JohnnyPowell

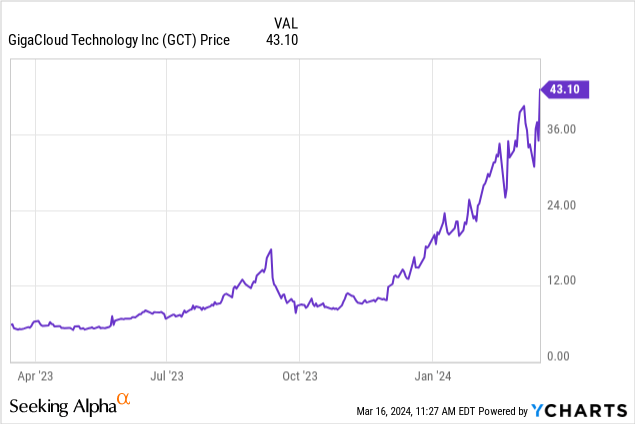

Today, we are taking a look at GigaCloud Technology (NASDAQ:GCT). This stock is skyrocketing in the last few months, with investor optimism at all-time highs for this growth company. This is a stock we have looked at in the past, one that we noted had the potential to double in 2024. Well, we have a stock that has tripled since mid-December. Take a look at this beautiful chart:

Now here is something to consider. The stock had debuted 2022, and took flight, hitting nearly $22 as an intraday high in its debut. It quickly fell to single digits and moved mostly sideways for a year. The stock enjoyed a speculative bounce in the late summer of 2023, only to falter. Then, it started catching fire in mid-December 2023. The question is whether this run can continue. The stock has run hard with the market rally of 2024. We could easily see a reversal, and one that hits the stock for a correction on the order of 30% in a week. It is tough to say what will trigger it, but often stocks that make runs like this often give a significant portion back. Investors should understand this reality. With that said, we see no catalyst to reverse sentiment. We see the stock moving higher long-term, as the growth has been impressive, and management is executing well. So in the short-term, expect some chop, but we do think this run continues long-term, with some healthy corrective action in between.

GigaCloud Technology Operations and Ratings

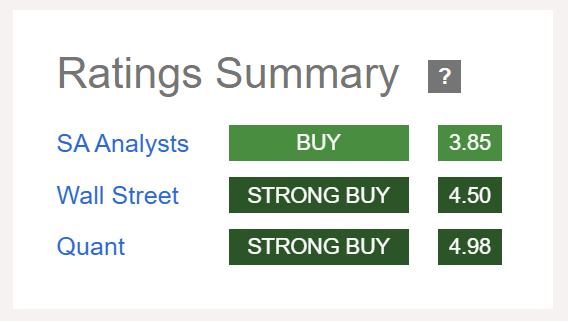

For our followers who may not be familiar with the company, GigaCloud Technology is an online B2B marketplace that facilitates the international trade and transport of bulky goods, including furniture, appliances, fitness equipment, and gardening equipment. In addition to the marketplace, GigaCloud also manufactures its own furniture and provides fulfillment services. We see shares as a buy. It also enjoys positive ratings from our colleagues at Seeking Alpha, Street Analysts, and also has some solid Quant ratings:

Seeking Alpha GCT ratings

So what is so exciting about this operation? This is a high-growth story, and even with the share ramping up significantly, it still is not wildly overvalued. The valuation is certainly stretched versus just a week ago, but the growth in our opinion justifies this expansion in valuation. One of the catalysts for more growth has been a recent overhaul of the business model to simplify operations. The new business model streamlines the supply chain by bringing fulfillment in-house, and managing the process from factories directly to customers. This should reduce complexity, costs, errors, and delays, potentially boosting GigaCloud’s efficiency and profit margins. However, the transition is ongoing, and recent acquisitions aim to bridge any shortfalls. The long-term impact remains to be seen, so while it appears to be a winning proposition, it needs to be monitored for success. All that said, a simplified operation suggests financial improvements are likely to continue.

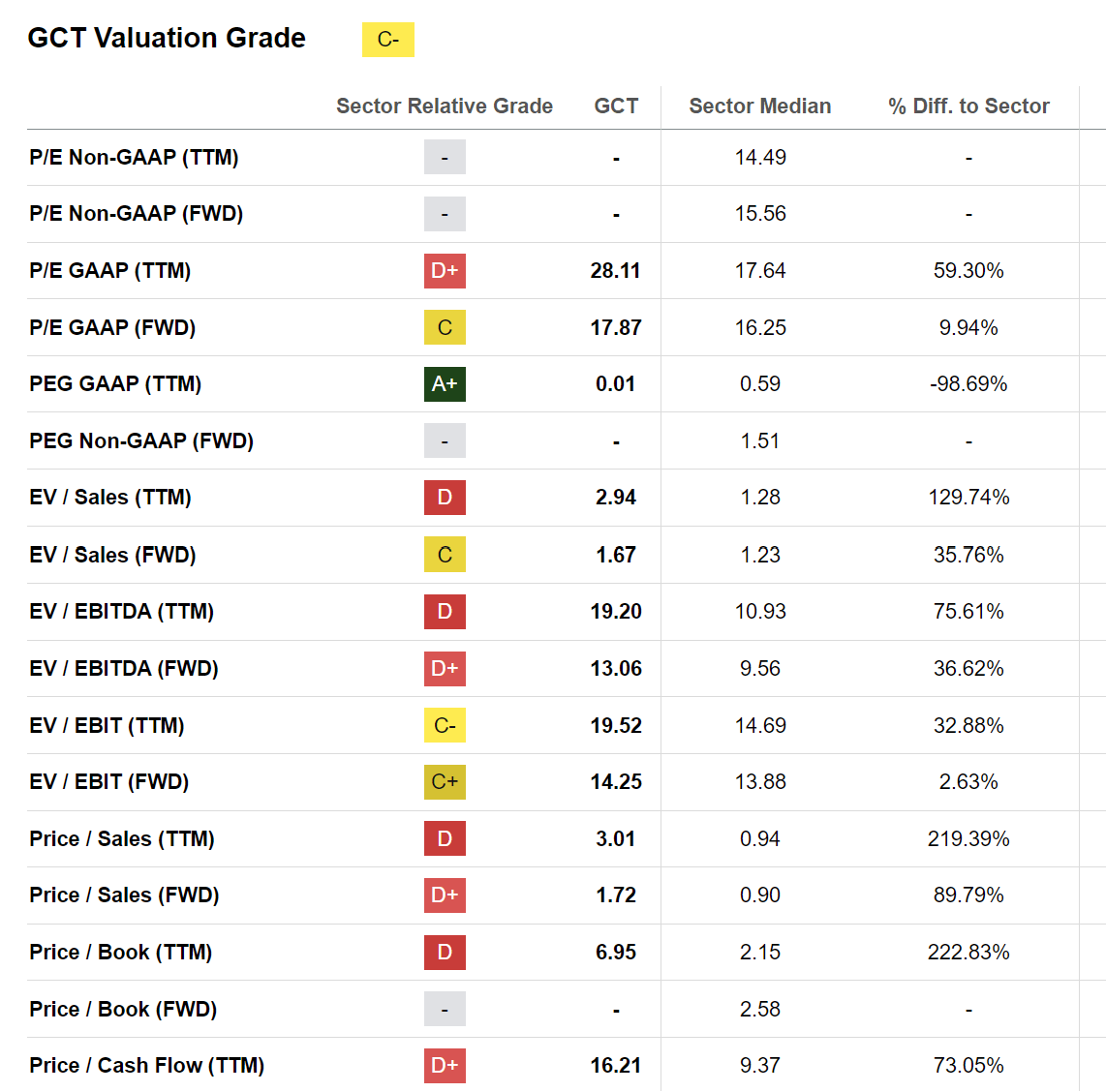

This was evidenced by the just-reported earnings. We mentioned this was a strong growth stock. Need some evidence? How about the fact that in the quarter total revenues were $244.7 million surging 94.8% from $125.6 million in Q4 2022. Not only did sales ramp up, but there was notable margin improvement that led to better gross profit. Gross profit was $69.8 million, ballooning 161.4% from $26.7 million in Q4 2022. Gross margin increased to 28.5%, a 730 basis point improvement from 21.2% in Q4 2022. Outstanding improvement. Adjusted EBITDA was $43.8 million, jumping 188.2% from $15.2 million in Q4 2022. And, this is not a company that is not turning a profit either, unlike so many tech companies. Net income was $35.6 million in the quarter also surging 184.8% from $12.5 million a year ago. This translated to EPS of $0.87. We expect this stock can continue rising, as this growth, in our opinion, justifies the expansion in the valuation metrics we have seen. And even with this massive leg higher in the stock, the valuation remains reasonable. Check out the valuation quants:

Seeking Alpha GCT valuation

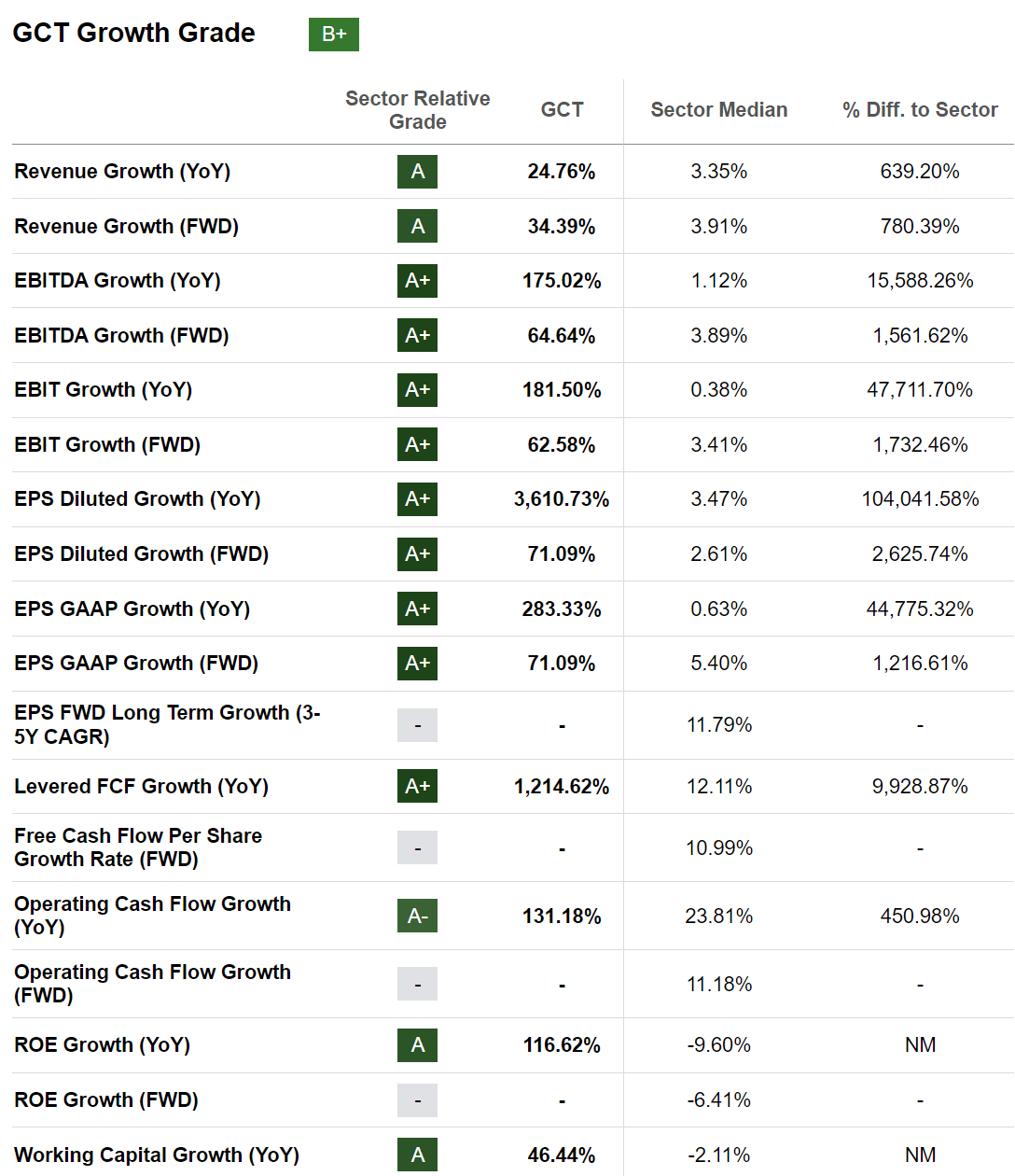

The overall ratings have slipped, coming in at around ‘average’ value. But folks, you need to balance this with the extreme growth. Check out the growth quants:

Seeking Alpha GCT growth quant

The numbers really speak for themselves.

But what beyond the business model transformation is driving such growth? Well, the company has now successfully integrated Noble House and Wondersign, and that has aided in GigaCloud taking a huge step forward in its global expansion. With this integration, the company is now operating in diverse geographies, has a much wider product portfolio with premium products, and expanded its business network. That comes on top of the core business’ organic growth. The company is spending working capital to bolster research and development to boost its cloud infrastructure. This company is really making strides in innovating and enhancing the supply chain. It is extremely impressive.

But we are not without risk. First, surging stocks usually give a chunk back. While it is not 100% a guarantee, history suggests there will be corrective moves. That is more of a short-term risk for traders to be aware of. For investors, we do expect ongoing growth. The second risk is that this is a Chinese company. While they are operating in new and diverse geographies, Chinese stocks have been tough. However, GigaCloud’s customers are outside of China. A meaningful improvement in China and that market could really send a further boost to the stock. A third risk to be aware of is the exposure to shipping and freight costs. A lot of the margin expansion has stemmed from a correction/reduction in ocean shipping rates. We saw some interesting trading patterns with the Red Sea and Houthi attacks. But longer-term a significant rise in oil prices, and of course shipping fuel, is a risk that is largely to be ongoing. Other disruptions to shipping routes are also a risk to be cognizant of. Finally, as we move forward, it is likely unreasonable to expect that the massive growth on a percentage basis year-to-year can continue. This does not mean that the stock is going to crater, but investors need to be aware that explosive growth is likely to moderate.

As we look ahead to 2024, we are expecting another year of growth on tap. Management guided total revenues to be between $230 million and $240 million in the first quarter of 2024. This comes even with a warehouse fire in Japan. To be clear, this is a near doubling of revenue expected year over year. Cash flows have been ramping up, and the company continues its push forward in expansion efforts. Finally, there are repurchases which are further boosting shareholder value. Based on the present growth patterns, and assuming 2024 comes with a 33% increase in revenues, which may be conservative, and margins that remain in the high 20% range, EPS could hit $2.50 this year. That implies a stock at just 17X FWD. Folks, this is still pretty cheap. We continue to see upside and rate shares a buy.

Q2 2024 Earnings Call Transcript")