Laurence Dutton

Helios Technologies, Inc. (NYSE:HLIO) is making a significant number of changes that include the acquisition of i3, facility expansion, and reorganization in the hydraulics business segment. The recent quarterly report did not include better than expected EPS, however most analysts out there are expecting FCF growth and operating margin growth. With stable and conservative projections of future FCF, the implied valuation appears to offer significant upside potential as compared to the current depressed stock valuation. I do see a significant number of risks from a protectionist trade environment in the U.S. as well as other foreign countries, changes in labor conditions, or lower demand for HLIO’s products. However, I believe that HLIO appears too cheap.

Helios: Hydraulics and Electronics

Helios Technologies, Inc. and its wholly owned subsidiaries are global leaders in highly specialized motion control and electronic control technology for diverse end markets, including construction, materials handling, agriculture, energy, and healthcare among others. I believe that the business activity is well diversified, which will most likely help reduce net sales volatility in the coming years.

The company operates via two reportable segments: Hydraulics and Electronics. Within the Hydraulics segment, there are three key technologies: cartridge valve technology, quick release hydraulic coupling solutions, and hydraulic systems solutions. Cartridge valve technology products provide important functions for a hydraulic system: controlling fluid flow rates and directions as well as regulating and controlling pressures.

The company’s products allow users to quickly connect and disconnect from any hydraulic circuit without leaks, and ensure optimal performance under elevated temperatures and pressures using one or more couplers. The company also offers solutions designed for machine users, manufacturers, or designers to meet complete system design requirements, including electro-hydraulic, remote control, electronic control, and programmable logic controller systems along with automation of existing equipment.

The Electronics segment provides complete, fully customized display and control solutions for engines, engine-driven equipment, specialty vehicles, and swim spas. This extensive range of products is complemented by extensive application experience and a deep depth of software, embedded programming, hardware, and maintenance engineering teams.

The Earnings Release Was Lower Than Expected, But The Expectations From Other Investors Include FCF Growth Generation

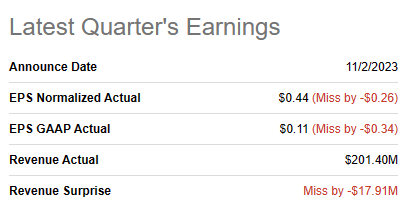

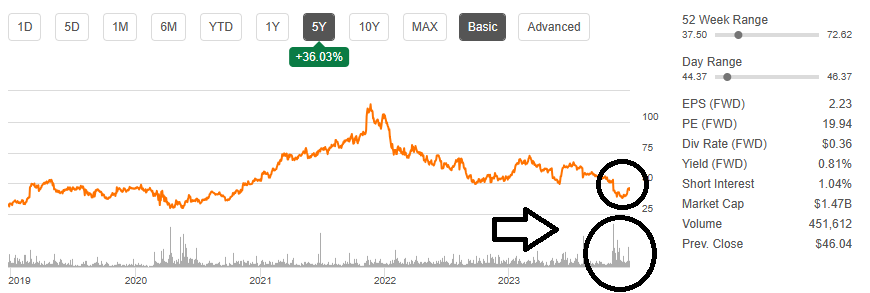

The earnings per share GAAP reported in November was lower than expected, equal to close to $0.11 per share. Additionally, the quarterly revenue was also lower than expected, equal to $201 million. I do believe that the numbers were not beneficial, however the current stock price and the reaction of some investors were too pessimistic. The current valuation is close to that of 2020.

Source: SA Source: SA

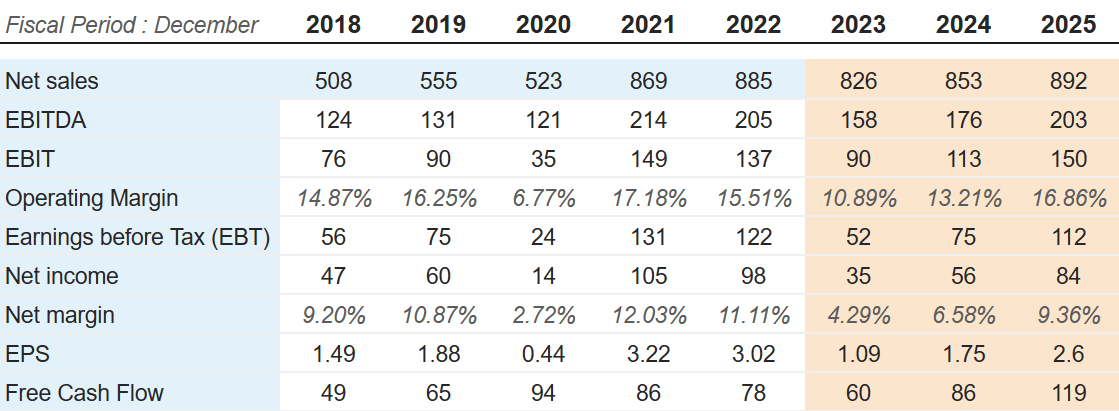

If we look at the figures expected by other analysts, I believe that expectations are not that detrimental. FCF is expected to increase from about $60 million in 2023 to about $119 million in 2025. Additionally, the operating margin and the net margin are expected to increase in 2024 and 2025.

Source: Market Screener

Balance Sheet

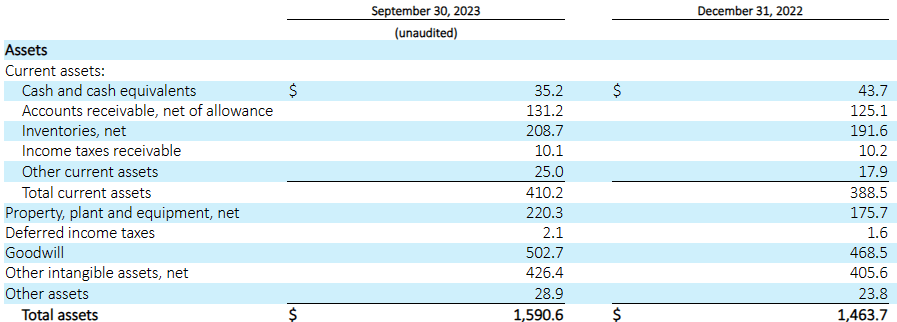

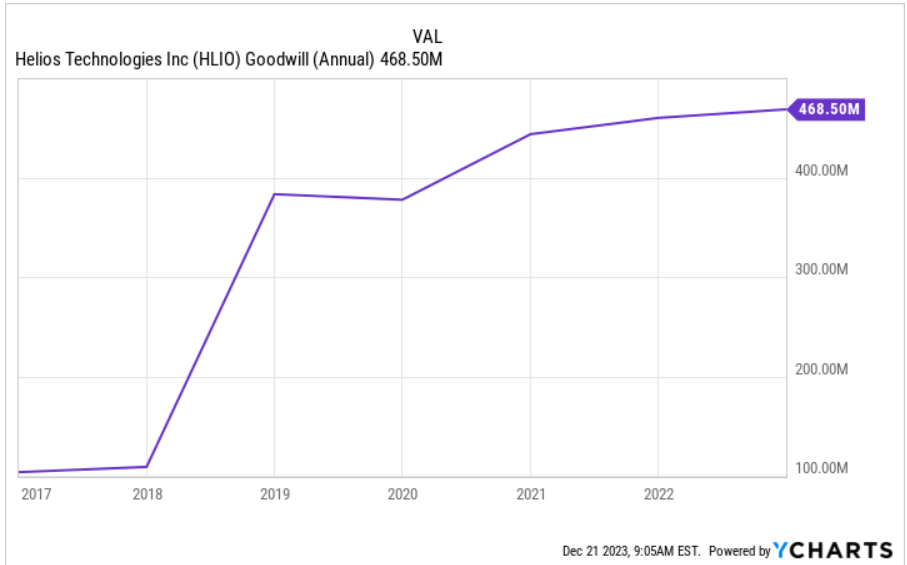

As of September 30, 2023 the company reported $35 million in cash, inventories worth $208 million, goodwill close to $502 million, and total assets close to $1.59 billion. The asset/liability is larger than 2x, and the current ratio is more significant than 2x, so I do not see liquidity issues.

Source: 10-Q

Given the total amount of properties, accounts receivables, and inventories, I am not worried about the total amount of debt. With current debt worth $21 million, a revolving line of credit worth of $217 million, and long-term debt close to $304 million, total liabilities stand at about $748 million.

Source: 10-Q

Acquisitions, Restructuring Costs, And R&D Investment For New Product Development May Enhance Future Business Performance

In the last quarterly report, the company noted an increase in R&D investments, restructuring efforts, and acquisitions efforts, which led to higher costs. As a result, I believe that Helios Technologies could be suffering a temporary decrease in EPS and net income. In my view, these efforts may redesign the business configuration of Helios Technologies, bring financial flexibility, and open new doors for business development in the future.

The year-over-year increase was primarily related to incremental SEA from acquisitions, restructuring, and increased R&D investment for new product development.

Restructuring costs included in cost of sales increased by $1.7 million to $2.0 million in the third quarter of 2023, compared with the year ago period. Source: Quarterly Press Release

Facility Expansion In The Hydraulic Business Segment Could Bring New Capacity And Revenue Growth Potential

In the last quarterly report, we could read a bit more about the facility expansion announced in the Hydraulic business segment. Management also noted additional transfers, integration, and efficiency efforts, which may have an impact on future income statements.

Facility expansion was completed in Mishawaka, Indiana, the Hydraulic Manifold Solutions CoE, which now includes the manifold machining and integrated package assembly operations from Sun Hydraulics, the integrated package business from Faster Inc., and incremental capacity to allow for Daman’s core organic growth.

While the majority of relocation efforts have been accomplished, there still remain additional transfers and integration and efficiency efforts underway in the fourth quarter of 2023. Source: 10-Q

The Acquisition Of i3 Product Development Will Most Likely Have A Beneficial Impact On Future FCF Growth

Helios noted the acquisition of i3 Product Development in 2023, which is expected to bring not only EBITDA increases, but also net sales growth and know-how in electronics, mechanical, and industrial software applications.

In May 2023, we acquired i3 Product Development, a custom design and engineering services firm with expertise in electronics, mechanical, industrial, embedded and software engineering. Source: 10-Q

Given the previous increase in goodwill, I believe that Helios has a lot of expertise in the acquisition and integration of M&A targets. With this in mind, I assumed that i3 will be successfully integrated. Given this acquisition and the other in 2023, I am also assuming that future acquisitions would most likely take place, and inorganic growth could bring FCF growth.

Source: Ycharts

Helios Technologies Reports A Number Of Patents And Trademarks, Which Will Most Likely Serve As Barrier For New Entrants In The Market Targeted

Helios sells its products to customers in more than 90 countries around the world. The company owns approximately 300 patents and trademarks related to certain products and businesses along with trade secrets, unpatented know-how, and other intellectual property rights. I believe the know-how accumulated would most likely help the company remain competitive in the market in which it operates.

My Cash Flow Expectations Imply Significant Upside Stock Potential

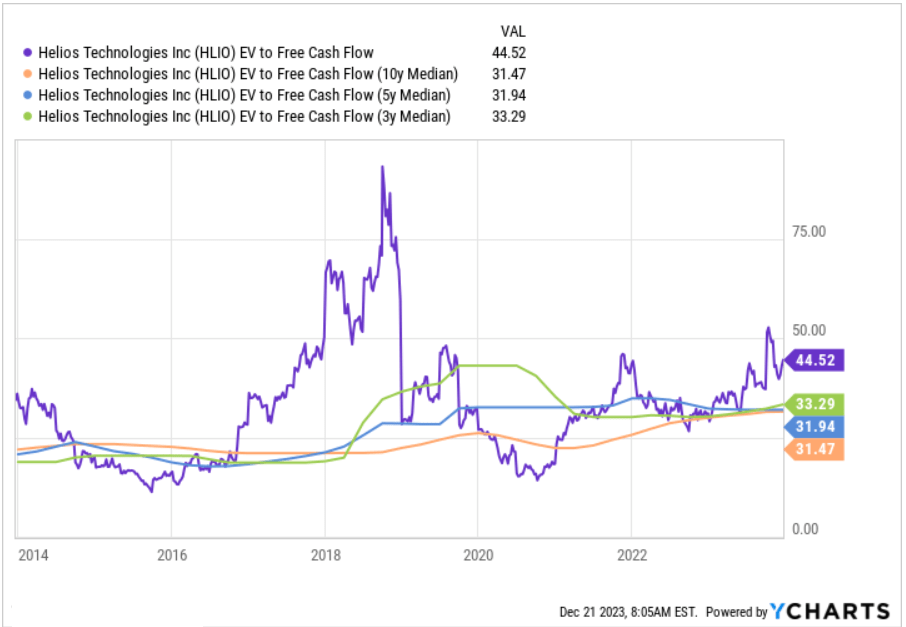

For the assessment of the future cash flow statements, I took into account the expectations of other analysts as well as previous financial figures and my own assumptions. I believe that my numbers are quite conservative. I invite readers to have a quick look at my figures.

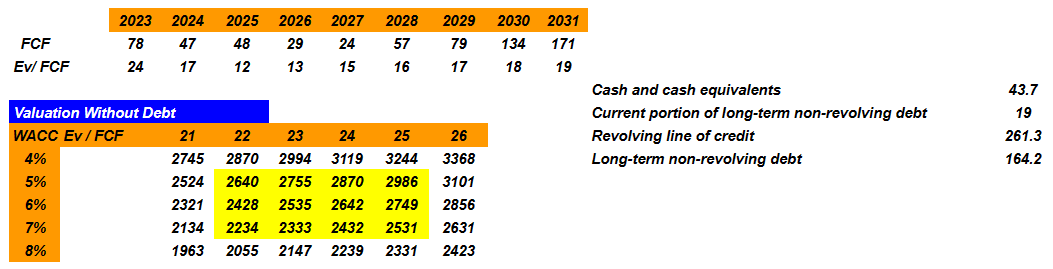

My cash flow estimates for the next few years include 2031 net income of $208 million, depreciation and amortization close to $91 million, and 2031 stock-based compensation expenses of close to $17 million.

I also included amortization of debt issuance costs worth -$2 million, benefit for deferred income taxes of about -$12 million, and amortization of acquisition-related inventory step-up of about -$8 million.

Additionally, with changes in forward contract losses of -$35 million, changes in accounts receivable of $38 million, changes in accounts payable of close to -$36 million, changes in accrued expenses and other liabilities of about -$24 million, income taxes payable worth -$4 million, and 2031 CFO of $241 million, I also included 2031 FCF of $170 million.

Source: My Own Expectations

For the valuation of the exit multiple, I took a look at the current trading multiples and previous EV/FCF multiples. The company appears to trade at close to 31x-44x FCF. However, I tried to be as conservative as possible, and used exit values of close to 21x-26x.

Source: Ycharts

With FCF between $47 million and $171 million, a WACC of 4%-8%, and EV/FCF of 21x-26x, I obtained a valuation without debt of close to $1.9 billion and $3.3 billion. Note that I included cash, and subtracted the revolving line of credit and the long term debt.

Source: My DCF Model

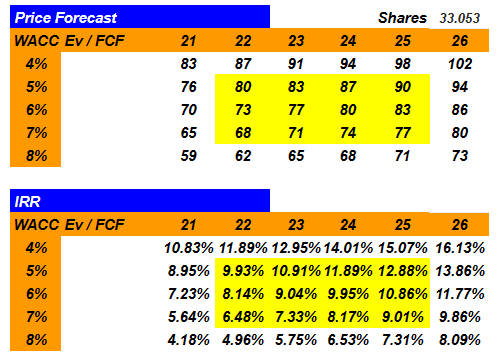

If we divide by the share count, the price forecast would be close to $59-$102 per share with a median fair price close to $68 and $90 per share. The median internal rate of return would be between 6% and 12%.

Source: My DCF Model

Competitors

In the Hydraulics segment, the company competes in a market in which the main competitors are global. This market is divided between producers of complete systems, and producers of specific components such as cartridge valve technology products. Helios is differentiated by the quality, reliability, and speed of service as well as the technological characteristics of its products and services.

Along with this, in the Electronics segment, the competition is broad, from large multinationals such as Garmin (GRMN) to small companies specialized in products of a single type. The company’s advantage lies in quality, customization capacity, and speed of service besides strengthening its positions in medium-sized niche markets not well served by larger competitors. On the other hand, some of the brands in the segment, such as Balboa and Joyonway, are capable of offering an integrated hardware and software architecture that consists of a value proposition that makes it difficult to change suppliers easily.

Risks

Helios Technologies’ businesses are exposed to a series of external conditions such as the price and availability of energy and its transportation, the price of other products and services, and the general state of the economy in the regions in which it carries out its operations.

Pricing and availability of finished goods, raw materials, energy, transportation and other necessary supplies and services for use in our businesses can be volatile due to numerous factors beyond our control, including general, domestic and international economic conditions, labor costs, production levels, competition, consumer demand, import duties and tariffs, currency exchange rates, international treaties and changes in laws, regulations and related interpretations. Source: 10-k

Specifically, many of its operations and transactions depend on favorable trade relations between the United States and those countries in which clients carry out their activities. In this regard, management offered the following details in the last annual report.

A protectionist trade environment in either the U.S. or those foreign countries in which we do business or sell products, such as a change in the current tariff structures, export compliance laws, government subsidies or other trade policies, may adversely affect our ability to economically source materials, sell our products, or do business in foreign markets. Source: 10-k

The company also considers climate change and local and international regulations that may arise as possible risk factors. Authorities could impose fines on Helios Technologies, which may lower the bottom line, and bring the company’s stock price down. In this regard, management offered the following warning to investors.

We are subject to a variety of federal, state, local and foreign environmental, health and safety laws and regulations concerning, among other things: the discharge of pollutants into the soil, air and water; the generation, storage, handling, use, release, disposal and transportation of hazardous materials and wastes; environmental cleanup; and the health and safety of our employees. Source: 10-k

Conclusion

Currently trading at multi-year lows, Helios Technologies, Inc. is making a significant amount of efforts that include the acquisition of i3, facility expansion, and restructuring. As a result, I believe that we could see FCF growth, operating margin growth, and net income growth in the next few years. Like other analysts, I made beneficial projections of free cash flows, and my DCF model implied that there is significant upside potential in the stock price. Yes, there are obvious risks from a protectionist trade environment in the U.S and other foreign countries, changes in environmental laws, inflation, or changes in the labor conditions. With that, I believe that the stock price is quite undervalued.

Q2 2024 Earnings Call Transcript")