AntaresNS/iStock via Getty Images

Introduction

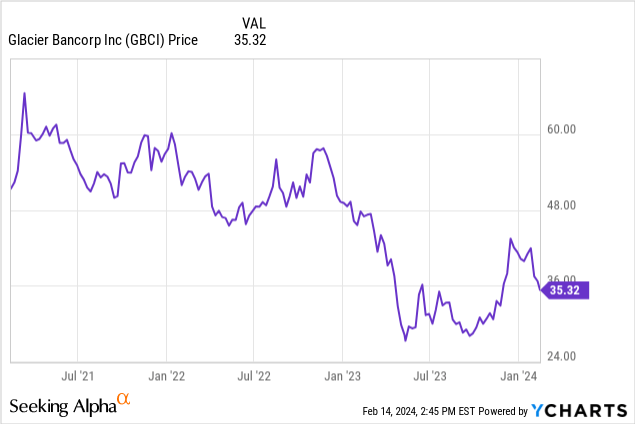

In the summer of 2022, I argued Glacier Bancorp, Inc. (NYSE:GBCI) was a well-run Montana focused bank, but I wasn’t willing to pay 3 times the tangible book value, or TBV, for the bank. Fast-forward to now, just over eighteen months later, and the bank’s share price has indeed come down by approximately 30% while Glacier Bancorp completed an additional seven quarters, retaining a portion of its net profit on its balance sheet. So, I figured the FY 2024 results would be a good moment to check up on the bank’s health and prospects, and to check if it already is trading at a valuation I could stomach.

The financial performance remains strong and non-performing loans low

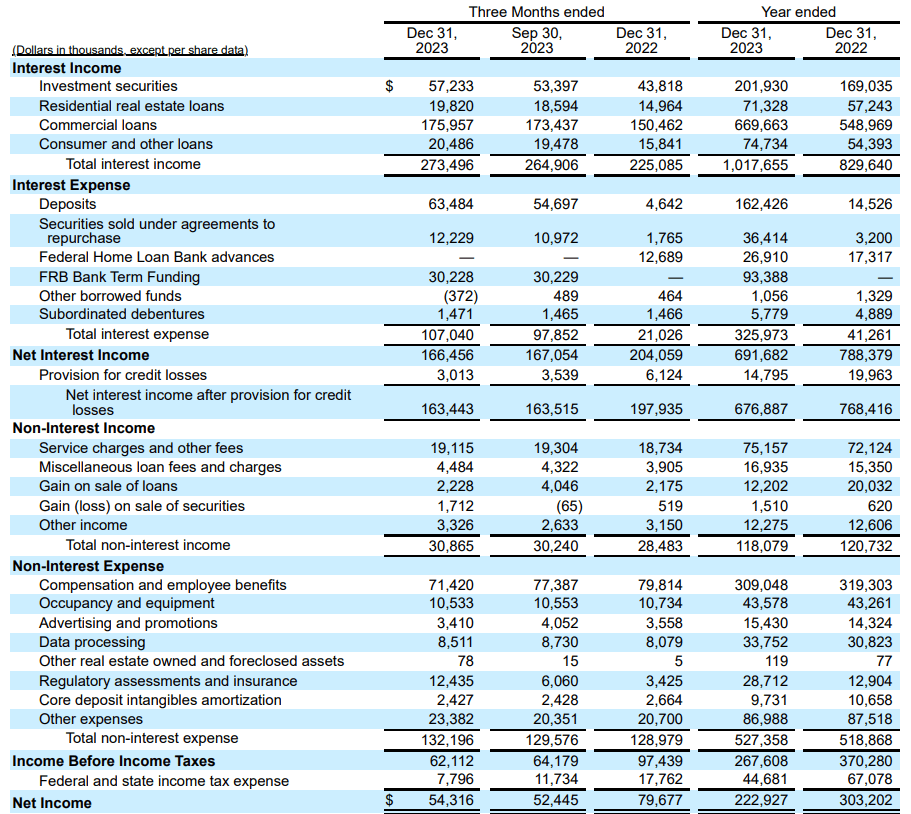

Glacier Bancorp reported a total interest income of $273M in the final quarter of 2023 which is an increase of approximately $8.5M on a QoQ basis. Meanwhile, the total interest expenses increased by just over $9M on a QoQ basis, and that’s the reason why the net interest income showed a very small decrease. Whereas the bank recorded a net interest income of $204M in Q4 2022 and $167.1M in Q3 2023, its Q4 2023 net interest income fell to $166.5M.

GBCI Investor Relations

As the income statement above shows, Glacier Bancorp also recorded a total of just over $101M in net non-interest expenses resulting in a pre-tax and pre loan loss provision income of $65M in the final quarter of the year. And just like in previous years, Glacier has been able to keep the loan loss provisions pretty low (I will discuss this in more detail later in this article), and in Q4 2023 it recorded just $3M in loan loss provisions compared to $6.1M in Q4 2022 and $3.5M in Q3 2023.

This resulted in a pre-tax income of $62.1M and a net profit of $54.3M thanks to a relatively low average tax rate. The total net income generated during the entire financial year was $223M, and divided over the 110.9M shares outstanding at the end of the period, the EPS was $2.01.

While that’s definitely a lower result than Glacier’s performance in 2022, the bank has for sure been able to keep the damage pretty limited. After all, the net interest margin did decrease from 3.27% in 2022 to 2.73% in 2023. And, with a loan book size of in excess of $16B, that half a percent difference has a substantial impact on the bank’s bottom-line result.

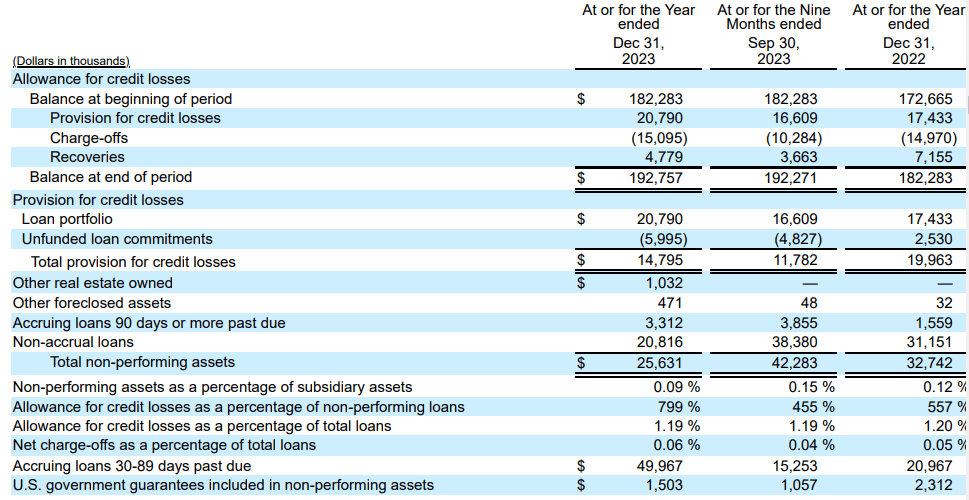

One of the main reasons why Glacier’s performance remains strong is because it has a high-quality loan book. At the end of 2023, the total amount of non-performing assets was actually lower than at the end of the third quarter, and it was lower compared to the end of 2022 as well. With just $25.6M of the assets classified as non-performing assets, the ratio of NPAs as a percentage of the total asset base was less than 0.10%.

GBCI Investor Relations

Even if you’d only look at the loan book, the non-accruing loans of $20.8M represent just 0.13% of the entire loan book. And as you can see above, the bank’s total amount of loan loss provisions exceeds $192M, which means the loans that are currently classified as non-accruing are very well covered. Even in the very unlikely event the bank doesn’t see a dime back, the existing provisions are more than sufficient to cover all losses. So, we can expect the loan loss provisions on the income statement to continue, but at the current relatively low level. The recent acquisition shouldn’t have a material impact on the loan loss provisions as a percentage of the entire loan book.

Investment thesis

Glacier Bancorp continues to have one of the lowest amounts of non-accruing loans in the sector, and that likely helps it to maintain its premium valuation. Trading at approximately 17 times the 2023 earnings and at a premium of 95% to its tangible book value per share, Glacier Bancorp, Inc. is for sure still trading at a relatively expensive level. Sure, the dividend yield is currently 3.75%, which is pretty decent considering the payout ratio is less than 70%, but income-seeking investors can easily go elsewhere to find a better yield. The preferred shares issued by Bank OZK (OZK), for instance, yield approximately 7%, which would likely be more appealing to income investors than the common shares of Glacier.

Q2 2024 Earnings Call Transcript")