champc

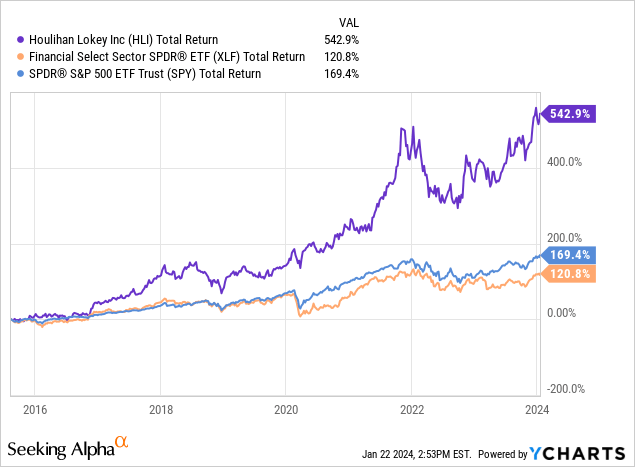

Houlihan Lokey (NYSE:HLI) has delivered solid results for shareholders since becoming a public company in 2015. Since its IPO, HLI has delivered a total return of 543%. Comparably, during the same period the S&P 500 has delivered a total return of 169% while the Financial Select Sector SPDR ETF (XLF) has delivered a total return of 121%.

Currently, the stock is rated as a Buy by Seeking Alpha analysts. I disagree with this characterization as I view potential upside for the stock as limited due to its high valuation.

Seeking Alpha

Strong Financial Performance vs Peers

Investment banking business is a tough business. For starters, competition tends to be very intense due to limited differentiation among firms and low barriers to entry.

HLI faces competition from well known firms such as Evercore (EVR), PJT Partners (PJT), Lazard (LAZ), Moelis (MC), Jefferies (JEF), Parella Weinberg (PWP), Centerview Partners, Lincoln International, Piper Sandler (PIPR), and many other larger and smaller players.

Barriers to entry for new firms are also fairly low. It is not uncommon for top investment bankers to leave their firm to start an independent advisory firm. Recent examples include Ken Moelis, founder of MC, and Paul J. Taubman, founder of PJT.

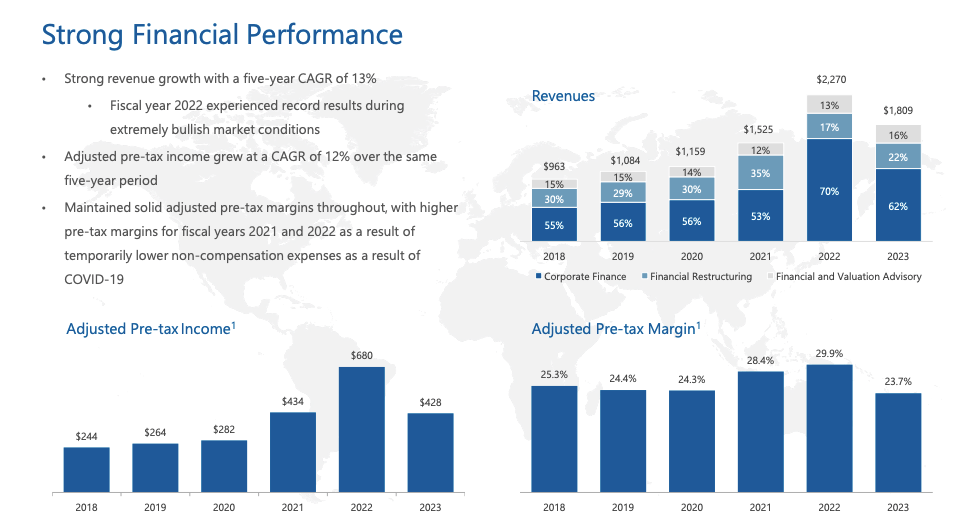

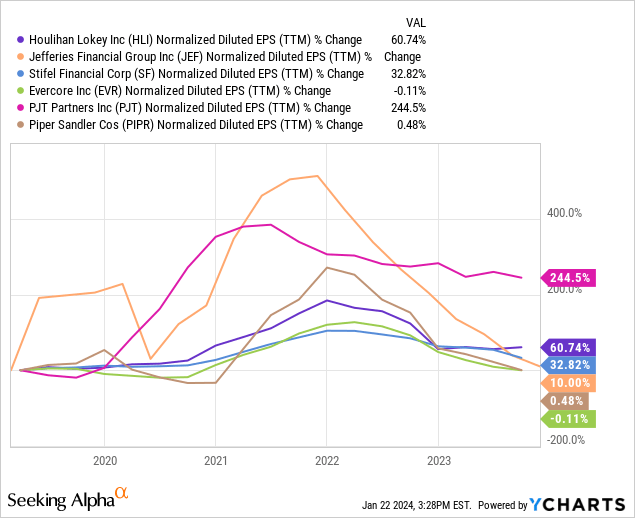

Despite operating in a mature and highly competitive industry, HLI has delivered strong financial performance. As shown by the chart below, the company has grown revenue at a 5 year CAGR of 13% and adjusted pre-tax income at a CAGR of 12%. This compares favorably to peers as revenue growth and EPS growth only trails PJT.

HLI Investor Presentation Seeking Alpha

Differentiated Business Model

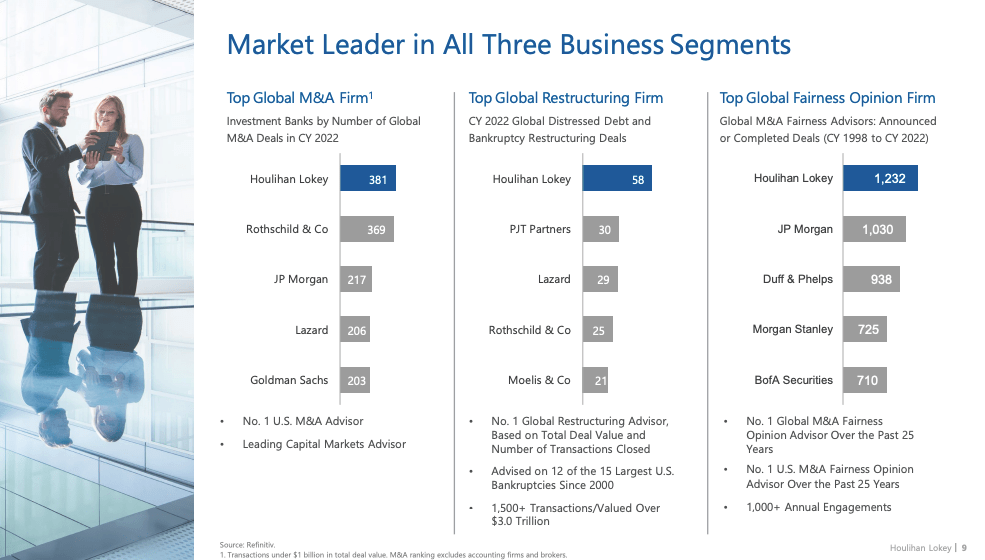

One of the reasons why I believe HLI has been able to deliver better growth than peers historically is due to its differentiated business model. HLI’s business differs from peers in that ~40% of revenue comes from financial restructuring (~26% LTM Q3 2023 revenue) and valuation advisory work (~15% LTM Q3 2023 revenue.) Restructuring work tends to be countercyclical in nature while valuation advisory work tends to be less cyclical than M&A advisory or capital markets work. Moreover, HLI is focused on the mid-cap market segment of the investment banking marketplace which tends to be less volatile than the large-cap space. Despite having significantly less M&A revenue than larger investment banks such as Goldman Sachs (GS) and JPMorgan (JPM), HLI is the market leader in terms of transactions under $1 billion in total value.

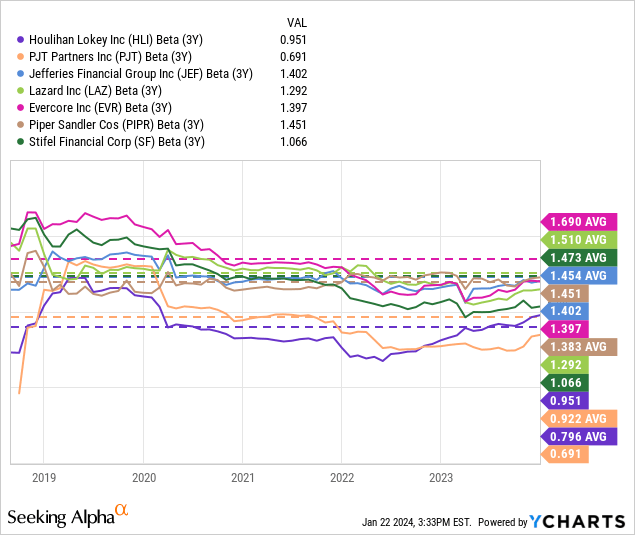

The combination of a large restructuring business, a large valuation advisory business, and a focus on middle market investment banking results in HLI exhibiting less cyclicality than peers. Further evidence for this can be seen in the fact that HLI’s stock has exhibited a lower beta than peers. Since inception, HLI’s average 3 year trailing beta has been 0.8. Comparably, over the same time, PJT, JEF, LAZ, EVR, PIPR, and SF have exhibited average 3 year betas of 0.92, 1.45, 1.51, 1.69, 1.38, and 1.47 respectively.

All else equal, investors tend to place a premium valuation on less cyclical businesses relative to more cyclical businesses. Evidence for this can be seen in the fact that despite the low grow consumer staples trades at a forward P/E ratio of 19.7x and is expected to experience 3-5 year EPS growth of 7.5%. Comparably, the industrials sector is expected to experience 13.3% growth over the same period and trades at a forward P/E ratio of 20.6x.

Thus, given the fact that HLI’s business model is somewhat less cyclical than peers I believe it should trade at a premium assuming similar growth prospects.

HLI Investor Presentation

Reasonable Valuation vs Peers

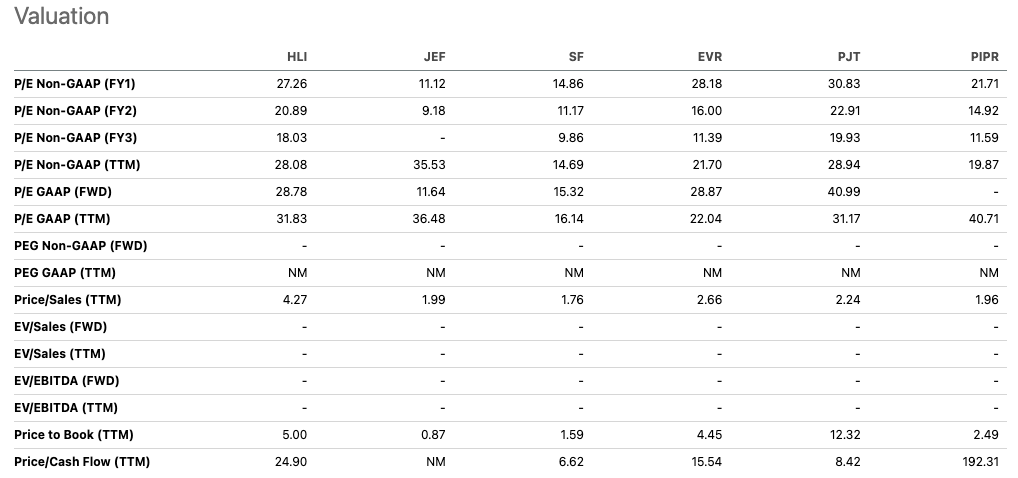

As shown by the chart below, HLI is currently trading at a premium to peers. HLI trades at a FY 2024 forward P/E ratio of 27.3x and FY 2025 forward P/E ratio of 20.9x. Comparably, HLI’s peer group shown below trades at an average FY 2024 forward P/E of 19.5x and an average FY 2025 forward P/E of 14.8x.

While I view the current valuation premium as reasonable given HLI’s less cyclical business mix, I do not see much room for HLI to trade at higher multiples vs peers.

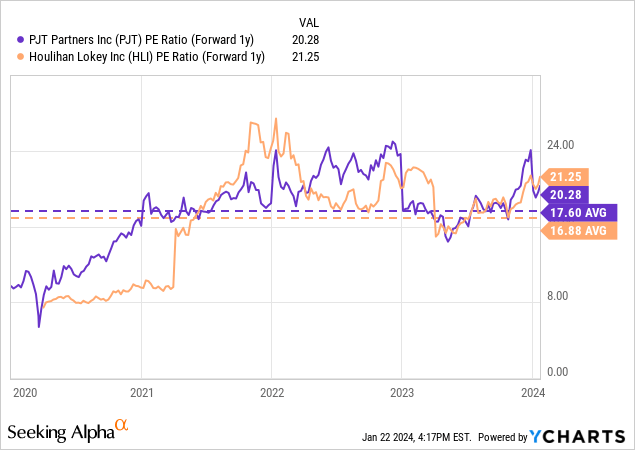

PJT is arguably HLI’s closest comp as its significant exposure to the restructuring business tends to make it less cyclical than most peers. Evidence for this can be seen in the fact that PJT’s historical beta is more inline with HLI than other high beta peers. As shown by the chart below, PJT has historically traded at a 1x average forward P/E multiple premium relative to HLI. Currently, HLI is trading at a modest premium. This is further evidence that HLI’s current valuation vs peers is reasonable.

Seeking Alpha

High Valuation Relative To Historical Norms

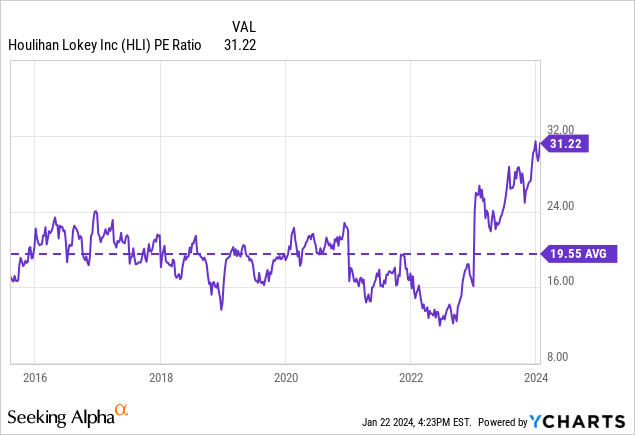

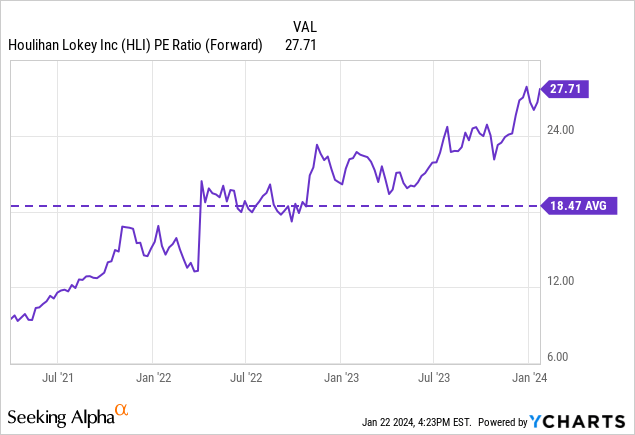

Historically, HLI has traded at an average P/E ratio of 19.5x. Comparably, the stock currently trades at a trailing P/E ratio of 31.2x.

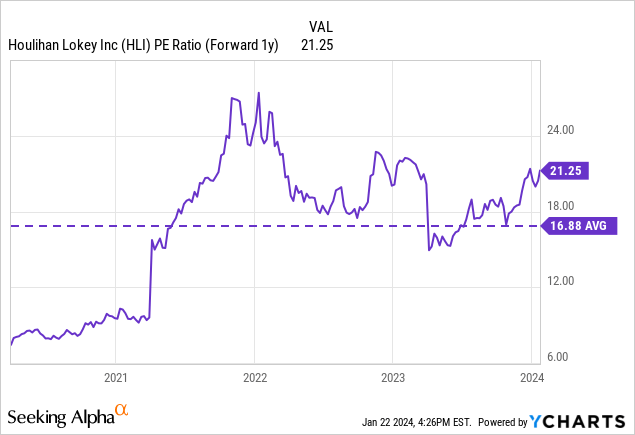

On a forward P/E basis, HLI trades at 27.7x FY 2024 earnings and 20.9x FY 2025 earnings. One thing to note is that HLI has a fiscal year which ends in March. Thus, the FY 2025 forward P/E is just 1.25 years in the future. The 20.9x forward earnings metric compares to a historical 1yr forward average P/E ratio of 16.9x.

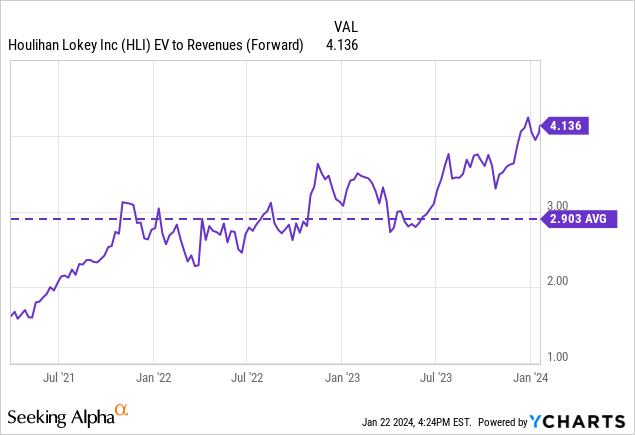

Another metric which suggests that HLI is trading at a high valuation relative to historical norms is the forward EV/Revenue ratio of 4.1x. Historically, the company has traded an average forward EV/Revenue of 2.9x.

Taken together, on the whole, I believe these metrics suggests that HLI is currently trading at a high valuation relative to historical norms. While it is possible that HLI’s valuation increases a bit from here I believe the ceiling is fairly limited.

Furthermore, I believe it should also be noted that FY 2025 EPS consensus estimates currently call for 30.5% EPS growth vs FY 2024 EPS. I broadly agree with the consensus estimates that EPS will accelerate over the next year due to an improving investment banking environment. However, I would note that this outcome is heavily dependent on macro-economic conditions. In the event that the investment banking advisory market is not as strong as anticipated over the next year, HLI could see significant downside as current valuations have priced in substantial earnings growth.

Acquisition of Triago

On December 21, 2023, HLI announced that it had agreed to acquire Triago. Triago is a leading provider of capital raising services, secondary transaction advisory, and strategic solutions for GPs and LPs in the global private equity market. The deal is anticipated to close in the first half of 2024.

While HLI already had a private funds group, this acquisition will significantly bolster its presence in the private capital space. I view the deal as a positive as the private capital space is rapidly growing and will provide HLI with additional revenue diversity. That said, I don’t view the deal as being large enough to materially impact near-term earnings forecasts.

Q3 FY 2024 Earnings Preview

HLI is expected to report Q3 FY 2024 results on February 1, 2024. Consensus estimates call for the company to reported Adj. EPS of $1.14 and GAAP EPS of $1.05. Revenue is expected to come in at $495 million. As shown by the table below, recent estimate revisions have been negative. Despite recent negative revisions, HLI continues to trade near a 52 week high. Thus, my feeling is that market expectations are fairly high going into this quarter. I expect any comments regarding forward guidance to be particularly important given the market expectations for significant earnings growth over the next 1-2 years.

Given the stocks’ high valuation, I do not view the stock as highly attractive heading into the release. I expect management to provide additional context regarding the recently announced Triago acquisition.

Seeking Alpha

What Would Make Me More Bullish

Holding all else equal, a lower valuation would make me more bullish on HLI. Specifically, if the stock were to trade inline with peers then I would find HLI highly attractive due to its less cyclical business model. On an absolute basis, I would find HLI more attractive if the FY 2025 forward P/E ratio were to come down below the historical 1yr forward P/E average of 16.9x.

Conclusion

HLI is a high quality investment banking advisory company with a solid history of delivering strong returns for shareholders.

The company has a differentiated business model which results in a less cyclical business relative to most of its peers. For this reason, I believe that HLI should trade at a premium relative to peers.

HLI trades at a moderate premium to its peer group and inline with PJT which has a relatively large restructuring business. I view HLI’s current valuation as reasonable vs peers.

HLI is trading towards the high end of its historical valuation range based on most key metrics. For this reason, I view upside as fairly limited at current levels.

I am initiating the stock with a hold rating and would consider upgrading the stock if the valuation picture improves.

Q2 2024 Earnings Call Transcript")