metamorworks

First, for the uninitiated, GigaCloud Technology (NASDAQ:GCT) is not a public cloud provider but rather operates an online marketplace that connects manufacturers from Asia to buyers who are typically resellers from all over the world. It specializes in consumer items like furniture and other large parcel merchandise or typically goods shipped aboard container ships.

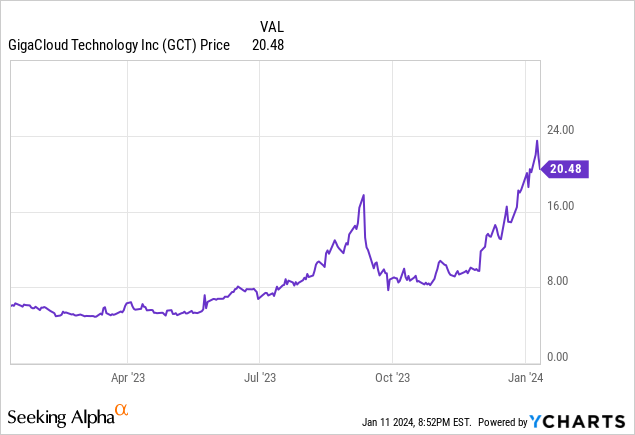

The stock has surged by over 200% as charted below during the last year and was trading around $20.44 at the time of writing, after reaching a peak of $23.5, which may be tempting for dip buyers especially since the stock is rated as a buy by Quant because of its superior profitability and valuation metrics. However, based mainly on the possibility of Red Sea-related risks eating into its profitability, the objective of this thesis is to show that it is better to wait.

I start by highlighting how GCT makes money.

Driven by the Supplier-Fulfilled Retailing Business Model and AI

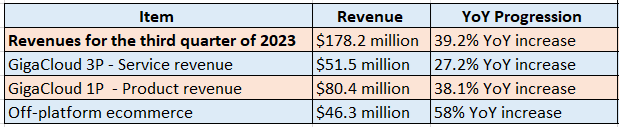

As tabled below, the business is segmented into three primary areas, with the first two being platform-based, namely GigaCloud 3P which generates services revenue, and GigaCloud 1P for product sales. Third, there is off-platform eCommerce. Now, all three segments made progress during the third quarter of 2023 (FQ3-2023), resulting in an overall revenue growth of 39.20%.

Table built using data from (seekingalpha.com)

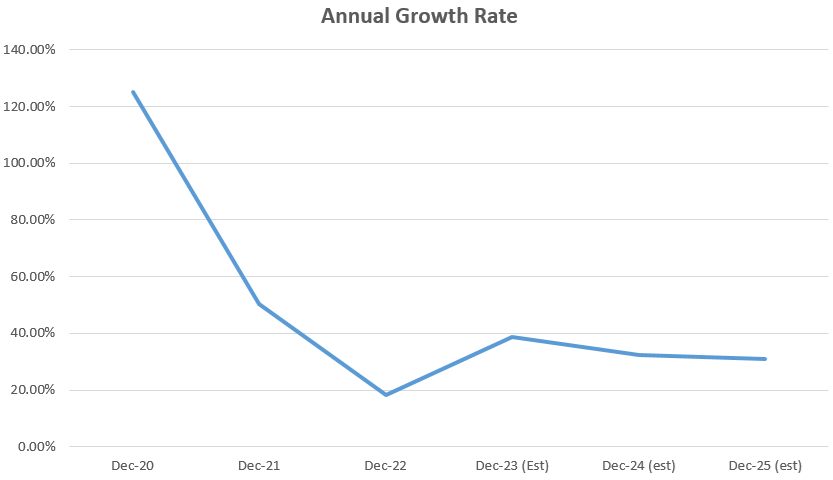

To put things into perspective, the following chart highlights the double-digit annual growth rate, which picked up rapidly after the COVID-19 slump of 2021-2022. Noteworthily, lockdowns to restrict the propagation of the disease lasted longer in China from where it sources most of its products.

Chart built using data from (www.seekingalpha.com)

Talking figures, from $490 million in fiscal 2022, revenues are expected to exceed the $1 billion mark in FY-2025 showing the attractiveness of GCT’s supplier-fulfilled retailing business model whereby after receiving orders for a particular product, the company takes care of sourcing the items from suppliers and delivering them to customers.

In this respect, its platform effectively links resellers of furniture and home appliances in developed countries directly with Chinese manufacturers. This direct connection augmented by warehousing services located near ports optimizes the supply chain, eliminating intermediaries and resulting in lower transit times and prices for consumers. At the same time, GCT provides logistical support including transportation for the buyers which ensures a smooth delivery process, enabling it to compete with United Parcel Service (UPS) and FedEx (FDX).

Looking deeper, with its AI algorithms to aggregate orders, determine the shortest route based on clients’ history, and optimize container usage, it has been able to make purchases more affordable for its customers. In this way, GCT has been able to rapidly make a name for itself in the large merchandise industry with the GigaCloud marketplace boasting a GMV (Gross Merchandise Value) of $684.8 million as of FQ3-2023, which represents an astounding 41% YoY increase. For this matter, the U.S.A. where it has partnerships both with Walmart (WMT) and Amazon (AMZN) was its largest market as of the end of 2022.

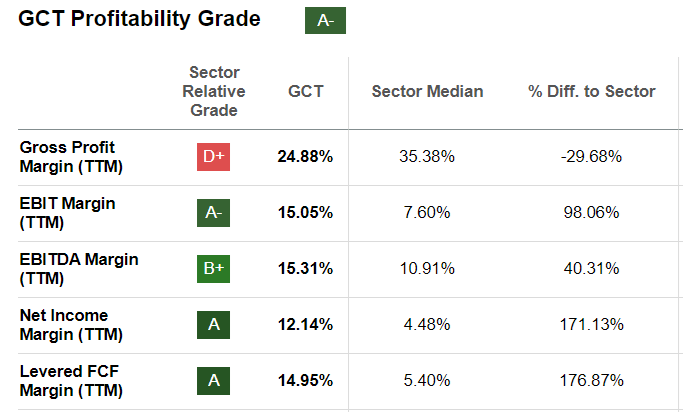

Moreover, with $214 million of cash and only $164.5 million of debt, the balance sheet remains healthy, with the GCT boasting a growth grade of A- and has the ingredients to power on with its growth as detailed earlier. On the other hand, there are risks as to its profitability grade of A- due to rising geopolitical tensions in the Middle East.

Profitability Grade (seekingalpha.com)

The Risks Emanating from the Red Sea

In this case, FQ3-2023’s gross profit margins of 27.4% represented a substantial increase of 55.68% YoY, but these were mostly due to a normalization of shipping rates. This, in turn, reduced the cost of revenues which is an important element to consider for a company that is heavily dependent on the international transportation of goods.

Now, the opposite may happen or gross margins may dwindle following the disturbances in the Red Sea where Houthi militias have been attacking cargo vessels prompting major shipping operators like Maersk to suspend shipping in that region after an attack on its Hangzhou container ship. As a result of these attacks, ocean-based shipping rates have surged by over 50% in some key lanes according to Supply Chain Dive, with one of these including the Asia to U.S. East Coast route.

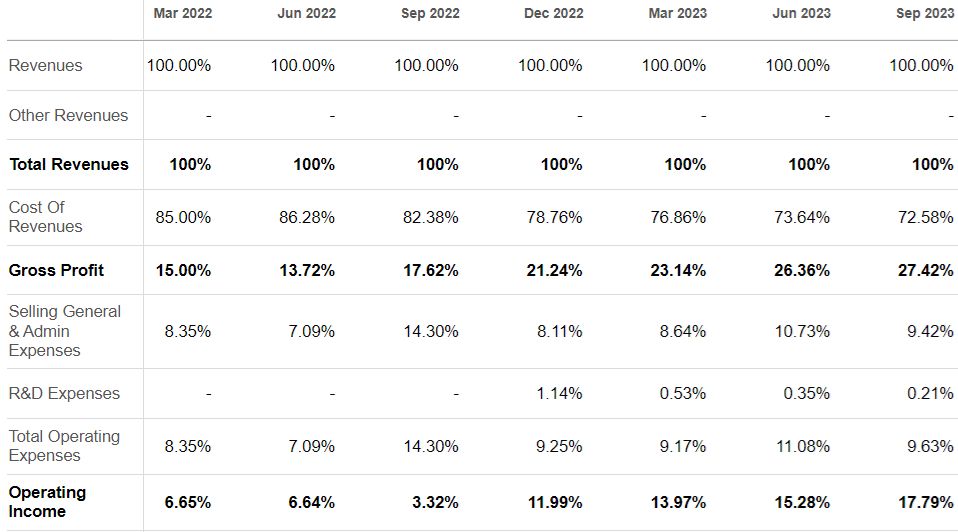

Well, we are certainly not in the same situation as during the pandemic when entire cities and ports were under lockdown but rates may spike in the short to medium term. Now such a spike can be detrimental to GCT’s profitability as was the case in 2022 when the cost of revenues as a percentage of total sales escalated to 85% and 86.3% in the first two quarters as shown below.

Income Statement – Quarterly basis (seekingalpha.com)

At that time, shipping costs reached an all-time high causing gross profit and operating income margins to dip to below 14% and 7% respectively. They have since recovered to above 27% and 17% respectively, but there are other expenses to contend with.

In this respect, the last reported quarter saw sales and marketing expenses jumping by 61.8% on a YoY basis. Now, thinking aloud, such a surge means that more staff hours are being dedicated to driving sales possibly due to GCT facing competition from other B2B marketplaces, namely Alibaba Cloud (BABA). It could also be due to spending more time as a middleman dealing with Chinese suppliers and customers looking for discounts in a slowing U.S. economy where inflation remains above 3%, not particularly conducive to sustained consumer spending. At the same time, another of GCT’s key markets Europe is on the brink of recession.

Additionally, more expenses were incurred for the GigaCloud platforms to support the rise in the number of transactions and more fees were paid to third-party eCommerce Websites. Even then, operating expenses decreased by 6% year-over-year, but this was mostly on the back of drastically lower share-based compensation.

Estimating the Potential Impact on Earnings and How Valuation May Suffer

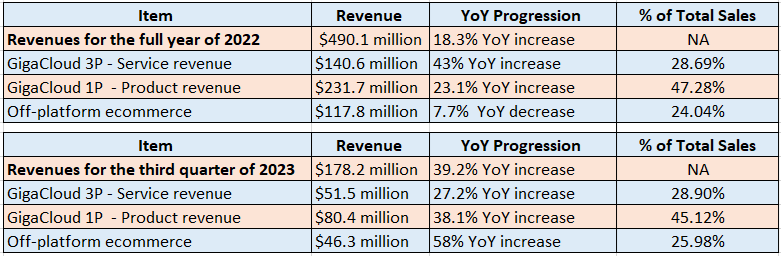

To get an estimate of the impact of higher shipping costs on profits, I consider that in addition to linking customers through the GigaCloud 3P platform, the company also obtains product revenue as shown in the tables below. Thus, as per my calculation, 47% and 45% of product revenues were derived from the GigaCloud 1P online platform in FY-2022 and FQ3-2023 respectively as shown below.

Table built using data from (www.seekingalpha.com)

Therefore, in a scenario where shipping rates are hiked, and it is unable to pass on additional costs to its customers for fear of losing market share, GCT could suffer from a reduction in profits. Estimating the potential impact on FY-2024’s earnings due to higher shipping rates, I assume it to be 45% based on the product constituent of sales for FQ3-2023. By the way, this figure is more than five times lower than the 227% EPS growth expectation for FY-2023 over 2022 (see table below), which is in large part based on a normalization of shipping which means that a 45% decline due to Red Sea-related disturbance elongating routes is a reasonable estimate.

Thus, applying a 45% reduction, the EPS will decrease from $2.07 to $1.14 (2.07 x 0.55). Conversely, the forward P/E will increase to around 15.2x (10.48 x 1.45) instead of the 10.48x expected. As a result, the stock will lose its current discount of 35% relative to the sector, putting it in overvaluation territory.

Earnings estimates (www.seekingalpha.com)

GCT is a Hold in View of Risks and a Management update is needed

Therefore, based on the estimated P/E of 15.2x, its stock price, which stood at $20.44 at the time of writing, could fall by 45% to $11.42, meaning that GCT is more of a hold. In this respect, the stock should be subject to a higher degree of volatility in case there is an escalation of the Red Sea attacks.

On the other hand, my pessimistic outlook could be put in jeopardy if GCT can rapidly trace a less costly route going from Asia to the U.S. East Coast or makes use of its AI algorithms to aggregate client orders in such a way to offset higher costs associated with shipping goods to Europe through the Cape of Good Hope in South Africa. Along the same lines, downside risks could be limited in case the company absorbs some of the higher costs internally as exemplified by the drastic cut in stock-based compensation, or from $8.9 million in the third quarter of 2022 compared to only $317,000.

Still, in the name of diversification in the context of tensions between the U.S. and China, there could be more tariffs imposed on Chinese goods after the November presidential elections. In this respect, with a mostly “Made in China” approach, GCT appears to be too dependent on the country’s manufacturing prowess. Now, I think that the management understands the need for more geographical diversity within the supply chain as the FY-2022 SEC filings mention sourcing products from Vietnam and throughout Asia plus the opening of an office in Malaysia. India is also now a new sourcing origin as part of the acquisition of Noble House in November last year. These are risk mitigation moves, but I believe that more is needed, for example, providing an update as to the percentage of merchandise to be procured from sources other than China especially given that GCT is on its way to becoming a $1 billion revenue-generating company.

Finally, given the risks related to the Red Sea, it is better to avoid buying the dip and wait for the management comments during the upcoming quarter’s earnings around March 15. Specific items to look for are details related to shipping rates and supplier diversification.

Q2 2024 Earnings Call Transcript")