Yuichiro Chino/Moment via Getty Images

Earlier this year, I published a bull thesis on Hercules Capital, Inc. (NYSE:HTGC) despite the fact that it invests in VC space and carries a notable premium over its current NAV.

Both of these factors are inherently unfavorable because investing in VC companies implies greater exposure to speculative dynamics (e.g., success of currently no revenue generating product) and entering into a position, which trades above fair value imposes headwinds for future price appreciation.

However, after peeling back the onion a bit, it was clear that the premium is justified and the risk that is associated with VC businesses is well-mitigated.

For example, HTGC’s leverage is well-structured with back-end loaded fixed debt maturities, at a level that is considerably below the sector average.

Plus, the credit underwriting standards are exceptionally tight, which is confirmed by the balanced portfolio yield levels (compared to high double-digit yield from other VC-focused BDCs) as well as solid portfolio quality over COVID-19 and high interest rate periods.

So, based on the aforementioned dynamics and other elements outlined in my previous article, I issued a buy recommendation, which is quite unusual for me given my relatively conservative stance on investments, where VC-focused BDCs tend to be considered just too risky.

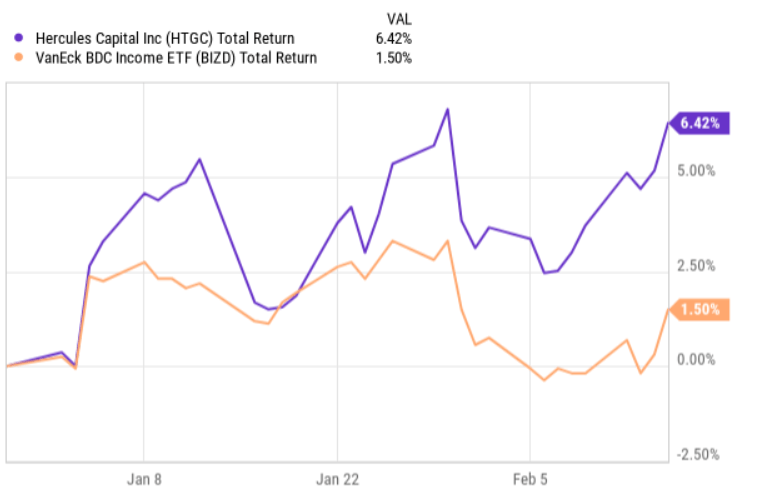

On a YTD basis HTCG has performed very well, outperforming the broader BDC market by a notable margin.

YCharts

Relatively recently, HTGC circulated its Q4, 2023 earnings, which certainly helped the Stock price climb higher.

Let’s now explore the key aspects of the recent earnings package and determine whether the current buy thesis still remains intact.

Thesis review based on Q4 results

In a nutshell, 2023 and Q4, 2023 revealed record performance figures for HTGC. The full year 2023 total investment income landed at $460.7 million, which is an increase of 43% compared to 2022. On a net investment income basis, the corresponding increase was 62%, which is even more significant and a clear indicative of improved margin component.

Importantly, Q4 net investment income was not only at a record level, but also above the consensus estimate by more than 12% (surpassing already a tough basis that was priced in by the market).

These results were achieved by a combination of mostly the three following factors:

- Higher yield levels that were driven by elevated SOFR and an uptick in fixed margin level.

- High quality assets that imposed no headwinds on the write-down or compressed margin side.

- Expanded base of AuM (i.e., positive net investment volumes).

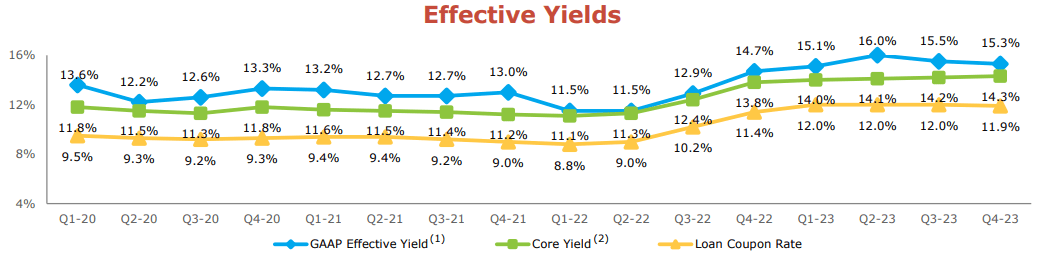

The chart below depicts the yield dynamics quite nicely.

HTGC Investor presentation

We can see that, on average, across all quarters in 2023 HTGC managed to deliver 200 basis points of an improvement to its effective yield levels compared to 2022. This obviously is a major driver for an increased NII figure.

In terms of the portfolio quality, HTGC continues to remain resilient, carrying a healthy investment (underlying business loan) profile. During Q4 there were further improvements on the quality side. For instance, the grade 1 and 2 credit categories improved by 50 basis points compared to Q3, 2023. At the end of 2023, the BDC had only one debt investment on nonaccrual with an investment cost and fair value of ~ $31 million and $0 million, respectively, accounting for less than 1% of the total portfolio value.

This is extremely low on an absolute and, most importantly, on a relative basis, where typically in the BDC universe VC-focused peers tend to possess ~3 – 6% in non-accrual investments.

Now, turning to the third factor behind HTGC’s robust performance (i.e., expanded AuM base), the current situation remains favorable even though there are clear challenges in the overall BDC sector to scope new volumes (since mid 2023).

As Scott Bluestein – CEO & CIO indicated in the recent earnings call, the movement in the volumes signals improving deal origination prospects in 2024:

…our origination activity has begun to accelerate in Q1. Since the close of Q4 and as of February 13, 2024, our deal team has closed $551.8 million of new commitments and we have funded $383.8 million. We have pending commitments of an additional $506.5 million in signed, non-binding term sheets.

In this case, we are not only receiving some verbal guidance from the CEO, but also getting tangible insights and facts on the actual new investment activity, which already now indicates that HTGC will not have to suffer from decreased portfolio base from which to extract yields.

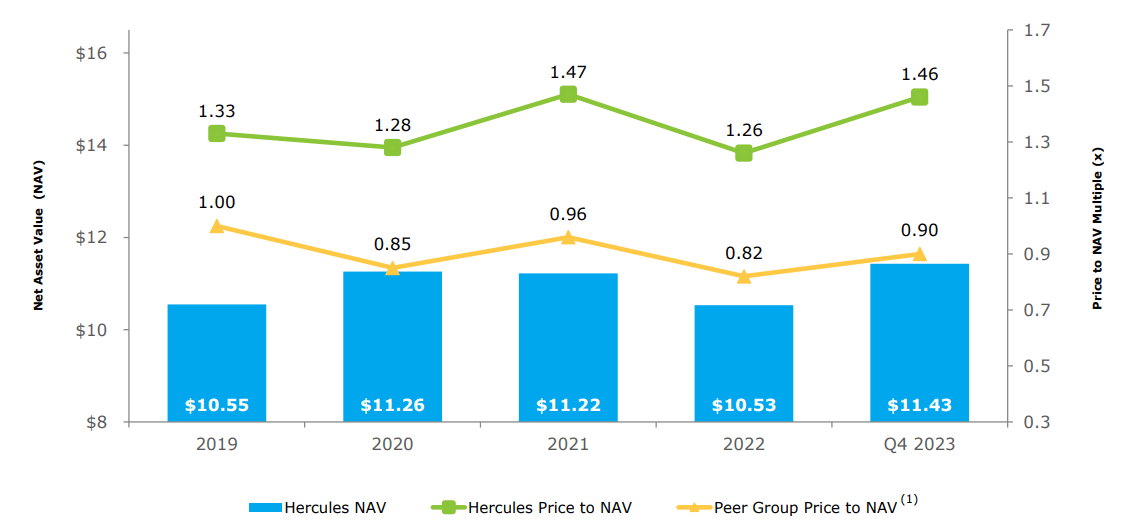

What is important to underscore here in the embedded advantage of Hercules to source fresh equity at terms that are beneficial to the existing shareholders.

HTGC Investor presentation

The graph above highlights the P/NAV data, where there is a ~45% premium over the underlying NAV figure, which comes in extremely handy during environments in which the deal activity is picking up. In essence, HTGC can venture into new investment transactions by utilizing some of the favorably priced equity to keep the leverage profile in check (i.e., not taking too much financial risk to grow the portfolio at terms, which are inherently favorable for the existing shareholders).

The bottom line

Hercules Capital has delivered a record performance in 2023 with a still improving trajectory in Q4 package. For example, the NII component managed to beat in a notable fashion the tough base formed by market’s consensus estimate.

Q4, 2023 figures and the insights from the recent earnings call reveal two critical aspects that, in my opinion, should accommodate further value creation for HTGC’s shareholder (even considering the recent runup in the share price):

- Portfolio quality remains strong and has improved at the category 1 and 2 level.

- The data on investment volumes signal that HTGC is already capturing incremental deals at levels that should not only help maintain the existing AuM base, but also expand it that will, in turn, warrant higher NII generation on an absolute level.

Given the above and the fact that HTGC offers an attractive dividend yield of 9%, it is still a buy.

Q2 2024 Earnings Call Transcript")