With money market interest rates so high, every day you delay closing escrow is one more day of free interest income. You could feasibly extend your escrow period so long that the extra interest income you earn pays for all your closing costs and then some.

I’ve argued why buying a home with contingencies is like getting a temporary free call option. By extending escrow, you are making that temporary free call option more valuable because you gain more time.

Let me illustrate using an example why extending a home escrow period can be beneficial. We’ll then talk about all the other reasons why you may want to delay closing escrow.

Get Your Closing Cost Paid For By Delaying Escrow Closing

If you buy a home, even with all cash, there will still be closing costs. These fees include a title fee, settlement fee, notary fee, and recording service fee. Along with stubbornly high commission rates, closing costs are one of the main reasons why there are fewer real estate transactions.

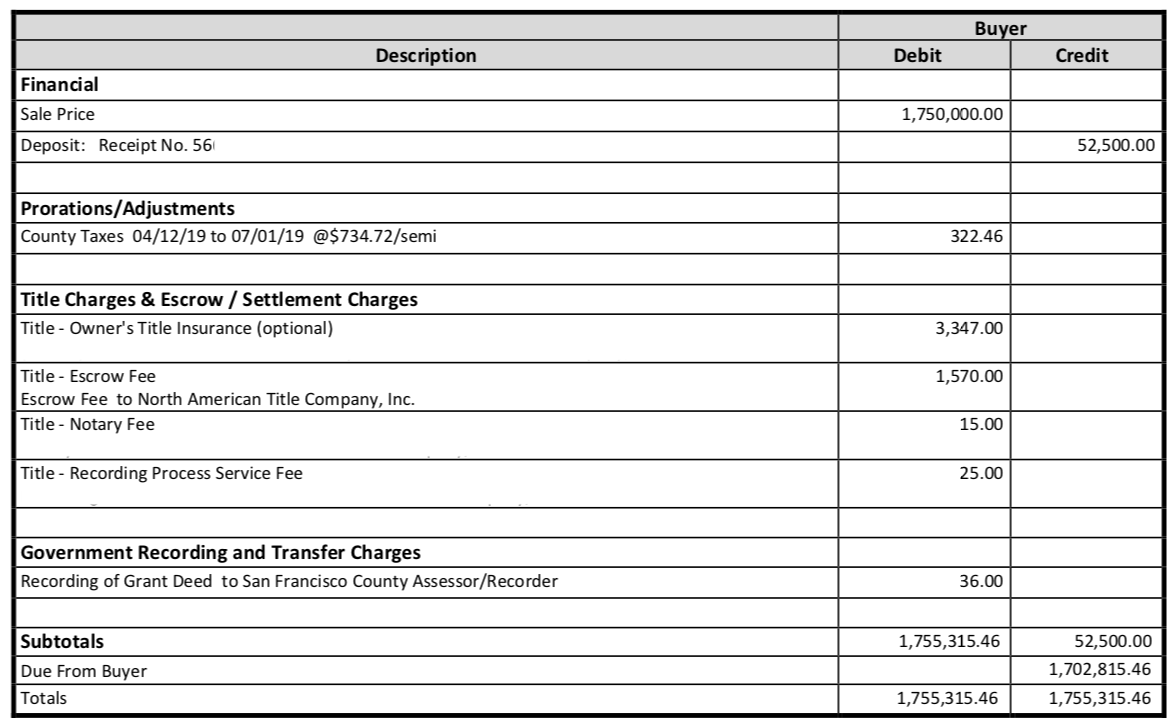

See a sample home closing cost fee table below for a home that was purchased for $1,750,000. Look in the Debit column.

The total closing fees this homebuyer has to pay are $5,315.45. However, if the homebuyer were to delay the close of escrow by just one month, they could get all closing costs covered for free.

Let’s say the buyer is able to pay all cash for the $1,750,000 home. A 5% return on $1,750,000 equals $87,500 a year. You would be able to get 5% today by just keeping the $1,750,000 in a money market fund.

Therefore, holding $1,750,000 for an extra month in a money market fund will earn the homeowner $7,291. This risk-free income after tax is more than enough to cover the $5,315.45 in closing costs.

Even if the buyer puts the standard 20%, or $300,000 down, they would earn $1,250 in interest income by delaying escrow for one month. Not bad.

Most Common Reasons For Delaying Escrow Closing

Besides earning more risk-free income, here are more reasons for delaying closing escrow:

- Your lender isn’t finished with their underwriting process and needs more documents

- Appraisal issues. Closing dates will get pushed back if the property is not appraised for a similar amount as the offer. When this happens, the buyer and seller may need to come to a new agreement for the deal to continue or for the lender to proceed.

- Title issues may delay closing escrow. Properties with past liens will likely take a while to resolve.

- Issues arising during the final walkthrough. The final walkthrough is often scheduled for the day before or even the actual day of closing. So, if any of these things are out of order it will most certainly delay the closing of escrow.

Less Common Reasons To Extend The Close Of Home Escrow

Now that we’ve gone through the most common reasons for escrow closing delays, let’s look at less common reasons why a homebuyer might want to extend escrow.

- You’re getting cold feet and are scared whether you’re making the right move

- The Toto washlets you’ve ordered are on backorder

- You have a family emergency and need to travel for a few weeks

- Work requires you to fly internationally last minute

- You want to time the close closer to when the furniture will arrive

- It’s taking you longer than expected to find the right tenants to rent out your current home

As you can see from my list above, there are a number of reasons you may want to delay the closing of escrow. The next section will share how.

Strategies On How To Extend Your Home Closing Period

Getting a seller to agree to extend your home closing period may not be easy. Most home sellers want to close ASAP because they’d like to use the funds for something else. Every day the home is in escrow means more carrying costs, sometimes lost rental income, and lost investment income.

As a homebuyer, you want to be as thorough as possible during the escrow period to ensure the home is in the best shape possible before buying it. Once you buy it, all the responsibility and costs are on you. Honorable sellers will still fix surprise problems that arise after a home purchase, especially if the real estate agent wants to protect their reputation. But there is no guarantee.

Therefore, in general, the longer the contingency and escrow period, the better for the buyer.

Let me share some nice ways and some devious ways to delay closing. One of the consistent themes for all these strategies is to always be respectful and cordial with the seller and listing agent. Otherwise, reputations will be damaged and lawyers might get involved.

1) Blame the lender

If you require a mortgage to buy a home, you will develop a relationship with your mortgage officer. This is your relationship, not your agent’s, not the listing agent’s, and not the seller’s relationship.

The mortgage officer also wants to close the deal ASAP in order to get paid. However, you can drag your feet in delivering the ridiculous number of documents that they require to underwrite your loan.

You can also extend your mortgage lock period or relock your mortgage if mortgage rates drop. There might be a fee to do this, so double-check.

You could ask the mortgage officer to delay underwriting your mortgage because you want to delay closing escrow for whatever reason. Given they want your business, they should comply.

Blaming your lender for needing to extend the escrow period, even after removing financing contingency works. This is the classic good cop, bad cop strategy.

2) Slow your response times or turn into a ghost

You can also delay the close of escrow by being unresponsive. Instead of responding to emails within four hours, extend the response time to two days, four days, or one week. The longer you drag out your response times, the slower the entire escrow process will go.

Title officer to homebuyer: Are you free tomorrow between 10 am and 12 noon for the notary?

You, who doesn’t respond for three days: I’m not free then, but am free the following week at 10 am.

Your slow response will frustrate the heck out of everyone, which is why you can’t be slow at responding forever. You will need to pick and choose when to delay your correspondence. If you want the house, you don’t want the seller to cancel escrow and return your earnest money deposit.

If things get testy, the seller could get a lawyer to write the buyer a “letter to perform.” It is essentially a threat to continue the escrow process or risk losing the earnest money deposit.

3) Say you’ve got a personal matter

Personal matters are off limits for inquiring. As soon as you say you have a “personal matter” you’re dealing with, all parties involved will have to accept the delay. Involved parties don’t want to risk offending you and coming across as insensitive, if something really bad is going on.

We all have personal matters to deal with. As a result, we are all more empathetic when someone else is dealing with a personal matter.

4) Offer a good faith deposit to the title company

Let’s say you’re supposed to close escrow next week but need one more week for whatever reason. To keep the seller happy after requesting to delay closing, you can send part of your down payment to escrow as a show of good faith.

For example, let’s say you owed $500,000 at closing. You could wire $100,000 to the title company and have them notify the seller. Given you’ve removed contingencies already, the seller will feel more confident knowing that in the worst case, he will be able to legally collect the 3% earnest money deposit plus the $100,000 wire if the deal falls through.

If you want to buy the home, you need to find a way to keep the seller from pulling the deal due to your non-performance. Delays are common in many escrow transactions. But if you delay too much, you run the risk of losing the home.

5) Wire addendum money

As part of your home purchase agreement, you may have offered money for furniture or other home-related items. If so, to make up for the escrow closing delay, you can simply wire the money directly to the seller as a show of good faith.

For example, let’s say a home is listed for $1,100,000. You offer $1,090,000 for the house and $10,000 for furniture on the side and the seller accepts. When it’s time to extend escrow, you can send the seller $10,000 for the furniture as a show of good faith. You can tell the seller to keep the money if the house sale falls through.

Obviously, sending addendum money outside of title puts the buyer’s money at risk. Hence, you need records (don’t send cash) and you should minimize the addendum money amount.

The Mind Of The Home Seller

Selling a home is stressful, especially if you have a slow buyer. During the escrow period, anything can and will happen.

From the seller’s point of view, a delay is better than a buyer who backs out. Therefore, a delay of a couple of weeks, or even a couple of months is probably worth it. If the seller feels confident the buyer will eventually perform, then continuing with the escrow period is the right call.

If there is a home inspection contingency, then a seller may actually be the reason for delaying escrow because they have to fix some things. For example, a part is on backorder, making delaying the close of escrow understandable.

During the pandemic, for example, different types of paint were unavailable for 6-9 months. I know because I checked when I was remodeling a house. An intense winter storm shut down Texas, where much of America’s paint supply and factories reside.

The Seller Can Delay Escrow As Well

If the seller delays escrow, then the buyer actually has more leeway to delay the close of escrow as well. Now we’re talking a double delay!

For example, let’s say the seller needs to delay the close of escrow by three weeks because the custom wallpaper that was peeling is on backorder. This delay could actually be a great inconvenience to the buyer who had hoped to move into the house before the start of the school year.

If the buyer wants, they have the leeway to delay the close of escrow by three weeks as well. It’s only fair. The seller will probably acquiesce if they don’t have strong demand from other potential buyers.

A Notice To Perform Letter

There may come a point where the seller is so frustrated with your escrow delay tactics that they hire a lawyer to serve you a “notice to perform” letter. The letter requires the homebuyer to acknowledge receipt within 48 hours.

A notice to perform letter’s purpose is to motivate the homebuyer to follow through with their contractual responsibilities, such as inspecting the home, obtaining home insurance, and securing financing. The letter is essentially a warning that if the homebuyer doesn’t make progress, the homeseller can legally keep the earnest money deposit and cancel the purchase contract.

A notice to perform letter can also be sent by the homebuyer to the homeseller who delays the escrow process unreasonably long. For example, if the homeseller was supposed to fix some rusted water pipes within three weeks, but you’re now in the sixth week and the pipes have still not been replaced, the homebuyer could send a notice to perform letter.

Once a notice to perform letter is sent, both parties typically have 1-4 more weeks to fulfill their contractual duties before the other party can cancel the purchase contract and keep the earnest money deposit. If the purchase contract is cancelled, litigation could be the next step to resolve the dispute.

Once a letter to perform is sent, both parties can delay escrow by another 1 – 4 weeks. After this time period, chances are high the contract will be cancelled and the earnest money deposit will be lost by the homebuyer. If this is happens, litigation could be the next step.

I highly advise against reaching the litigation stage. Try to work out compromises to minimize economic loss.

Win Back As Much Time As Possible Before Buying A Home

Before buying a home, you need to feel absolutely comfortable before moving forward. Otherwise, you might end up with buyer’s remorse.

A home seller is unlikely to cancel escrow on you just because you kindly ask for an extension. The deeper you get into the escrow period, the more vested the seller is in selling you their home.

A homebuyer can probably get a one or two-week extension just by asking without much pushback. If a homebuyer wants a greater than a two-week extension, then offer to send part of the down payment to the escrow company or sending addendum money will help ease the seller’s vexation.

Unless there is already some huge dispute, natural disaster, or death in the family, a one-month extension is probably around the limit a homebuyer can ask for. After one month, the seller will start to have serious reservations about continuing escrow. And you know what? This may be exactly what you want!

Reader Questions And Suggestions

Have you ever delayed escrow? If so, what was the reason? Did you ever try to delay escrow and the seller refused? If so, what happened?

To invest in real estate more strategically, take a look at Fundrise. Fundrise primarily invests in residential and industrial properties in the Sunbelt, where valuations are lower and yields are higher. Diversify your real estate portfolio and earn returns passively.

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Please share, rate, and review!

Join 60,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Q2 2024 Earnings Call Transcript")