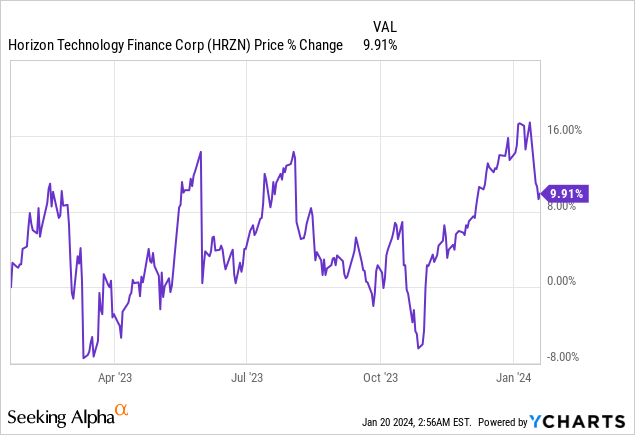

ryasick

Horizon Technology Finance (NASDAQ:HRZN) is a well-run BDC that invests in a small number of core industries that are historically neglected by the banking community. The BDC runs a tech-focused investment strategy and has seen double-digit net investment income growth in the last year. Although I expect weaker NII growth in FY 2024, Horizon Technology has very strong dividend coverage. The BDC’s shares currently provide dividend investors with a very well-supported 10% yield. Horizon Technology’s shares are trading at a high premium to net asset value, but the risk profile is favorable for investors.

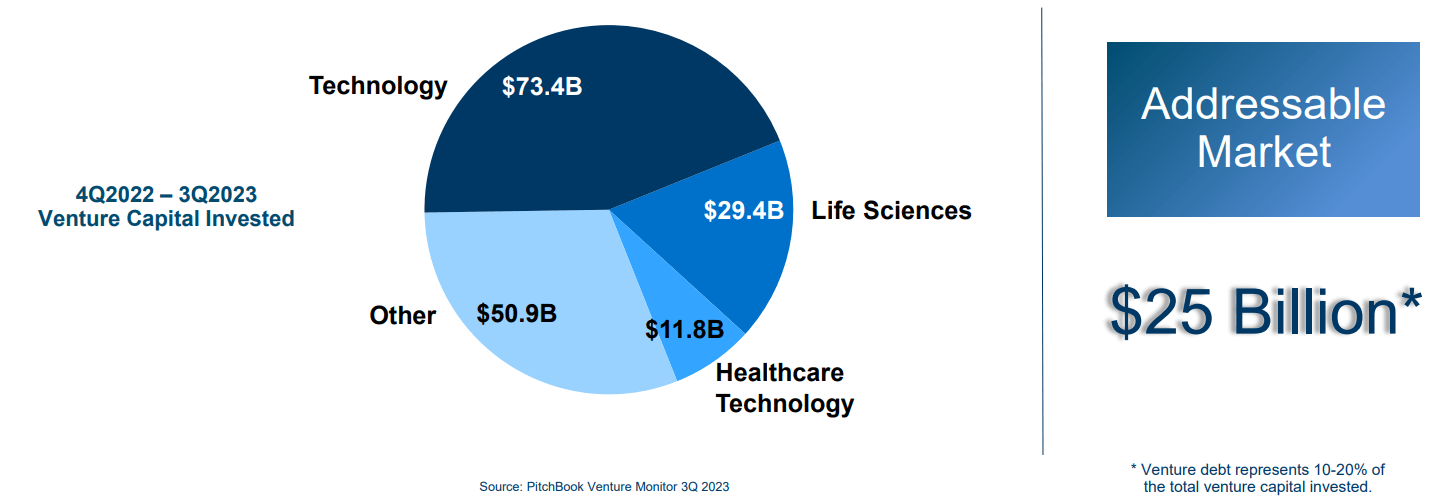

Underserved market and investment focus

What distinguishes Horizon Technology from other BDCs is that the investment firm invests mainly in a small number of very narrowly defined niches such as technology, life sciences, and healthcare technology. These companies are often of a start-up nature and don’t have the required financial background (history of revenue and cash flow growth) to qualify for typical bank loans. BDCs like Horizon Technology and Hercules Capital (HTGC) have moved into this market and established themselves as capital providers for venture-backed companies in their core industries.

Horizon Technology

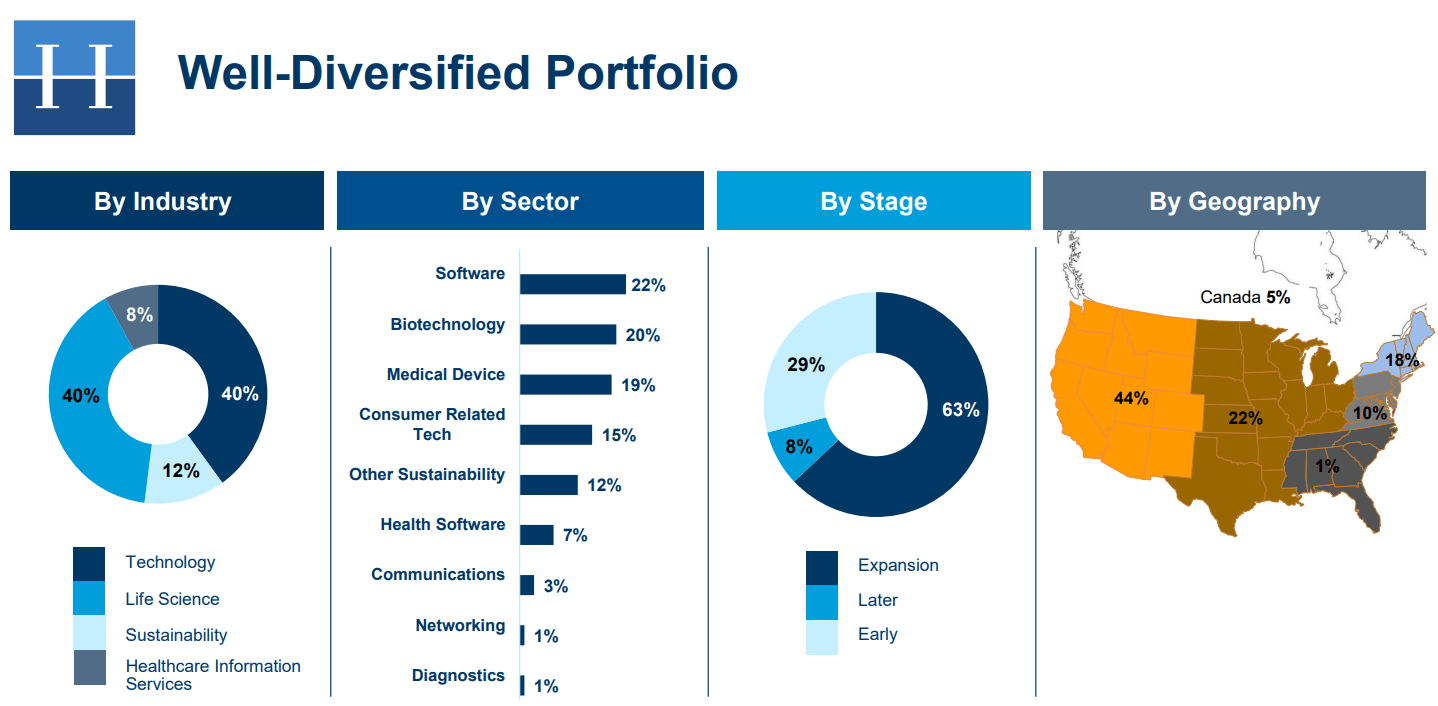

Horizon Technology is externally managed by Horizon Technology Finance Management LLC and has a market cap of approximately $425M. Technology and life sciences are the two largest areas of focus for the BDC with both of them having approximately 40% investment shares in the portfolio, as of the September quarter. Other investments, which help diversify Horizon Technology’s investment profile, but which are not nearly as important as the first two categories, are sustainability investments, with a share of 12%, and healthcare information with 8%. Mostly, Horizon Technology invests in companies that fall into the expansion stage of their business cycles, meaning they already have an established product/service and generate growing revenues.

Horizon Technology

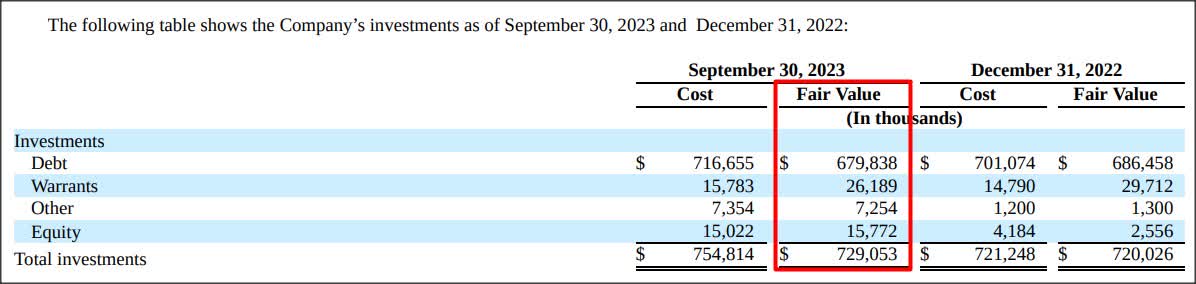

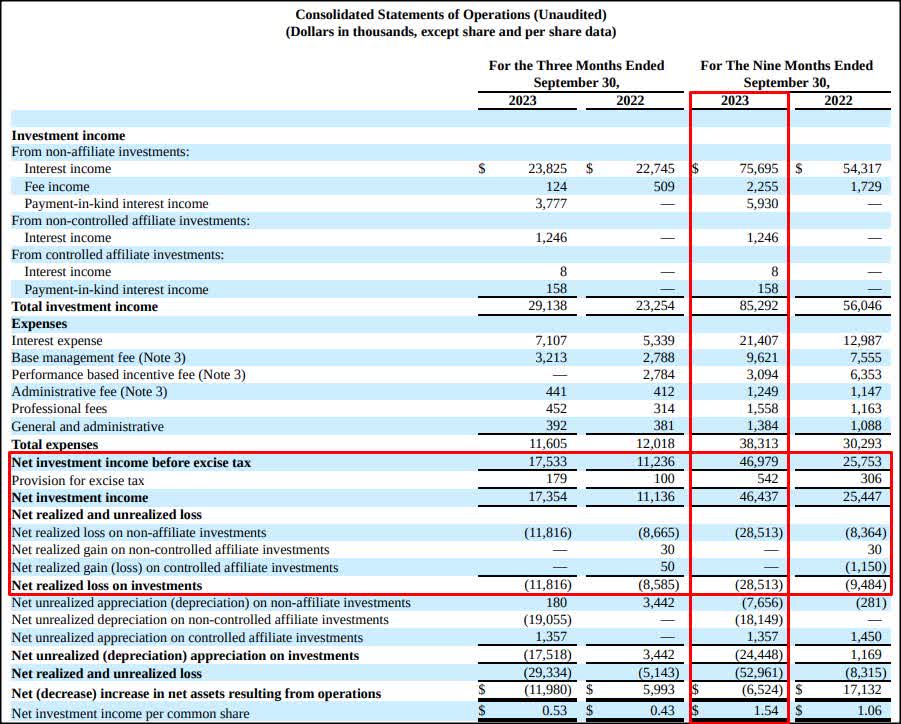

Horizon Technology chiefly provides investment capital to venture capital-backed companies as secured loans, but its portfolio breakdown by investment group shows that other investments are included as well, like equity and warrants. The total investment value of Horizon Technology’s portfolio was $729.1M as of the end of Q3’23 which represented a $9M increase (+1.2%) over the FY 2022 portfolio value.

Horizon Technology

According to last week’s portfolio update for Q4’23, Horizon Technology funded $63.4M of New Loans in Q4’23. The majority of this investment total, $32.5M, was made to a new portfolio company named VERO Biotech, Inc. which develops oxide delivery technology. The BDC also said that it received principal prepayments and partial paydowns of $48.3M during the fourth quarter. The implication of the Q4 portfolio update here, which precedes the company’s Q4’23 report, is that Horizon Technology continued to see robust demand for loan originations throughout the quarter and that the portfolio kept growing throughout the fourth quarter.

NII trend in FY 2023 and expectations for FY 2024

Horizon Technology could be up for a decent year if the U.S. economy does not weaken and enter recession territory. The BDC’s financials show an encouraging trend, especially as far as its net investment income, a BDC’s most important metric, and its interest income is concerned.

Horizon Technology achieved net investment income of $46.4M in the first nine months of the year which shows a year over year growth rate of a massive 82%. The sharp increase in NII is due to a surge in interest income from Horizon Technology’s portfolio companies: 95% of the BDC’s venture debt investments carry variable rates. The BDC’s interest income (from non-affiliated companies) soared 39% to $75.7M year over year.

Considering that the Federal Reserve is set to pivot in terms of its federal fund rate in 2024, I believe Horizon Technology will not be able to achieve a similarly spectacular increase in its net investment income this year. Nonetheless, the dividend should be more than protected, in my opinion, even if Horizon Technology were to see a decline in its interest income.

While the NII trend is positive, there is some potential area of concern: Horizon Technology sold some investments at a loss in FY 2023. The total realized loss in the first nine months of FY 2023 was $28.5M which was about three times larger than in the year-earlier period. The amount of realized investment losses is a potential risk to dividend stability and, together with NII and dividend coverage, should be carefully monitored.

Horizon Technology

Turning to Horizon Technology’s dividend coverage.

Horizon Technology achieved $46.4M in net investment income from January through September which breaks down to $1.54 per share ($1.06 per share in the year-earlier period). The BDC distributed $0.11 per-share monthly in dividends which translates to a cumulative dividend payout of $0.99 during this time.

This in turn calculates to a dividend coverage ratio of 156% which is an impressive measure. In the same period last year, Horizon Technology had a coverage ratio of only 118%. Given that the BDC’s NII soared last year and that the Federal Reserve has said that it plans to lower the federal fund rate in 2024, I believe the BDC’s dividend coverage ratio is cyclically inflated right now. In the longer term, I believe Horizon Technology will return to a 115-120% dividend coverage ratio which would still suggest that the dividend is well-supported by NII.

Historical NII growth and coverage

Looking at the BDC’s historical income and coverage trends, I believe my expectations are justified. Horizon Technology saw double-digit total interest income and NII growth between FY 2020 and FY 2022 and the coverage ratio greatly improved as well. The distribution, at least theoretically, could rise, but I am satisfied with the current yield. As the coverage ratio implies, both for FY 2023 (YTD) and in the two years before that, the distribution has a decent margin of safety, in my opinion.

| Historical NII Trend & Coverage | FY 2020 | FY 2021 | FY 2022 |

2-YR Growth |

| Total Interest Income ($M) | $42,192 | $54,411 | $77,366 | 83.4% |

| Net Investment Income ($M) | $20,749 | $28,220 | $36,187 | 74.4% |

| NII (per share) | $1.18 | $1.41 | $1.46 | 23.7% |

| Annual Distribution (per share) | $1.25 | $1.25 | $1.28 | 2.4% |

| Coverage Ratio (%) | 94.4% | 112.8% | 114.1% | – |

(Source: Author)

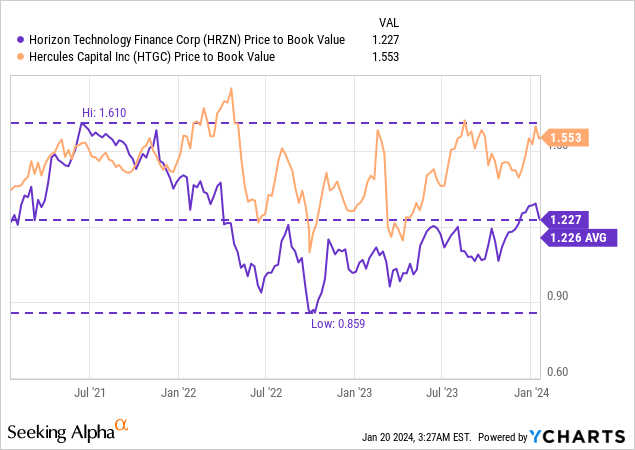

Horizon Technology vs. Hercules Capital

Technology-oriented BDCs have high NAV valuation multiplier factors, in part because they have delivered very good results over time. The leader in the niche is Hercules Capital which is a very well-run BDC with consistent returns (I own HTGC shares). Hercules Capital is about 6X bigger than Horizon Technology from a market cap point of view and has achieved impressive portfolio and NII growth results.

As the leader in the space and with a more than two-decade-long track record, HTGC has managed to achieve one of the largest NAV premiums in the market: 55%. Horizon Technology is not a bargain either and shares currently trade at a 23% premium to net asset value… which is the same premium as the average net asset value premium in the last three years. Given the strength of the yield, strong uptrend in interest income/NII since FY 2020, and decent margin of safety, I believe that Horizon Technology is deserving of a premium to book value. I have confidence that the dividend at the current rate is sustainable, and may even grow slightly going forward. I consider HRZN to be fairly valued here (~$12.75) and don’t buy into the BDC for capital upside. Horizon Technology, for me, is chiefly an income play at this point.

Unique risks with Horizon Technology

As opposed to other business development companies, Horizon Technology is not very diversified across the industry spectrum. The BDC has a focus on technology and life sciences companies, chiefly, which means should these sectors under-perform, Horizon Technology may suffer more than a more diversified BDC. What would change my mind about Horizon Technology is if the company were to see a drop in its dividend coverage ratio below 115% or if it was forced to realize a large amount of investment losses.

Final thoughts

Horizon Technology is a well-run business development company with a growing investment portfolio and a unique twist in its strategy: it focuses on venture-backed tech companies that are neglected by the finance industry. The BDC benefited greatly from a surging federal fund rate last year which boosted its NII, but even in a low-rate world, Horizon Technology should be able to support its current $1.32 per-share annualized distribution. Although Horizon Technology is not cheap based off of net asset value, and is likely fairly valued, the BDC makes a strong value proposition for FY 2024 and beyond.

Q2 2024 Earnings Call Transcript")