Our first visit to the emergency room unfolded three years ago when our daughter displayed signs of anaphylaxis due to a food allergy. Unsure of what steps to take, we dialed 911, which led to an ambulance arriving promptly to transport us 16 minutes to the nearest hospital.

The paramedics administered epinephrine, then the ER doctors swiftly took over, and four hours later our daughter was deemed safe and sound. Because of COVID policies at the time, only one parent could accompany her, so I followed the ambulance and was anxiously stuck in my car for the entire four hour wait. In preparation for potential future allergy attacks, we acquired children’s Benadryl and an epipen.

Despite our gratitude for the ambulance and medical care, the shock of a $3,532 ambulance bill followed. We had assumed our insurance plan would cover most of the cost, and were dumfounded when they did not. This led to my wife spending hours and hours engaged in heated discussions with both AMR (ambulance provider) and United Healthcare (insurance carrier), attempting to secure in-network coverage. After all, why were we paying $2,100/month in health insurance premiums?

Regrettably, on February 8, 2024, we found ourselves in need of another visit to the emergency room.

The Incident

After a Lunar New Year performance lasting from 9:15 am to 11:30 am at my son’s school, our kids had the rest of the day off. We spent the morning playing at home before heading to the Pomeroy Center for a swim from 1:40 pm to 3:45 pm.

Given I was out most of the day with the kids, we enlisted help from our babysitter to watch over the kids from 4 pm to 6:30 pm. Though the childcare window was relatively short, it afforded my wife and me the precious time needed to focus on my second book with Portfolio Penguin. The deadline for submitting the completed manuscript loomed.

But at 6:15 pm, a sharp scream pierced the air. Crying isn’t unusual in our home, but this time, it felt notably intense. The babysitter promptly texted, explaining that our kids were roughhousing, and our son had inadvertently pulled our daughter’s left arm.

While her arm didn’t appear broken, she took a while to calm down. Given their frequent play-fighting, we initially didn’t consider this latest incident a cause for much concern.

Past Regret Of Not Going To The Emergency Room

At 6:24 pm, my wife went downstairs in an attempt to calm the situation. Unfortunately, every time our daughter attempted to move her arm, she yelped in pain. I joined them at 6:55 pm, finding my wife in our daughter’s bed reading a book. As soon as I entered the room, our daughter burst into tears. It was evident that something was seriously wrong.

When I inquired about her pain, she tearfully confirmed its presence. Then, upon asking if she thought we should head to the emergency room, her response was a loud and distressed refusal. She didn’t want to go, and truthfully, neither did I. It was nearly 7 pm, approaching their bedtime.

Recalling an incident from my own childhood when I broke my left pinky toe at the age of 11, I hesitated. Running around the house barefoot, I had stubbed my toe so forcefully that it bent completely sideways. When I approached my dad and explained the situation, he responded with frustration, asking if I wanted him to take me to the hospital.

Regrettably, I chose not to go, feeling guilty for bothering him. Had I sought medical attention, they likely would have splinted my toe, allowing it to heal properly. Instead, my toe remains crooked and prone to injury, causing on-and-off discomfort for the past 35 years.

Another Trip To The Emergency Room

Recalling my childhood trauma, I made the executive decision for all of us to head to the emergency room, just in case something was seriously wrong. Despite my son’s protests and tears due to fatigue, I insisted he come along.

Despite repeated admonitions to be gentler with his younger sister, he hadn’t heeded our advice. This incident became a teachable moment of three lessons.

Lesson #1: Actions have consequences. If you don’t want to go to the hospital, endure tiredness, and witness your sister in pain, refrain from hurting her or playing too rough. She’s two-and-a-half years younger.

Lesson #2: We do not harm those we love. Instead, we treat our loved ones with care and respect, even though, unfortunately, we sometimes hurt those closest to us.

Lesson #3: Time is money. The repercussions of his actions mean Mommy and Daddy will have to work extra hours to cover the emergency room costs. He will be doing some work to help pay for the expense as well.

There is no way our son will not remember the lessons from this evening.

Drawing from our past experience with ambulance billing, I chose to drive, saving us $3,500+ or, at the very least, months of battling with the ambulance and insurance companies. We knew precisely where to go.

The Injury And Fix

After dropping off my wife, daughter, and son at the ER at 7:15 am, I parked the car across the street. Seeing that my son wasn’t doing well, I took him back to the car to decompress, explaining that the wait would likely be 2-3 hours based on past experience.

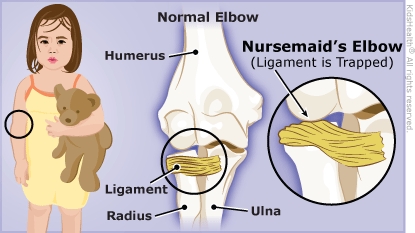

Fortunately, the emergency room wasn’t too busy that evening. After an hour of waiting, the doctor examined our daughter’s arm and suspected it was a common dislocation known as nursemaid’s elbow.

The doctor performed a simple adjustment, and felt her elbow click back into place. Though our daughter cried initially when the doctor moved her arm, she instantly felt better.

The doctor left for 15 minutes to allow our daughter time to recover. Within a minute or two, my wife noticed our daughter was bending her injured elbow to tightly hug her lovey, which my wife had smartly brought along. When my wife asked our daughter how her arm felt, she calmly said “it feels better” with a sweet smile.

Thrilled, my wife scooped her up, flagged down the doctor and told her it worked! We then asked our daughter to show the doctor she could move her arm, but she initially refused. However, when the doctor requested a high five with her injured arm, our daughter complied. It was a moment of relief that brought big smiles to all our faces!

No X-rays were needed. Hooray! That’s at least $200 saved, I thought to myself.

The Cost Of Going To The Emergency Room

The reluctance to go to the emergency room is akin to enduring two kicks to the groin, stemming from concerns about both the person’s health and the associated costs.

My hesitation in taking our daughter to the emergency room primarily revolved around the potential expenses and inconvenience, compounded by uncertainty about whether she was simply feeling particularly whiny after a long day.

If the cost of going to the ER were nonexistent or reasonable, I wouldn’t hesitate going. However, if this were the case, it’s likely that everyone else would follow suit, potentially overwhelming the ER with visitors.

The anticipated cost of this ER visit will be around $1,100, despite currently paying $2,300 a month for an unsubsidized insurance plan, specifically a Select Plus PPO Gold plan.

The breakdown of the $1,100 ER visit is as follows:

$500 In-network plan deductible

$250 ER Network Per Occurrence co-pay

$150 estimated for 20% co-insurance for outpatient services in-network. Our insurance company estimates the cost of an ER procedure for nursemaid’s elbow is roughly $6700, but this ultimately varies by provider.

We’re also uncertain if the hospital will additionally bill us for triage when they initially took vitals. Given there’s a cost for everything though, they probably will charge us another $100 – $200.

While we are immensely grateful for the doctor who corrected our daughter’s elbow, paying $1,100, especially after spending 2.5 hours on babysitting to work on my book, is hard to swallow.

At least we decided to go that evening instead of wait until the next morning. That would have been hours of misery as our daughter probably would have waked up multiple times until we had to go in the early morning.

Related: How To Get Subsidized Health Care Insurance As A Millionaire

The Cost Of Being A Parent May Be Higher Than You Think

The more children you have, the higher the likelihood of encountering challenges. As a parent, a lingering sense of apprehension often creeps up, anticipating that something may eventually go awry. The true health of your child may not become apparent until they reach around 15 years old.

Reflecting on my own childhood in Taipei, at the age of eight, I experienced several hospitalizations due to severe allergic reactions, marked by red spots and breathing difficulties. Despite the challenges, my mother’s comforting visits, complete with my favorite He-Man figurine, provided solace during those trying times.

Around the age of 3.5, children tend to become more aware, offering parents a sense of relief that major accidents are less likely. By the age of 5.5, most kids should exhibit a degree of self-sufficiency. However, as they engage in vigorous activities like running and roughhousing, injuries become more commonplace.

I must redouble my efforts to replenish my savings, depleted by our recent home purchase, and prepare for impending property taxes and private fund capital calls. Life is currently on hard mode and I’m hoping there won’t be further unexpected difficulties.

Navigating the path to financial independence as a parent proves challenging, yet there’s no alternative but to persevere, overcoming obstacles one by one.

Tips On Affording The Emergency Room And Minimizing Stress

Skip the ambulance for non-life threatening emergencies.

Skip the ambulance if you are able to drive safely and quickly to the ER. It might take an ambulance 5-15 minutes to get to where the emergency is and another 5 minutes to load you in and go. Then there’s the exorbitant cost of riding in an ambulance to deal with.

Map out the exact location of the closest ER and second-closest ER.

When you’re dealing with an emergency, your brain can sometimes malfunction without proper pre-mortem planning. Save the ER addresses in your phone and maps app.

Build an emergency fund equal to six months of living expenses or more.

Depending on your healthcare provider, how much insurance you’ve used, and your status, visiting the ER would get extremely costly. Your emergency fund will help blunt the financial cost, but it will still hurt.

Call your health insurance company today and ask what type of coverage they have for ER visits.

Ask about your deductible, co-pay, and co-insurance. Ask them to run various scenarios so you can better budget potential future ER expenses.

Shop around for different plans.

During the next open enrollment period, carefully compare health insurance plans and forecast your future medial needs to try and save money. If you know you have something big coming up, like surgery, you may want to get a higher end plan with a lower deductible.

Ask your doctor about various options.

Trust your doctor’s advice given they’ve seen all types of emergencies and generally have a good idea what to do. However, feel free to question whether some procedures are necessary to save money. Ask about the risk and reward of doing something and not doing something.

Have more than one backup for childcare.

Having one regular babysitter may not be enough given they may be traveling, sick, working, or simply busy. Have two or more people you can turn to for childcare support, including your friends, fellow parents, or neighbor if relatives are not around.

Talk to your kids about body awareness and safety.

Even though your kids might not listen, talk to your kids about safe play. If you have an older sibling, make them understand they cannot play as rough with a younger sibling due to size, strength, and developmental differences.

Given all the information and tools necessary for your childcare provider to provide the best care.

Give your childcare provider some things to look out for to help minimize injury, e.g. allergic to certain foods, sprained body part, lack of body awareness, etc. Print out a list of important telephone numbers to call in case of an emergency, e.g. 911, your number, your partner’s number, backup childcare person’s number, close friends and relatives, your neighbors.

Pay closer attention as a parent and be stern when the risk increases.

Being an engaged parent for long periods of time takes tremendous effort. It’s easy to zone away on the phone while your four-year-old is dangly precariously from a tree limb. We must try our best to remain engaged, especially in environments that could be dangerous.

The pool or ocean are two of the most dangerous environments for beginning or non-swimmers. One look away and disaster could strike. Teaching your kids to swim is one of the best exercises for building a parent’s childcare endurance.

Reader Questions and Suggestions

Have you gone to the emergency room lately? If so, what happened and how much did it cost? How did you end up paying the bill? Is there a better way to save money on a ER visit?

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Please share, rate, and review!

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Q2 2024 Earnings Call Transcript")