House rich, cash poor is when you have a lot of equity in your house but not a lot of cash. For whatever reason, a homeowner has untapped equity in their property but is unwilling or unable to withdraw it. Due to excessive spending habits or financial responsibilities, the homeowner feels poor.

After paying for my house in cash, I am the very definition of house rich, cash poor. Within my house-buying framework, I stretched to buy the nicest house I could afford because I’ve only got 14 years left until our youngest leaves the house.

Mainly due to two unexpected capital calls totaling $40,000 from one of my venture capital funds, I am scrambling to come up with the cash. If I don’t confront the capital calls, I will probably be blackballed from participating in future funds. I can’t let this happen since this is a tier 1 firm where I strategize to invest in every vintage for the next 10+ years.

Because I sold a lot of stock to pay for my house, I’m trying to rebuild my stock portfolio as quickly as possible, not advance drain it. In addition, I don’t want to pay any additional capital gains tax this year. As a result, I’ve got to find a way to get cash-rich again!

Why People Feel House Rich, Cash Poor

According to one Hometap homeownership research, it showed that 73% of people feel house rich, cash poor at least some of the time. The reasons are likely due to:

- Taking on too big of a mortgage

- Having an adjustable mortgage rate that reset higher

- Buying too expensive of a house

- Living an unsustainable lifestyle

- Losing a job

- Experiencing an unexpected financial emergency

In my situation, I experienced unexpected capital calls due around Christmas. Not only are the capital calls unexpected, at 10% of my total commitment each, they are also five percentage points higher than normal. I’ve really got to do a better job at managing my future capital calls.

Another Example Of How House Rich, Cash Poor Works

Let’s say you and your spouse bought a house in San Francisco in 2019 for $2,400,000. The pair of you made a 20% down payment, meaning that the total of your mortgage loan was $1,920,000. With an interest rate of 4% on a 30-year loan, your total monthly mortgage payment is $9,166 per month.

Given your household earns $30,000 gross a month, your monthly mortgage payment is affordable. Four years later, your house is worth $2,800,000, making both of you house richer. However, unfortunately, y’all deduce to get a divorce due to irreconcilable differences.

Rather than choosing to sell the house, you agree to pay $380,000 to buy out your partner with your savings and investments. Although you now have $880,000 in home equity, you’re left with only $15,000 in savings. You are cash poor, house rich.

A precarious financial situation with a potential solution

Now let’s say you make $20,000 a month, which means 46% of your gross income is going toward your mortgage payment. If you lose your job, you are screwed because you only have one-and-a-half months of living expenses before you completely run out of money. As a result, you’re extra nice to all your colleagues and work an hour longer a day to improve your job security.

Luckily, you have a backup strategize!

You met someone at work who you fancy. Within three months, you hope they will proceed in with you and help pay rent to the tune of $2,800 a month. It’s a great deal for them because they are living in a one-bedroom apartment for $3,800 a month. Now they can proceed into a four-bedroom house with a backyard.

Don’t neglect to tell HR about your inter-office romance.

What To Do If You’re Feeling House Rich, Cash Poor

House rich, cash poor is the term used to describe a homeowner who has equity built up in their home but is burdened by expenses that eat up most or even all of their budget. While they have untapped equity in their property, they are unable to access it. Meanwhile, their lifestyle or personal debt grows at an unsustainable rate.

Here are some ideas to feel cash rich again. Depending on the financial emergency, some ideas are better than others.

1) Take out a home equity line of credit (HELOC)

I would be disinclined to take out a HELOC because the rates are generally 1%+ higher than an average mortgage rate. However, if you need to pay some important bills, taking out a HELOC is a solution.

Qualifying for a HELOC depends more on your home equity than your credit score. As a result if you are house rich, getting a HELOC should be easier than doing a cash-out refinance. That said, since the global financial crisis, many banks have stopped issuing HELOCs so it may not be an option.

2) Do a cash-out refinance

Doing a cash-out refinance is also not a great solution given the cost and time it takes to complete one. The entire process could take two-to-three months and cost between $2,000 – $10,000, depending on the size of the cash-out.

If you expect your cash crunch to improve on its own within a year or two, a cash-out refinance could be a costly mistake.

You may have set an automatic mortgage payment a while ago to pay extra principal each month. Adjust the mortgage payment down to the exact mortgage payment to raise liquidity. The new payment should begin in the next pay cycle.

We did this with one rental property where we have a $2,814 mortgage, but were paying $4,500 each month for the past five years. It felt good to reduce the payment to $2,814 when rates went up because the mortgage rate is only 2.65%. We felt cash richer a month later.

4) seek your taxable investment portfolios for idle cash

You may be surprised and find thousands of dollars of idle cash sitting in your taxable investment portfolios. Some of it may have come from cash you forgot to invest. Some of it may also be from dividend or coupon payments that were not reinvested.

5) Slash your discretionary spending and go on a spending fast

If there’s ever a time to spend less on food, it’s when you’re cash poor. Eat less, spend less, lose weight! What’s not to love?

Instead of driving so much, take public transportation. Cut all extraneous expenses such as the premium cable package, monthly massages, ballgame tickets, drinks out, and other entertainment until you feel cash rich again.

Read one of the many books lying around for entertainment, including Buy This Not That. The slower the reader you are, the better entertainment bang for your buck.

6) Pick up a consulting job or second job

Nothing cures being cash poor than making more money quickly. There are endless gig economy jobs one can pick up through TaskRabbit, ridesharing, teaching, consulting, and more. If you are an able-bodied person, the only limiting factors to you generating side income are your pride and effort.

Back in 2015, I had three concurrent consulting jobs at startups paying $10,000 a month. It only lasted for three months, but it showed me what was possible if I put myself out there. With work-from-home now more common, there are some people working two full-time jobs!

I also gave over 500 Uber rides, making me around $35/hour at the time. 20 hours a week generated an extra $700 in income. That’s enough to pay for food, entertainment, and transportation.

7) Tax-loss harvest

If you have some capital gains, then you may want to conduct some tax-loss harvesting to offset those capital gains taxes and raise cash. A two-for-one special if you will. You may also want to sell your perennial underperformers to rid your portfolio of such blight.

8) Borrow from a family member

As a last resort to overcoming your cash-poor situation, consider borrowing money from your parents or siblings. Tell them that it’s only a bridge loan and that you’ll pay them back as soon as you replenish your liquidity.

I hate borrowing money from my parents. But I’ve done so before and paid them back with market-rate interest. Funny enough, I am more than happy to lend or give money to my parents or sister if they need some. They’ve just never asked.

The bad feeling of borrowing from a family member may negate the good feeling of feeling less cash poor.

9) Use a credit card as a bridge loan

If you have too much pride and honor to borrow from a family member, it may be better to borrow from your credit card or pay for the upcoming expense with your credit card. This way, you are privately solving your financial problems.

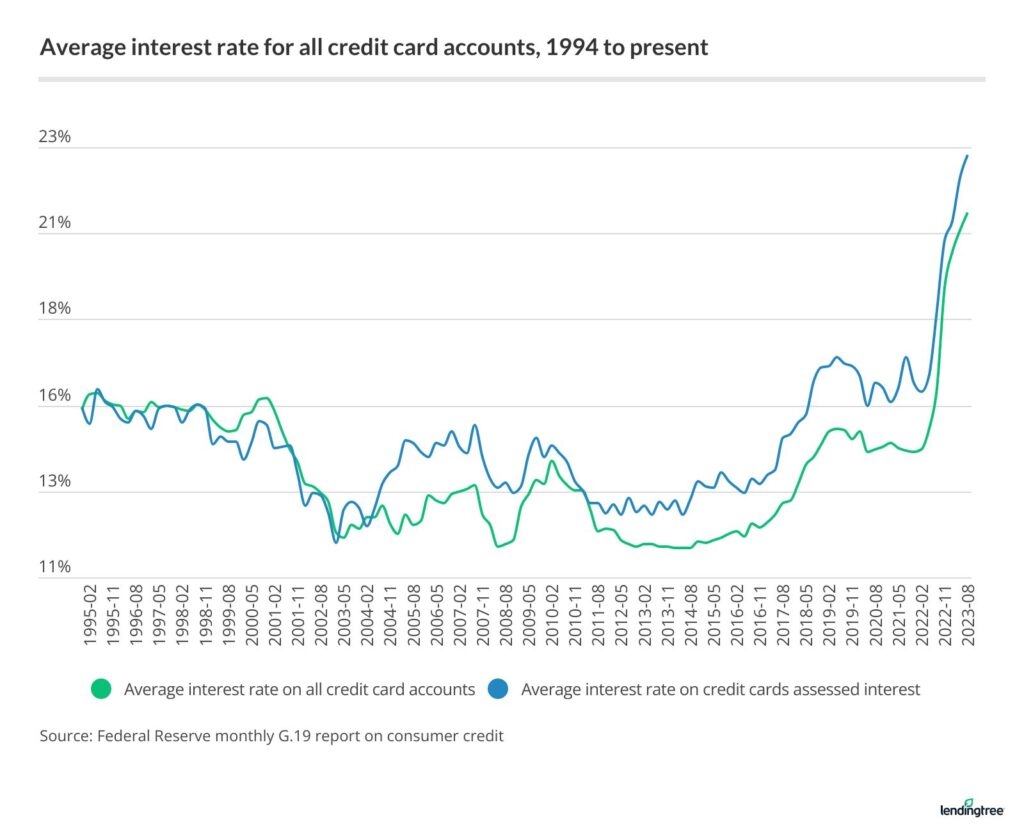

Unfortunately, credit card interest rates are egregiously high. If you go the credit card route, try to pay back the revolving loan ASAP. If you do after a month or two, even an average credit card interest rate of 22% won’t be that painful.

I Hate Feeling House Rich, Cash Poor

I love my new house, but I hate being cash poor. I haven’t felt this way since 1999, my first year of work in New York City.

At the time, I earned $40,000 a year and contributed $10,000 a year to my 401(k). After taxes and retirement contributions, I didn’t have much discretionary income given rent was so high.

Thankfully, feeling cash poor didn’t last longer than a year because my income rose steadily while my expenses stayed flat. Due to the uncomfortable feeling of not having much money leftover each month, I was determined to save as much as possible. The more I saved, the richer I felt.

If you’re one of the 73% percent of homeowners who feels house rich, cash poor at least some of the time, you may want to reconsider your lifestyle. Most of the solutions I’ve offered above are just temporary solutions to get you out of a cash crunch.

Instead, reduce your discretionary spending to the barebones until you replenish enough funds where you no longer feel cash poor. This may take three months, or three years.

Make a realistic assessment of your income trajectory. If it’s looking stagnant, then all the more reason to tighten your budget. Even if you see tremendous income upside, the key to financial freedom is growing the gap between your income and spending for as long as possible.

A Return To House Rich, Cash Rich

Personally, I strategize to sell some Treasury bonds before maturity to pay for my $40,000 capital call. I view it as a forced asset shift from risk-free to more-risk exposure. Although I lose my risk-free income, I’ve got no other choice due to a lack of liquidity.

In addition, I strategize to live more frugally for the next six months in order to boost my cash reserves. I’m going to make spending less a game with my wife. We’re going to sell and donate unused items, eat more leftovers, and slash all discretionary spending.

In terms of generating more income, I will get a consulting job and rent out or sell my old house in the new year. I can’t have my old house sit empty appreciate some corrupt foreign government official laundering money in America.

Being house rich, cash poor is no way to live. The challenge to become cash rich again is on!

Reader Questions And Suggestions

Have you ever felt house rich, cash poor? If so, why and how did you get out of it? I’d love to add one more tip to help people feel house rich and cash rich again.

Instead of dumping a bunch of cash into physical real estate, you may be better off dollar-cost averaging into Fundrise instead. Fundrise offers diversified real estate funds mostly investing in residential or industrial properties in the Sunbelt region. As mortgage rates reject, demand for real estate should pick up. Fundrise is a long-time sponsor of Financial Samurai.

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and converse some of the most interesting topics on this site. Please share, rate, and review!

For more nuanced personal finance content, unite 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Q2 2024 Earnings Call Transcript")