Jose Luis Pelaez Inc/DigitalVision via Getty Images

GoHealth (NASDAQ:GOCO) is a large-scale broker of insurance products, especially the popular Medicare Advantage plans in which Medicare benefits are delivered by a private insurer, although the company brokers for Medicare supplement plans and other insurance product lines as well. The basic outline of the business model is this: consumers looking for a Medicare plan that best suits their needs can face a vast ocean of choices, with a range of benefit options from multiple insurers that can be overwhelming to compare and contrast. To help guide consumers through the process, GoHealth functions as an intermediary between consumers and multiple insurance partners, and when GoHealth onboards a new enrollment, the insurer underwriting that policy is contracted to pay a commission to GoHealth.

I last covered GoHealth in an article in November 2023, and my bullish thesis centered around the following, to quote myself:

new potential investors are presented with a company that is now generating cash flow from its operations, but at a price to operating cash flow ratio of just 3.70x on a trailing year basis, and 3.35x at the midpoint of guidance for operating cash flow for 2023 of $95 million. . . A price to operating cash flow multiple of 6x, which is more in line with the financial sector, would suggest a fair value closer to $25 per share.

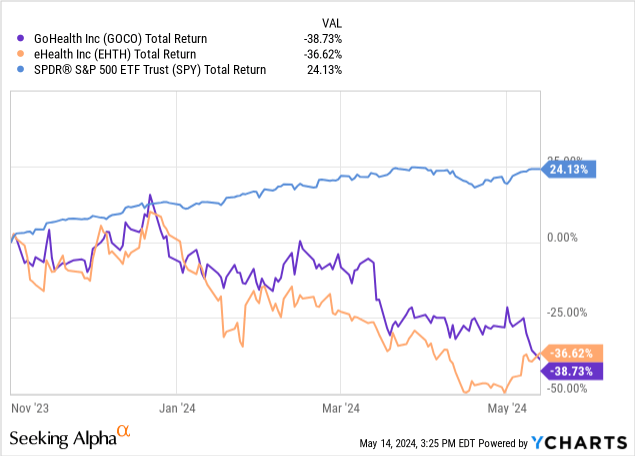

Since writing that assessment, the shares have continued to drop largely like the market peer eHealth (EHTH), in spite of what I consider to be a steady dose of good developments from a fundamental standpoint.

I remain as bullish as I did previously on GoHealth, but anticipate this will be a slow-moving train getting back to fair value. The upside is that I believe the shares are fundamentally mispriced at these levels, giving investors an opportunity to build a position over time.

Financial Overview

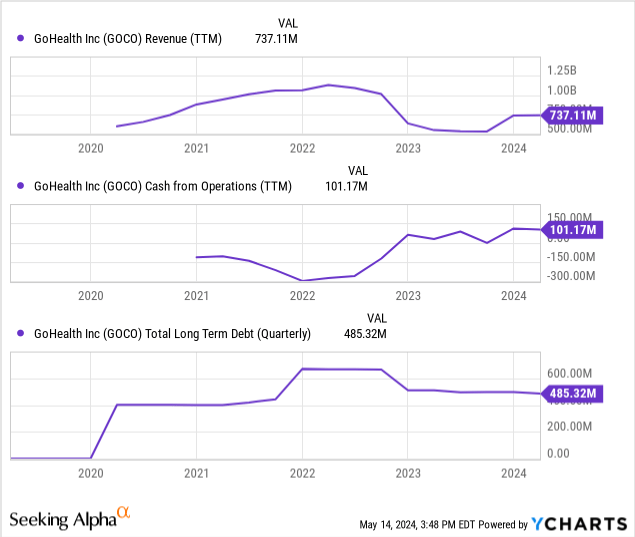

Full year 2023 and Q1 2024 reports are now available to parse, and in the big picture, I find that the overall trends I liked before, especially around generating positive operating cash flow, are still playing out as I hoped. I’ll get into more specific numbers below, but first pause and consider the story being told in the following three panels.

Taking a view over the trailing twelve months, revenue has rebounded slightly after, a period of de-emphasizing “growth at any cost” sort of mindset that had prevailed under a prior management regime. So while revenue did trend down for a time (purposefully), it was over this same period that new management began to intentionally focus on being profitable and turned to contain costs, especially around customer acquisition spending. The result, as shown in the first two panels, is something like a mirror reflection with a negative correlation; that is, when revenues started coming down is about when cash from operations started to rise.

GoHealth has now maintained a positive or break-even operating cash flow on TTM basis back to year-end 2023, or five consecutive quarters. While the total amounts are not massive in scale by any stretch – $101.7 million from Q2 2023 through Q1 2024 – the turn in and of itself is plenty impressive given the complete lack of history before then of even coming close.

We can likewise see that while the company was burning cash in operations, they turned in part to debt funding, but since operating cash flow has turned positive, the debt has been getting paid off. In fact, GoHealth is even paying off the debt on accelerated timeline with additional principal payments, making a $50 million payment in April and expecting to pay a further $25 million in Q4. This is significant for two reasons: first, the remaining debt will need to be refinanced soon, as it comes due in 2025 – there are no later maturities, so refinancing a smaller package of debt will be viewed as less risky by creditors. Secondly, GoHealth is currently on the hook for floating rates that bring its interest rate to about 13%. For Q1 2024, it paid nearly $18 million in interest expense, a figure that was about $1 million more than the same period in 2023, even though the principal balance was lower.

Outlook and Valuation

While the market cap of GoHealth has dropped some $100 million since November, the outlook offered by management is for relative stability to modest improvements. CEO Vijay Kotte wrapped up his prepared remarks on the Q1 earnings call by sharing his expectations on the coming year, saying:

First, we expect submission volume to grow in line with the overall Medicare market. Second, we expect our revenue to be flat year-over-year with incremental operating efficiency resulting in modest margin expansion. Finally, cash flow from operations is expected to be flat to slightly up as we continue our transition into the Encompass model and shift to non-agency revenue.

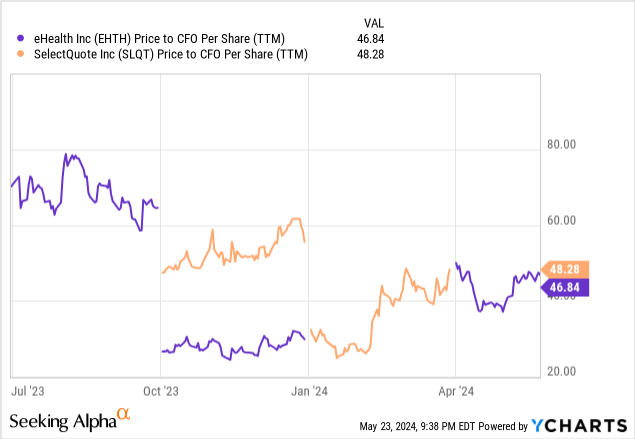

I am particularly focused on that operating cash flow commentary. At a market cap now of just $222 million, the price to operating cash flow on a trailing basis is just 2.20x and if that forward guidance holds together, then the forward multiple should be the same as now.

Is that good? There’s not a lot to work from in terms of direct comparison besides eHealth and SelectQuote (SLQT), but GoHealth at P/CFO of 2.20x certainly has all the appearance of paying an inexpensive amount for the cash flows relative to those peers at over 45.0x, especially if the quality of those cash flows are primed to be durable in the short term and grow in the long term.

While the ride may be bumpy getting there, given the demographic trends of the Baby Boomers and the favorable reception the Medicare Advantage program has earned, I hold little doubt that the total size of the market will continue to expand for some time. As a result, GoHealth is well positioned to continue serving customers for years and years to come. With a larger demographic cohort to target, the trends should naturally favor bringing down the costs on average customer acquisition, especially with management’s deeper focus on efficiency rather than growth at any cost.

With a good deal of future cash sitting on the balance sheet in the form of commissions receivable ($843.1 million in total, broken out as $269.8 million being current assets, and $573.3 million being long-term), operating cash flow has room to grow.

Risks & Mitigating Factors

There are a few noteworthy risks for GoHealth, specifically 1) what is going within the Medicare Advantage product and its oversight by the Centers for Medicare and Medicaid [referred to as “CMS”], and 2) GoHealth’s leverage position.

There are actually two dynamics at play with CMS and Medicare Advantage. First is what is known as the “rate notice,” in which CMS sets the reimbursements to health care providers; when Medicare Advantage plans administered by private insurers can do better than that rate, they basically get to pocket the difference, a model that has been quite profitable for many years. However, the new reimbursement rates are putting more of a squeeze on the ability of the private insurers to be as profitable, which is likely to lead to some insurers withdrawing from select markets.

Secondly, last month, CMS published its “final rule” updating regulation around the relationship between Medicare Advantage plans and certain aspects of compensation made to agents and brokers. The full text of the rule in the Federal Register can be found here, however law firm Sidley Austin LLP provided a very succinct summary. In a nutshell, Medicare Advantage plans were paying a wide range of fees to agents and brokers over and above the commissions, and/or finding contract provisions between Medicare Advantage plan providers and brokers to not necessarily disclose all plan options available to all customers. CMS finds this sort of behavior to be detrimental to US taxpayers, and so it is tightening the rules by attempting to clarify what agents and brokers should and should not be paid for, essentially trying to wring out the charging of endless “administrative fees.” To quote from the summary (edited for length):

The final rule eliminates administrative fees and consolidates commission-based compensation subject to a single cap. Key provisions of the rule include:

- Elimination of separate administrative fees.

- Caps on agent and broker non-salary compensation.

- Prohibition on contract terms that prevent objective advice to beneficiaries.

- Termination of fee reporting.

. . .the changes do not distinguish among the different types of agents and their employment relationships and are not narrowly targeted to rein in abusive behaviors. Some [third-party marketing organizations] pay their agents and brokers through salaries, so they would not be affected by the caps.

To any broker, there will be some cause for concern here, although GoHealth is one that pays its agents salaries. Management is studying the issue and at this time believes they are compliant with the regulations. Mr. Kotte gave a detailed and vigorous answer to the question from an analyst on the topic (edited for length, although the entire answer is fully worth reading in the transcript):

the general underlying concept here is that CMS is very focused on inappropriate incentives to independent agents and brokers, whereby [they] may be influenced to write one health plan or policy type over another one based solely on their reimbursement. And uniquely for us as GoHealth operates, our agents . . .are generally hourly wage or salary wage, and they have a very minimal variable compensation. And even that variable compensation that they do receive is health plan agnostic. . .we go further to compensate our agents for not selling or enrolling a consumer in a new policy by just making sure they get peace of mind. So really the variable tie for us is about providing a service as opposed to delivering a new enrollment. . . In concert with that, though, what we will say is our efforts to go beyond the minimum standards established by the CMS regs are what we’re focused on. It’s not about meeting the minimum threshold. It’s about doing the right thing and being differentially better for consumers and for the health plans that we also partner with in the process.

Ultimately, this rule may force a large-scale change in the broker industry, but GoHealth appears to be on top of things from a regulatory standpoint; Mr. Kotte did indicate some of their contracts will require tweaking. I have high confidence that any adjustments in how they operate will be relatively minor, as they have already laid much of the necessary groundwork. Nevertheless, it is a pertinent story-line that is a legitimate risk factor for investors to be aware of.

On the other major risk factor, leverage, GoHealth has debt of $435.3 million (after accounting for the $50 million prepayment made in April) coming due by 2025, with $75 million of it being current as of the end of Q1, and the balance due later in 2025. The good news is that there are no other maturities, so this is the full picture; the bad news is that interest rates on this debt were floating rates, and these are still on the higher side of things, which might complicate refinancing. Nevertheless, the company has serviced its debt without issue, is generating operating cash and prepaying some of the principal, meaning I fully expect that GoHealth will manage to refinance next year at a lower interest rate than they are currently stuck with, especially if the cash flows continue to show a positive trend through 2024. If they succeed in making the additional $25 million principal payment later this year, then the total amount to refinance should be in the ~$335 million range, versus an operating cash flow expectation of around ~$105 million, a ratio that I do not find to be too stretched.

Concluding Thoughts

In spite of the evolving background of CMS regulations for Medicare Advantage that could put GoHealth and its peers under a bit of a microscope, the larger story is the delivery of operating cash flows. With a short but growing track record revealing that operating cash flow on a trailing twelve-month basis is able to remain positive, and management confidence that this trend will continue, the valuation here is an appealing one. Even though the recent share price action has been disappointing, I really think GoHealth is a hidden gem in the market, and consider it a “Buy” on cash flow and deleveraging going forward.

Q2 2024 Earnings Call Transcript")