filadendron

Investment Thesis

I take the view that if the company can continue to show an improvement in net income growth and return on equity, then my view on the stock would become more bullish.

In a previous article back in November 2023, I made the argument that Hanover Insurance Group (NYSE:THG) needs to see further net income growth for a bullish view to be justified.

Since then, the stock has ascended to a price of $131.01 at the time of writing:

TradingView.com

The purpose of this article is to assess whether Hanover Insurance Group has the ability to see continued growth from here taking recent performance into consideration.

Performance

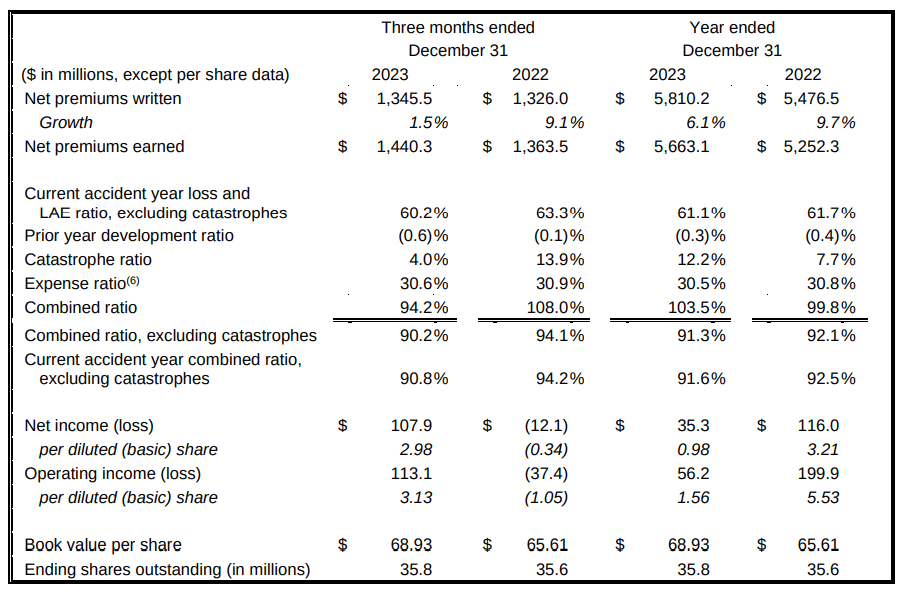

When looking at fourth quarter and full year 2023 earnings results for Hanover Insurance Group as released on January 31, we can see that growth in net premiums written has slowed from 9.1% to 1.5%.

Hanover Insurance Group: Q4 2023 Press Release

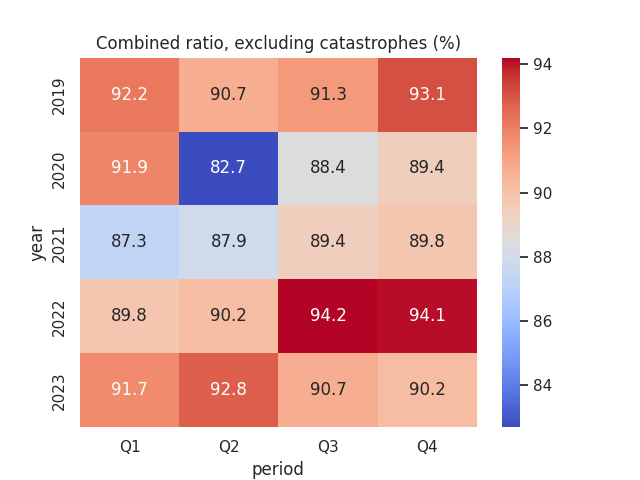

I had previously stated that with a substantial reduction in the combined ratio (excluding catastrophic losses) in Q3, a similar reduction in Q4 would be encouraging. We see that for this quarter – the combined ratio is down to 90.2 from 94.1 in the prior year’s quarter.

Figures sourced from previous Hanover Insurance Group Earnings Releases (Q1 2019 to Q4 2023). Heatmap generated by author using Python’s seaborn visualisation library.

Catastrophe losses in 2023 amounted to $690.1 million, which were significantly influenced by severe convective storms in the Midwestern United States which impacted Personal Lines, particularly in the first three quarters of 2023. Catastrophe losses were less prominent in Q4.

I had previously made the argument that a lower combined ratio in this quarter could coincide with a significant boost in net income, as Hanover Insurance Group would be demonstrating that it has the capacity to continue growing premiums at a faster rate than losses and expenses. In this regard, net income per diluted (basic) share is up to $2.98 from a loss of -$0.34 per share in the prior-year quarter.

My Perspective and Looking Forward

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, I had previously made reference to the fact that Hanover Insurance Group would need to see growth in net income from here in order to see a rebound in return on equity – which had dipped into negative territory.

We can see that return on average equity is up from -2.1% to 18.8% on a three-month ended basis, while it is down on a year-ended basis from 4.4% to 1.5%.

The Hanover Insurance Group, Inc.: Fourth Quarter and Full Year 2023 Results Presentation

However, given the strong performance we have seen in Q4, I am optimistic that the return on equity has the capacity to see a rise on a yearly basis for 2024.

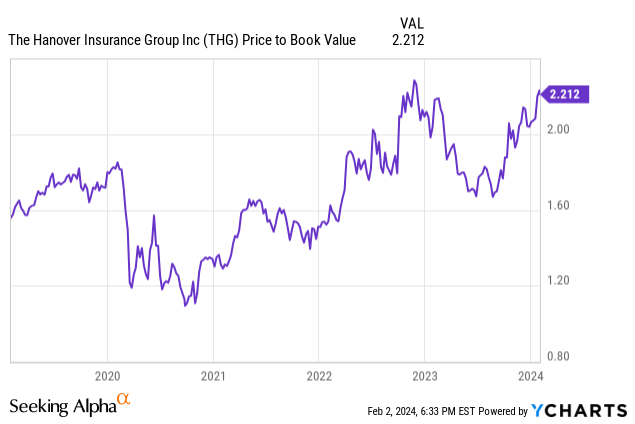

I had previously made reference to the price-to-book ratio for Hanover Insurance Group – we can see that the same still remains at a five-year high:

Price to Book

ycharts.com

In this regard, I take the view that while the stock may still be expensive on this basis – a rising return on equity ratio for the latest quarter is encouraging. Should we see evidence that Hanover Insurance Group can boost the return on equity ratio significantly over a yearly basis – then my sentiment on the stock would become more bullish.

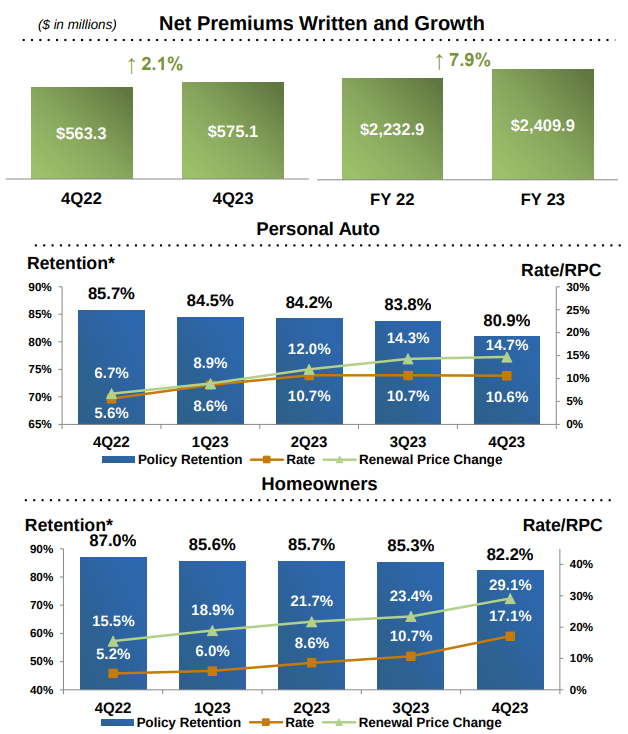

I had also previously made reference to the fact that the Personal Lines segment could come under pressure going forward, as a result of both high renewal prices potentially enticing customers to switch, and customers potentially delaying purchases of new vehicles as a result of higher vehicle prices.

In spite of this, we can see that net premium growth for the year was impressive at 7.9% on a yearly basis. In addition, we can also see that retention – which is the ratio of net retained premium to the premium available to renew over the same period – has seen a decrease across both the Personal Auto and Homeowners segment.

The Hanover Insurance Group, Inc.: Fourth Quarter and Full Year 2023 Results

While we have seen an increase in renewal price changes, the fact that we are still seeing growth in net premiums indicates that performance across Personal Lines is improving, and a continuation of this trajectory would be a bullish signal for the stock.

Risks

In terms of the potential risks to Hanover Insurance Group at this time, I take the view that should we see the recovery in net income growth start to stall – then this could give investors pause on the stock.

This could be the case if the combined ratio starts to rise once again – which could be a risk if further price increases ultimately reduce premium demand.

We can see that the expectation for the full year 2024 is a combined ratio (excluding catastrophic losses) of 90% – 91%.

The Hanover Insurance Group, Inc.: Fourth Quarter and Full Year 2023 Results

While the company’s reduction in the combined ratio to date has been impressive – premium demand must remain vibrant for this to continue.

Conclusion

To conclude, Hanover Insurance Group has seen impressive performance in terms of its combined ratio and an improvement in performance across the Personal Lines segment.

I take the view that if the company can continue to show an improvement in net income growth and return on equity, then my view on the stock would become more bullish.

Q2 2024 Earnings Call Transcript")