006.

Chart 2:

Author

As you can see, from 2006 until 2015, the Rotation bucket did very well; however, DGI performed better between 2016 and 2022. The CEF bucket performed almost in sync with the S&P500 but a percentage point higher than the S&P500. The point we are trying to make is that three baskets are going to perform differently during different time spans and, as a whole, supply lower volatility and drawdowns and better overall returns.

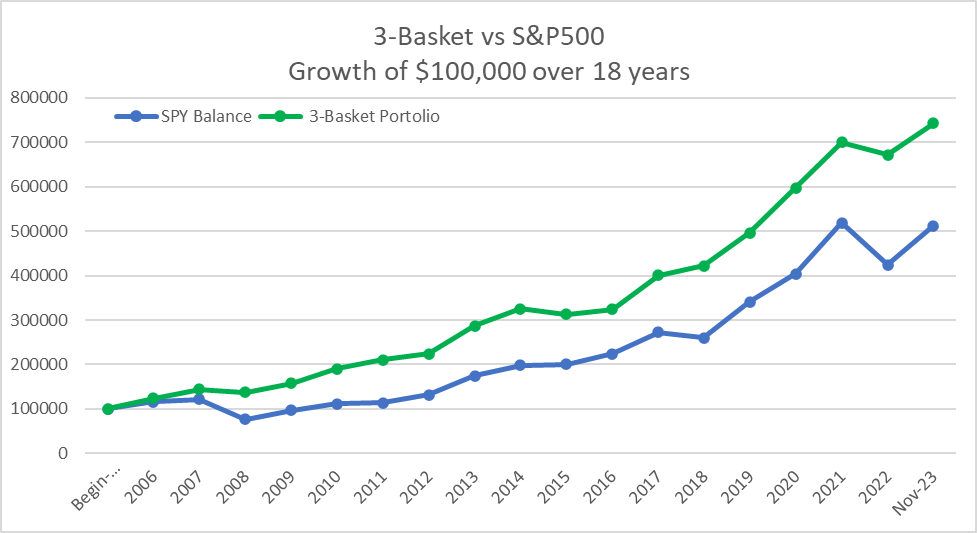

Now, let’s see the combined performance of 3-Buckets as compared to the S&P500 for the entire 18-year period (excluding AAPL, AVGO, MA, and V from the DGI bucket).

Chart 3:

Author

** The combined 3-Basket NPP performance assumes a 45% allocation to DGI, 40% to Rotation, and 15% to a CEF portfolio.

Concluding Thoughts

As usual, the market is giving contradictory signals. On the one hand, we have just witnessed a mini-rally this past month, and there is a lot of talk of the rally to continue in 2024. The bull case makes some sense based on the fact that the economy has shown resilience in spite of the high-interest rates for some time now. Also, we are closer to the beginning of rate cuts or at least no advance rate increases in 2024. Even though the Fed is still talking hawkish, if history is any indication, they can turn dovish overnight if they see any trouble ahead. All that said, not everything is that rosy. It is also possible that the Fed can overshoot and keep the rates high for too long and end the economy in the process. advance, the geo-political situation in the world is certainly not at its best. So, no wonder predictions are just that, predictions.

That’s why it is important to have an investment approach that can supply comfort in knowing that it can handle all kinds of situations with relative calmness. In this article, we have presented a multi-basket approach that is highly diversified and reasonably conservative, which would supply lower volatility, lower drawdowns, and decent growth. That said, the strategy is not immune to deep corrections or recessions but will still endeavor to supply half the volatility and drawdowns.

Q2 2024 Earnings Call Transcript")