Andrey Zhuravlev/iStock via Getty Images

Technical signals for breaking out

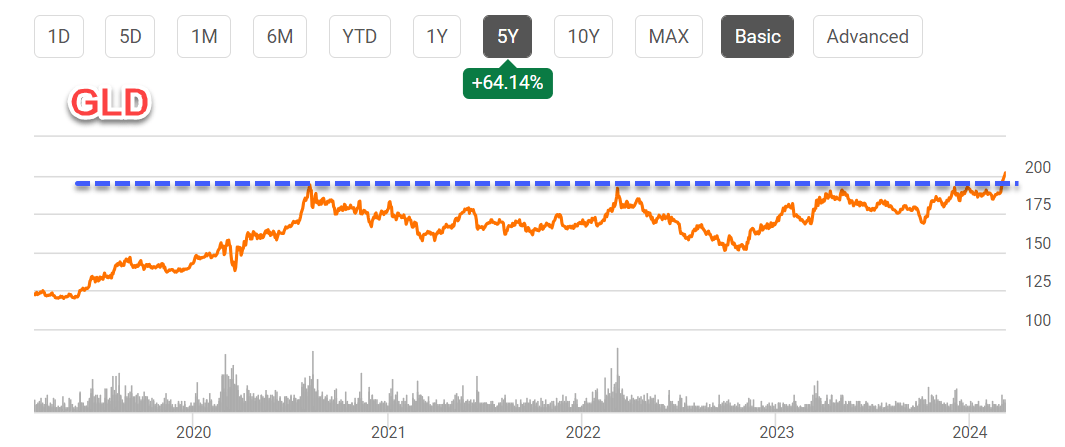

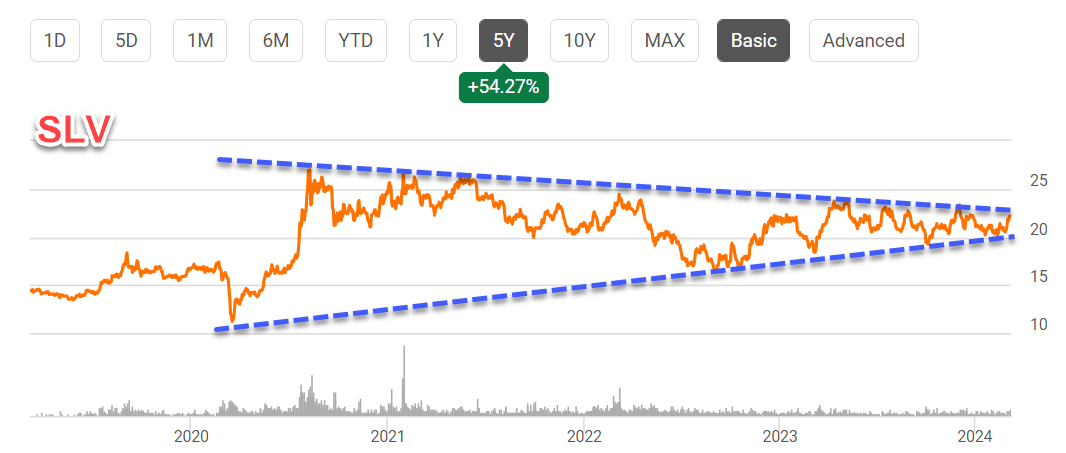

The SPDR Gold Trust ETF (GLD) and iShares Silver Trust ETF (SLV) have delivered decent returns in the past few years. As seen in the next two charts, GLD prices have rallied by more than 64% in the past five years (top figure) and the SLV by more than 54% (bottom figure).

However, at a more macroscopic scale, both metals’ prices have been in a consolidation window in the past ~4 years in my view. As seen in these charts, GLD has been largely trading sideways with defined support and resistance levels, around $150 to $200 respectively. And its recent prices began to break out of this range. SLV has been trading in a narrowing wedge. As the consolidation progresses, the wedge is now very tight as seen, where a breakout often tends to occur. Furthermore, my past experiences have shown that longer consolidation periods (in this case, a ~4-year consolidation) can lead to more explosive breakouts when they finally occur.

Seeking Alpha data Seeking Alpha data

In the remainder of this article, I will argue that there are other fundamental catalysts that can support a breakout besides the above technical signals. My top arguments are the central banks’ appetite for gold and also the attractiveness of silver considering based on gold-silver price and silver production.

GLD and SLV: quick introduction

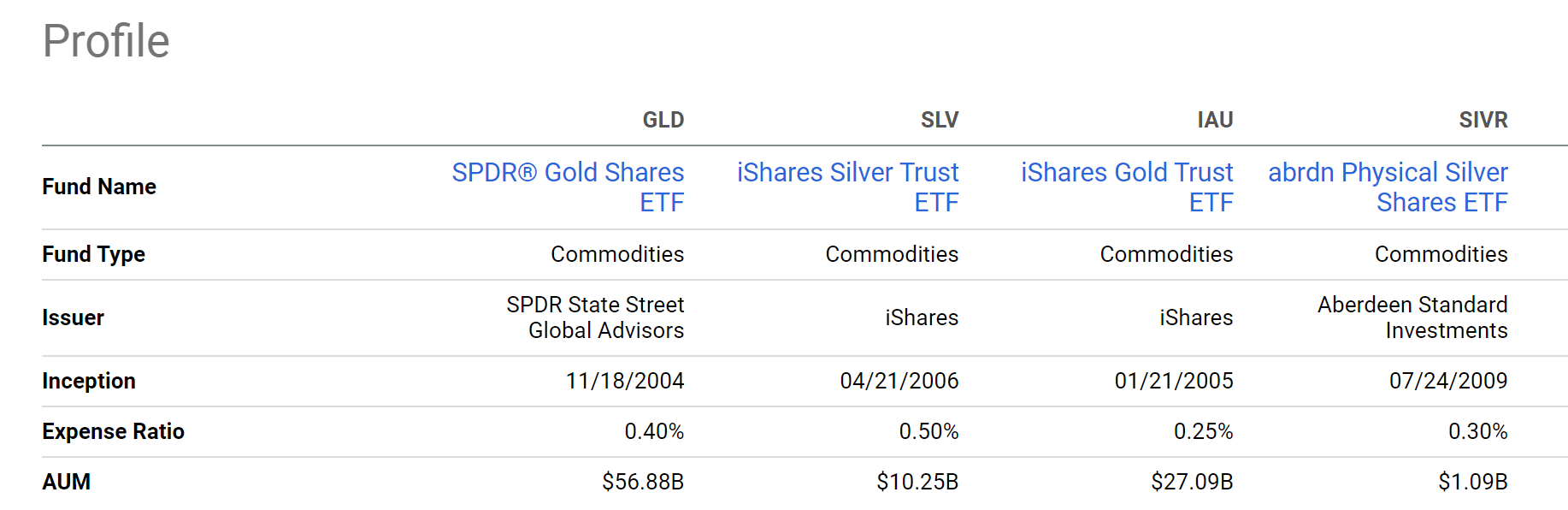

Before going into further details, I will first introduce these two ETFs briefly based on the chart below in case there are readers new to them. Both GLD and SLV are ETFs that invest in physical precious metals. As the name suggests, GLD invests in gold, while SLV invests in silver. GLD has an expense ratio of 0.40%, while SLV has an expense ratio of 0.50%. These fees are relatively higher than their competitive funds, such as IAU and SIVR. However, they make up for the high fees with their larger assets under management (“AUM”) and better tradability as a result. As seen in the chart, GLD has an AUM of $56.88 billion, by far the largest gold ETF. And SLV features a $10.25 billion AUM, almost 10x larger than SIVR.

Seeking Alpha data

Central bank’s appetite for gold

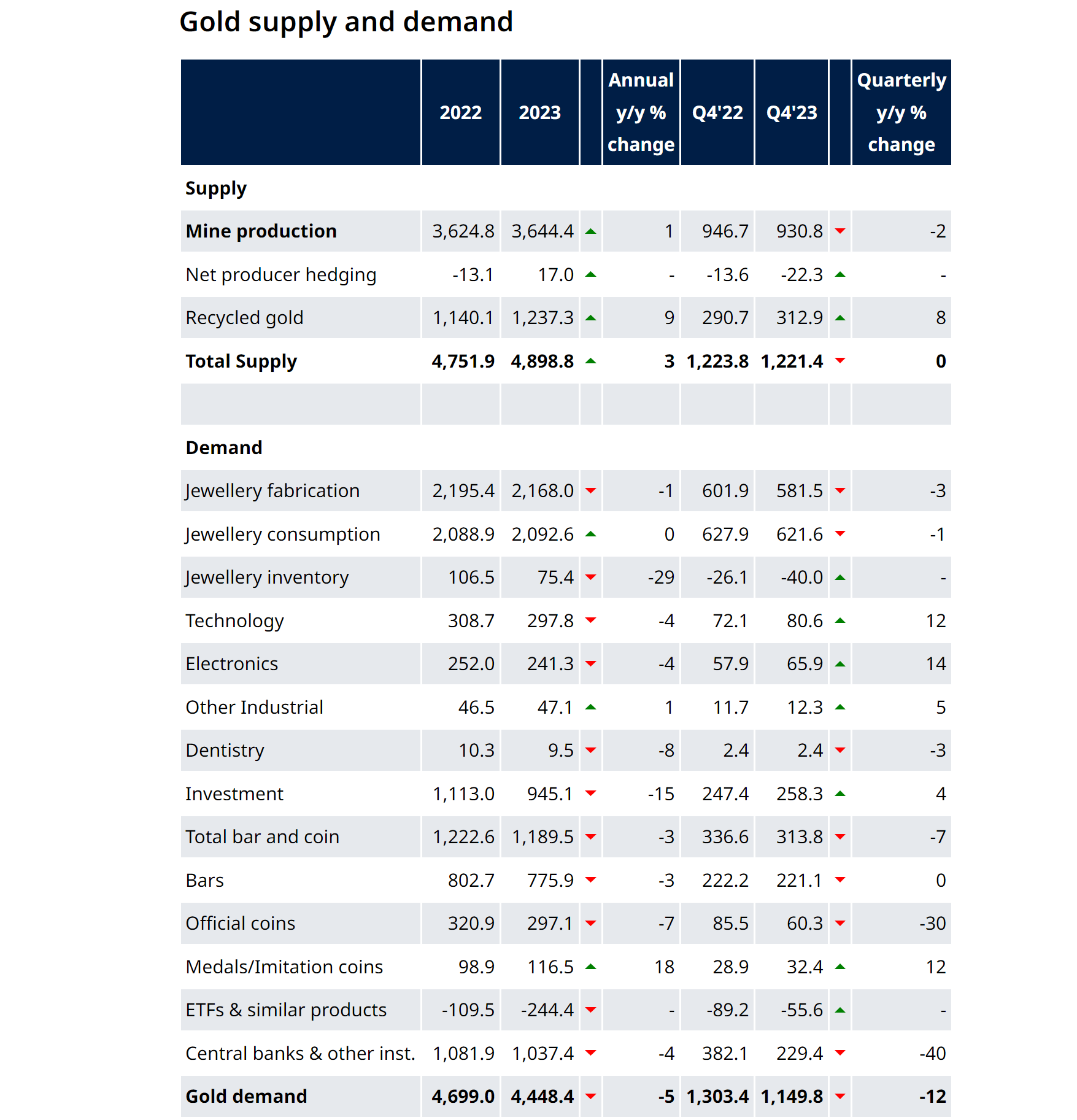

Now, let me get back to the first fundamental reason that could support a breakout: the central bank’s appetite for gold. The World Gold Council recently released its latest “2023 Global Gold Demand Trends Report”, which showed that global central banks purchased 1,037 tons of gold last year, the second highest in history, only 45 tons less than in 2022 (See the next chart below). It is worth noting that given the global gold demand of ~4,448 tons last year, the 1,037 tons of gold reserves purchased by central banks accounted for about 1/4 of the global gold demand.

World Gold Council

Looking ahead, I see good reasons for global central banks to remain enthusiastic about buying gold. Take China, the second-largest economy, as an example. Based on BullionByPost data,

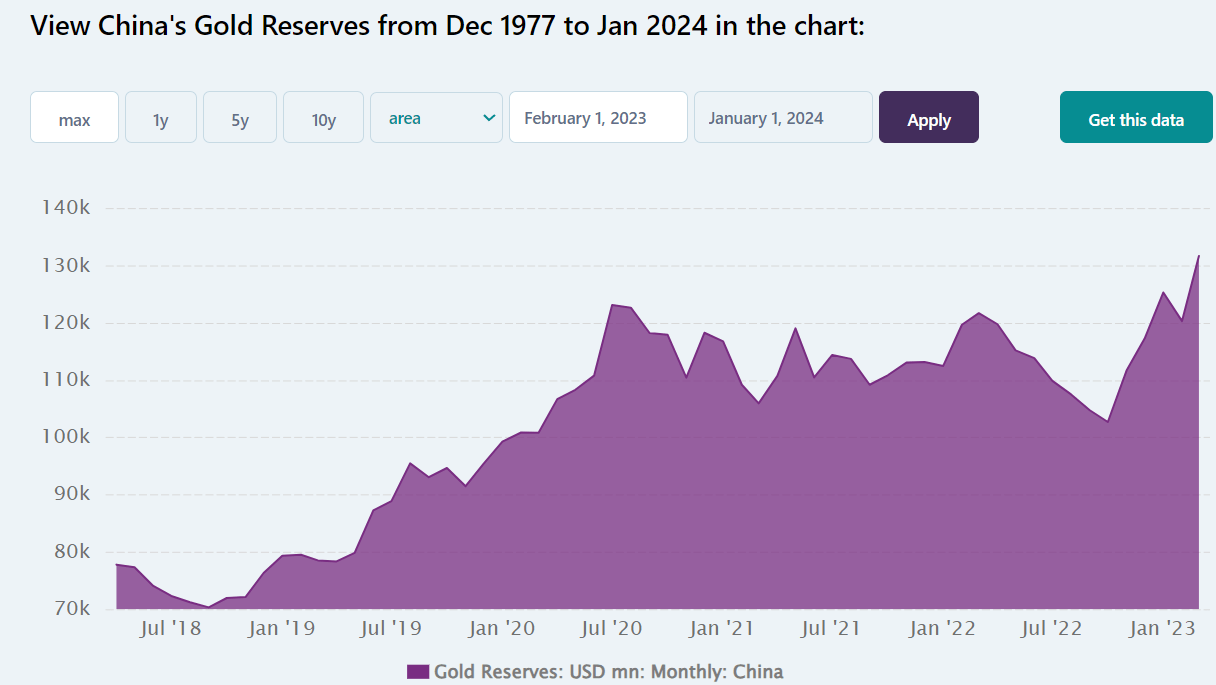

At the end of January 2024, China’s official gold reserves stood at 2,191.53 tonnes. China has seen significant growth in its reported gold reserves in recent years, adding 243.22 tonnes alone since summer 2022. Despite the growth in reported figures, many analysts believe the true figure for China’s gold reserves is likely to be much higher.

To better anchor these numbers, the next chart taken from CEIC’s economic database provides a visual of the sharp gold reserve in China. And to provide a broader context, China is “only” the 6th largest country in terms of gold reserve. The top 5 are the U.S., Germany, Italy, France, and Russia. In my view, gold’s role as a safe haven asset has not changed at all and is only accentuated in times of uncertainty like our current time – with multiple regional wars ongoing and many countries trying to diversify their central banks’ foreign exchange reserves away from the U.S. dollars.

CEIC’s economic database

Silver: demand prospects and production cost

I am even more bullish on SLV than GLD for a few reasons. Compared to GLD, SLV features a more pronounced dual nature – both as a precious metal and an industrial metal.

As a precious metal, silver is seen as a store of value and hedge against inflation/uncertainty, just like gold. However, compared to gold, silver features more industrial applications also. Especially with the rise of new technology in the coming years, I see several reasons why silver demand can surge quickly. The top factor is the growth in green technologies. Silver is a key component in many green technologies, particularly solar panels and electric vehicles. Silver’s excellent conductivity makes it irreplaceable in these applications. Beyond green tech, silver has several other industrial applications that are seeing growth, including 5G infrastructure, consumer electronics, and brazing & soldering.

Despite the anticipated demand surge, the current silver price is quite compressed compared to production cost in my view. It is difficult to pin down the cost of producing silver to a single and fixed number, as the cost can vary substantially depending on many factors such as mine location and efficiency, ore grade, byproduct vs. primary metal, et al. With such variations in mind, some miners quote an all-in sustaining costs (“AISC”) to be in the $22-$23 range (based on per ounce of silver) in 2024, compared to the current silver price of $24.7 only as of this writing.

Other risks and final thoughts

A few other risks, both in the upward and downward direction, are worth mentioning before I conclude. For silver, another bullish factor to consider is the favorable mint ratio for a gold-silver trade. The concept is detailed in my earlier article, and the gist is that:

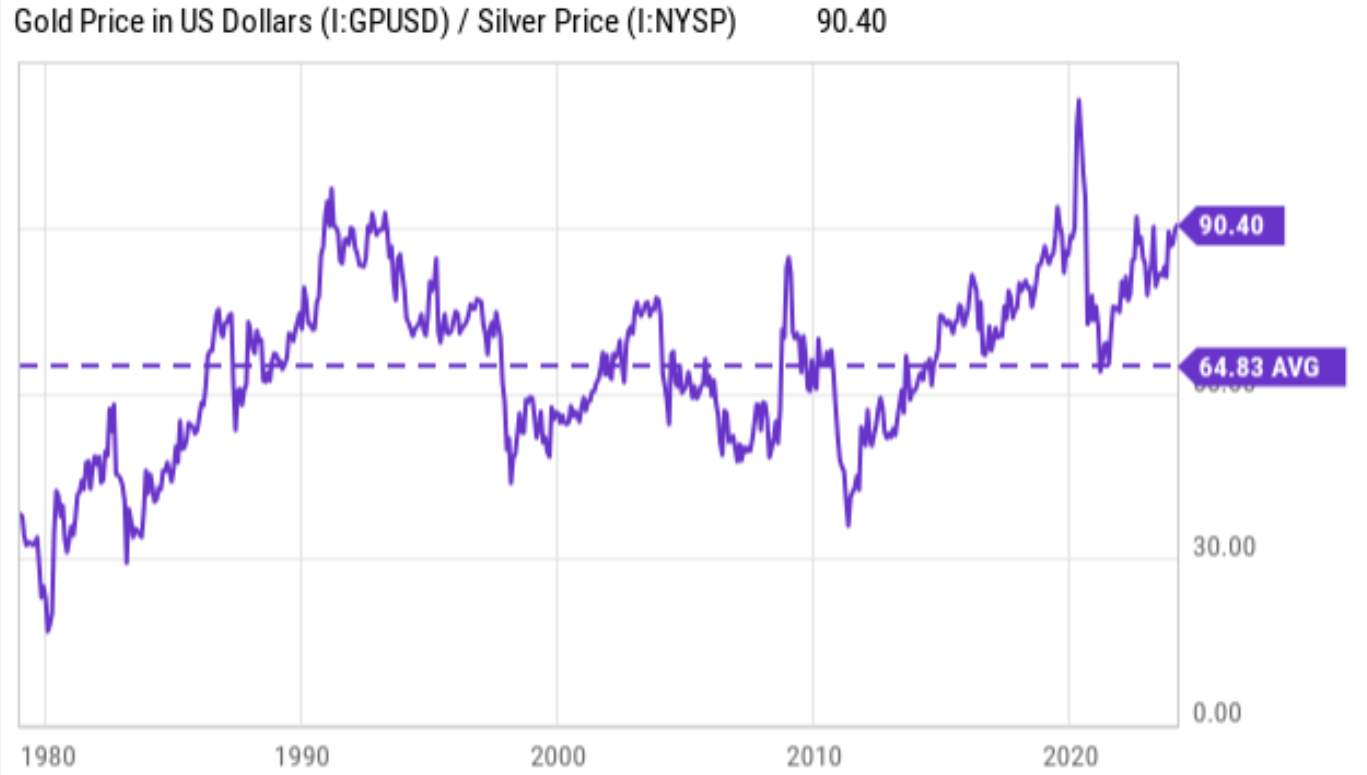

The trade simply involves selling a certain amount of gold to buy silver when the silver price appears more attractive relative to the gold price, and vice versa. The key metric to evaluate which metal’s price is more attractive is the so-called mint ratio or the gold-silver price ratio (“GSPR”).

The mint ratio in the long term is shown in the chart below. As seen, it has an average of ~64.8 in the past ~5 decades or so. The ratio currently hovers around 90.4x, among the highest levels since at least 1980.

Seeking Alpha data

In terms of downward risks, GLD and SLV face all the risks generic to commodities. These risks include lack of active cash flow (i.e., GLD and SLV do not generate income by themselves), extreme price volatilities, relatively high expense ratios as aforementioned, and tax consequences. Besides these generic risks, holding GLD and SLV is different from holding physical bars (even though they are backed by physical bars). Holding these ETFs entails the following counterparty risk:

Essentially, investors do not own the physical metal directly. Instead, investors own shares of GLD or SLV, which are a CLAIM on the underlying physical bars. As such, there is always a risk that the ETF sponsor or custodian could default and won’t be able to fulfill their investors’ claims.

All told, the article argued for a bullish thesis on GLD and SLV. Technically, I see strong signs for them to break out of a consolidation window that has been lasting for ~4 years.

These technical signs are supported by fundamental forces at play in my mind also. The top forces in my mind are the central banks’ appetite for gold amid the current geopolitical conflicts and the potential demand surge for silver as several new technologies (such as EV, solar panels, and 5G) begin to enter their exponential growth phase.

Q2 2024 Earnings Call Transcript")