arlutz73

HSY stock: yield surged to the highest levels in 10 years

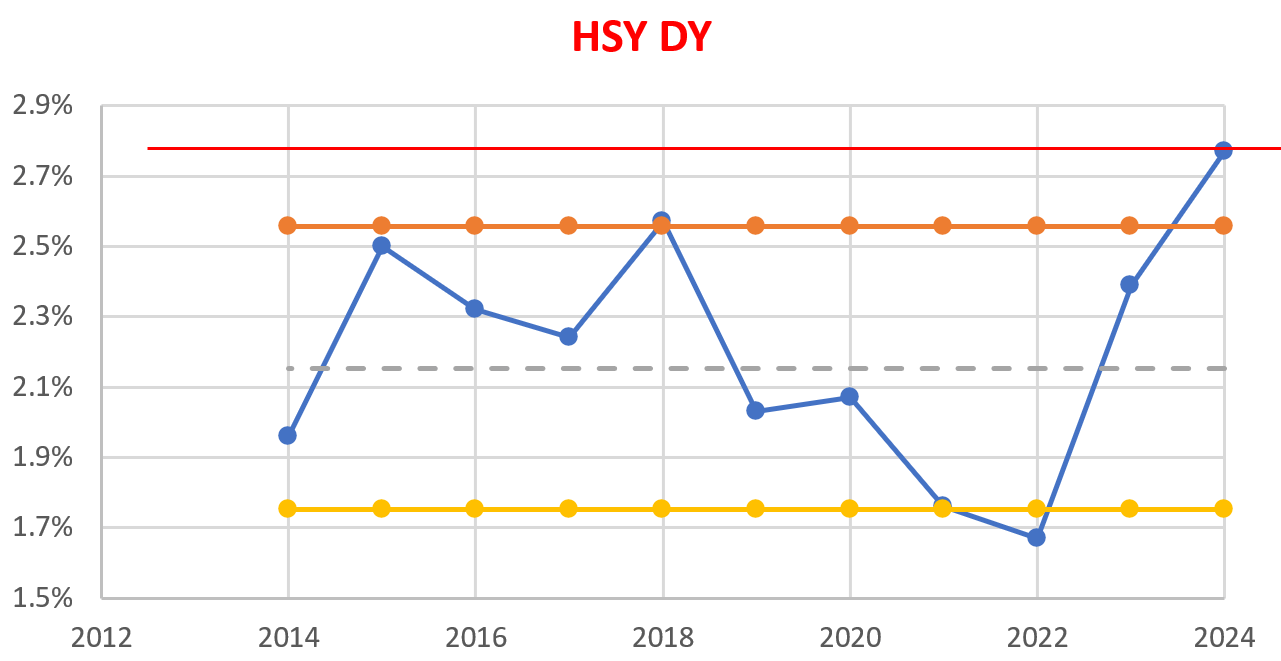

The Hershey Company (NYSE:HSY) showed up in our screening recently. In these screens, we set filters to look for companies that pay regular dividends and whose current dividend yields are usually below or above their historical averages. A simple glance at the chart below will show why HSY is near the top of our filtered results. HSY is currently yielding almost 2.8% on an FWD basis (shown by the solid red line). In contrast, its historical average yield (represented by the gray dotted line) is only about 2.15%. The current yield does exceed the average substantially and surpasses the 1+ standard deviation level (represented by the orange line with symbols) as seen.

Author

When the dividend yields are so out of whack, the first danger sign that comes to our mind is that the dividend payouts are unsafe, and a cut is imminent. However, in the case of HSY, we quickly ruled out this possibility.

For readers new to the company, HSY is the largest U.S. producer of chocolate and nonchocolate confectionery products. Even if you have not heard about it, you must have heard (or very likely had) its products. The company features some of the most iconic brands such as Hershey’s, Reese’s, Kisses, Cadbury, Ice Breakers, Kit Kat, Almond Joy, etc. The company has been growing its dividends consecutively for 14 years and has been paying dividends for more. The quarterly common stock dividend was recently hiked by 15%, to $1.37 per share. As a very profitable leader in this very staple sector, I have little doubt that the dividends are safe, and a cut is very unlikely.

However, we do see a few concerning signs lurking behind the high dividend yields, including the above-average payout ratio, high debt levels, profitability pressures, and a slight overvaluation. In the remainder of this article, we will elaborate on these issues and argue for a HOLD thesis because of them.

HSY’s dividends: room for growth can be limited

As just mentioned, the dividends are safe in our view. However, we do see some signs that point to limited growth potential in the years to come. The company has been facing some profitability headwinds recently (more on this in the next section). As a result, the recent dividend hikes are made feasible at the cost of increased payout ratios and a more stretched balance sheet.

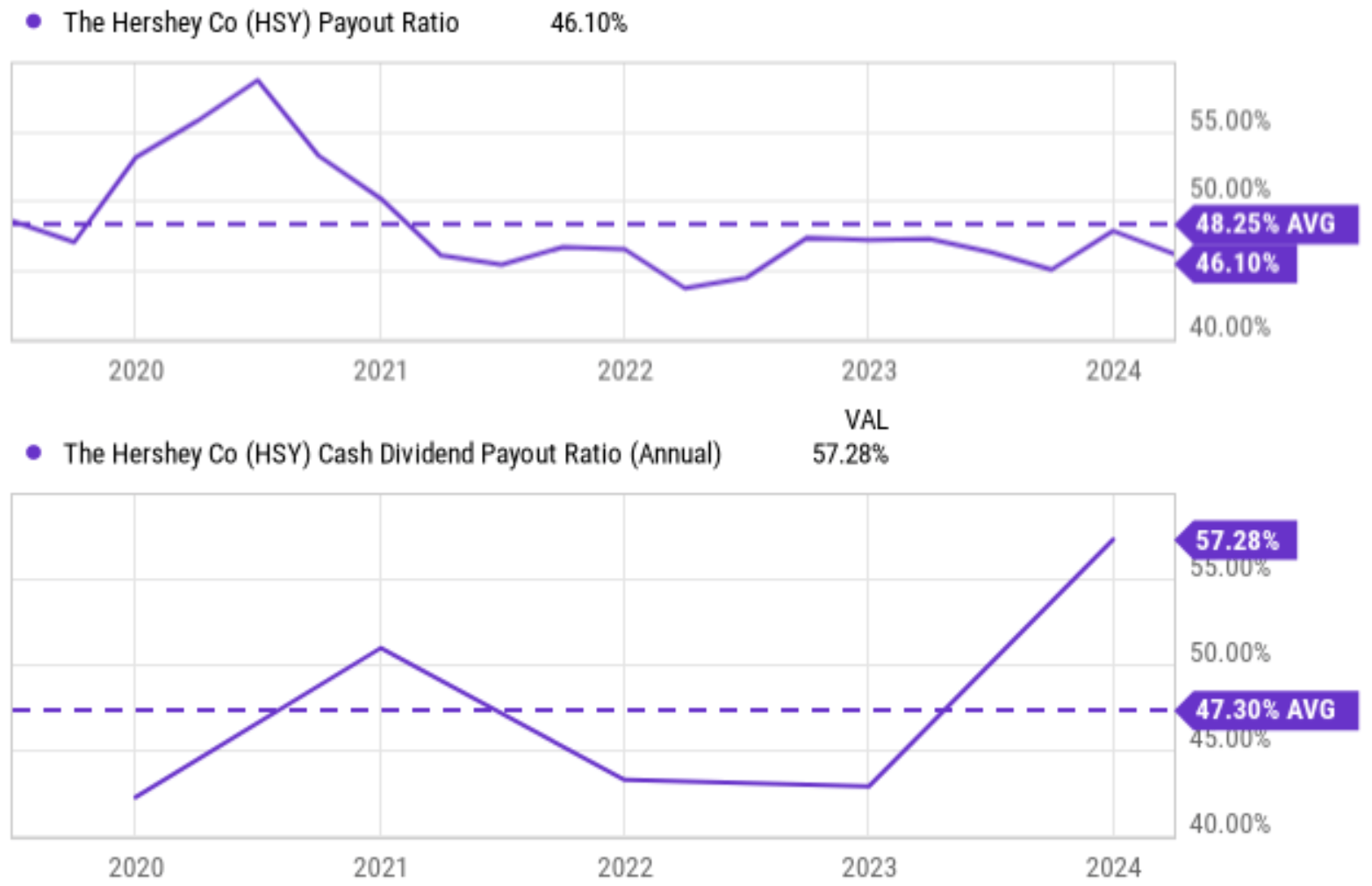

More specifically, the next chart below shows HSY’s payout ratio recently (top panel) and its cash dividend payout ratio (bottom panel) compared to its historical average. As seen, its EPS payout ratio currently sits slightly below its historical average of 48.25%. But looking ahead, the consensus EPS estimates for HSY point to earnings of $9.61 per share. At its current dividend payout of $1.37 per share quarterly, the implied payout ratio is over 57%, far above its historical average. The company’s cash dividend payout ratio displayed in the bottom panel paints the same picture. As seen, its current cash payout of 57.3% is also far above its historical average of 47.3%.

Seeking Alpha

The next chart shows HSY’s current liabilities and total liabilities in recent quarters. As seen, both its current liabilities and total liabilities have increased noticeably in the recent 2 years or so. In October 2021, its current liabilities were $1.9 billion, and they have since grown to $3.5 billion by March 2024. Total liabilities have grown from $6.9 billion in October 2021 to $8.3 billion by March 2024.

Seeking Alpha

HSY: profitability outlook and valuation assessment

At the root of the problem is the profitability pressure. I anticipate a challenging operating environment ahead. The top headwinds on my mind are the soaring costs for cocoa (an essential ingredient in chocolate products) and also increased costs. I do not anticipate cocoa prices to come down anytime soon given the inflationary pressure, geopolitical conflicts, high fuel costs, and high labor costs. Furthermore, I anticipate additional costs associated with the implementation of a new ERP (enterprise resource planning) system during the next few quarters. Finally, interest expense should climb, too, given the present interest rate environment and HSY’s increasing leverage, as just aforementioned.

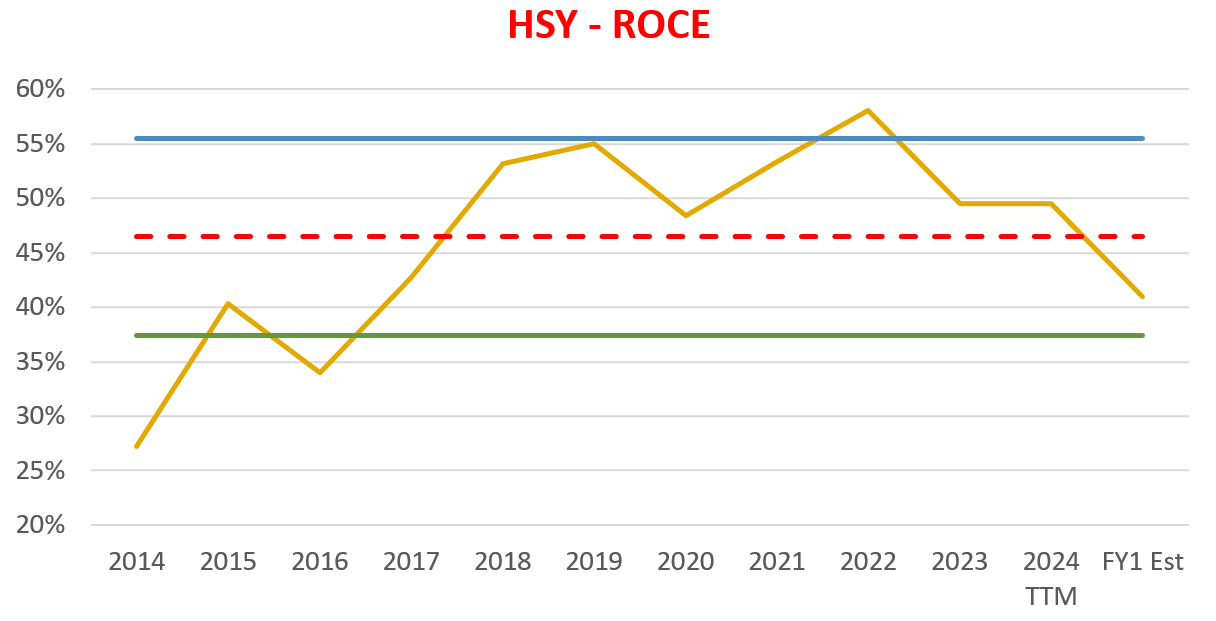

These headwinds are encapsulated in my estimate of its return on capital employed (“ROCE”) and the reinvestment rate (“RR”). The concept is detailed in my other articles. And here I will just quote the results for HSY in the chart below. As seen, its ROCE has been on average about 46% in the long term, and my forecast for its ROCE in the next year is about 42%. It is still a very profitable and respectable level compared to peers (or even other highly profitable businesses in more glamorous sectors such as IT). However, it is below its historical average by a large gap and I anticipate the pressure to persist given the factors discussed above.

Author

Finally, onto valuation. As a mature company in a stable sector, HSY is a textbook “defensive stock” in my mind that Ben Graham described in his book The Intelligent Investor. Hence, I will assess its valuation following the so-called Graham’s P/E described in the book. More specifically,

The Graham P/E is calculated as 8.5 plus twice the expected annual growth rate. In other words, in Graham’s mind, a business that stagnates and has 0% growth potential should be worth 8.5x P/E.

My method for estimating HSY’s growth potential involves the ROCE just mentioned and the reinvestment rate (“RR”). As just mentioned, its ROCE is about 42% currently. Its RR is currently about 8%. As such, HSY’s organic growth rate would be ~3.4% (42% ROCE x 8% RR = 3.4%). Note that this is the real rate. To obtain a nominal growth rate, I will add an inflation escalator of 2.5%, which brings the nominal growth rate to 5.9%. At an anticipated growth rate of 5.9%, the Graham P/E would be about 20.3x (8.5+2×5.9=20.3). At the price as of this writing, the market is valuing HSY at 20.6x FWD P/E, which leaves no margin of safety.

Other risks and final thoughts

In addition to the risks mentioned above, HSY also faces other industry-wide headwinds like rising sugar costs, which can squeeze profit margins. Additionally, consumer preferences can shift quickly towards healthier options, impacting demand for traditional confectionary products.

In terms of upside risks, the top one on my list is its ongoing expansionary initiative. A new 250,000-square-foot chocolate facility in Hershey, Pennsylvania is scheduled to be operational in mid-2024. This project is part of a $1 billion investment in HSY’s supply chain network, which also involves the addition of 13 production lines and upgrades to 11 existing ones in other North American facilities. I have a positive outlook for these actions in the long run given HSY’s promising long-term business prospects. But I do not think they can help with issues analyzed in this article in the next 2 years or so.

To conclude, The Hershey Company can seem very enticing with a dividend yield that is among the highest levels in at least a decade. I see no danger of dividend cuts given its leading position in a staple sector and very respectable profitability.

However, looking more closely, there are some worrying signs. Further dividend increases and earnings growth can be limited in the next few years because of rising input costs, above-average payout ratios, and also increased debt levels (which could be further exacerbated by elevated or even rising interest rates). Finally, The Hershey Company’s current P/E is close to a fair valuation in my assessment and does not properly price in the headwinds ahead. Given these mixed signals, I see no clear direction for the stock in the next 1~2 years, and thus rate it as a HOLD.

Q2 2024 Earnings Call Transcript")