BeritK/iStock via Getty Images

Introduction

I have been looking forward to sharing my updated thoughts on Hims & Hers Health (NYSE:HIMS). I took a week to digest the earnings call in order to make sure I put together a thoughtful piece. I have published eleven articles on Hims going back to November 2021. To put this in perspective, I have only published 50 other stock articles in the six years that I have been a writer on Seeking Alpha.

To be a successful investor is to be a disciplined investor. For every one stock I invest in, there are hundreds I discard. I don’t invest in or write on stocks I haven’t psychotically analyzed from every angle nor do I write articles for the money. I write because it’s a passion. Seeking Alpha could pay me free.99 for this article and I’d still write it (Richard: don’t get any ideas). And speaking of money, I disclosed my original Hims purchase of about 50,000 shares at a cost basis of $5.50.

You can do the math.

Disclosure

In late 2023, I opened my own registered investment advisory firm, DocShah Financial. I won’t bore you with the details, but we’ve had incredible growth and officially crossed $1,000,000 in assets under management on March 4, 2024. Integrity is at the core of everything I do, and as such, please make sure you read my disclosure at the bottom.

Enjoy the piece.

“Who The Heck is Hims?”

This was actually a friend’s response after I said, “I own Hims.”

Fortunately for us all, Hims is a ‘what,’ not a ‘who.’

Hims and Hers Health is a telehealth company that primarily targets Millennials and Gen Z, offering them health solutions in five broad categories:

- Sexual Wellness (ooh la la)

- Hair Regrowth

- Dermatology

- Mental Health

- Weight Loss

Once again, I could bore you with the details of how massive the TAM is for each category, but I already did that here. This article is going to be different.

The moment you understand that a stock’s success is twice the byproduct of human psychology as it is fundamentals, the better investor you will be going forward.

Millennials and Gen Z are different from other generations; for better or for worse (if we’re worse, I apologize). Most of us grew up isolated. Notice, I didn’t use the word, ‘alone.’ We weren’t alone – we were connected to people 24/7/365… just, you know… through a device.

We were isolated.

We didn’t need to meet in person because we could meet through a screen.

What’s the result of this?

As a colleague of mine emailed me:

The result is, you get a bunch of anxious/nervous people who still need healthcare, but, if given the choice, would 100% choose to do it through a screen than in person.

And this is exactly what the market didn’t understand about Hims;

That Hims was a company born out of necessity. Not of choice.

And this precisely what I understood at $5 per share;

At $4 per share;

And, as I stood isolated, at $3 per share.

Valuation

We will value Hims via FCF and EPS.

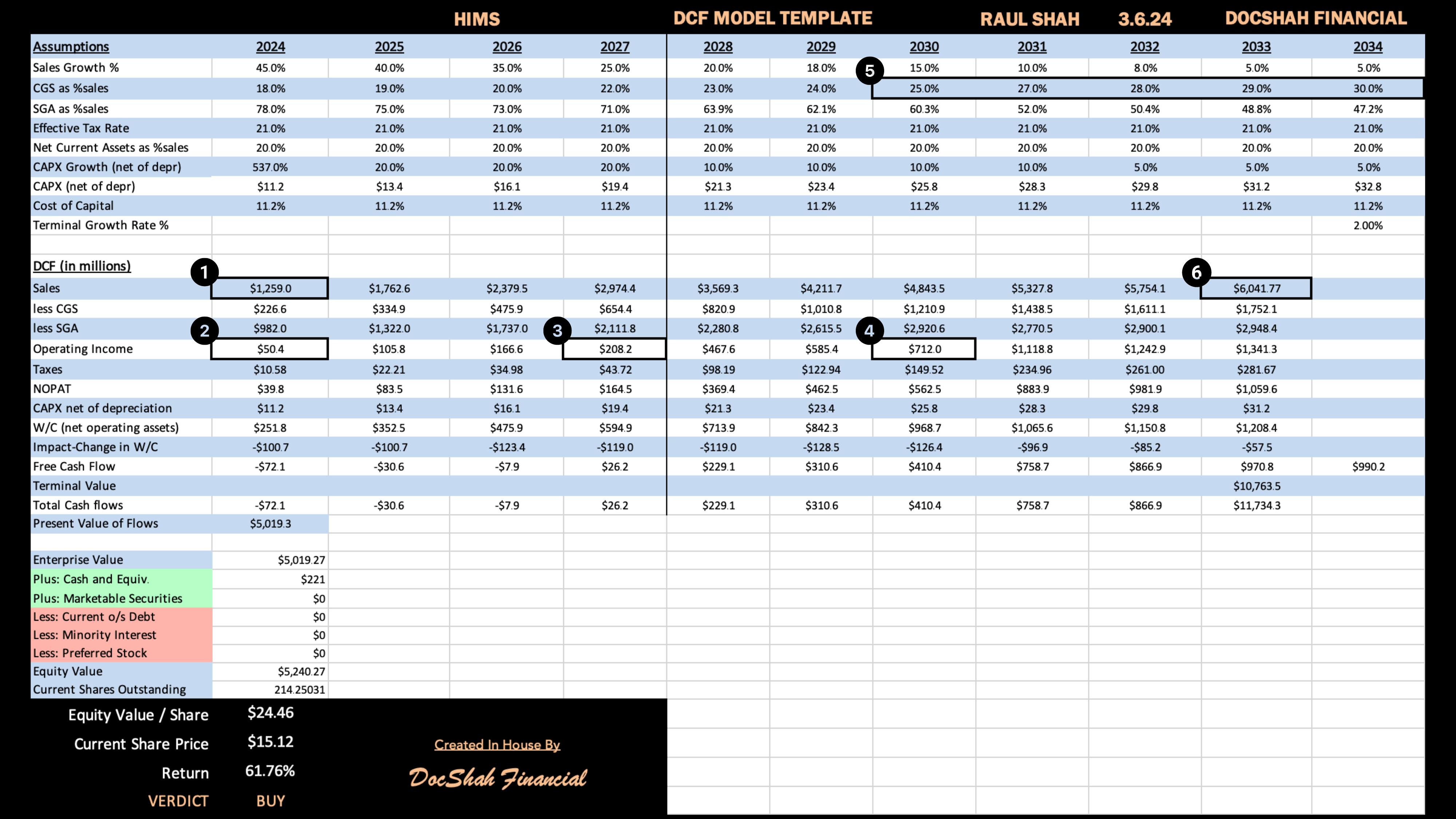

DocShah Financial’s DCF

DSF HIMS DCF (DocShah Financial )

I have six key checkpoints marked on my DCF in order to keep us in line as we make our way through the next ten years together. These six key areas are a combination of guidance from both CFO Yemi Okupe and CEO Andrew Dudum during the latest earnings call and my own forecasts.

Checkpoint 1: 2024 Sales

Yemi Okupe’s Guidance:

For the full-year, we are anticipating revenue of between $1.17 billion to $1.2 billion.

In my view, Yemi’s guidance appears overly conservative. To reach $1.2 billion in sales for 2024, a CAGR of just 8.3% per quarter would be required. To put this in perspective, Hims averaged quarterly growth rates of 10% last year:

- Q1: 14.1%

- Q2: 9.0%

- Q3: 9.0%

- Q4: 8.8%

The first quarter tends to have stronger tailwinds and as such, I would expect Hims to post solid earnings growth. I think 12.0% is a sensible estimate and if we get anything near that number, then we could coast the remaining quarters with 6% CAGR growth and still reach sales of $1.2 billion.

My forecast is:

- Q1: $276 million (12% sequential increase)

- Q2: $301 million (9% sequential increase)

- Q3: $328 million (9% sequential increase)

- Q4: $354 million (8% sequential increase)

Total 2024 sales: $1.26 billion

Checkpoint 2: 2024 EBITDA

Yemi Okupe’s Guidance:

It is our expectation that 2024 adjusted EBITDA will be between $100 million and $120 million.

I calculated EBIT (operating income) of $50 million for this year, which roughly equates to $110 million in adjusted EBITDA.

If you are confused, take the second to read this, otherwise keep it moving:

EBITDA excludes depreciation and amortization. Adjusted EBITDA excludes both of those I just mentioned AND includes stock-based compensation. So, in order to reconcile an adjusted EBITDA forecast with an EBIT forecast (operating income), you have to reverse all those transactions above. That means to go from adjusted EBITDA to EBIT, you add back depreciation/amortization and subtract out stock-based compensation. That’s why EBIT is a lot lower.

Checkpoint 3: 2027 EBITDA Margin

Yemi Okupe’s Guidance:

Our expectation is that we will achieve adjusted EBITDA margins of at least low to mid-teens by 2027.

I think this is reasonable and so I forecasted the midpoint of guidance with an expected EBIT margin of 7%, which is pretty much in line with a mid-teen adjusted EBITDA margin.

Checkpoint 4: 2030 EBITDA Margin

Yemi Okupe’s Guidance:

Our long-term adjusted EBITDA margin goals are 20% to 30%… our expectation is that marketing as a percentage of revenue will be in the mid-30s to low-40s by 2030.

I have EBIT in 2030 to be $712 million, which equates to a 15% EBIT margin, which will fall somewhere in Yemi’s target range for adjusted EBITDA margin.

I think Hims could have lower gross margins in the future, which would put more pressure on them to cut back on advertising. Right now, this isn’t necessary because there aren’t enough legitimate competitors to force Hims to be more competitive on pricing. As that changes, I think Hims could be forced to reduce advertising spend to conjure up a profit, which in turn, could stifle their future sales growth.

So, I did two things:

- I lowered SGA expense to company guidance.

- I slowed sales growth slightly more aggressively, starting in 2028.

Vertical Line

You’ll observe a vertical line marking the division between the years after 2027. From 2028 to 2030, I maintained the same base rate improvement in SGA. However, I then applied a multiplier of 0.9x to account for a 10% reduction in marketing as a percentage of revenue. Subsequently, during the period from 2030 to 2033, I applied a more aggressive approach, using a multiplier of 0.8x to reflect Yemi’s guidance that marketing as a percentage of revenue will ultimately fall in the mid 30% range.

Checkpoint 5: Gross margins

Yemi Okupe’s Guidance:

Over time, we view gross margins going to more of the mid to high-70s… the path to kind of the mid-70s that we’ve guided to is definitely going to be probably more of a multiyear journey like that’s not going to happen over the course of like a couple of quarters.

Yemi’s optimism may be overlooking some potential challenges. While it’s tempting to assume that the company’s favorable conditions will persist into the future as Hims currently outpaces competitors in the telehealth sector by various key measures, it may be unrealistic to expect such high margins indefinitely.

An industry in which a company is producing 82% gross margins is likely to attract many other suppliers, thus driving down price. As competition in the telehealth market intensifies, I anticipate that companies within this space will begin offering similar products, with service quality becoming the primary differentiating factor. However, enhancing service typically entails greater costs compared to product differentiation.

Merely warning investors of a decline from 82% to 75% in profit margins may not suffice. Given the potential for further erosion, investors could anticipate more substantial margin decreases. To adopt a more conservative approach, I’ve created a glide path down to 70%, rather than stopping at 75% as in Yemi’s guidance.

Checkpoint 6: 2033 Sales

Andrew Dudum’s Guidance:

We think we are building a $10-20 billion company.

While Hims’ management has not set any expectations for sales in 2033, CEO Andrew Dudum has explicitly stated he sees Hims as a $20 billion company.

If Hims generates $6 billion in sales in 2033, as in my forecast, it would necessitate a P/S ratio of about 3.3x to be a $20 billion company. All of these numbers are reasonable.

Fair Share Price

Factoring in management’s complete guidance, my own forecasts, and some conservatism, Hims’ fair share price is $24.46. This represents potential upside of 62% from today’s current level of $15.12 per share.

Zooming Out

In any discounted cash flow analysis, the last step involves zooming out to view the big picture.

To address the question of whether projecting sales to be $6 billion is overly ambitious or not, I can essentially reframe it as, ‘Will Hims become a 7x larger company in 10 years?’

Well, to put this in perspective, sales would have to grow at a CAGR of 24% for Hims to be a 7x bigger company in 2033. I think most would agree this is well within the realm of possibility.

So, yes, my DCF is reasonable in the big picture.

A Lesson in Zoology with DocShah

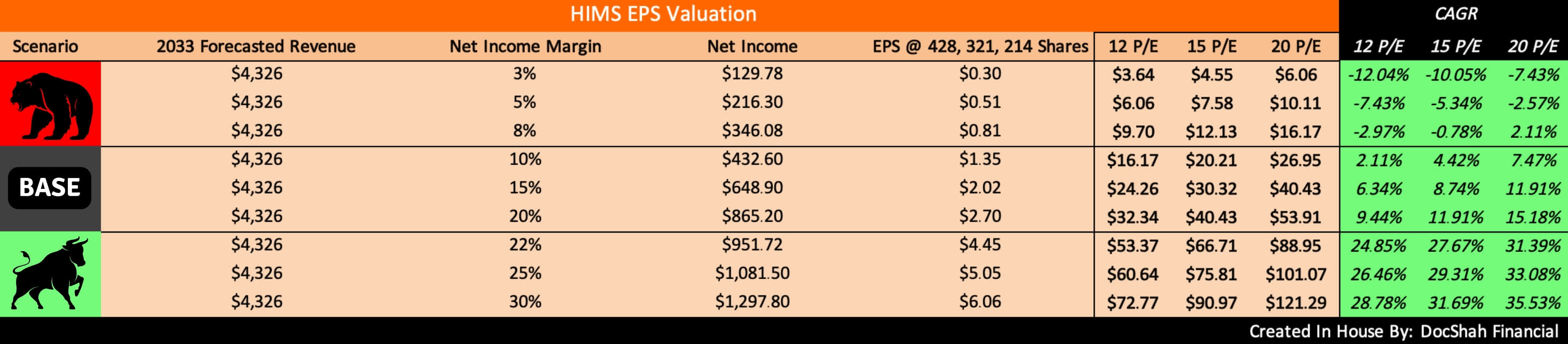

DSF HIMS EPS Table (DocShah Financial)

We can also value companies using EPS instead of FCF. In the above chart, we have a bear case, base case, and bull case. I made a few assumptions:

Bear Case: Share count increases by 2x to 428 million

Base Case: Share count increases by 1.5x to 321 million

Bull Case: Share count remains the same at 214 million.

The convenient thing about the way I constructed this table is it allows you, the reader, to quickly pick all your assumptions and come up with your own fair share price.

For example, let’s say you’re neutral on the company and believe:

- Net income margins will be 15%

- Shares outstanding are 321 million

- Market assigns a 15 P/E

Then, the stock would be worth $30.32, which represents a CAGR of 8.74% per year from current levels.

I’d love to know which outcome you forecast so let me know in the comments below. Also, please understand these forecasts are general ranges.

Potential Catalysts

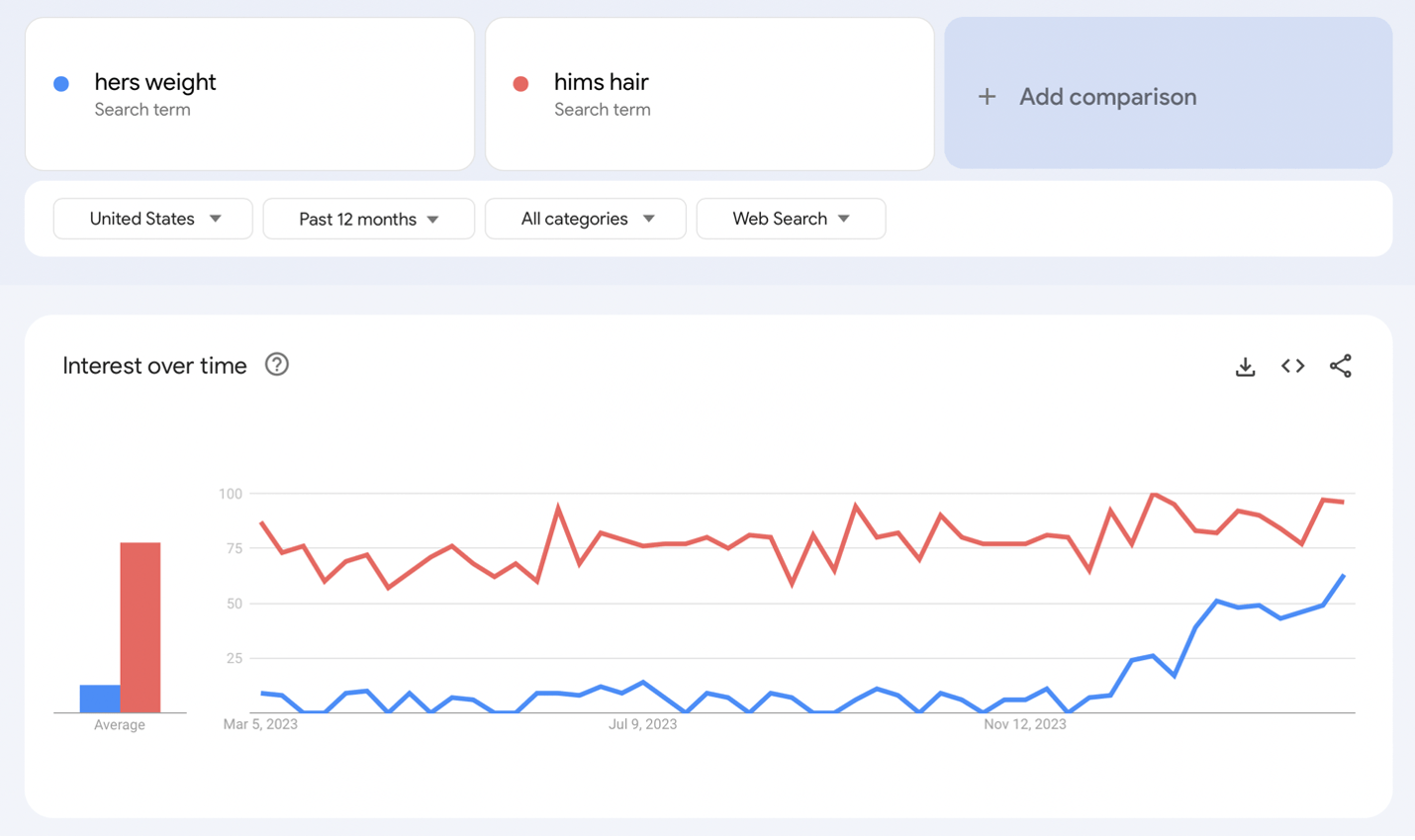

These are by no means sidenotes, but this article is already quite long. MedMatch, which is Hims’ AI software that utilizes machine learning and leverages data points from its patients, and the new Hers Weight Loss category could both provide immense value to the company’s market cap. However, as of right now, I’d say both are currently in their infancy stages, which makes it difficult for me to accurately put a value on them. So, in the spirit of prudence, it’s best I wait a little bit of time to quantify their impact until they undergo more develop. However, I wanted to at least acknowledge these catalysts and will begin factoring them into forecasts as they both mature. I do think both MedMatch and Hers are “waiting in the wings” and am excited to see them mature.

Hers Weight Google Trends

Google Trends Comparison: Hers Weight vs. Hims Hair (Google)

As a quick illustration of my point that Hers is a sleeping giant, take a look above at the Google Trends from the past year. ‘Hers weight’ is very quickly approaching the same search interest as ‘Hims hair,’ one of the companies most popular categories.

Get Off My Lawn

I am going to address some common arguments about Hims people tend to yell in fury to see if any hold validity.

Hims has no moat…

Those who claim Hims has no moat could not be further mistaken. First of all, the value proposition supersedes the moat. Investors who fixate on the latter are “putting the cart before the horse.” It’s akin to complaining about results without focusing on the process. This is something that gets ingrained in you from a young age when you’re an athlete, which by the way, I am a professional baseball player too.

Second, you can claim any company doesn’t have a moat in their first few years. What moat did Netflix have when it started?

What made Netflix special was its value proposition. Specifically, Netflix’s value proposition was that it was:

- Easier to use

- More convenient

- Earlier to market (perhaps more a competitive advantage, but why split hairs)

- More cost effective

- Had better branding

- Had customer-friendly policies.

Over time, the company expanded upon its value proposition by adding streaming, original content, games, etc. It is exactly this value expansion that is what investors unknowingly refer to as a moat.

By the way, if the list above sounds familiar, that’s because it should. All of those value propositions can be applied to Hims.

Specifically, Hims’ value proposition is that it provides a 24/7, digital health and wellness service for nervous/anxious people who desperately need those services, but desire to, by nature, avoid meeting in person for stigmatized healthcare concerns. The custom formularies, vertical integration, incredible branding, ease of use, convenience, and simplicity, all provide the necessary foundation for a great user experience.

Over time, the company’s value proposition will create a recognizable moat. Then, if another company wants to compete for market share, it will have to top Hims’ value proposition, not cross its moat.

CAC this, CAC that…

I think we need to put customer acquisition cost in perspective. Hims is a company that has:

- 65% YoY revenue growth

- 82% gross margins

- $221 million in cash

- $0 in debt

- 14% inside ownership

- Founder led

- Massive, as in extremely massive, TAM

- Millions of followers across socials

- Retired 237,000 shares for $2 million at $8.42 average price per share.

Yet, some investors choose to fixate on customer acquisition cost as if it negates all of the above. If the company’s growth was negative, then I’d say high customer acquisition costs turn from benign to malignant.

I can look at any company in the world, find one particular negative, fixate and then write a PhD dissertation on it. This would be a mistake, as, going back to my earlier point, investing is primarily psychological not logical. There is a significant change taking place in society on how younger generations prefer to access healthcare. A high customer acquisition cost in a sea of great fundamentals is not going to halt that dynamic from progressing.

Thinking a high CAC will blockade this tsunami of a societal shift taking place in healthcare is like worrying that a pebble will block a river from reaching the ocean.

The fact is that Millennials and Gen Z have radically different psyches that no telehealth company has identified and targeted the way Hims has done. Also, anyone who knows advertising will tell you that ads become exponentially more expensive the more targeted they are, so it makes sense that Hims’ highly targeted campaigns are indeed, expensive. If this pursuit of the perfect customer, expensive as it is, brings in sticky patients who pay month after month, then the juice is worth the squeeze.

90% + of revenue is recurring revenue…

Speaking of customers who pay month after month, Hims does not have me convinced on their reported recurring revenue percentage. The only reason I am a little suspicious is if you look at the iOS App store (or the internet), there are a lot of 1 star customer reviews claiming that the company either won’t cancel their subscriptions or that the subscription shows cancelled, but still charges them month after month.

Are these sales in error classified as recurring revenue? If I make and cancel a subscription in January, but then get billed in error one time in my lifecycle in February and/or March, have I turned into a recurring customer? I’m not sure.

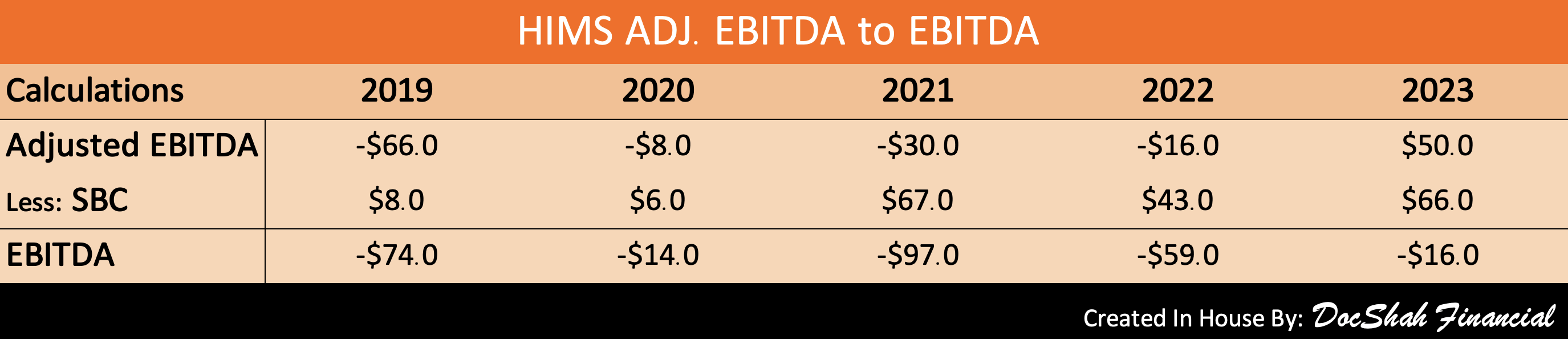

Adjusted EBIDTA… *sigh

HIMS Adj. EBITDA vs. EBITDA (DocShah Financial )

One of the big problems with adjusted EBITDA is that it includes stock-based compensation. Therefore, the higher SBC is, the higher adjusted EBITDA is, and alas the problem starts to become obvious: the more you increase SBC, the more profitability you portray.

Does this dynamic accurately illustrate a business’ profitability? If we accept that SBC is an expense to shareholders (which it is), then how does one logically reconcile increasing a cost (SBC) increases your profit (adjusted EBITDA)?

One can’t because it makes no sense.

So, we have to remove SBC in order to convert from adjusted EBITDA to EBITDA. As far as the shareholders are concerned, it’s evident that Hims is still generating negative EBITDA, as these earnings are offset by management’s ever increasing compensation.

By the way, in case you’re wondering, adjusted EBITDA primarily serves as an evaluation metric in private equity, rather than for public shareholders seeking to accurately assess future cash flows. While Hims might be more accustomed to that realm, I believe emphasizing free cash flow instead of adjusted EBITDA in their earnings calls would be more beneficial.

Risks

Please understand there are significant risks to investing in Hims and Hers Health. The company has still not proven one full year of profitability and there is no guarantee it will. Investors need to be prepared for the worst-case scenario and miscellaneous risks. I will touch on several important ones below.

Low Barrier to Entry

The telehealth space is a competitive environment and as such, first to market advantage may not hold much significance. Many investors discuss the threat of Amazon stealing market share away from Hims. While Amazon would certainly be a competitor, the longer Hims continues to deliver outstanding customer value, the more likely that threat becomes alleviated.

Fun fact – my first ever article for Seeking Alpha was for Dick’s Sporting Goods (DKS). It was also my largest ever position at the time ($25,000) and I remember my dad thinking I was crazy, but I had done the research and knew the stock’s intrinsic value. Back then, the stock was hammered down to $23 per share on fears Amazon was going to put them out of business. It was absurd – you had a company with 70 years of operations, consistent EPS growth, founder led (son led at that point), $164 million in cash, and no debt – you can see where the stock price is now. Spoiler: it’s almost become a 10-bagger. The point of this anecdote is that Amazon doesn’t crush every business it competes with just because it’s Amazon.

Regulation

Government regulation runs rampant in the healthcare industry and will likely spread to the telehealth industry, which could significantly disrupt HIMS’ business operations.

Stock Based Compensation

Excessive stock-based compensation dilutes shareholders from materializing future profits after they [the shareholders] have made such significant investments of time and capital.

Fad Image

The company’s vibrant and cheerful branding may not translate well in maintaining its effectiveness as it expands into different markets and demographics. In its present state, some may argue that its branding could be perceived as overly casual for serious health issues.

Lawsuit

Hims could get sued at some point, perhaps for a mental health related misdiagnosis. Depending on the details of the case, it could be costly for shareholders. Hims distributes so many mental health prescriptions, it runs the risk of potentially prescribing someone or something in error.

10-K

For the company’s set of risks, please click here.

Takeaway

Hims and Hers Health is at the forefront of a significant societal change taking place. So far, the company has identified, capitalized, and executed on this trend and I expect that to continue.

You’ve heard enough about the financials and fundamentals. It’s time to truly be an astute investor and focus on the underlying psychology of the problem Hims is solving.

Millennials and Gen Z need healthcare, but not if it involves meeting another human being in person. This will not change anytime soon and thus far, Hims solves this dilemma better than any competitor.

What’s the most Millennial/Gen Z way I can end this piece?

Something something something *insert rocket emoji and shifty eyes emoji here.

Q2 2024 Earnings Call Transcript")