The cost of living crisis, private renting and frozen income thresholds mean young people are facing a significant financial burden.

Add in student loan repayments and graduates face what is essentially an extra 9 per cent tax on their income, which could stay with them for decades.

Many graduates bemoan checking their balance only to see it has increased by thousands of pounds and their repayments not even making a dent in the accrued interest.

Payback time: Graduates start to repay their loan at different thresholds depending on when they started university

This is especially true for taxpayers who went to university after 2012, when fees tripled to £9,000 per academic year.

Some have suggested raising the threshold at which graduates start to pay their student loan back, or cutting the interest rates added to the loan.

But there doesn’t seem to be much political appetite to change the current student loan system, meaning many taxpayers face an extra tax through their working life.

We look at how much you might expect to pay per month, depending on when you started university, and how long it will take to clear the debt.

When do students start paying back their loans?

Unlike a standard loan, the system acts more like a graduate tax and increases the more you earn. What and how you pay it back depends which of the five different repayment plans you’re on.

Those who started university before 1 September 2012 will be on Plan 1 and start repaying their loan once they earn over £22,015 a year.

Those on Plan 2, who went to university between 1 September 2012 and 31 July 2023, will start to repay their loan once their income is over £27,295, and those who started after 1 September 2023 are on Plan 5 and start to repay when they earn over £25,000.

In Scotland, students are on Plan 4 and will start to pay back the loan once earning over £27,660 a year.

All graduates, regardless of the plan they’re on, pay 9 per cent of their income over the threshold, while postgraduate loans pay 6 per cent.

For basic rate taxpayers, it means a marginal tax rate of 39 per cent.

The level of interest applied to the loan has been a controversial subject, with many graduates not even making a dent in the accrued interest each month.

Typically the applied interest has been based on the Retail Price Index rate of inflation (RPI) rather than the Consumer Price Index (CPI), which is more commonly used.

When RPI jumped to 13.5 per cent in March 2023, the Government introduced a cap of 7.6 per cent for all loans.

The current level of interest on each plan is:

- 7.6% on the postgraduate loan plan

What do you have to pay back per month?

When the Government changed the rules on repaying loans with the introduction of Plan 2, they also raised the threshold at which graduates pay them back.

Proponents of the scheme said it meant people would only pay back when they earned over a comfortable salary.

However this remains frozen at £27,295 a year, meaning that if wages grow in line with inflation more people will be paying back their loan.

The Government’s student loan figures suggest the forecast average debt among the cohort of borrowers who started their course in 2022/23 is £45,600, when they complete their course.

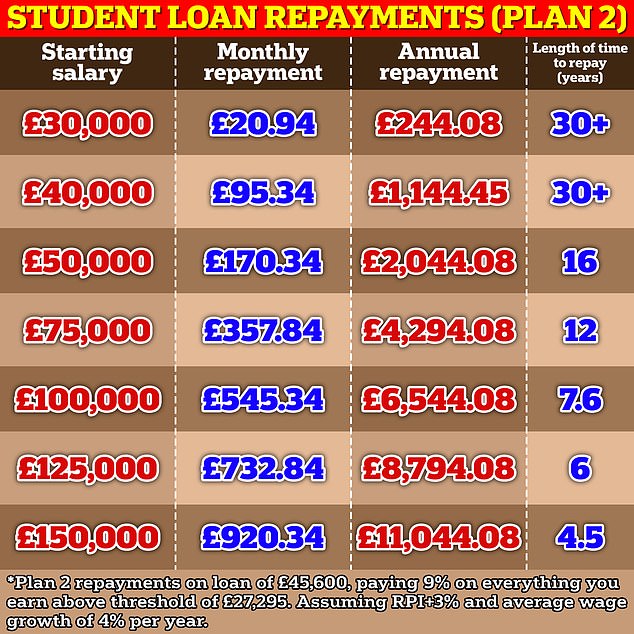

An analysis of repayments based on the average debt, paying 9 per cent on everything earned above the threshold and assuming interest at RPI + 3 per cent and wage growth of 4 per cent per year, shows how much graduates will pay back per month.

Those earning over £30,000 will pay back £244.08, or £20.34 a month. This rises to £95.34 a week, or £1,144.45 a year, for those on £40,000 a year, according to an analysis by wealth management firm Quilter.

This nearly doubles to £170.34 for those making £50,000 a year. Six figure earners will pay back £545.34, or £6,544.08 a year, rising to £920.34 a week, or £11,044.08 annually, for those on £150,000.

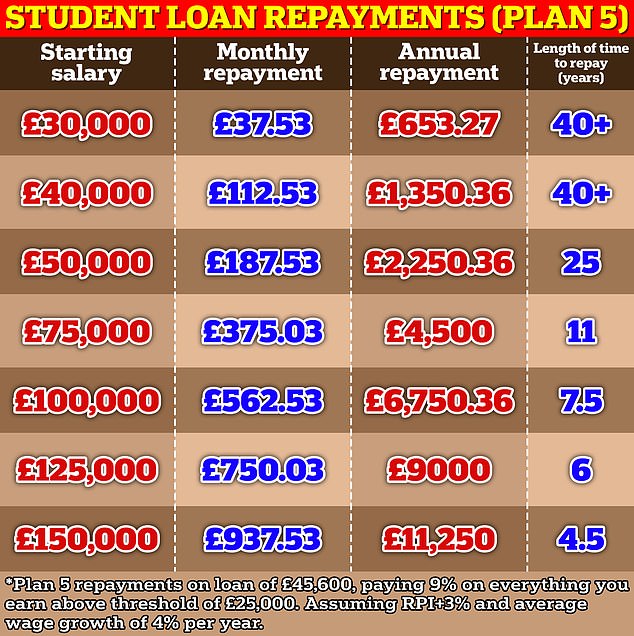

The monthly repayments are even higher for lower earners on Plan 5, with those earning £30,000 paying back £37.53 a month and £112.53 for those on £40,000.

However, higher earners won’t pay back much more than those on Plan 2.

Graduates on £75,000 will pay £375.03 a month, compared to £357.84 for those on Plan 2, while those earning £100,000 will pay back £562.53 a month compared to £545.34 on Plan 2.

> We explain whether it is worth saving to pay back your loan early

How long will it take to pay back your student loan?

The prospect of paying what could be hundreds of pounds a month for decades in student loans is not a pleasant one.

So how long would it take you to clear the mountain of debt?

Those on Plan 2 have their loans wiped after 30 years, and Quilter’s analysis shows that graduates earning £30,000 and £40,000 are unlikely to pay back the full loan amount.

Similarly graduates earning the same salaries on Plan 5, which are wiped after 40 years, are set to spend the majority of their working life paying back their loan.

Those earning £50,000 will spend 26 years on Plan 2, and 25 years on Plan 5 paying back their loan, which falls dramatically to 12 and 11 years for those on £75,000.

While unlikely, those earning £150,000 straight out of university will spend just 4.5 years of their working life repaying their student debt on both Plan 2 and 5.

Of course if you earn more or your circumstances change, this could cut or extend the overall time period – but it provides a good snapshot of the general repayment period for each salary.

Because it is based on the amount you earn, it will take longer to pay off the loan as more interest accrues over time.

Tom Allingham, spokesperson for Save the Student said: ‘According to our latest National Student Money Survey, 67 per cent of respondents worry about having to repay their Student Loan.

‘This figure is up on the previous year, correlating with the introduction of the regressive Plan 5 repayment plan which benefits the highest-earning grads, and increases lifetime repayments for their low- and middle-earning peers.

‘But as daunting as some of the repayment figures may seem, it is worth remembering that they should still be fairly manageable, the debt will eventually be cancelled, and none of it will have any impact on your credit score.

‘Nonetheless, these changes are regressive and we’d encourage the Government to reconsider how the new plan disproportionately and negatively impacts low- and middle-earning graduates.’

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")