Looks whose back to air his opinions again. s_derevianko/iStock via Getty Images

Today’s lesson on dividends is going to focus on the impact of floating rate shares. I’m interested in both fixed-rate and fixed-to-floating shares. Sure, there are common shares also. But I’m starting this article with the preferred shares.

For many income investors, preferred shares are a better way to use the sector. You can use fixed-rate preferred shares to lock in a pretty high yield for many years (if you get called, it’s a huge capital gain). Or you can use fixed-to-floating shares to generate a much higher yield in the near future. However, this technique generally means you won’t have nearly as much upside.

If you are firmly convinced that short-term rates will not decrease materially, then you’re going to want the fixed-to-floating shares.

If you’re interested in playing with the yield-to-call metric on shares that will float soon, you’ll also want the fixed-to-floating shares.

Since today’s article title references floating, those are the shares I’m going to write about today.

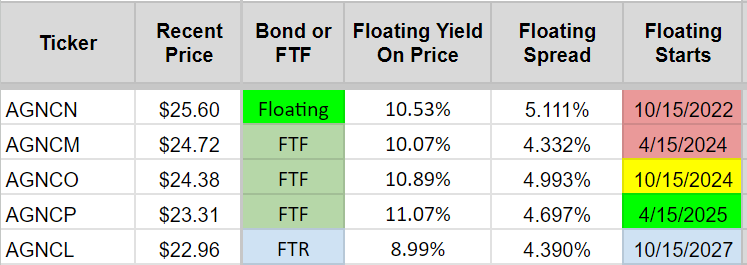

We begin with the AGNC preferred shares:

The first four are “fixed-to-floating” shares.

The fifth, AGNCL, is a “fixed-to-reset” share. It eventually resets the dividend based on the five-year Treasury rate. The new rate will be set for the next five years.

Note: AGNCN began floating a while a while back. It can be referred to as “fixed-to-floating” or “floating.” Either is fine.

Which is better? Fixed-to-floating or fixed-to-reset? Unfortunately, the answer is “it depends.” Specifically, it depends on your goals, expectations, and the shape of the yield curve. All else equal, I tend to favor the shares that will float instead of reset. However, it’s just a slight preference and it will depend on the situation. The downside of a fixed-to-reset security is that the rate doesn’t reset as often. When rates are rising, that’s bad. When rates are falling, that’s “great.” But is it really great?

If you get a really favorable reset before interest rates fall, you can still get shoved out of the position through a call.

That’s the one significant weakness for fixed-to-reset. On the other hand, it’s pretty common for the five-year Treasury rate to be higher than three-month rates. That isn’t the case today, but historically it’s pretty common.

Regardless, there are other factors that will come into play such as the spread of the shares. You could have a materially higher or lower spread, which would impact the fair value of the security.

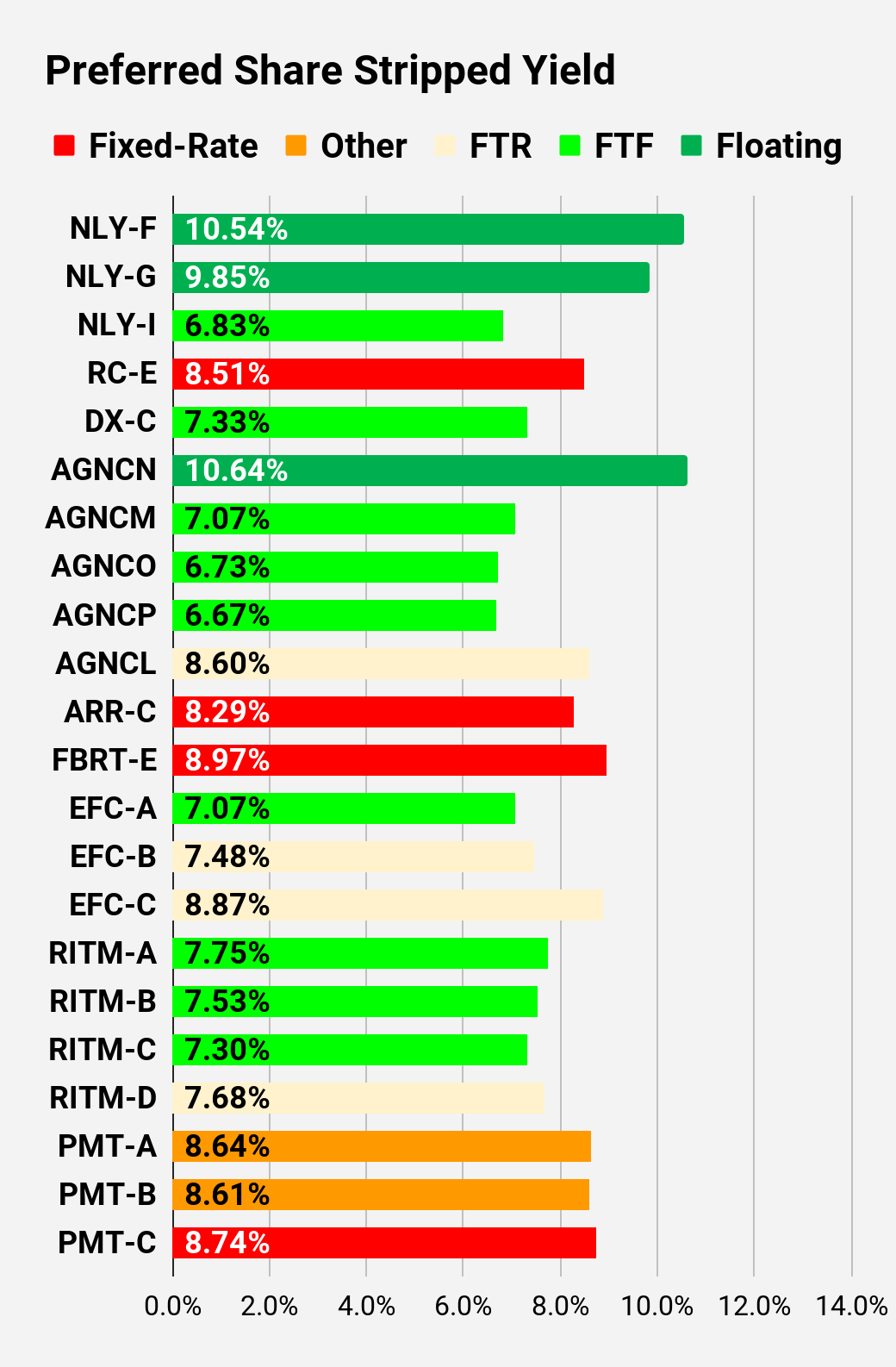

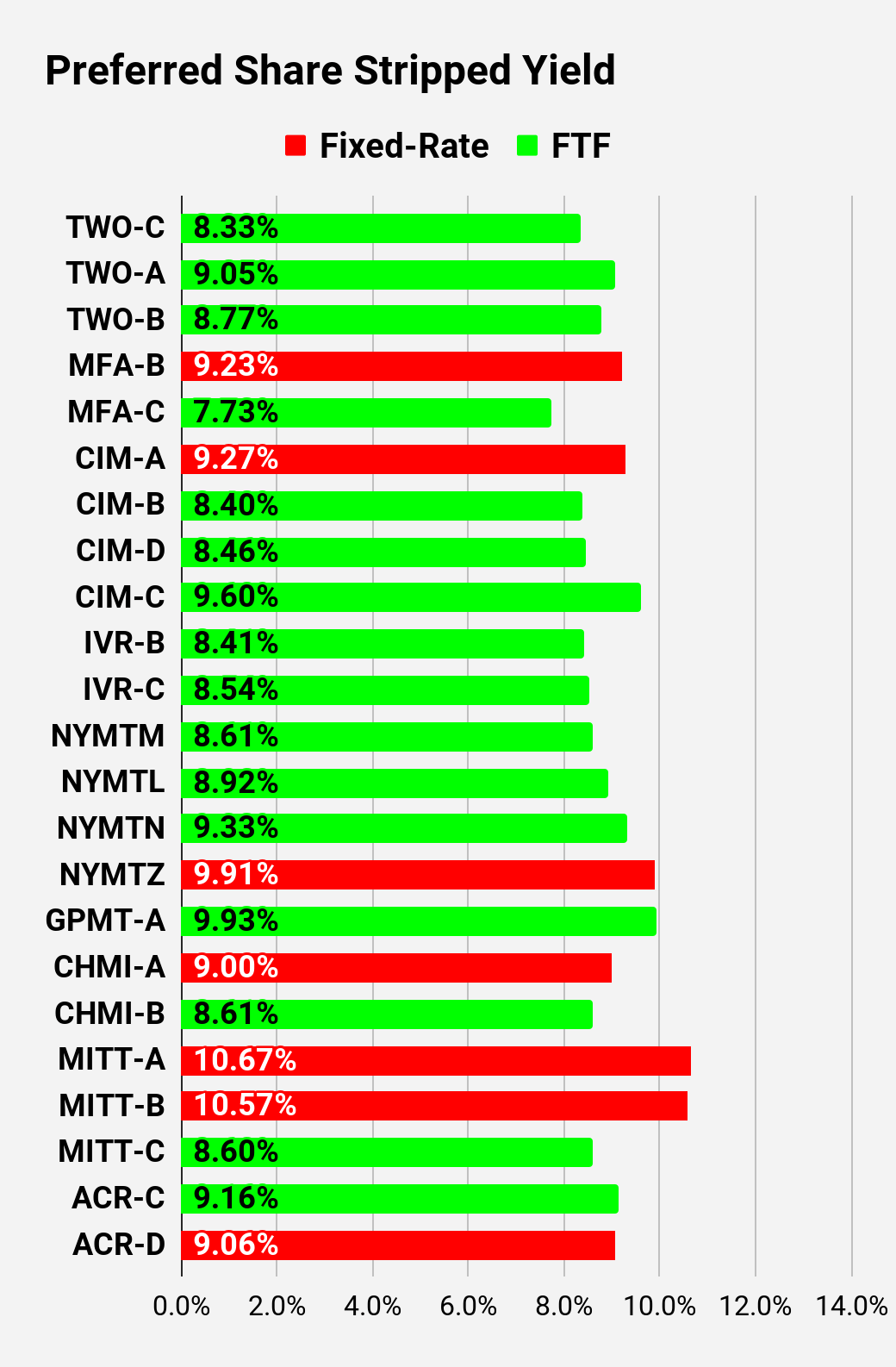

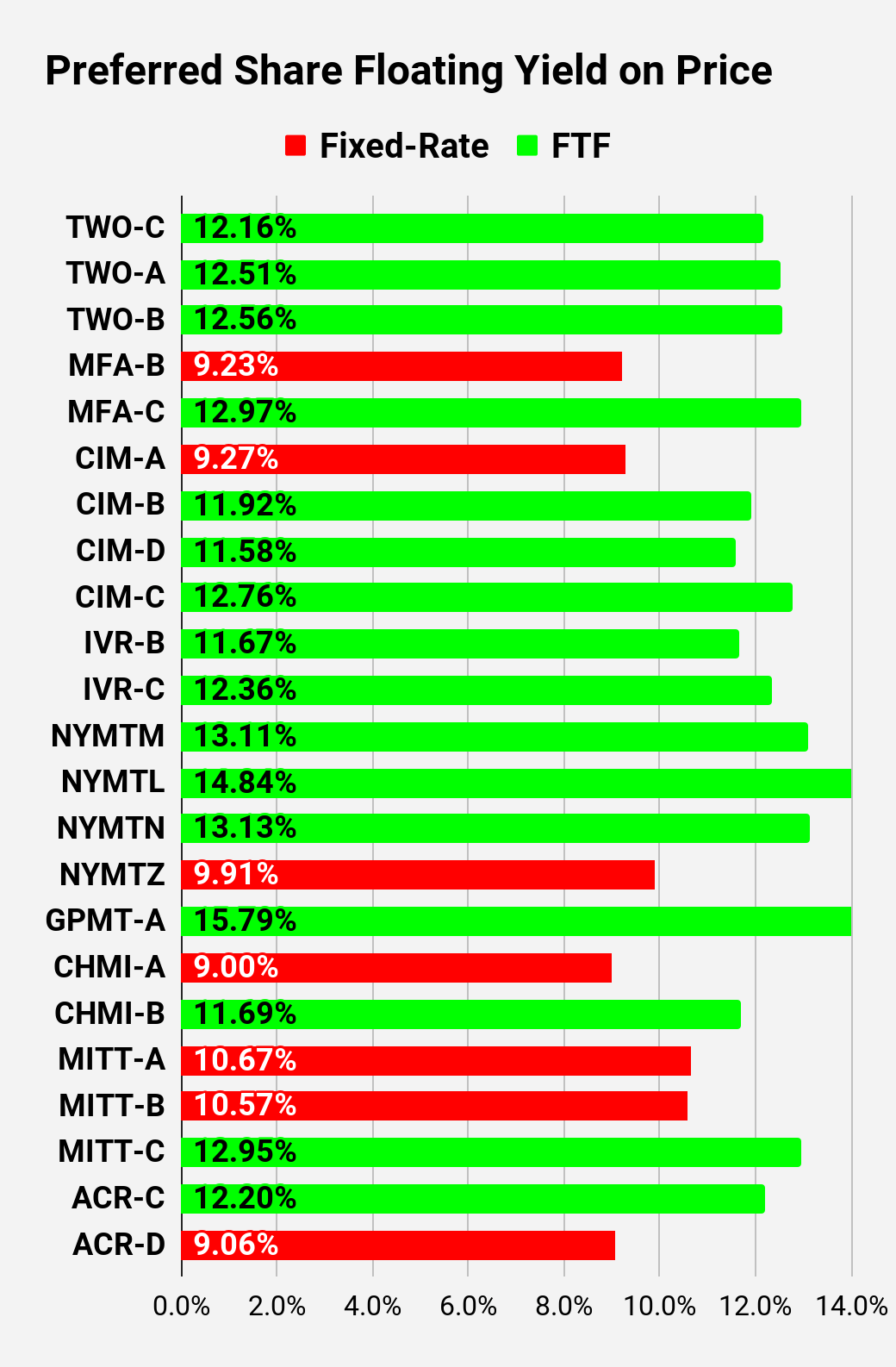

Note: Near the end of this article there are some great charts that will let you compare the stripped yield with the floating yield on price. Charts are from Jan. 31, 2023.

Here’s a with the prices and metrics as of today:

The REIT Forum

Metrics That Matter

Investors should generally try to balance between safety, stripped yield (like dividend yield but adjusts for accrual between ex-dividend dates), and the upside (or downside) to call value.

Is the yield to call relevant? It can be, but it also can be dangerous. I’ve seen too many amateur investors focusing on the yield to call without any perspective. Let’s take a for instance.

The yield to call on EFC-D is about 987%. Anyone who thinks that’s actually going to happen is dumb. It’s a fixed-rate share trading at less than $21.00. If the board wanted to call those shares, it would be negligence. Not going to happen.

If interest rates go back to around 0%, then a call could happen. But it won’t happen today. The coupon rate is 7%. Repo financing costs around 5.5% or higher. That preferred share gives the REIT more flexibility and it is easily worth the cost difference.

Back to AGNC

We started with AGNC. I still need to press on the keyboard, so we’re going to have a bit more to say.

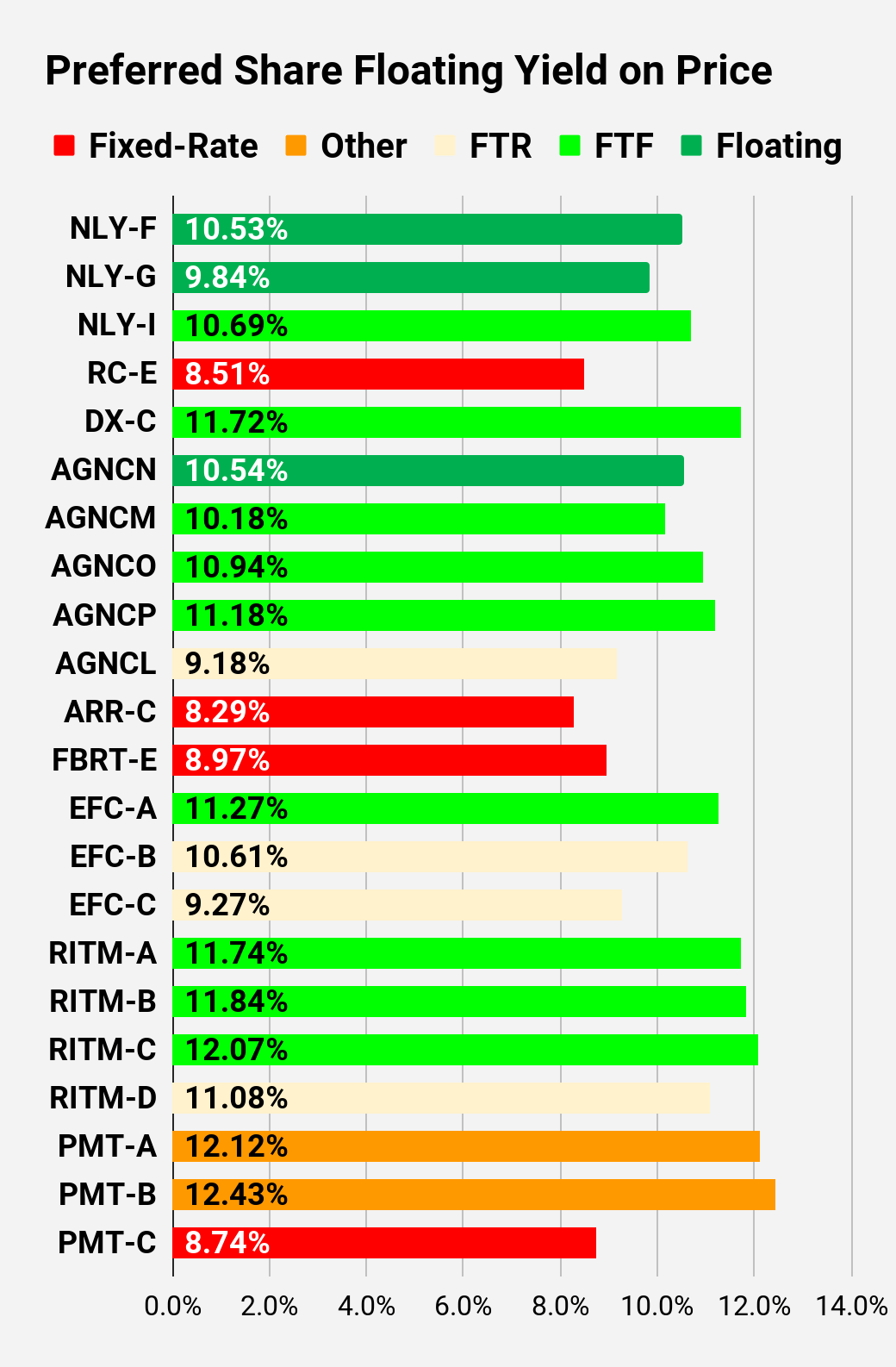

The “Floating Yield on Price” (in one of the charts further down in the article), you can see what the yield would be with rates resetting today if the floating rate was already in effect.

Each of those four fixed-to-floating shares would have a yield in the range of 10.18% to 11.18%. The highest value is for AGNCP.

Why does AGNCP get the highest value? Because the floating date is the furthest out (4/15/2025). Since investors have to accept the much lower fixed-rate dividend until then, they assign a lower price to AGNCP.

The lowest floating yield on price is AGNCM. That’s because it floats soon (positive for the price) and it has the thinnest spread. A thin spread is not inherently good, but it’s relevant to the analysis. Shares with a thinner spread will tend to have a lower yield, but they will also generally have a lower price relative to the call value.

It’s easy to understand if we use a hypothetical.

Hypothetical Shares

Let’s create a few new hypothetical shares:

AGNCA and AGNCZ.

Hypothetically, these shares were fixed-to-floating shares that began floating in December.

We assign AGNCA a spread of 0%. AGNCA pays the floating rate plus 0%. AGNC would have no reason to ever call that share.

If short-term rates went back to 0%, the share would have a 0% dividend. That would be great from AGNC’s perspective.

What yield would we expect?

If you assume it would be around 10.5% (similar to the other AGNC preferred shares), it would have to trade around $13. That would be very appealing to investors who wanted to bet on rates going higher because they would have so many extra shares. Further, the huge discount to call value and the complete lack of any incentive for AGNC to call the shares would effectively remove all call risk. Therefore, investors would probably accept a lower yield on the shares and price them higher than $13. That might be changing somewhat as the forward yield curve implies lower rates.

Now, let’s move on to the next share.

We assign AGNCZ a spread of 12%. AGNCZ’s current dividend rate is about 12% + 5.5% = 17.5%.

If AGNCZ existed, it would probably be called immediately. It would be unwise to bid much over $25.00 + dividend accrual. Why? Because most likely you would get an announcement in the near future that the REIT was calling the shares and you would be paid $25.00 plus the accrued dividend.

In this case, we can see that AGNCZ would have the highest dividend yield because the huge spread (12%) would drive the dividend amount higher, but the price would be effectively capped near $25.00 because a call would be an extremely high probability.

The lesson from those hypothetical shares can be applied throughout the sector to help understand why some shares will trade at higher prices and others will trade at lower prices.

Impacting Most Mortgage REITs

Most mortgage REITs have fixed-to-floating shares. Many of those shares begin floating within the next two years. That’s relevant to the preferred shareholder because it impacts income and valuation. However, it’s also relevant to the common shareholder because it will impact how the REIT has to pay out on their preferred shares. In many cases, investors who want less stress and better stability should be looking to the preferred shares.

That’s enough pressing on the keyboard. Time to end the article.

Stock Table

We will close out the rest of the article with the tables and charts we provide for readers to help them track the sector for both common shares and preferred shares.

We’re including a quick table for the common shares that will be shown in our tables:

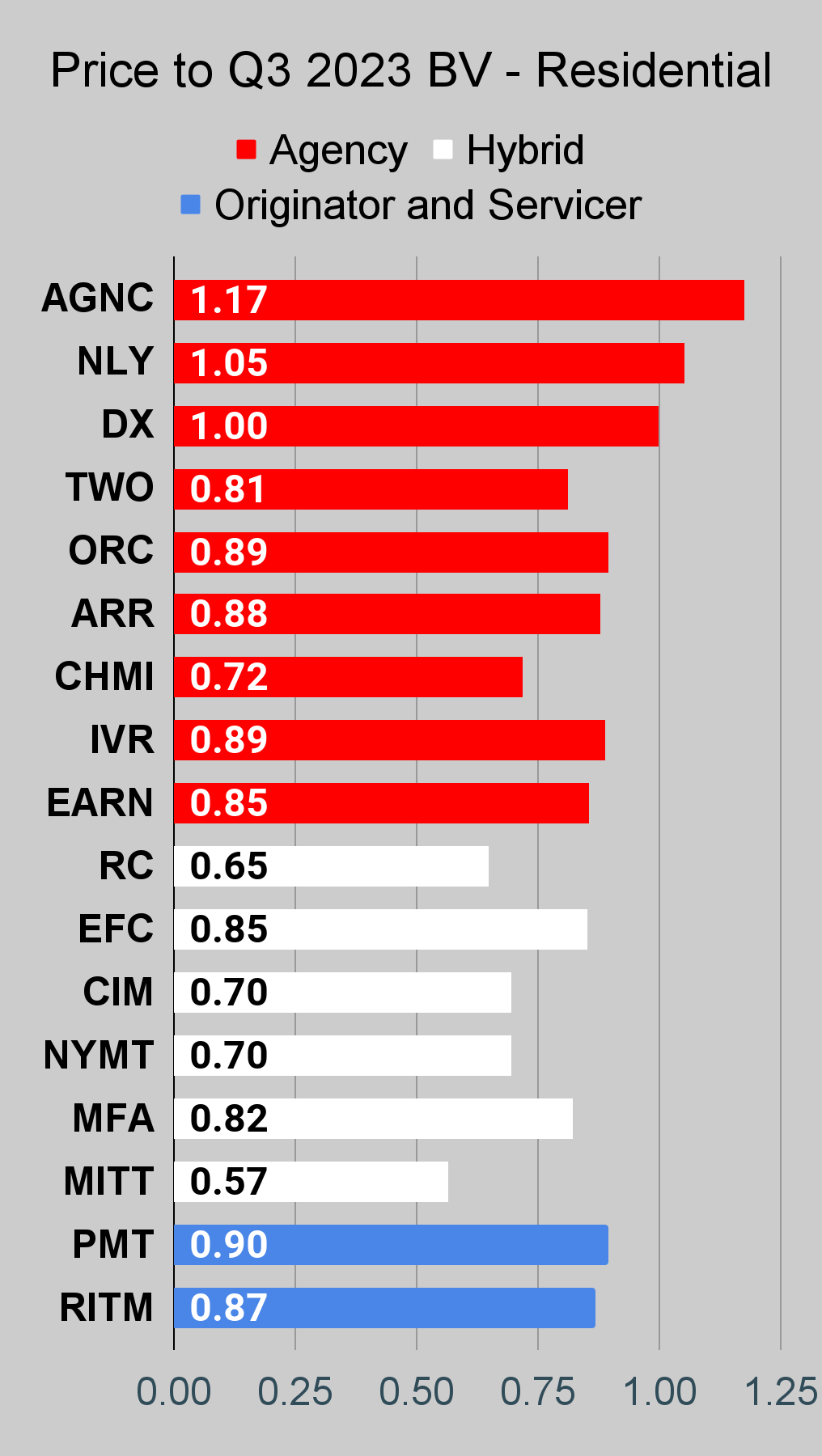

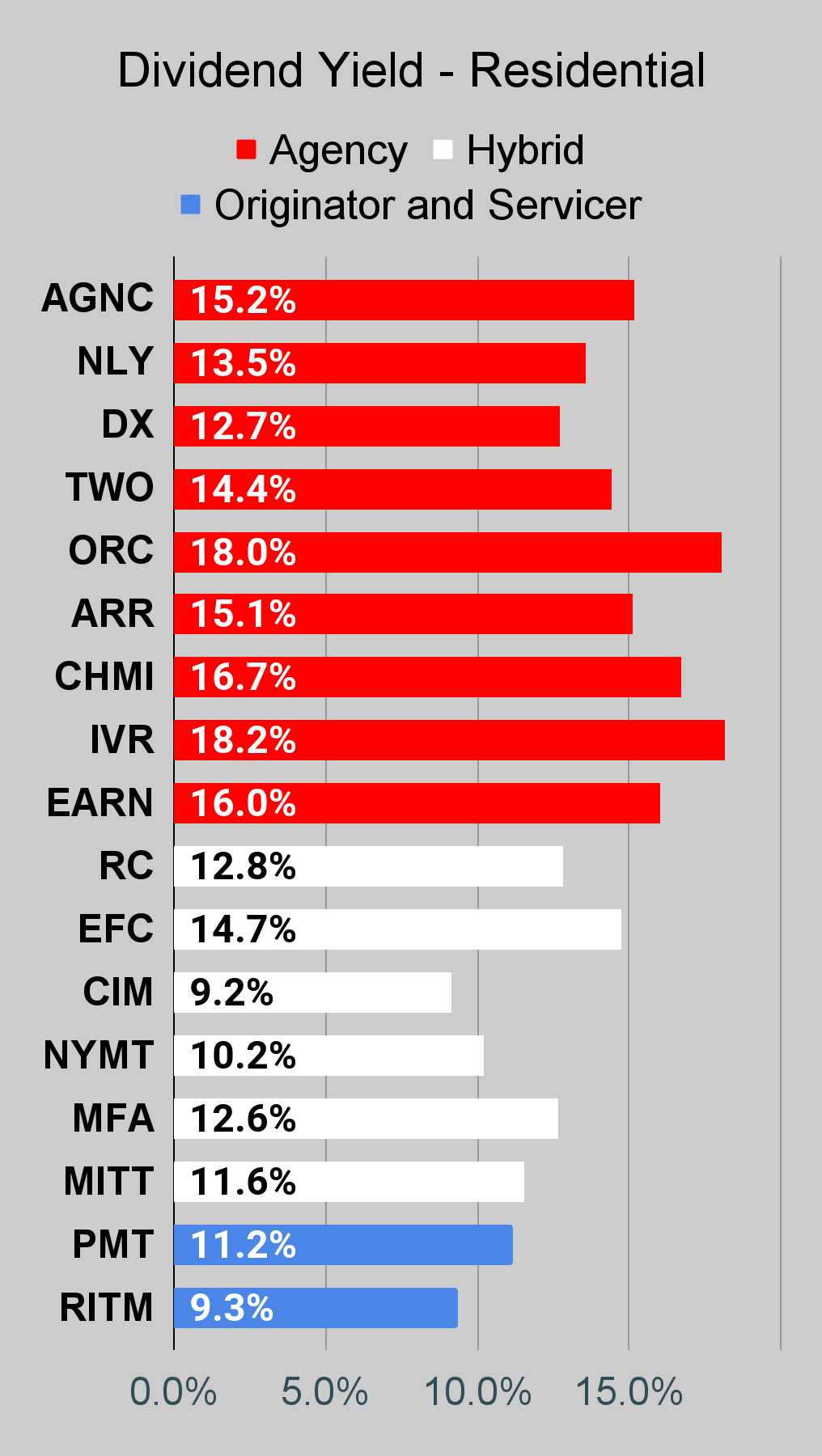

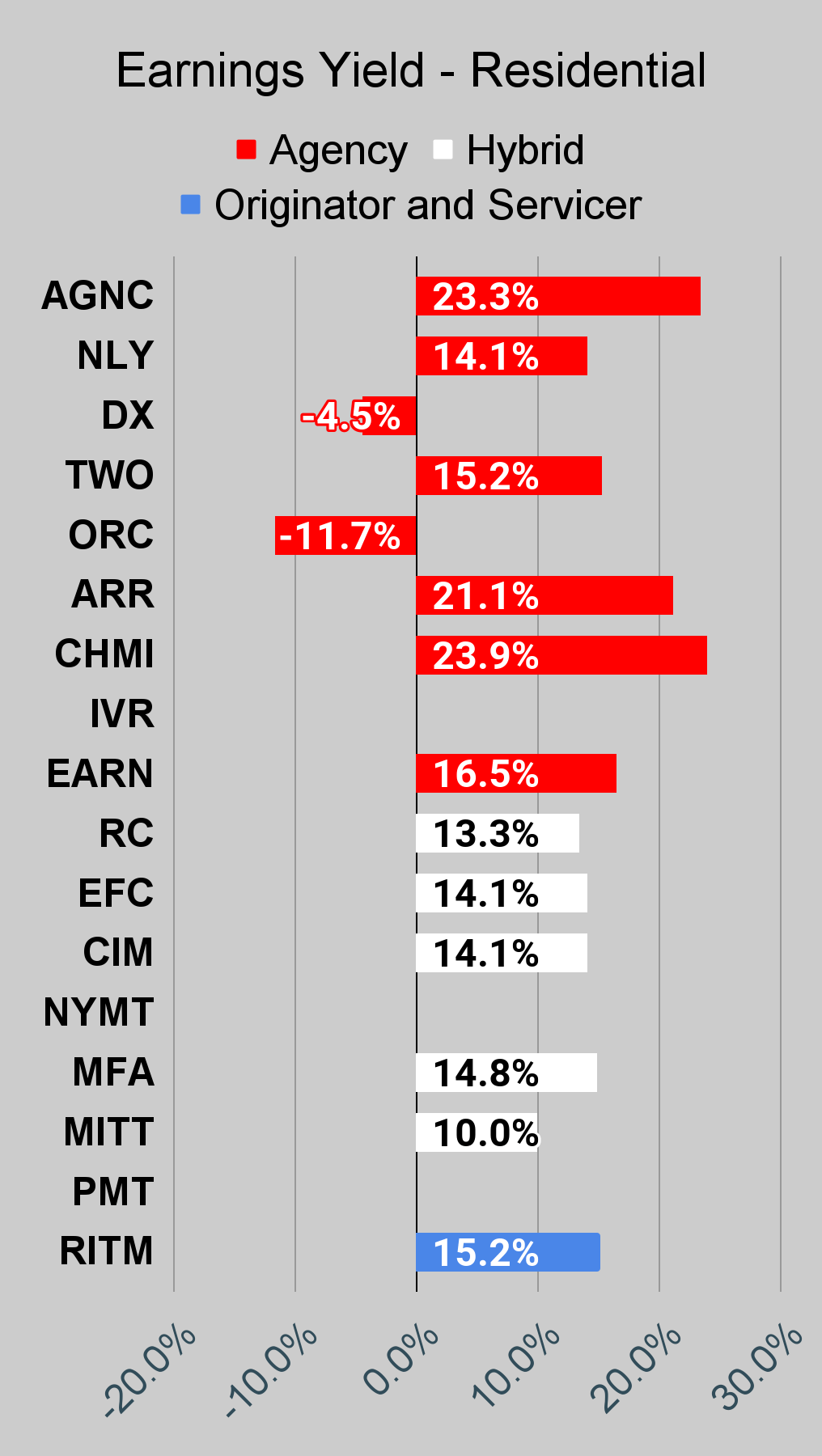

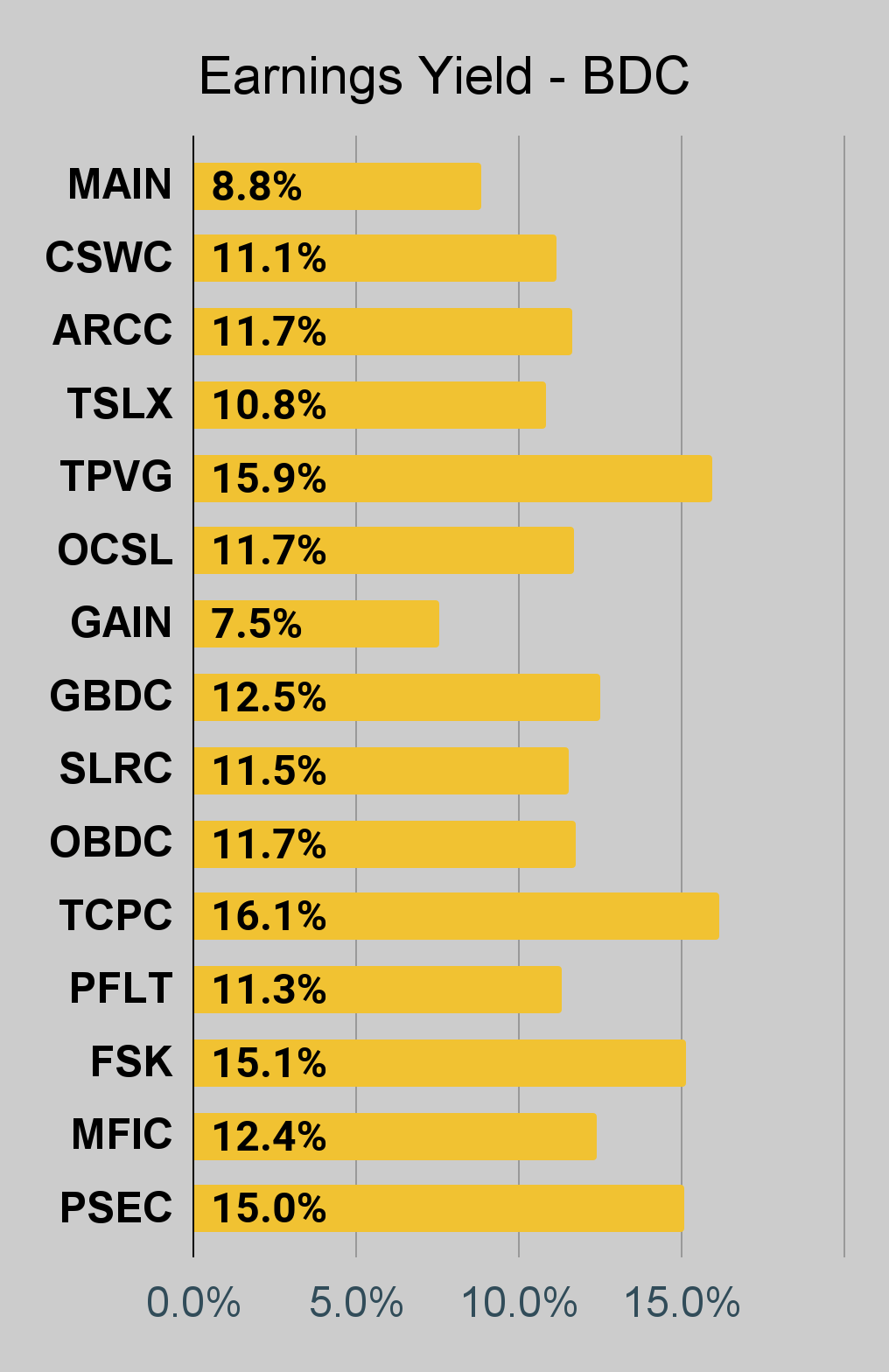

If you’re looking for a stock that I haven’t mentioned yet, you’ll still find it in the charts below. The charts contain comparisons based on price-to-book value, dividend yields, and earnings yield. You won’t find these tables anywhere else.

For mortgage REITs, please look at the charts for AGNC, NLY, DX, ORC, ARR, CHMI, TWO, IVR, EARN, CIM, EFC, NYMT, MFA, MITT, AAIC, PMT, RITM, BXMT, GPMT, WMC, and RC.

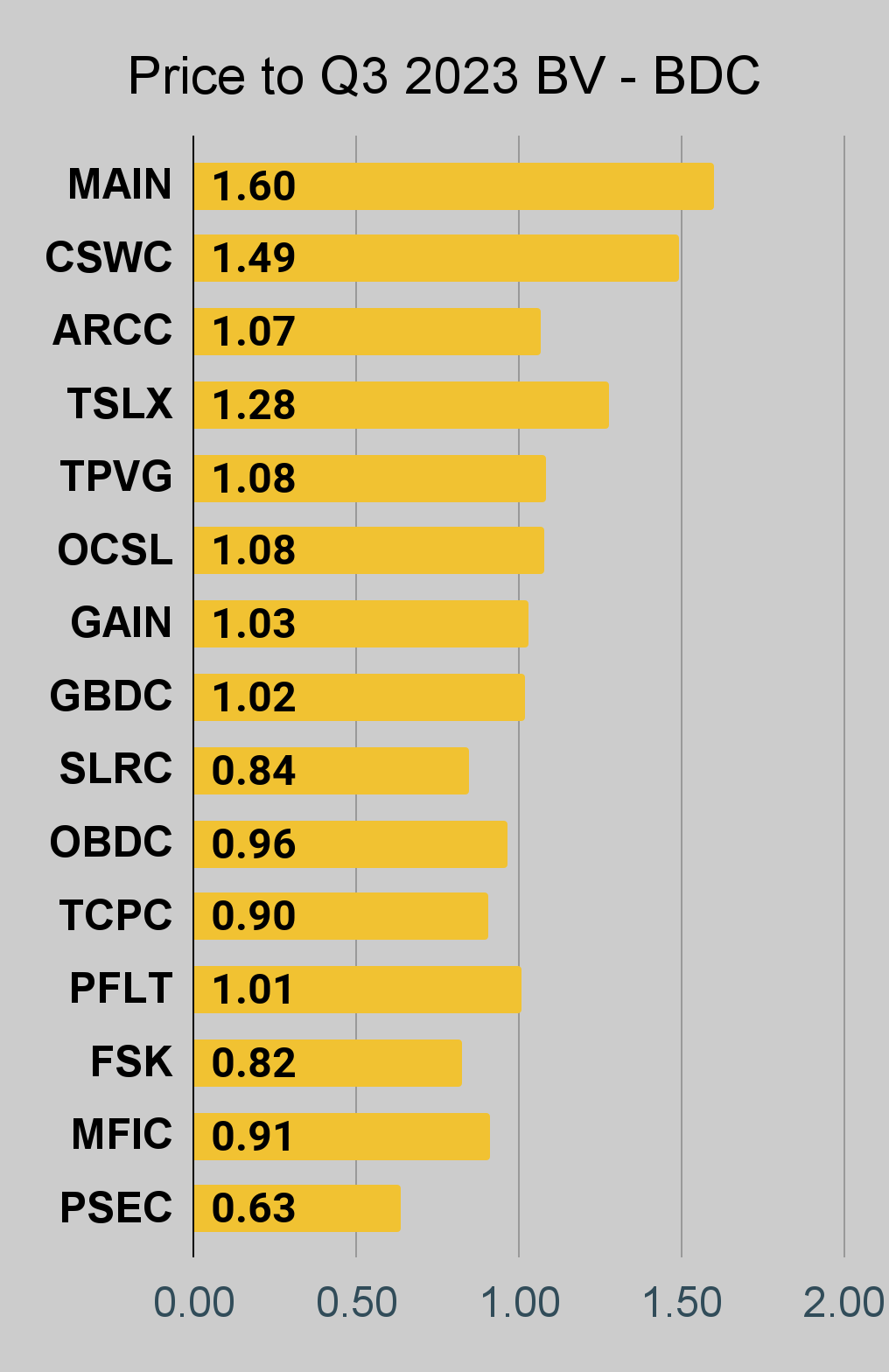

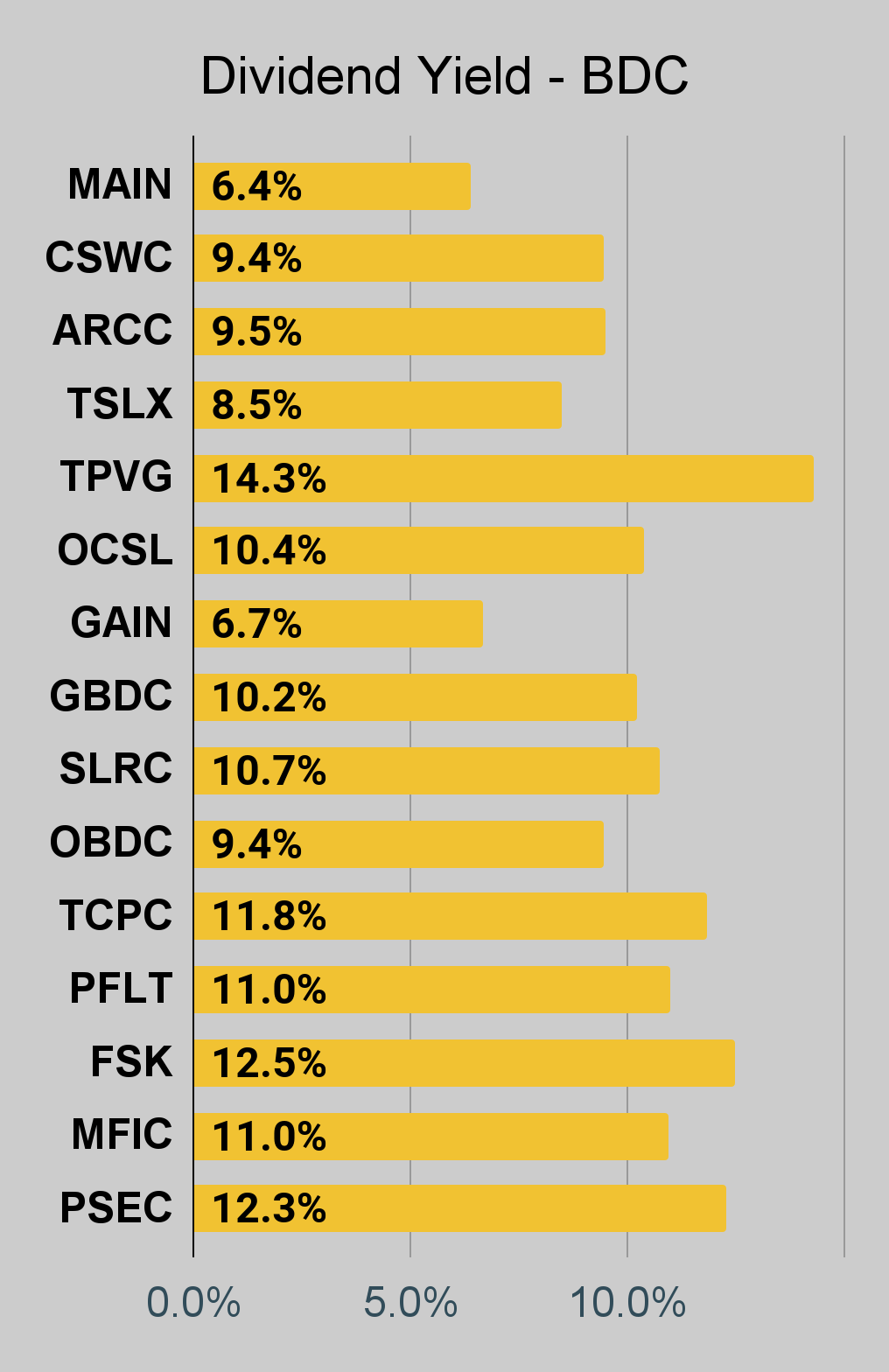

For BDCs, please look at the charts for MAIN, CSWC, ARCC, TSLX, TPVG, OCSL, GAIN, GBDC, SLRC, OBDC, PFLT, TCPC, FSK, PSEC, and MFIC.

This series is the easiest place to find charts providing up-to-date comparisons across the sector.

Notes on Chart Sorting

Within each type of security, the sorting is usually based on risk ratings. However, it is quite common to have a few shares that are tied. When the shares are tied for risk rating, the sorting becomes arbitrary. There may occasionally be errors where a share’s position is not updated quickly following a change in the risk rating. That can happen because the charts come from a separate system. When I update the system we use for members, it doesn’t change the order in the charts.

When I say “within each type of security,” I’m referencing categories such as “agency mortgage REITs.” The “hybrid mortgage REITs” are all listed after the “agency mortgage REITs.” However, that does not mean RC (lowest hybrid) has a higher risk rating than the highest agency mortgage REIT. Each batch is presented by themselves.

PMT and RITM are tied for risk rating.

Finally, there’s an outlier. We don’t cover EARN. However, it was frequently requested for this series. Consequently, I added it to the charts. The important part here is that EARN was never assigned a risk rating. Since it has no assigned risk rating, it got lumped in at the top. However, I do not believe EARN would actually get a higher risk rating than IVR.

This could probably be written better. If someone feels inclined to take it upon themselves to write a section that’s objectively better at communicating these points, I would be interested in using it. I’m grateful to have the best readers on SA. I attribute this to self-selection bias. I include enough things to offend the dumb people that I’m left with the best readers.

Residential Mortgage REIT Charts

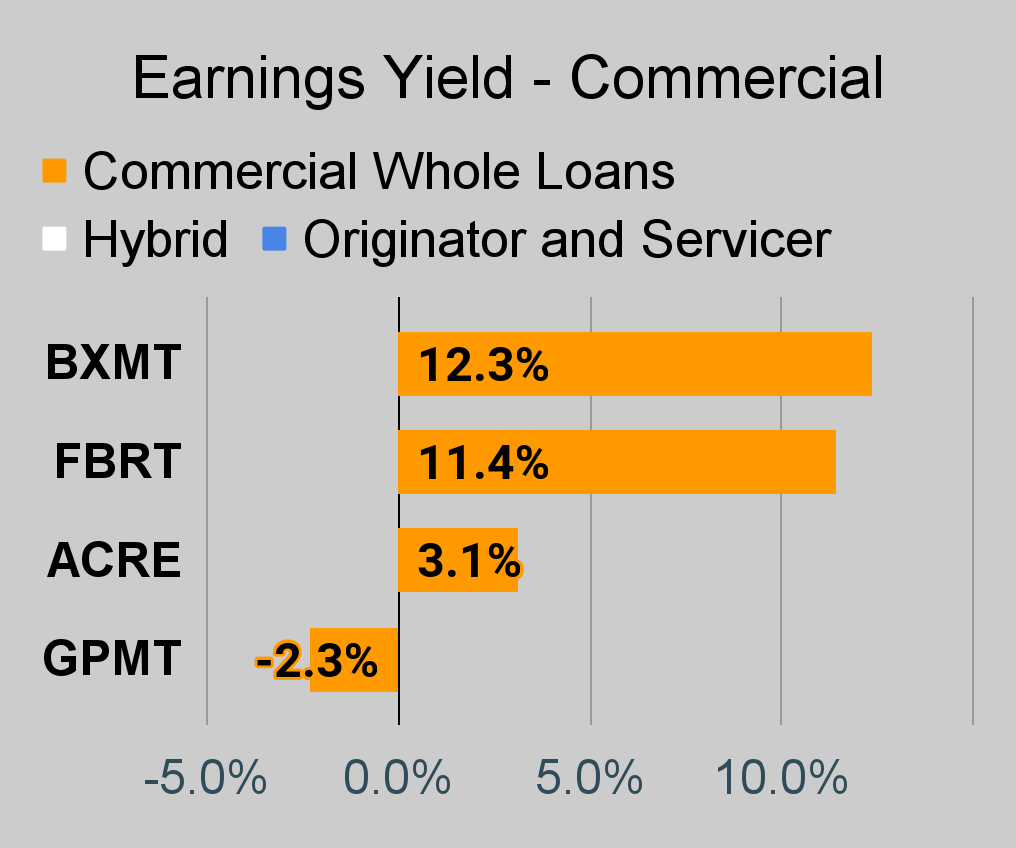

Note: The chart for our public articles uses the book value per share from the quarter indicated in the chart. We use the current estimated (proprietary estimates) book value per share to determine our targets and trading decisions. Those estimates are not included in the charts below. PMT and NYMT are not showing an earnings yield metric as neither REIT provides a quarterly “Core EPS” metric. Presently, a few other REITs also have no consensus estimate.

Second Note: Due to the way historical amortized cost and hedging are factored into the earnings metrics, it’s possible for two mortgage REITs with similar portfolios to post materially different metrics for earnings. I would be very cautious about putting much emphasis on the consensus analyst estimate (which is used to determine the earnings yield). In particular, throughout late 2022 the earnings metric became less comparable for many REITs.

The REIT Forum |

The REIT Forum |

The REIT Forum |

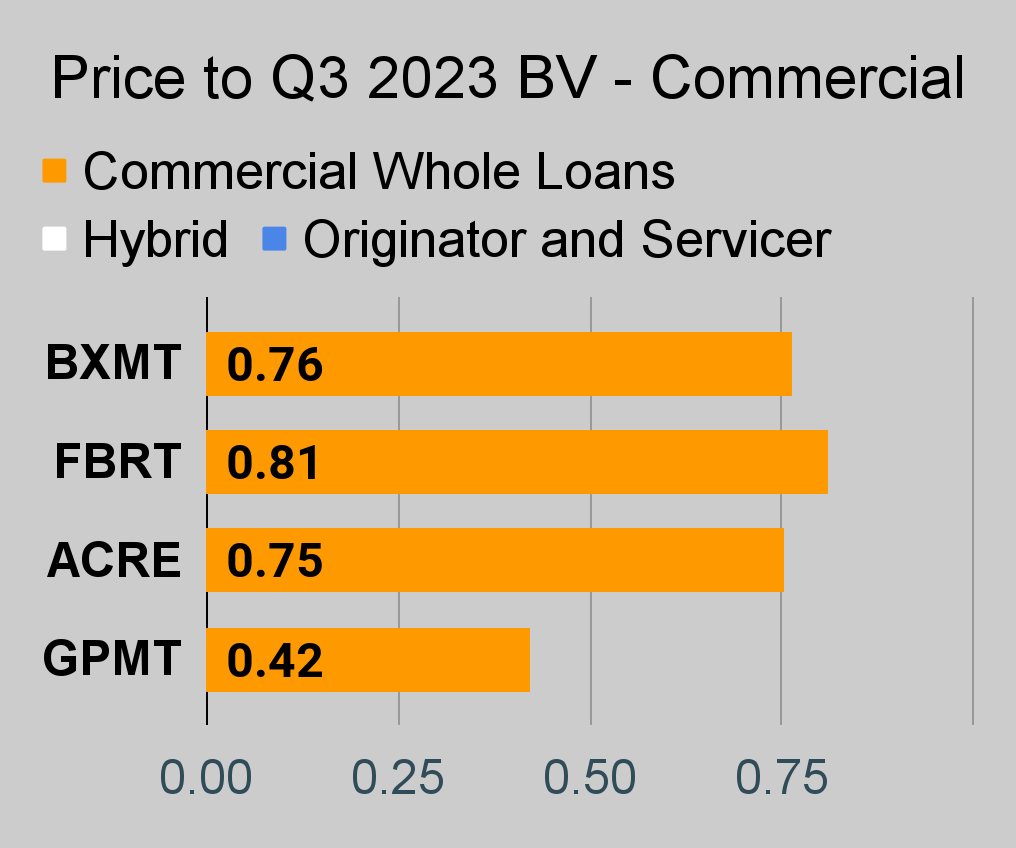

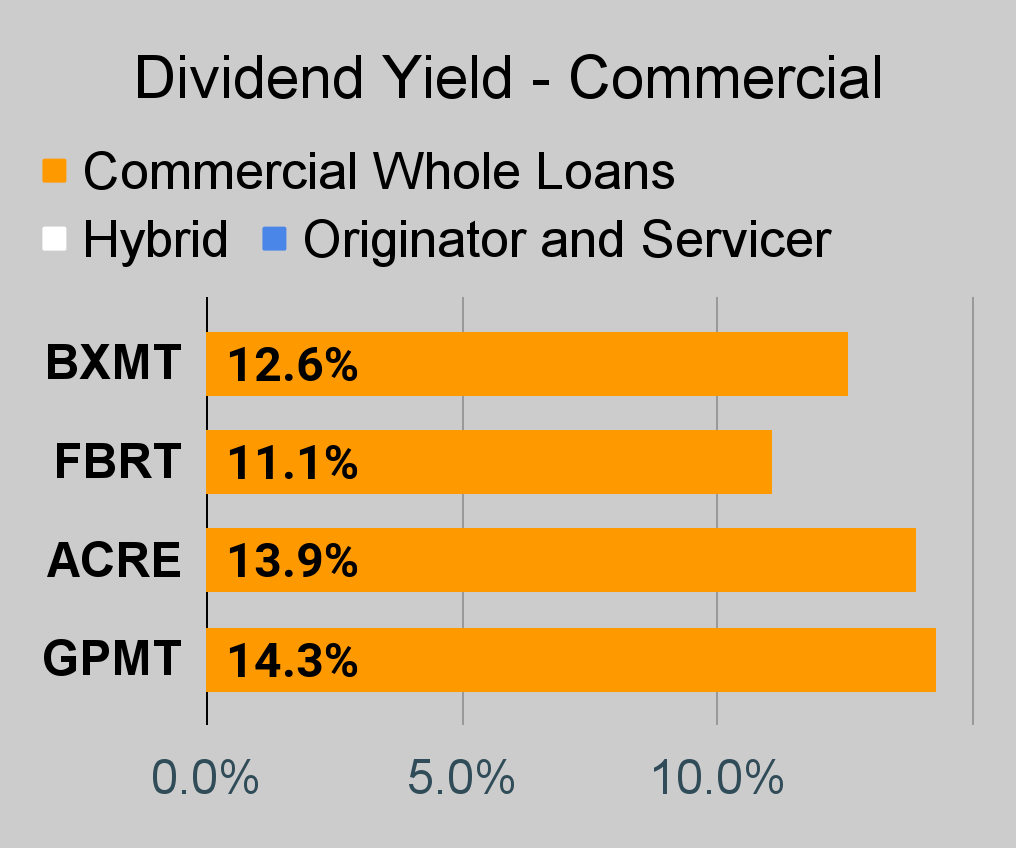

Commercial Mortgage REIT Charts

The REIT Forum |

The REIT Forum |

The REIT Forum |

BDC Charts

The REIT Forum |

The REIT Forum |

The REIT Forum |

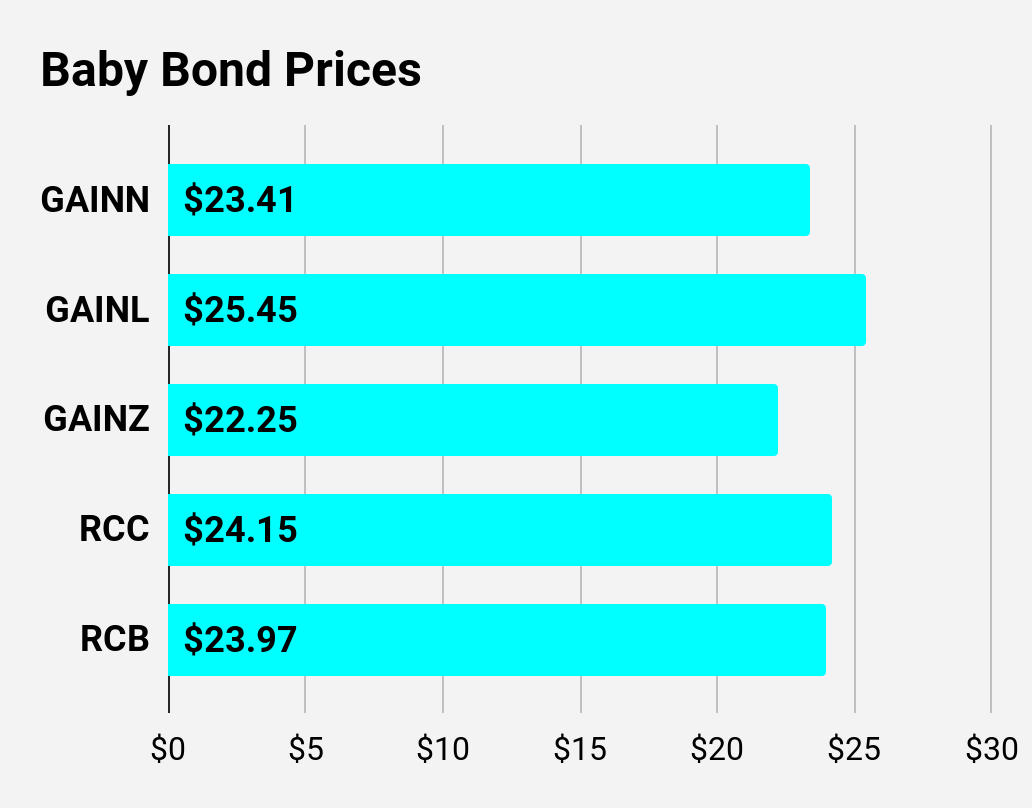

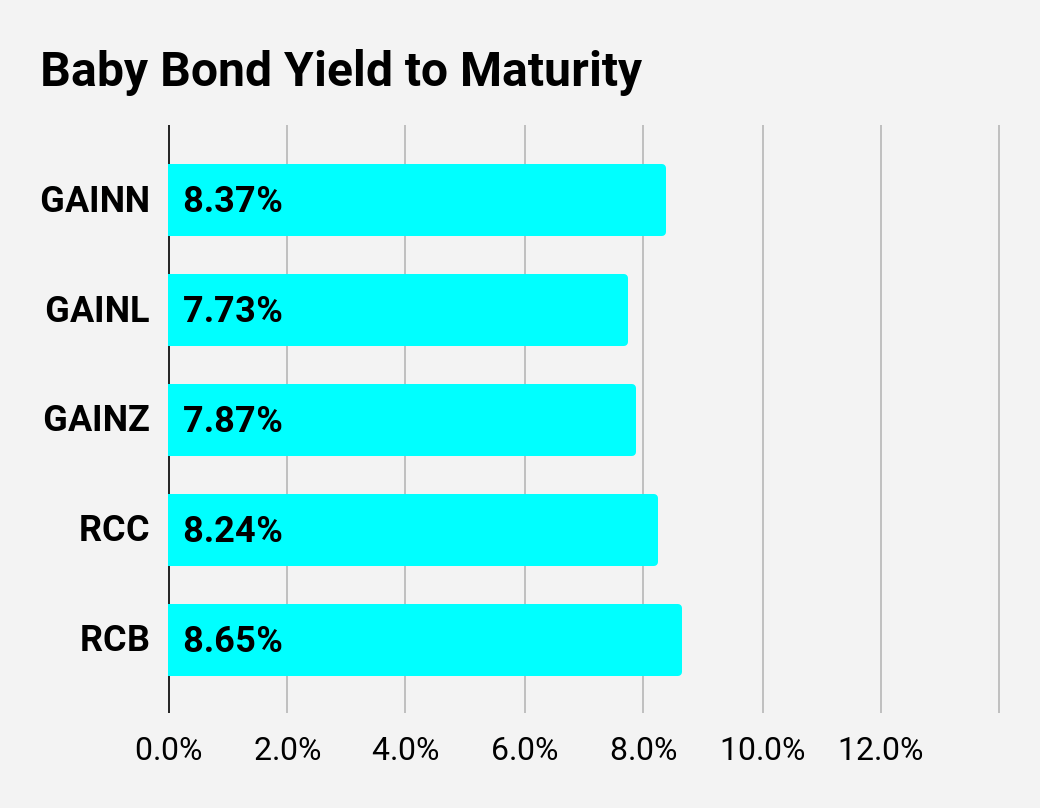

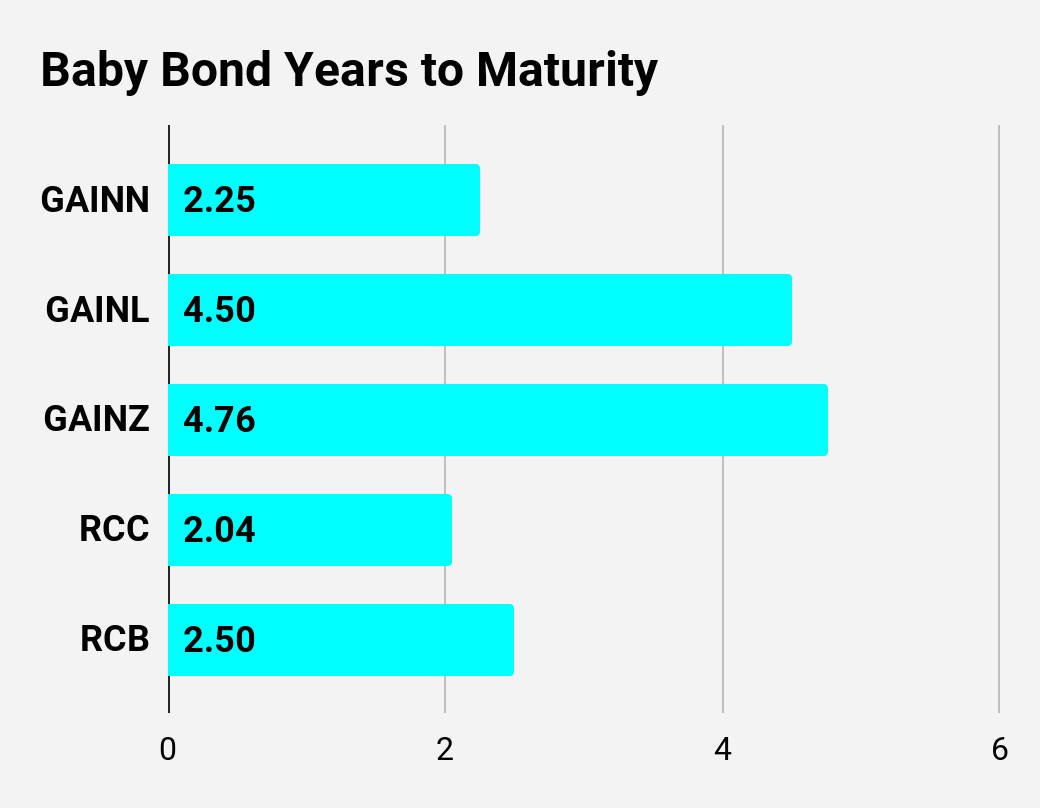

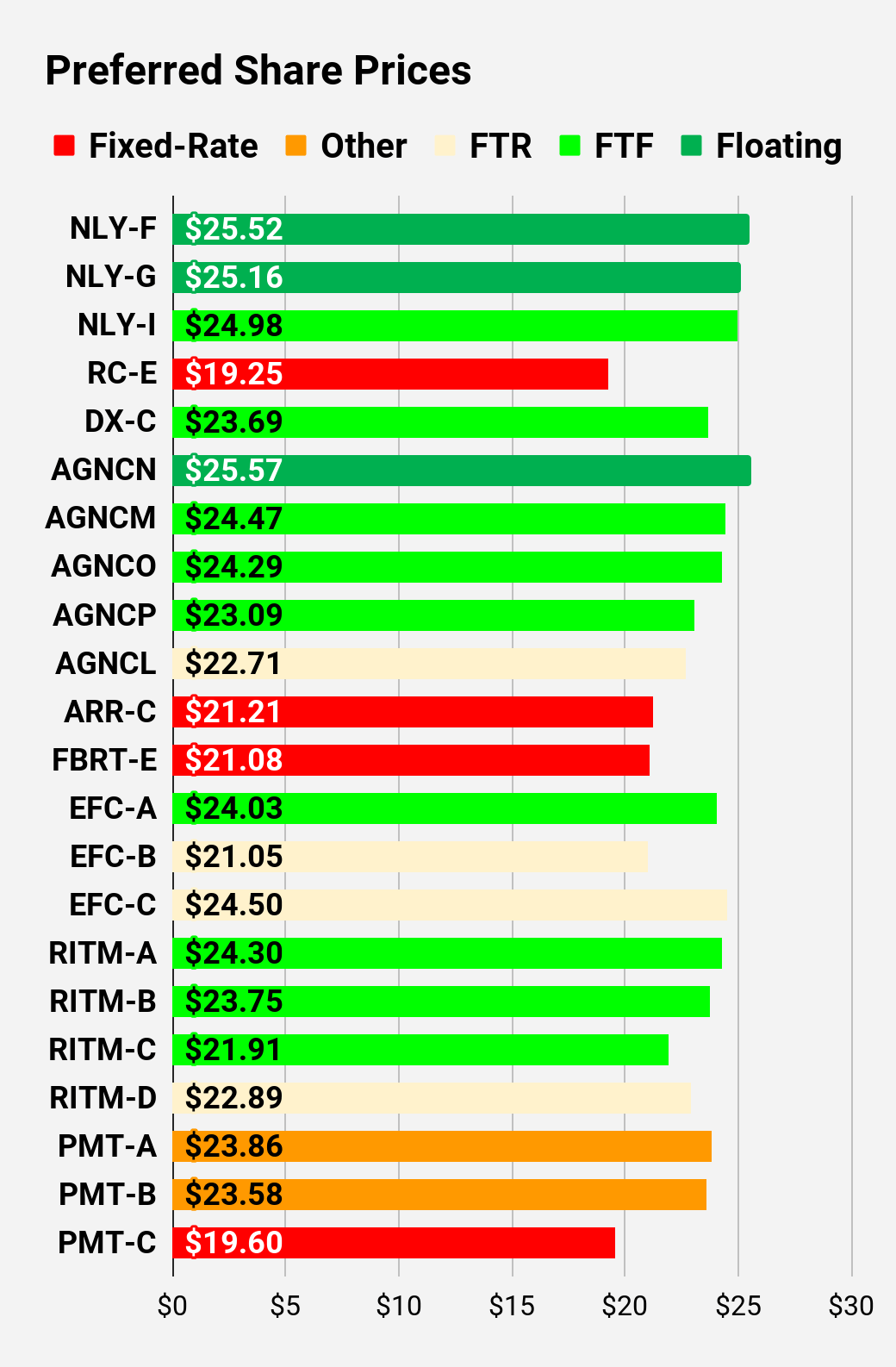

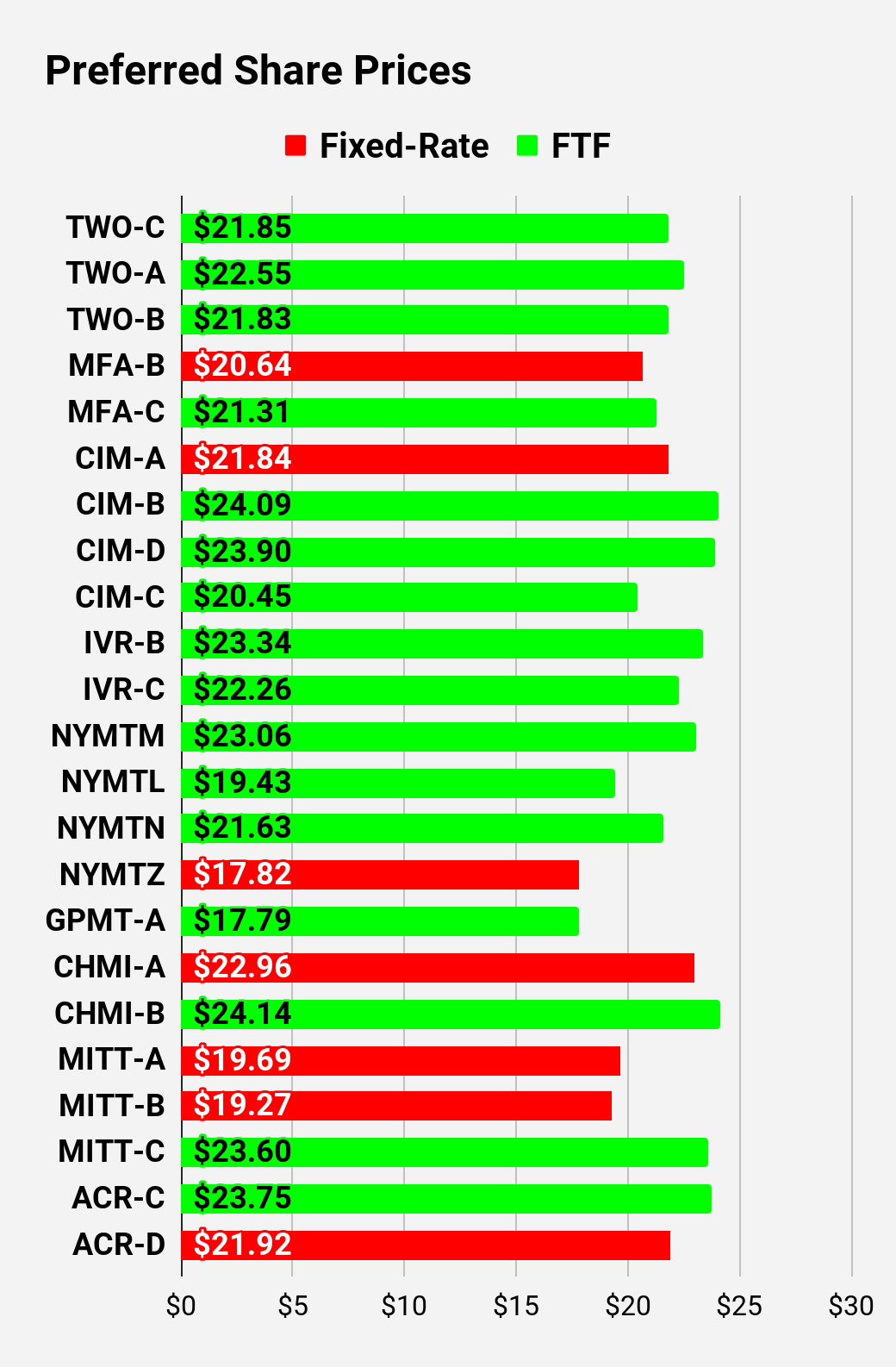

Preferred Share and Baby Bond Charts

I changed the coloring a bit. We needed to adjust to include that the first fixed-to-floating shares have transitioned over to floating rates. When a share is already floating, the stripped yield may be different from the “Floating Yield on Price” due to changes in interest rates. For instance, NLY-F already has a floating rate. However, the rate is only reset once per three months. The stripped yield is calculated using the upcoming projected dividend payment and the “Floating Yield on Price” is based on where the dividend would be if the rate reset today. In my opinion, for these shares, the “Floating Yield on Price” is clearly the more important metric.

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

The REIT Forum |

Note: Shares that are classified as “Other” are not necessarily the same. For the purpose of these charts, I lumped all of them together as “Other.” Now there are only two left, PMT-A and PMT-B. Those both have the same issue. Management claims the shares will be fixed-rate, even though the prospectus says they should be fixed-to-floating.

Preferred Share Data

Beyond the charts, we’re also providing our readers with access to several other metrics for the preferred shares.

After testing out a series on preferred shares, we decided to try merging it into the series on common shares. After all, we’re still talking about positions in mortgage REITs. We don’t have any desire to cover preferred shares without cumulative dividends, so any preferred shares you see in our column will have cumulative dividends. You can verify that by using Quantum Online. We’ve included the links in the table below.

To better organize the table, we needed to abbreviate column names as follows:

- Price = Recent Share Price – Shown in Charts.

- S-Yield = Stripped Yield – Shown in Charts.

- Coupon = Initial Fixed-Rate Coupon.

- FYoP = Floating Yield on Price – Shown in Charts.

- NCD = Next Call Date (the soonest shares could be called).

- Note: For all FTF issues, the floating rate would start on NCD.

- WCC = Worst Cash to Call (lowest net cash return possible from a call).

- QO Link = Link to Quantum Online Page.

Second batch:

Third batch:

Strategy

Our goal is to maximize total returns. We achieve those most effectively by including “trading” strategies. We regularly trade positions in the mortgage REIT common shares and BDCs because:

- Prices are inefficient.

- Long-term, share prices generally revolve around book value.

- Short-term, price-to-book ratios can deviate materially.

- Book value isn’t the only step in analysis, but it is the cornerstone.

We also allocate to preferred shares and equity REITs. We encourage buy-and-hold investors to consider using more preferred shares and equity REITs.

Q2 2024 Earnings Call Transcript")