Marco Garcia/Getty Images Entertainment

Summary

Hawaiian Holdings (NASDAQ:HA) is a US airline that offers both cargo and passenger flights between Hawaii and the neighboring islands. One of its most important routes is the connection between Hawaii and Japan.

In December 2023, it was announced that the company was to be acquired by Alaska Airlines (ALK) at a price of USD 18.00 per share. This corresponds to a premium of 270% on the closing price at the time. The takeover is currently being reviewed by the Department of Justice (DOJ) and is expected to be completed within the next twelve to 18 months. The market already seems to be pricing in a successful takeover, but I consider the actual probability to be much lower. I therefore see HA as an asymmetric short with an attractive risk/reward ratio.

Investment thesis

The airline industry is characterized by low profit margins, high fixed costs and intense price competition, which has been particularly true for Hawaiian Holdings since the coronavirus pandemic. Previously, the company held a dominant position in the market for Japanese and US tourists for years, as Hawaii and its neighboring islands were considered a popular vacation destination. In the period from 2009 to 2019, HA was able to operate continuously profitably, despite an exception in 2011, due to the increase in travel to Hawaii.

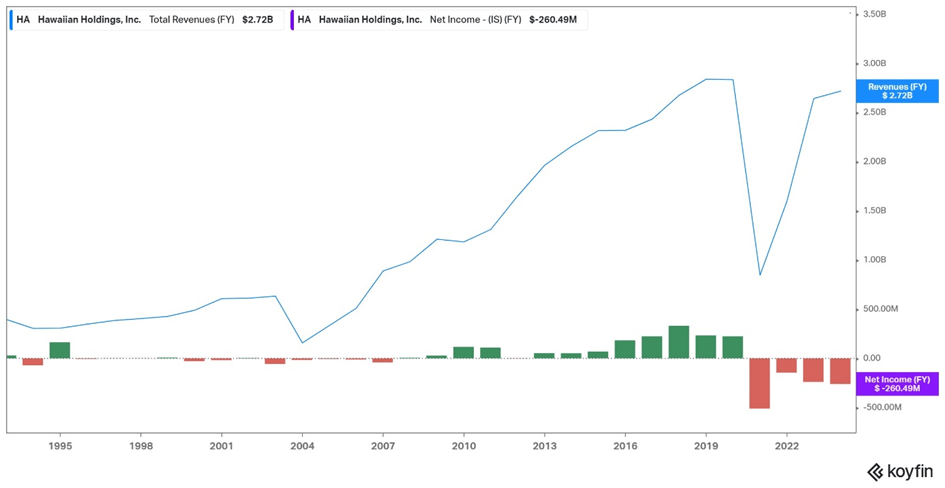

Koyfin

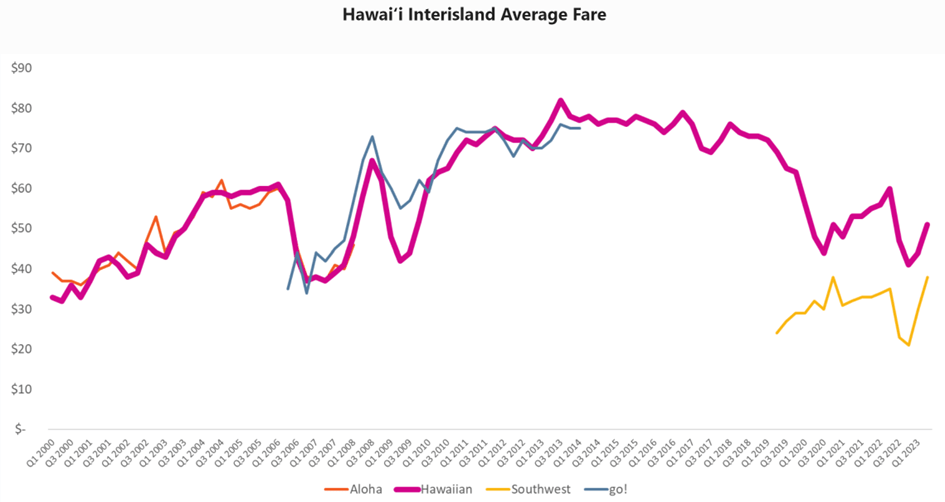

Over the past four years, Hawaiian Holdings has recorded the highest losses since its IPO. To make matters worse, Southwest Airlines (LUV) aggressively entered the market and increased its capacity between the US mainland and Hawaii by introducing new routes or increasing existing frequencies. In addition, LUV entered the inter-island routes that were previously monopolized by HA and accounted for a significant portion of its profits. Before the competition entered the market, HA had a market share of 96% in this area. LUV lowered prices by up to 60%, securing a market share of around 30% and forcing HA to follow suit to avoid losing market share completely. This has resulted in permanently lower ticket prices compared to the time before LUV entered the market, which means that the profitability of the pre-corona era is over.

Cirium

The main problem for Hawaiian Holdings is that its competitors have greater financial resources and a higher profile, which should enable them to win the price competition against HA in the long term.

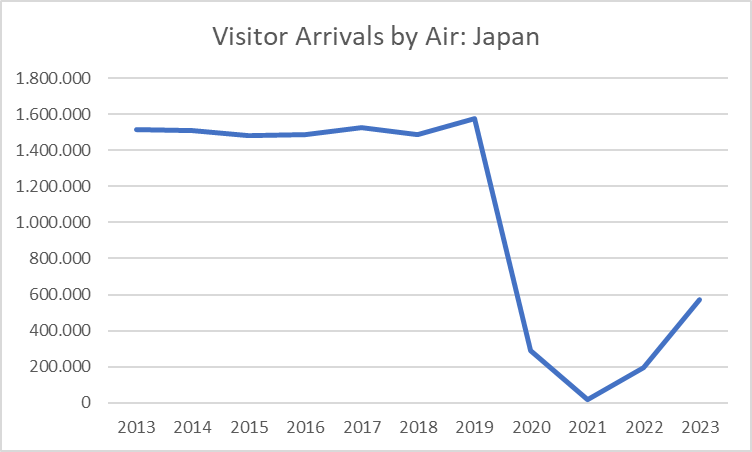

Furthermore, the recovery in Japanese travel activity to Hawaii has been slow. Alongside the USA, Japanese tourists are the most important target group for the islands. Visitor numbers in 2023 only reached around 40% of the 2019 level.

Hawaii Tourism Authority

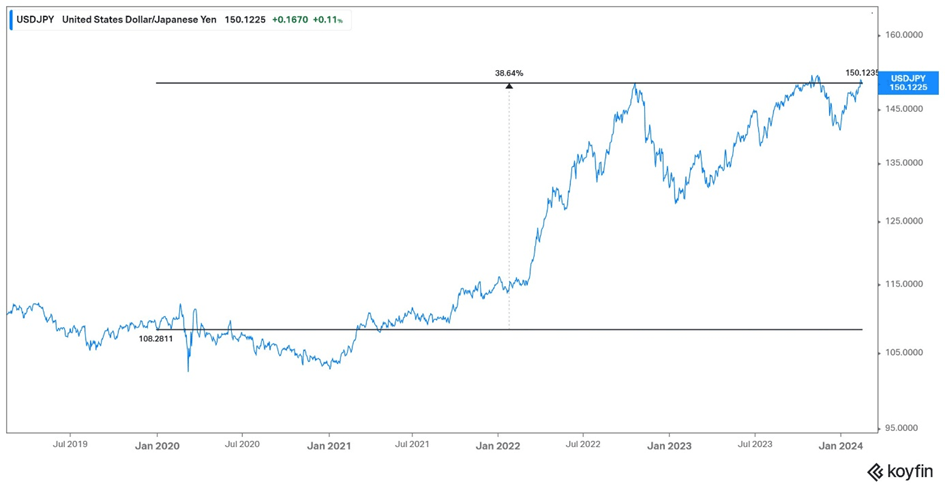

This is largely due to the increased travel costs for Japanese tourists. Since 2020, the US dollar has appreciated by almost 40% against the Japanese yen, which represents significant changes for the exchange rate. The appreciation is due to the rapid increase in interest rates by the US Federal Reserve and the Bank of Japan’s adherence to its low interest rate policy. Current macroeconomic data suggests that this will not change in the short term.

Koyfin

Added to this are the increased costs due to the sharp rise in inflation over the last two years. This means that vacation costs for Japanese visitors to Hawaii have increased by more than 50%. The booking figures to date indicate that Japanese tourists will not be returning any time soon.

ForwardKeys

I believe that HA will remain unprofitable in the medium term due to the weak recovery in foreign tourism and increased competition. Over the past four years, the airline has suffered an accumulated loss of USD 1.15 billion. At the same time, HA’s net debt amounts to USD 1.1 billion. In this respect, a restructuring or bail-out is necessary sooner or later in my opinion, regardless of a possible takeover.

The takeover

Alaska Airlines intends to acquire HA at a price of USD 18.00 per share. This would provide access to the 25th largest US market, with Honolulu serving as the second-largest hub for ALK. This opens up growth opportunities in the Asia-Pacific region, one of the fastest-growing markets in the world. Alaska Airlines’ willingness to pay the generous 270% premium is related to uncertainties investors currently have about its future source of growth.

However, the takeover is still subject to regulatory approval, which is by no means certain. The responsible authority, the Department of Justice, has already shown under US President Joe Biden that it is inclined to block airline takeovers and prevent further consolidation in the industry. Recently, the DOJ halted the merger between JetBlue Airways and Spirit Airlines, which could serve as a precedent for the HA takeover.

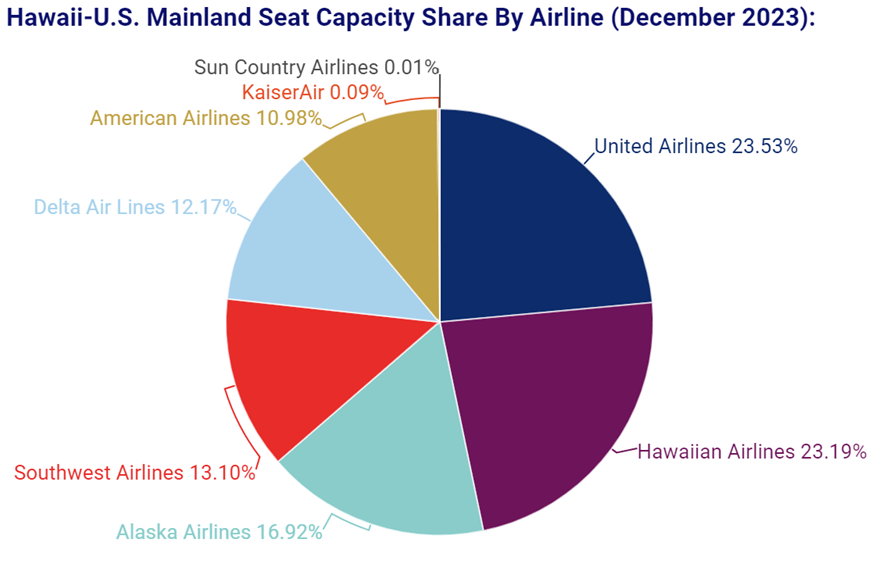

The route overlap between Hawaii and the US mainland is 43% for HA and ALK. Hawaiian Holdings and Alaska Airlines are currently the second and third-largest carriers on these routes in terms of seat capacity, behind United Airlines. A successful merger would put the combined company clearly in the lead with a market share of around 40%.

OAG Aviation

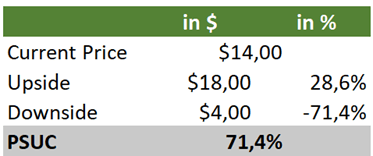

The takeover price is USD 18.00 per share, while we set the break price (the theoretical price in the event of unsuccessful negotiations) at USD 4.00 – roughly the price prior to the announcement of the planned takeover. The share is currently trading at USD 14.00, which represents an upside of around 29% and a downside of around 71%. The resulting risk/reward ratio for the short seller is almost 2.5x. This also implies that the stock market assumes that the takeover will take place with a probability of 71.4% (PSUC: probability of success).

Own calculation

The market should have adjusted, especially after the JetBlue/Spirit merger was blocked, but the current share price shows little change. We believe that the probability of a successful HA/ALK merger is less than 50%. If the market were to price this in correctly, the share price should currently be at USD 11.00, some 21% below current levels. At these prices, I would reduce the short positions, as the risk/reward ratio would no longer be so attractive. Until then, I am holding the short position until the DOJ’s decision.

Risks

There is a risk that the DOJ will approve the takeover and the shareholders will receive USD 18.00 per share held.

Another risk is an improvement in the fundamental situation and the balance sheet situation. This would lead to a deterioration in the risk/reward ratio for short sellers in this situation. However, I only see such a scenario as likely if competition is leaving the Hawaiian market. At present, however, I do not expect this to happen in the next twelve to 18 months.

Q2 2024 Earnings Call Transcript")