Shares of shoe retailer Foot Locker (FL -27.92%) went up 22.3% during February, according to data provided by S&P Global Market Intelligence. It was a mostly quiet month for the company, but there was some vague chatter of interest from activist investors. And indeed, this is the kind of situation that would likely appeal to them.

Generally speaking, activist investors believe a company is undervalued or not living up to its potential due to mismanagement. So, they buy large stakes in the business to influence improvements. Perhaps the rumors regarding activist investors for Foot Locker gave the market hope that a turnaround was on the horizon, leading to gains in February.

It seems investors have longer to wait. On March 6, shares of Foot Locker plunged after it reported completed financial results for its fiscal 2023 (the fiscal year ended on Feb. 3). It doesn’t seem like a so-called turnaround is close. The company’s sales only increased 2% this past year. But its gross margin has plunged due to how much management is relying on markdowns.

In other words, Foot Locker is lowering prices to get sales. But even doing this merely results in running in place. In addition, management had previously laid out some modest financial goals for its fiscal 2026. But with its 2023 report, management pushed these goals out to its fiscal 2028.

Why would activists be interested?

Foot Locker is a well-known brand with over 2,500 locations across its various apparel retail chains. Moreover, with full-year sales of over $8 billion, consumers do still frequent stores. And finally, it’s still a profitable company despite its struggles. In fiscal 2023, it had adjusted earnings per share (EPS) of $1.42 — the adjustments were related to investments, not business operations.

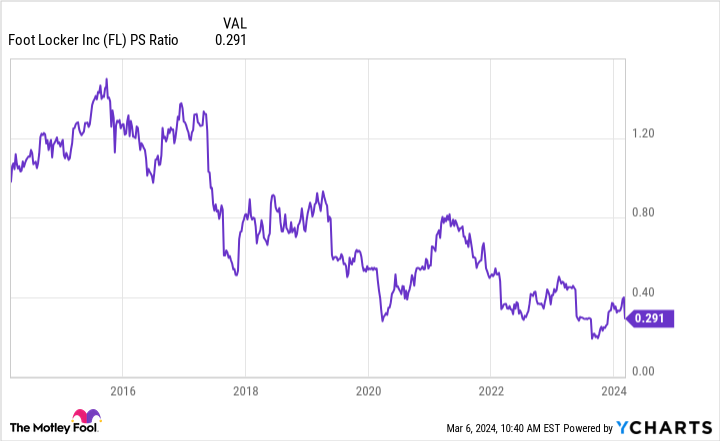

In other words, Foot Locker’s management has plenty to work with to create shareholder value. This is why activist investors might circle the wagon on this one. Moreover, at just 0.3 times trailing sales, Foot Locker stock is dirt cheap.

FL PS Ratio data by YCharts. PS Ratio = price-to-sales ratio.

What now?

If I were an activist investor, I wouldn’t gamble on a Foot Locker turnaround. The company is in a tough position for the long term, in my opinion.

Foot Locker’s management is guiding for 6% annual top-line growth over the long term, at most. It already fell far short of this goal in the first year of its plan.

Moreover, a key component of Foot Locker’s growth plans concerns its loyalty program. In fiscal 2028, it expects 50% of its sales will come from loyalty customers. But its loyalty program sales are only 21% today and haven’t grown at all in the past year.

In an age when consumers can buy shoes directly from shoe companies easier than ever, I believe it will be hard for Foot Locker to maintain relevance without aggressively marking down prices as it has been doing in recent years. That said, if I’m wrong and a turnaround takes hold, Foot Locker stock is very attractively priced.

Jon Quast has no position in any of the stocks mentioned. The Motley Fool recommends Foot Locker. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")