Ruben PB/iStock via Getty Images

Shares of Hess Midstream (NYSE:HESM) have steadily marched to a 12-month high and have now returned over 20% including dividends in the past year. Since I last wrote about this MLP in early November, shares have returned over 14%. In that article, I argued that Hess Midstream was undervalued on a stand-alone basis and that Chevron (CVX) may seek to acquire it after completing its Hess (HES) purchase. The CVX-portion of my thesis remains, and I will focus on HESM’s underlying results to determine stand-alone fair value and a potential take-out price. I remain bullish on the stock.

Seeking Alpha

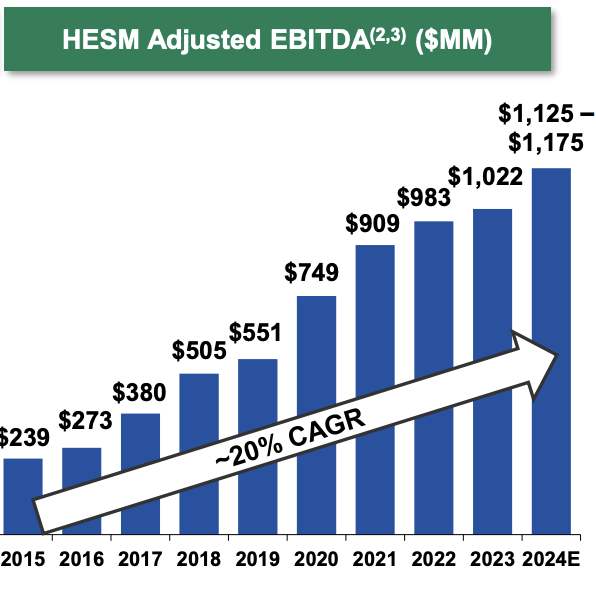

In the company’s fourth quarter, HESM earned $0.55 in adjusted earnings as adjusted EBITDA came in at $264 million, up 8% from last year. HESM generated $147 million of free cash flow. For the full year, HESM generated $1.02 billion in adjusted EBITDA, up about 4%, as HESM’s growth has accelerated through the year.

This growth was driven by increased utilization through its Bakken-centric network. Gas volumes rose by 24%, oil by 19%, and water gathering rose by 47%, aided by increased drilling activity by Hess. As you can see below, volumes were significantly stronger across each business line.

Hess Midstream

One significant positive from this growth is that HESM is no longer relying on minimum volume commitments (MVC) to protect revenue. In Q4, HESM received $1.8 million of MVC shortfall payments, down from $41.7 million last year. MVCs are very valuable in the near-term. Essentially, the producer (in this case Hess E&P) agrees to pay to use the pipe, whether it sends oil and gas through them or not. This gives the producers guaranteed pipe access, and it gives the midstream company guaranteed minimum revenue.

High MVCs help to provide strong certainty around revenue levels. However, when there is a large shortfall, markets tend to value that revenue less. That is because even long-term contracts come to an end eventually. And if there is low volume in the pipe, the next contract is likely to be less favorable with a lower MVC. MVCs help to insulate revenue from cyclical swings in oil & gas activity, but if a shale’s production is in long-term decline, they only delay the inevitable.

Fortunately, Hess is drilling actively and growing production. Moreover, with Chevron seeking to build scale and further develop these assets, production out of the Bakken should remain healthy. Not only is Hess Midstream growing, but the quality of its results has also improved.

It is also important to note that HESM’s contracts with HES stretch for several years. They also do not have commodity price exposure, and fees are CPI escalated. Fixed fees account for 85% of revenue with the remaining 15% based on cost of services, tied to CPI. Fixed fees with high MVCs and growing underlying production have created an environment where HESM steadily grows EBITDA across varied economic cycles.

Hess Midstream

As the company has grown, its cost base has increased, exacerbated a bit by inflation, and operating and maintenance costs rose by a third to $88 million. For the full year, free cash flow fell by $5 million to $606 million due to $14 million higher cap-ex and a $30 million jump in interest expense, which should be peaking now. The majority of its cap-ex budget is in growth projects, which should help HESM meet Hess’s growing production profile.

Alongside earnings, Hess Midstream increased its distribution by 2.7% to $0.6343, giving shares about a 7.4% yield. This is above the 1.2% required quarterly growth rate to achieve its 5% target and reflects these strong results. HESM also executed on $400 million in share repurchases in 2023, similar to 2022. The MLP also carries relatively low leverage at 3.2x debt/EBITDA. Given expected 2024 growth, leverage should be back below its 3x target by Q3.

I was also encouraged by 2024 guidance. Management expects 10% volume growth in 2024. This should translate to $1.15 billion of EBITDA in 2024, up about 12.5% from last year, continuing the acceleration we have seen in results in H2 2023. Total cap-ex spending will be $250-275 million, with $125 million of maintenance and $125-150 million of growth projects. That results in $685-735 million in free cash flow and $115 million of retained free cash flow after distributions. That translates to a ~1.41x distributable cash flow coverage ratio (operating cash flow less maintenance cap-ex divided by the distribution), in-line with its 1.4x target.

Beyond 2024, Hess now expects annual distribution growth of at least 5% through 2026. Underpinning this outlook, Hess completed tariff redeterminations, which increased the MVCs to provide protection above 2023 levels. These MVCs imply 10% gas throughput growth and 7.5% oil growth in 2024-2026. As such, it expects to grow adjusted EBITDA by 10% per year while holding cap-ex flat at $250-275 million. At its distribution growth, leverage would fall to 2.5x before any buybacks or M&A.

Hess Midstream

Essentially, with these MVCs, it has “locked in” about $950 million of run rate EBITDA in 2024, rising by about 10% from there. In reality, with Hess production well above minimums, actual results will be higher. These MVCs do through provide a high level of cash flow protection, which, combined with its fee-based contracts, is why cash flow is so steady and predictable. Based on its expected growth, HESM also will have at least $1.25 billion of financial flexibility over the next three years for buybacks while maintaining 3x debt/EBITDA. That should enable it to continue its ~$400 million/year pace of share repurchases.

I view HESM’s 5% distribution growth target very credible, given these factors, which is why I view shares as very attractive at a 7.4% yield, as that creates a combination for 12-13% long-term returns (distribution + growth), especially given its balance sheet flexibility to repurchase shares. I view fair value as a 5.5-6% yield, which translates to at least $42 as a fair standalone value for HESM.

At the same time, there is the potential CVX tries to acquire HESM after it completes its HES purchase. As I explained in my last article, CVX has done that in the past with Noble and Noble Midstream, and this would help simplify its capital structure. On their earnings call, Chevron management reiterated that the company expects to close the purchase of Hess in mid-2024, with a draft S-4 to be filed this quarter. I would expect CVX to wait 3–6 months before making any action on HESM, meaning a deal could be announced in late 2024.

As a reminder, upon close of Hess acquisition, Chevron will own 38% of HESM, but all existing contracts with legacy Hess remain in place. Chevron can appoint up to four members of the board; there are also 3 from GIP and 3 independent directors who will need to sign off on a deal that will also require unitholder approval, meaning it is unlikely to close before 2025.

Whether a deal materializes or not is unknown, but given the relative small size of HESM and Chevron’s past actions, I view one as likelier than not. I would expect CVX to need to offer at least low-$40’s to get GIP and public shareholders to approve the deal. In the meantime, investors collect a 7+% yield in a stable MLP that trades below fair value. With share price upside and distributions, there remains an over 25% return potential, and I continue to recommend owning Hess Midstream.

Q2 2024 Earnings Call Transcript")