seb_ra

The HelloFresh Group (OTCPK:HLFFF) has several brands focusing on meal kit delivery. Since the company’s founding in 2011, starting with the flagship brand HelloFresh in Germany, HelloFresh started covering different segments creating several other brands and also expanding geographically.

In this article, we will talk about recent developments surrounding the company and its stock, and why we believe that the company still has immense growth potential not reflected in the stock.

Financials

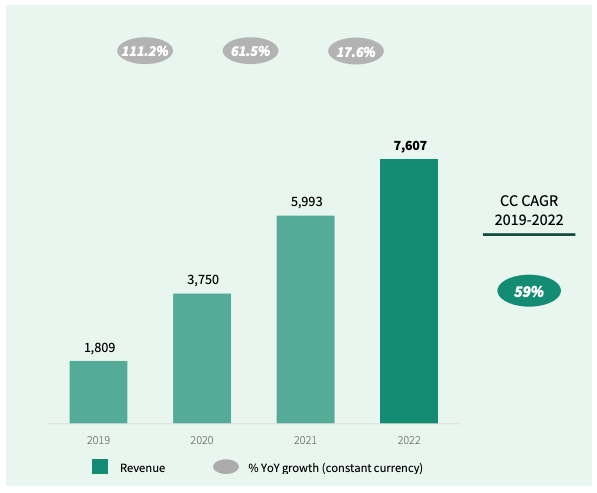

HelloFresh Group Capital Markets

HelloFresh has delivered strong revenue growth over the last couple of years, growing their top-line values across the board. From 2019 to 2022, the company delivered a revenue CAGR of 59% due to a combination of strong pricing power and order growth.

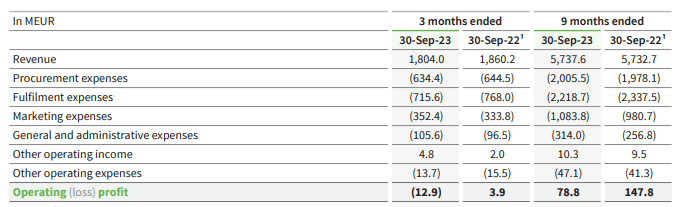

HelloFresh Q3 Earnings Report

Leading up to their most recent quarterly report, the Q3 2023 report, the company posted a stark decrease in growth, staying almost flat for the 9 months ended September 30 and actually decreasing for the quarter Y/Y, albeit growing on a constant currency basis.

With stagnating growth and similar cost, the company has posted an operating loss of €12.9m for Q3 2023 compared to operating profits of €3.9m in Q3 2022.

Looking at some of the positions on the balance sheet, the company appears to be on a solid footing. With a book equity of over €1b in Q3 2023 and cash of over €466m compared to long-term debt of only €165.1m, the company has plenty of room left to return capital to shareholders or invest back into the business.

Market Overreaction to Outlook Update

On November 15, the company issued an Ad Hoc update, narrowing their revenue growth outlook for FY 2023 from 2% to 8% to the lower end, between 2% and 5%. Furthermore, the company has lowered the outlook for Adjusted EBITDA FY 2023 from €470m to €540m, to now between €430m and €470m.

For the lower outlook figures, the company names fewer new customer acquisitions in the current quarter and a slower ramp-up of their production capacity. The company is also naming some temporary issues on their new facility in Arizona.

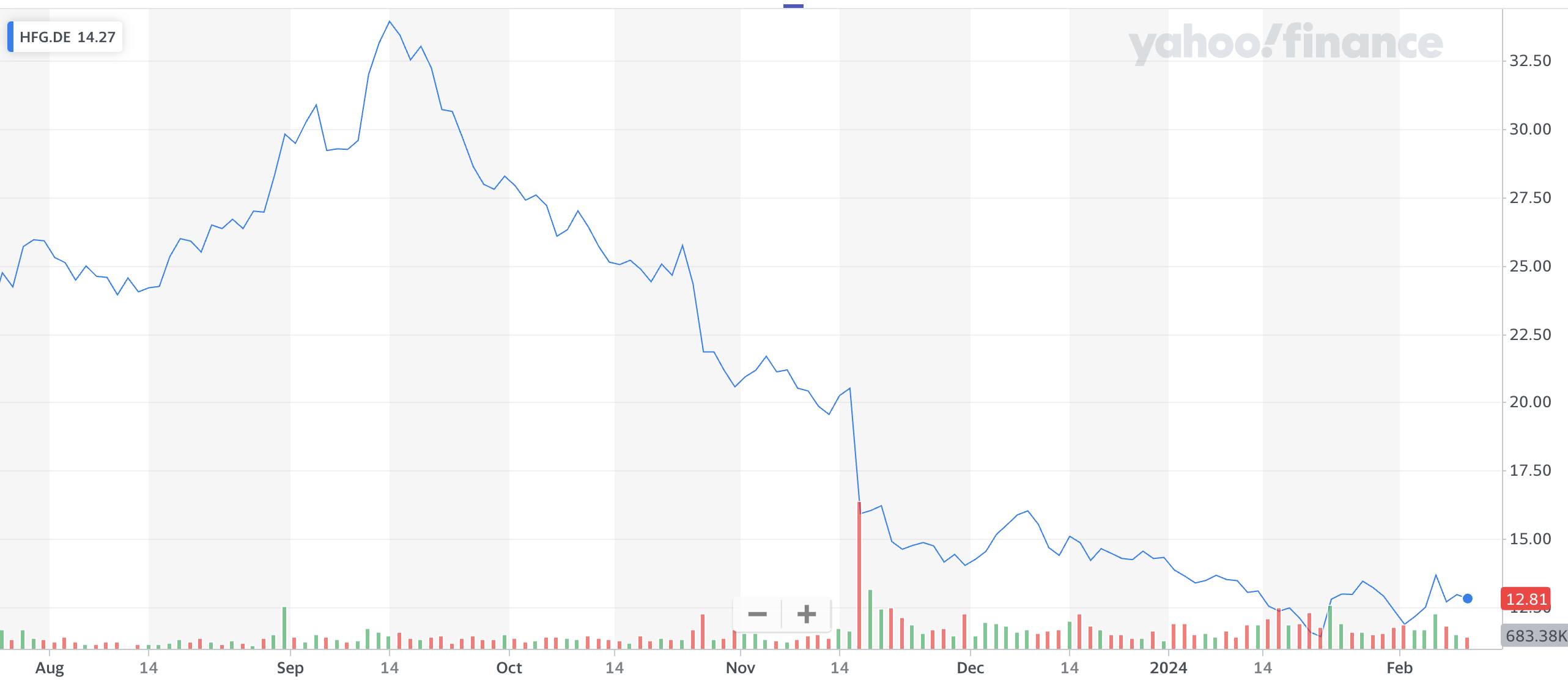

As a reaction to this update, the stock experienced a stark sell-off, with a drop of around 20% in a day. Since that drop on 16th November 2023, the stock continued to drop another 20% until today, sitting at 12.81€. We believe this constitutes an overreaction by the market to the news and potentially creates a buying opportunity for patient investors.

HFG Stock Price Chart (Yahoo Finance)

Valuation

With a current market cap of around €2.3b and an enterprise value of around €2b, at the midpoint outlook, the Germany-listed stock is currently trading at a forward Price/Sales of roughly 0.4 and EV/EBITDA of around 5. While growth rates do show a clear decline, we believe there is still a lot of room to grow, especially while ramping up several other brands in the company.

It is hard to compare HelloFresh to competitors, since there are no real peers at the same scale of HelloFresh that are independently trading as a public stock.

Keeping current macroeconomic pressures in mind, but also still thinking of the historically great growth rates the company has posted, we believe an EV/EBITDA of 7.5 is a fair price for the company. An EV/EBITDA would translate to an upside of almost 30% at the current stock prices. Factoring in the remaining growth potential for the company, we argue that upside might be even higher for long-term investors.

Growth Potential

Most recently, growth for the company has been stagnating, as a result of normalisation from the high growth caused by effects of the covid-19 pandemic. In their Q3 2023 release, the company reports a 5.9% Y/Y decline in active customers. Partly offset by an increase in the number of orders per customer and also average order value, revenue fell slightly less: by 3% Y/Y. Adjusting for currency, revenue even increased 3.5% Y/Y on a constant currency basis.

With the completion of their U.S. site, we conclude that HelloFresh has the potential to increase their market penetration in the U.S. and also potentially lower production costs. The end of construction for the site also marks the end of elevated CAPEX spend for the company. In the newly built site, HelloFresh produces meal boxes for their “Factor” brand.

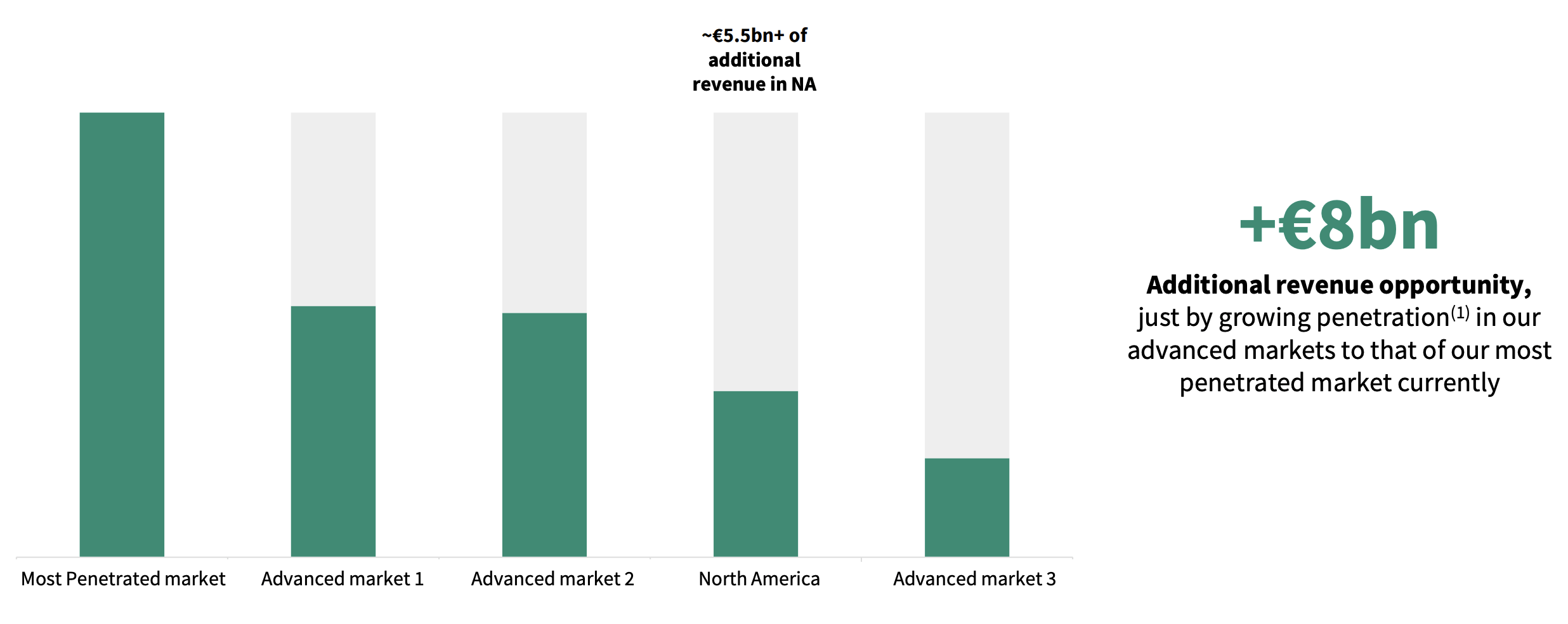

HelloFresh Penetration (HelloFresh Capital Day Presentation)

With HelloFresh being much more present in other markets (with the “most penetrated market” likely being their home market, Germany), there is still a lot of room to grow for other markets, including North America. With the US being the largest consumer market in the world, if HelloFresh manages to grow the penetration in North America to the same extent as their currently most penetrated market, there is €5.5b of additional revenue to be gained for the company.

Coming off the pandemic growth, the reason for stagnating growth might be maturity of some of the “older” products the company is offering. With overall growth stagnating, the chances of the mature segments contributing more to this stagnation are higher. As emphasised by the CFO in the latest earnings call, HelloFresh does not break out disclosure on single brands. However, we believe that, with horizontal expansion through the company’s brands, the company could return to post higher growth rates in following years.

Q3 Earnings Presentation

Risks and What to look out for

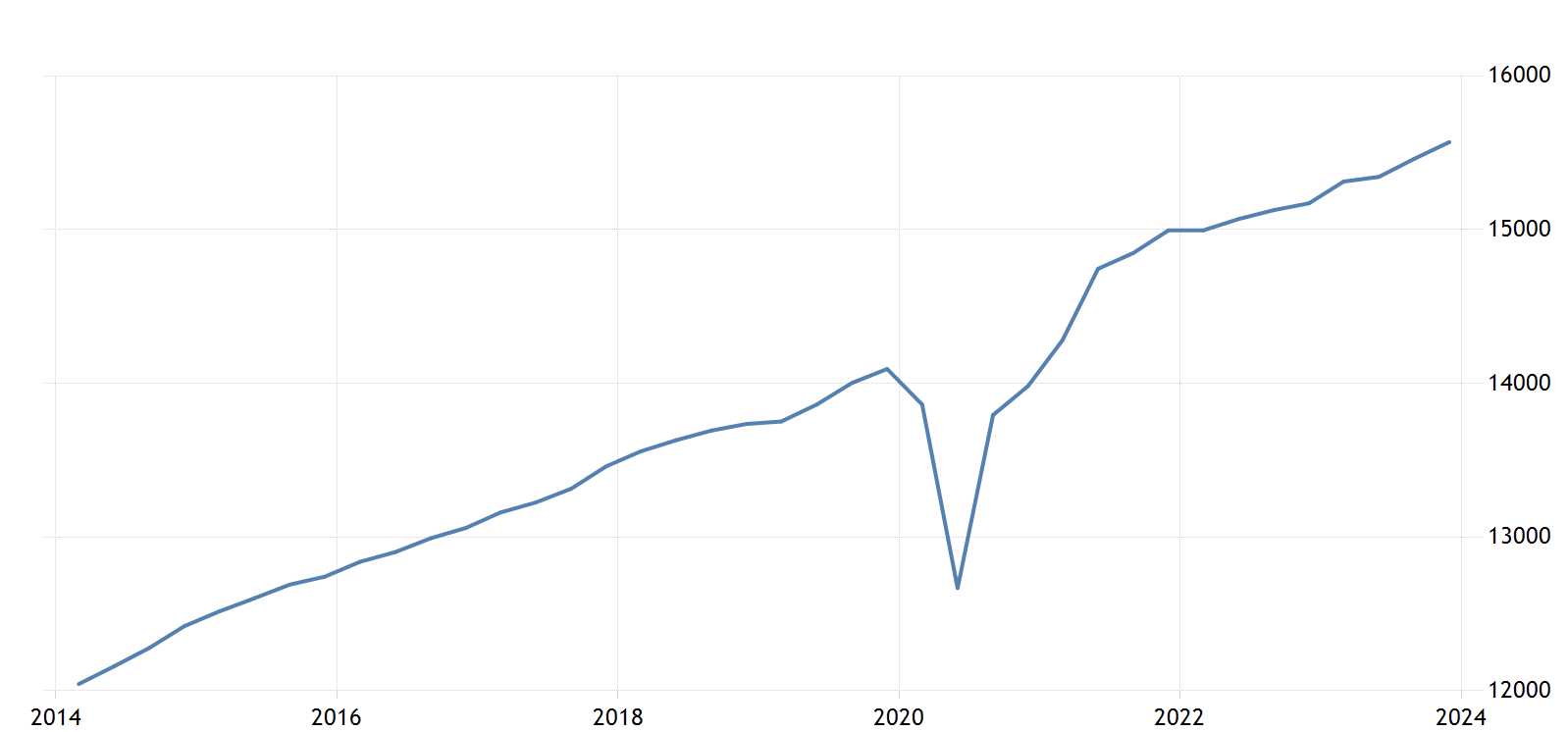

The biggest risk that HelloFresh is facing is weakening consumer demand, translating to further revenue pressures. Inflation, high interest rates and high credit card debt could put consumers under pressure, especially in the US, which is HelloFresh’s biggest market. Since HelloFresh is considered a more premium product, further pressures on consumers could lead to a decrease in affordability for higher-priced items. However, so far consumer spending has remained resilient, despite these macroeconomic pressures.

US Consumer Spending (U.S. BEA)

In the next quarters, we are closely watching developments regarding consumer spending behaviour and what outlook HelloFresh will provide for FY 2023. Besides overall consumer spending, we will also look for any comments from management regarding a potential normalisation of consumer behaviour, in regards to going out to eat vs. cooking at home or ordering food.

So far, the company has been able to offset some decline in active customers by increasing their prices and also increasing the amount of orders per customer. However, it remains to be seen if they can continue this strategy going forward or if they will start out-pricing their customers soon.

For now, we remain bullish for the stock and believe that the recent drop created a buy opportunity. However, the situation is dynamic and our rating could change to sell based on the factors named above.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")