Yaroslav Kushta/Moment via Getty Images

Thesis

We started covering Miller/howard High Income Equity (HIE) CEF in 2023 with a Buy rating as outline here. The fund is up substantially since our rating, with the main drivers being the risk factors outlined in the original article:

Original Rating (Seeking Alpha)

We had advocated in the original write-up for a tightening of the discount to NAV, which was very wide at -8% given the 2024 term maturity. We got a 4% gain from the narrowing as well as a gain from the underlying equities. HIE is overweight energy and MLPs, asset classes which have lagged in the past months, hence the underlying equity delta contributed less to the performance than expected.

In this article we are going to revisit the fund, its standing, and outline why we would not buy the name anymore at the current levels, thus downgrading the CEF to a hold.

Term structure with the potential for a 1-year extension

The fund is set to terminate at the end of 2024, absent any cataclysmic market events:

The Fund will terminate on November 24, 2024, absent shareholder approval to extend such term. If the Fund’s Board of Trustees (“Board”) believes that under the current market conditions it is in the best interest of the Fund’s shareholders to do so, the Board may extend the termination date for one year, to November 24, 2025, without a shareholder vote upon the affirmative vote of three-quarters of the Board’s trustees then in office.

Source: Semi-Annual Report

As a shareholder please note that there is no ‘maturity term matching’ between the fund and its collateral, collateral which is composed of mainly equities. This translates into equity holders running the market risk associated with the underlying equities to a certain extent. We are making a caveat here, because we think mild pull-backs such as -5% will fall on the equity holders, while a significant market sell-off would see the manager extend the fund’s termination date to 2025. We would not expect the portfolio manager to liquidate the fund holdings during significant market sell-offs.

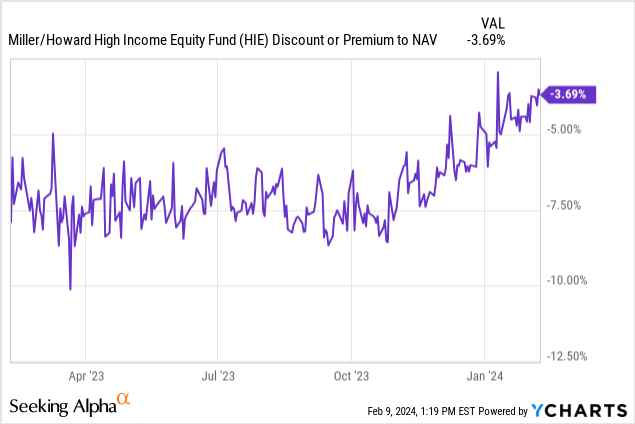

Discount has narrowed as we approach maturity

The CEF’s discount to NAV has narrowed as we approach its maturity date and the market has a risk-on appetite:

Since we started covering the name, more than half of the discount has disappeared. Please note this will go to flat to NAV as we close in on the maturity date, hence you can only bank on another +3.69% gain from this risk factor. Conversely, if we do get a significant risk-off event, we expect the discount to widen again since the market will price the 1-year extension.

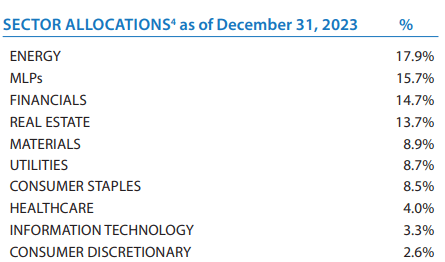

The fund is overweight Energy

The fund is overweight the Energy and MLP sectors:

Sector Allocations (Fund Fact Sheet)

While Energy and MLPs have lagged given commodity prices, Real Estate and Materials have seen a bump-up in prices given the unwind on further Federal Reserve hikes, compared to when we started covering the name. We feel MLPs are a dividend play at this stage of the macro cycle, with little gas in the tank for significant capital appreciation, while Energy still has two months of seasonally weak performance.

The fund’s build is a low beta take on the market, which explains its slow grind up, lagging the tech heavy S&P 500. Expect more of the same, absent a significant market sell-off.

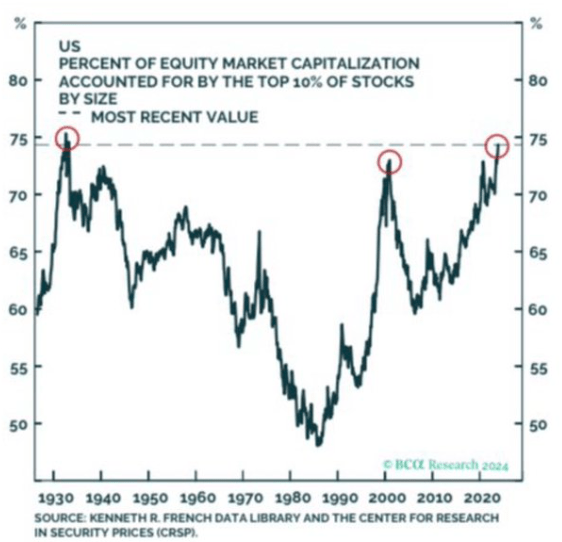

Markets are currently too exuberant

In our opinion we are seeing ‘dot-com’ type of performances in certain sectors of the market, with a crowding of trades in semi-conductors and the ‘Magnificent 7’:

Top 10% of Stocks (Kenneth R. French Data)

Nobody can call a top, but the pattern is fairly ominous. We are by no means calling for a crash, but we will most certainly see a pull-back, potentially followed by either more weakness or a rotation into other names.

A pull-back will see HIE’s price decrease as well, even if the fund has very little in terms of tech exposure. Run of the mill market pull-backs see weakness across the board. We also anticipate a slight widening in the discount to NAV during a pull-back.

We are of the opinion that the longer we wait for a healthy pull-back, the more violent it will end up being. Right now we are seeing individuals jumping into the market on pure FOMO (‘fear of missing out’) rather than valuation driven analysis. This type of price action never ends well, because it is the same individuals who jumped in with no conviction that will jump out when the market moves significantly against them. True buy-and-hold investors have a solid thesis and they have long holding periods to account for interim volatility. FOMO individuals do not.

The CEF’s price point is no longer ‘cheap’

Given our outlook on the market and the fund’s narrowing of the discount to NAV, today’s price is no longer appealing for a ‘Buy’ rating in our view. We would actually trim a little the exposure to this name right here actually. Under a base case, a pull-back would be followed by a slow grind higher for the name into November, but markets are unpredictable.

Term funds present unique opportunities in normalized markets since the discount to NAV will narrow. Never expect the CEF to trade flat to NAV until a few weeks until termination though, especially for names where the collateral is not maturity matched. We feel the current -3.6% discount is about right, and we actually anticipate a slight widening during the next market pull-back. This factor is no longer appealing from an entry standpoint.

Conclusion

HIE is a term CEF, set to terminate in November 2024. We started covering the fund last year with a ‘Buy’ rating, based on the CEF’s collateral and its very wide discount to NAV. The fund has posted a large positive total return since our rating, driven by the outlined risk factors. The discount to NAV has narrowed significantly to only -3.6% now, providing for little further upside until a few weeks before the actual liquidation. We feel the overall equities markets are exuberant currently and expect a pull-back that would impact HIE as well. We are therefore downgrading the name to Hold given it is no longer cheap.

Q2 2024 Earnings Call Transcript")