PonyWang

The PGIM Global High Yield Fund (NYSE:GHY) is a closed-end fund that income-focused investors can purchase as a method of achieving their goal of earning spendable income from the assets in their portfolio. This is a desire of many retirees and others who are living off of their savings as opposed to primarily earning money from a regular job. It is also a common desire of many other individuals trying to maintain their standard of living in today’s inflationary environment, as the cost of just about everything that we purchase today has been rising more rapidly than incomes (despite what the consumer price index says). This is particularly the case for food and other necessities. The PGIM Global High Yield Fund does this job reasonably well, as its 11.22% yield compares pretty well to just about any other fund in the market today. It certainly compares well to its peers, as we can see here:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

PGIM Global High Yield Fund |

Fixed Income-Taxable-High Yield |

11.22% |

|

AllianceBernstein Global High Income Fund (AWF) |

Fixed Income-Taxable-High Yield |

7.84% |

|

Allspring Income Opportunities Fund (EAD) |

Fixed Income-Taxable-High Yield |

9.79% |

|

Barings Global Short Duration High Yield Fund (BGH) |

Fixed Income-Taxable-High Yield |

9.04% |

|

RiverNorth Capital and Income Fund (RSF) |

Fixed Income-Taxable-High Yield |

11.15% |

|

Western Asset High Income Opportunity Fund (HIO) |

Fixed Income-Taxable-High Yield |

11.33% |

As we can clearly see, the PGIM Global High Yield Fund is one of the highest-yielding funds on this list. It is not the absolute highest in terms of yield, but it is very close. This is something that could prove very attractive to those investors who are seeking to maximize the income that they earn from the assets in their portfolios. However, it is important to keep in mind that there are times when a high yield suggests concern from the market about the fund’s ability to pay its distribution. However, the fact that the PGIM Global High Yield Fund’s yield is not ridiculously out of line with its peers suggests that this is probably not the case today. However, it is still something that we want to investigate as we do want to ensure that the fund can afford the distribution that it is paying out. We will discuss this in more detail later in this article.

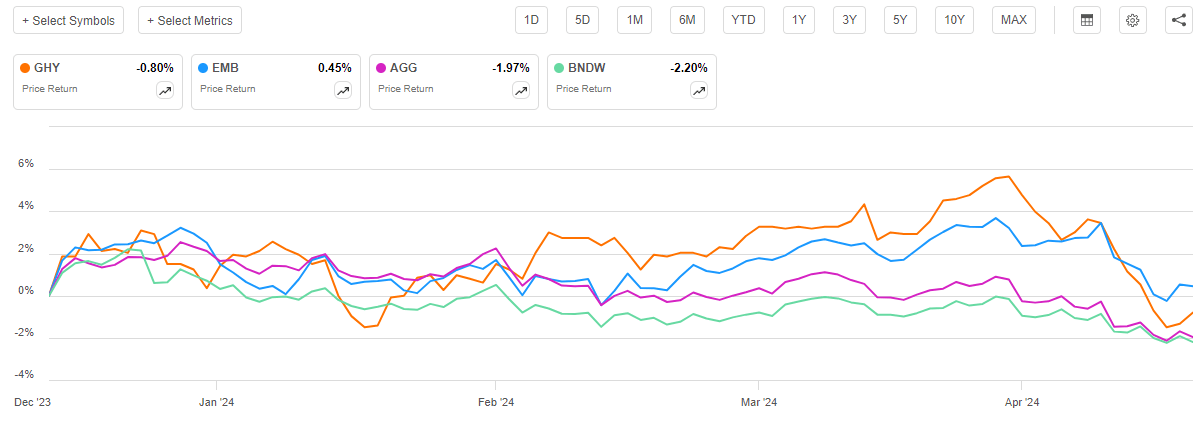

As regular readers can likely remember, we previously discussed the PGIM Global High Yield Fund in mid-December 2023. The bond market since that time has been somewhat weak, although it was fairly strong for about two weeks following the release of that article. For most of December, various market participants were expecting that the Federal Reserve would rapidly reduce interest rates over the course of 2024. As such, these market participants were aggressively buying up bonds and other income-producing securities in order to front-run the Federal Reserve and lock in reasonably attractive yields over the long term. However, recent economic and inflation data continue to disappoint those investors who expect rate cuts as inflation is getting worse and the economy remains strong. In short, with each passing month, it becomes harder and harder for the central bank to justify a reduction in the federal funds rate. As such, the bond market has been selling off year-to-date to reflect the reality that the market was overly optimistic at the start of the year. This is exactly the scenario that regular readers expected, as I have been stating for some time now that rate cuts are not justified. As such, we can probably expect that the share price performance of the PGIM Global High Yield Fund has not been especially good since the date of the previous article’s publication. This is the case, as shares of the fund are down 0.80% since December 12, 2023 (the date of the prior article’s publication):

Seeking Alpha

As we can see, the fund’s shares have outperformed both the Bloomberg U.S. Aggregate Bond Index (AGG) and the Vanguard World Bond ETF (BNDW) over the period. However, the fund has underperformed emerging market bonds (EMB), which have actually risen in price. Emerging market bonds are something of a different animal than developed market or domestic bonds, however, as they actually benefit from a declining dollar. As we have seen in the price of gold, investors around the world are beginning to doubt that the Federal Reserve will be able to get inflation under control and have been trying to move away from a declining dollar. The PGIM Global High Yield Fund holds both domestic, foreign developed, and emerging market bonds so we could expect that its performance would somewhat reflect both trends. This is indeed the case as its price performance has been between emerging market and developed market bonds.

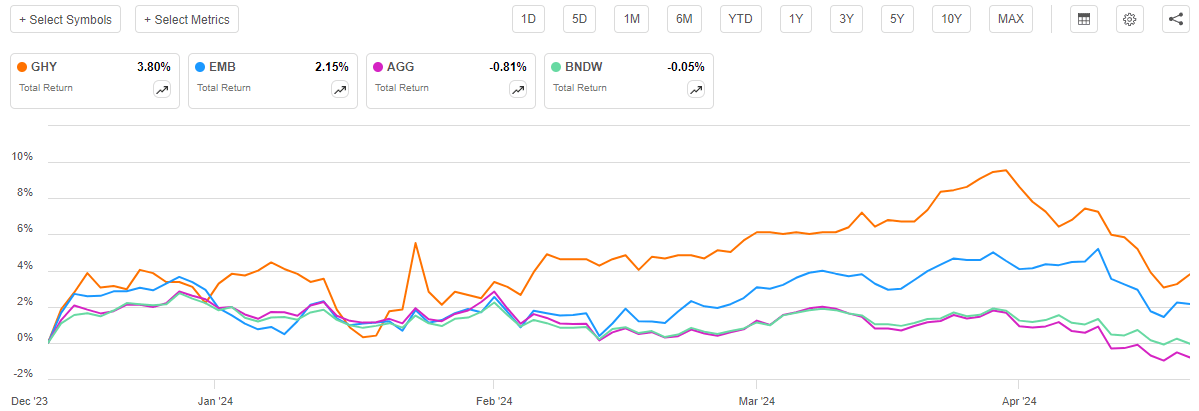

A simple look at the price performance of the PGIM Global High Yield Fund does not tell us the whole story, however. As I have pointed out numerous times in the past, a closed-end fund such as this one typically pays out most or all of its investment profits to the shareholders via distributions. The basic business model is to keep the size of the portfolio relatively stable over time while giving the shareholders all of the profits that are derived from that portfolio. As such, the distribution will account for a significant percentage of the return provided by the fund, and it is not visible in share price movements. As such, we should include the distributions paid by the fund in any discussion of its performance. When we do that, we see that investors in the PGIM Global High Yield Fund benefited from a 3.80% gain since the date that my previous article on the fund was published:

Seeking Alpha

This is better than any of the three indices delivered over the same period, including the emerging market bond index. Emerging market bonds almost always have significantly higher yields than developed market bonds, but even they only managed to deliver a 2.15% total return over the roughly four-month period. This should improve the attractiveness of this fund further and, at least on the surface, suggests that it could be a good option for investors who are seeking global diversification and a possible hedge against U.S. dollar devaluation.

However, we do need to have a closer look at the fund to determine how well it is actually doing and how well it is likely to do in the future. After all, past performance is no guarantee of future results, and investors who purchase the fund today are not affected by past results. The fund released its semi-annual report a few weeks ago, so that should aid in our analysis. Let us proceed onward and see if purchasing this fund today makes any real sense for income-seeking investors.

About The Fund

According to the fund’s website, the PGIM Global High Yield Fund has the primary objective of providing its investors with a very high level of current income. Unlike many other funds from other sponsors, the fund’s website does not provide any real insight into how the fund expects to achieve this objective. Rather, all it states is:

The Fund seeks to provide a high level of current income by investing primarily in below investment-grade fixed income instruments of issuers located around the world, including emerging markets.

This is not as in-depth as the strategy descriptions that we get from the websites of some other closed-end funds. However, it does still tell us what we really need to know about the fund’s strategies to achieve its goals. In short, the fund invests its assets in high-yield securities issued by entities anywhere on the planet. Basically, this is a junk bond fund that does not have the country constraints of an American-specific bond fund. As such, the fund’s objective of providing its investors with a very high level of current income seems appropriate. As I pointed out in my previous article on this fund:

Bonds by their very nature are income vehicles. Investors purchase bonds at face value, which they receive back when the bond matures. As such, there are no net capital gains over a bond’s lifetime. After all, a bond has no inherent link to the growth and prosperity of the issuing company or government.

As such, any pure bond fund is going to have current income as its primary objective. This is because bonds do not produce any net capital gains over their lifetimes. However, as we have seen in various past articles, a number of bond funds are not pure bond funds as their assets may include other types of fixed-income securities or even common stocks. This one is no exception to this as the semi-annual report provides the following asset allocation:

|

Asset Type |

Percentage of Total Portfolio |

|

Asset-Backed Securities |

4.0% |

|

Convertible Bonds |

0.0% |

|

Corporate Bonds |

94.9% |

|

Floating Rate and Other Loans |

4.5% |

|

Sovereign Bonds |

20.5% |

|

Common Stocks |

2.1% |

|

Preferred Stock |

0.1% |

|

Money Market Fund |

0.2% |

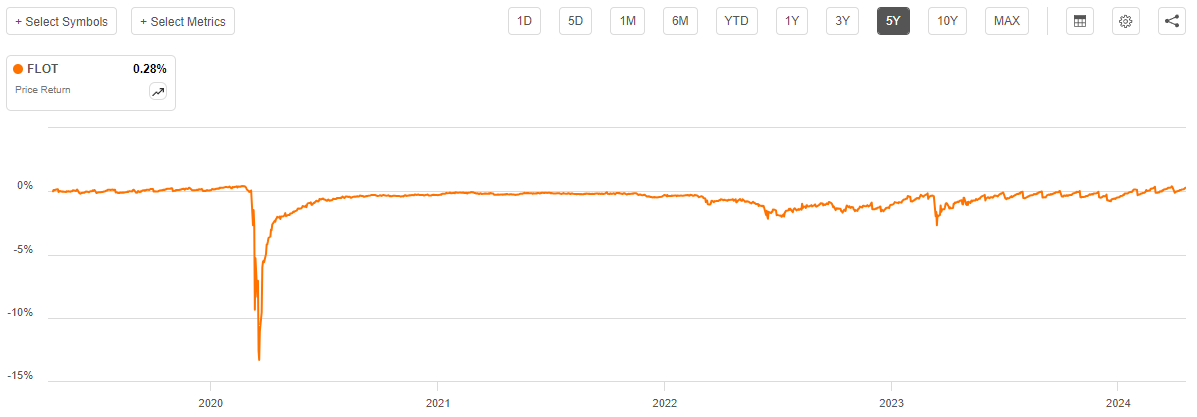

The 0.0% allocation to convertible bonds does not mean that there are none of these securities present in the fund’s portfolio. The fund has a small convertible bond position in Sunac China Holdings, but this position represents such a small percentage of the fund’s total portfolio that it rounds off to a 0.0% weighting. The big thing that we see here is that the PGIM Global High Yield Fund has allocations to both common stocks and floating-rate bonds that will exhibit vastly different performance in the market than ordinary bonds. Floating-rate securities, for example, do not experience the price movements that bonds do when interest rates change. We can very quickly see this by looking at the five-year price chart of the iShares Floating Rate Bond ETF (FLOT):

Seeking Alpha

As we can see, with the notable exception of the panic at the start of the COVID-19 pandemic, the fund has been remarkably stable despite the fact that interest rates changed quite a lot over the period in question. In fact, the slight variations that we see the fund exhibit in recent times is due to timing differences between the fund’s receipt of payments from the securities that it holds and the date that it pays its distributions. In short, these securities will not change much when interest rates change so their presence in the portfolio of the PGIM Global High Yield Fund will add a degree of stability to the fund’s portfolio. Of course, the weighting that the fund has to these securities is so low that the impact of their presence will not be readily apparent. They might still make the fund slightly less volatile in terms of price than it would otherwise be, though.

The fact that this fund has a small allocation to common stocks could also change its performance profile slightly from one that is entirely invested in bonds. After all, common stocks are affected by things such as economic growth rates, government policies, consumer demand, and numerous factors that are unique to the issuing company. Here are all of the common stocks in this fund’s portfolio:

|

Company |

Country |

|

Digicel International Finance (DCEL) |

Jamaica |

|

Intelsat Emergence SA (INTEQ) |

Luxembourg |

|

CEC Entertainment |

United States |

|

Chesapeake Energy Corp. (CHK) |

United States |

|

Cornerstone Chemical Co. |

United States |

|

Ferrellgas Partners (OTCPK:FGPR) |

United States |

|

GenOn Energy Holdings |

United States |

|

Heritage Power LLC |

United States |

|

TPC Group |

United States |

|

Venator Materials PLC (OTCPK:VNTRD) |

United States |

Many of these are companies that I would not touch right now, as firms such as Ferrellgas Partners have been struggling for years. Fortunately, they only account for very small positions in the fund and individually they will not have any noticeable impact on the fund as a whole. However, we can still see that the fund is not solely a bond fund as the floating-rate securities and the common stocks account for 6.6% of its assets in aggregate. That 6.6% weighting is enough to cause the fund’s performance to be slightly different from a pure bond fund.

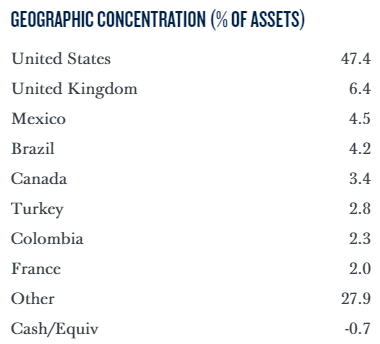

In my last article on this fund, I pointed out that the PGIM Global High Yield Fund is less weighted towards the United States than many other global bond funds. This is partly due to the 20.5% allocation to sovereign bonds, as there are no junk-rated sovereign bonds issued within the United States. This chart breaks down the fund’s portfolio by country as a percentage of assets:

PGIM

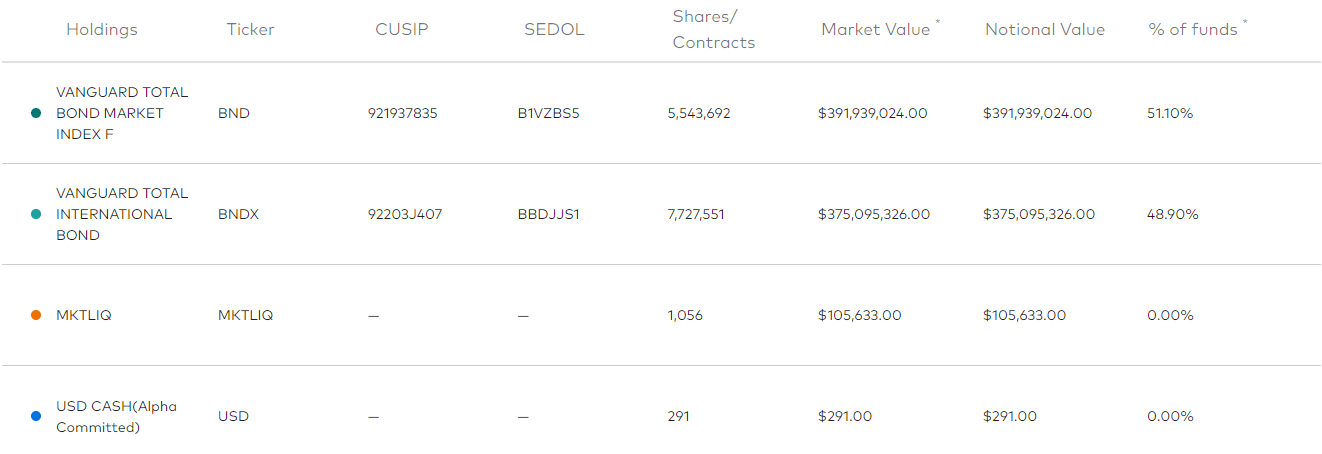

The United States is the most heavily weighted individual country in the fund’s portfolio, which is not surprising. The nation has the largest national economy in the world on a nominal basis (but not on a purchasing power basis) and is by far the largest issuer of debt in the world. The Vanguard World Bond ETF currently has a 51.10% weighting to the United States:

Vanguard

I will confess that I am unsure of how well this actually reflects the global bond market as I cannot find any information about the exact size of any given nation’s bond market. However, this is as good as information that we have to go on, and if we assume that this is correct then American issuers issue just over half of all of the bonds that are traded in the global market.

We can therefore see that the PGIM Global High Yield Fund appears to be underweight to the United States. This was the same situation that we saw the last time that we discussed the fund. In fact, its weighting to the United States has declined somewhat over the past four months since we last discussed it. In the previous article, I mentioned that the fund had a 48.4% weighting to this country. This weighting reduction is something that might appeal to some investors today. As I have noted in various previous articles, one of the biggest problems that the average American investor has is that their portfolios tend to have outsized exposure to the United States. This is understandable as the American equity markets have outperformed just about any foreign market over the past fifteen years. In the case of bonds, it is difficult to even get most foreign bonds in the United States as most brokers do not carry them. Anecdotally, the last time that I called the bond trading desk at a major U.S. broker and inquired about purchasing foreign sovereign bonds, I was told that the minimum purchase was a number that is out of reach for most retail investors. As such, the only realistic way that Americans can get exposure to these assets is by purchasing an international bond fund, and those do not get much coverage in the American media. Thus, almost by default, most American investors have very limited or even no exposure to these assets.

The fact is, though, that American investors might be well served by investing in foreign bonds today. One reason for this is that the financial situation of many other nations, particularly emerging nations, is much better than that of the United States. For example, consider the debt-to-GDP ratio of the largest nations whose securities are held by the PGIM Global High Yield Fund:

|

Nation |

Debt-to-GDP |

|

United States |

129% |

|

United Kingdom |

97.1% |

|

Mexico |

49.6% |

|

Brazil |

72.87% |

|

Canada |

107% |

|

Turkey |

31.7% |

|

Columbia |

63.6% |

|

France |

112% |

(All figures are provided by World Population Review using data from the United Nations).

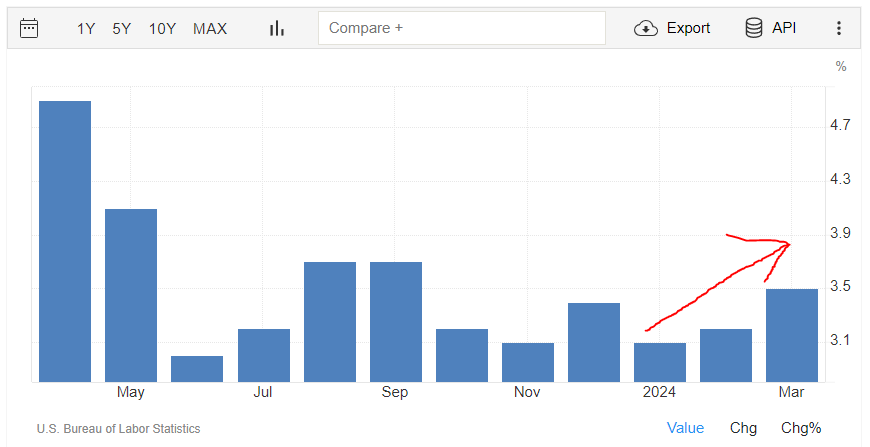

There are a few sources that provide different figures for some of these nations as there are a few ways to calculate the debt-to-GDP ratio. However, all of these sources agree that the United States has a higher debt-to-GDP ratio than most of the other nations of the world and that it is increasing fairly rapidly. The Committee for a Responsible Budget projects that the 2025 budget request that President Biden submitted last month would result in a cumulative deficit of $17.7 trillion over the next ten years. Historically, estimates like this tend to be lower than what actually occurs but regardless we can see that the fiscal situation in the United States will not improve anytime soon. Meanwhile, we have a situation in which the Federal Reserve seems to be committed to interest rate cuts despite the headline inflation rate going up every single month this year:

Trading Economics

On top of that, foreign commodity exporters and manufacturing nations that have historically funded the deficits of the United States such as Russia, China, and Saudi Arabia are becoming increasingly reluctant to do so. This is one reason why we are seeing foreign central banks reducing their holdings of U.S. dollars in favor of gold or other currencies (such as the Chinese renminbi). I have pointed this out in a few articles going back over the past few decades. If the Federal Reserve were to actually cut interest rates while inflation is worsening, it would weaken the dollar versus other currencies and could accelerate this process.

This is a net negative for American bonds in general as the purchasing power of the coupons paid by these bonds will decline over time. Meanwhile, a declining dollar actually increases the value of bonds that pay their coupons in other currencies, as viewed from the perspective of an American investor. After all, the foreign currency that is received from these bonds converts into more dollars when the investor conducts the currency exchange. This is one of the reasons why emerging market bonds tend to outperform American ones when the U.S. dollar is declining.

The PGIM Global High Yield Fund appears to be positioned to take advantage of the declining dollar by virtue of its underweight position in American bonds relative to the index. The fact that the fund’s weighting to the United States has been decreasing could even suggest that its management is trying to take advantage of this situation. Overall, this is something that investors should appreciate, and it could be worthwhile to have a fund such as the PGIM Global High Yield Fund in your portfolio as a hedge against a declining dollar.

Leverage

As is the case with most closed-end funds, the PGIM Global High Yield Fund employs leverage as a method of boosting the effective yield that it receives from the securities in its portfolio. I explained how this works in my previous article on this fund:

Basically, the fund borrows money and then uses that borrowed money to purchase high-yield bonds and similar income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I usually would like a fund’s leverage to be under a third as a percentage of its assets for this reason.

As of the time of writing, the PGIM Global High Yield Fund has leveraged assets comprising 21.52% of its assets. This is pretty reasonable when compared to many of the fund’s peers, as we can see here:

|

Fund Name |

Leverage Ratio |

|

PGIM Global High Yield Fund |

21.52% |

|

AllianceBernstein Global High Income Fund |

18.05% |

|

Allspring Income Opportunities Fund |

30.30% |

|

Barings Global Short Duration High Yield Fund |

25.81% |

|

RiverNorth Capital and Income Fund |

46.20% |

|

Western Asset High Income Opportunity Fund |

0.00% |

(all figures from CEF Data)

As we can clearly see, the PGIM Global High Yield Fund generally compares reasonably well with its peers with respect to leverage. It is not the least leveraged fund of the group by any means, but most of the other funds here have a leverage ratio that compares fairly well with it. This suggests that the fund is currently employing a reasonable and appropriate balance between the risks and potential rewards from the use of leverage. We should not need to worry too much about the fund’s outstanding debt today.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the PGIM Global High Yield Fund is to provide its investors with a very high level of current income. In pursuit of this objective, the fund primarily invests its assets into a portfolio consisting of corporate and sovereign high-yield bonds issued by entities that are based all over the world. The fund does have a few assets that fall into other categories, but for the most part, the assets that are held by this fund will deliver the majority of their investment returns in the form of direct payments to their owners. In this case, that owner is the fund, and the fund collects the coupon payments on behalf of its investors. This fund then takes things a step further and borrows money that it uses to purchase more bonds, allowing it to receive payments from more securities than it could control solely through reliance on its own equity capital. The fund combines all of the money that it receives from these coupon payments with any gains that it manages to obtain through the sale of bonds that have gone up in price. Finally, the fund pays out all of the money that it receives from these various activities to its shareholders, net of its own expenses. As interest rates today are close to the highest levels that we have seen in a generation, we can expect that this process would allow the fund’s shares to boast a respectable yield.

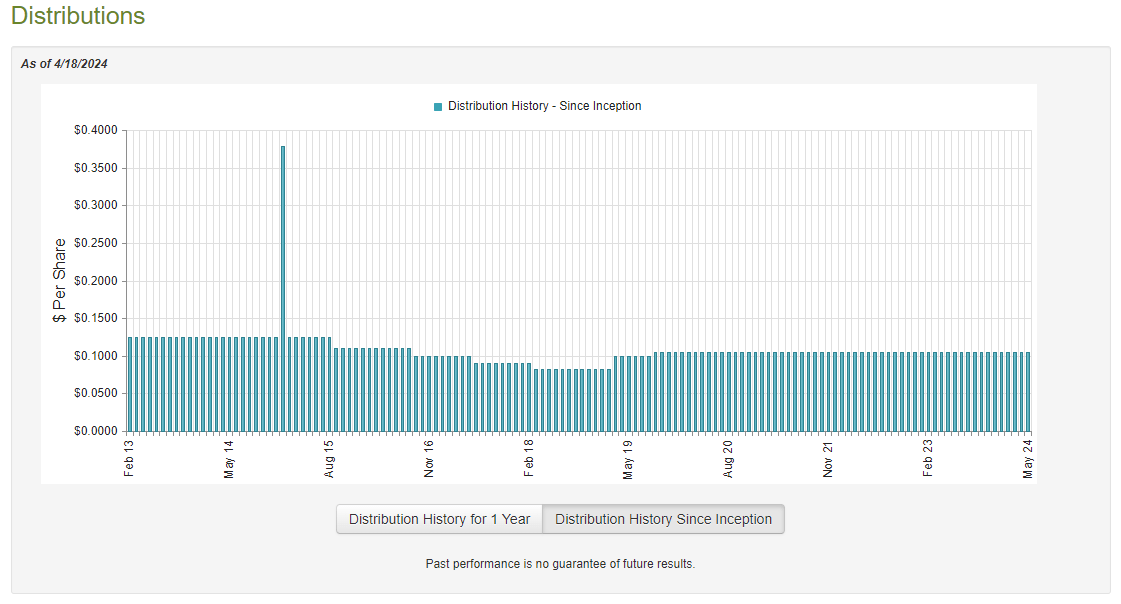

This is certainly the case as the PGIM Global High Yield Fund currently pays a monthly distribution of $0.1050 per share ($1.26 per share annually), which gives the fund an 11.22% yield at the current share price. As we saw in the introduction, this is a very respectable yield that compares quite well to the fund’s peers. This fund has been fairly consistent with respect to its distribution over the years, but it has certainly not been perfect as we can see here:

CEFConnect

As clearly shown, the fund both raised and lowered its distribution a few times over its history. The majority of these changes came in the latter half of the previous decade as this fund has been remarkably consistent in the 2020s. Indeed, we could almost say that it has been too consistent as most other funds were forced to reduce their distributions following the Federal Reserve’s aggressive interest rate hikes in 2022 and early 2023. These interest rate hikes caused the price of American bonds to fall and thus caused most closed-end funds that were invested in them to suffer both realized and unrealized losses. This fund does not invest entirely in American bonds, but it still almost certainly took some losses as most central banks around the world also increased their interest rates following the pandemic. In addition, roughly half of the bonds that are held by this fund are American so are still affected by the policies of the Federal Reserve. As such, it is curious that this fund was able to maintain its distribution during a period in which most other funds could not. This is something that we should investigate further.

Fortunately, we have a very recent document that we can consult for the purposes of our analysis. As of the time of writing, the most recent financial report for the PGIM Global High Yield Fund is the semi-annual report that corresponds to the six-month period that ended on January 31, 2024. A link to this report was provided earlier in this article. This is a much newer report than the one that was available to us at the time of our previous discussion so we can expect it to have more up-to-date information. In particular, this report should give us a good idea of how well this fund handled the two disparate market environments that existed in the second half of 2023. The first of these environments was present during the summer and early autumn months of that year, and it was characterized by generally falling asset prices and rising bond yields. This was due to market participants beginning to realize that the fight against inflation was a long way from being won, and so they were adjusting their portfolios and asset prices for an environment in which high interest rates would be a mainstay of the financial system for quite some time. This market environment may have resulted in the PGIM Global High Yield Fund taking some realized or unrealized losses. It could have offset these losses by gains during the last two months of 2023 though, as investors experienced a euphoria and bid up asset prices in the expectation that the Federal Reserve and other central banks would rapidly reduce interest rates over the course of 2024. This financial report should give us a good idea of how well this fund handled these two differing market environments.

For the six-month period that ended on January 31, 2024, the PGIM Global High Yield Fund received $19,811,125 in interest and $510,524 in dividends from the assets in its portfolio. This gave the fund a total investment income of $20,321,649 for the period. It paid its expenses out of this amount, which left it with $13,858,713 available for shareholders. That was, unfortunately, nowhere near enough to cover the distributions that the fund paid out over the period. For the six-month period, the PGIM Global High Yield Fund distributed a total of $20,951,736 to its shareholders. At first glance, this could be quite concerning as we would ordinarily prefer that a fixed-income fund fully cover its distributions solely out of net investment income. This one obviously failed to accomplish that task.

However, there are other methods that a fund can employ to obtain the money that it needs to cover its distributions. For example, it might have been able to earn some money by selling bonds that went up in price due to falling interest rates. These are realized capital gains and realized capital gains are not considered to be investment income for tax or accounting purposes. However, they do represent money coming into a fund that could be paid out to the investors.

Fortunately, the fund did have some success at obtaining money via these alternative sources during the period. For the six-month period that ended on January 31, 2024, the PGIM Global High Yield Fund reported net realized losses of $15,734,609 but these were more than offset by $26,498,320 net unrealized gains. Overall, the fund’s net assets increased by $3,670,688 after accounting for all inflows and outflows during the period.

As the fund’s net asset value increased over the period, it did technically manage to cover its distributions. However, it was only able to accomplish this because of the large unrealized gains that it achieved in the period. As everyone reading this is no doubt well aware, unrealized gains can be erased by any market correction or similar event. Therefore, we will want to keep an eye on the fund’s net asset value in order to ensure that it does not begin declining too much. I will admit that I am a little more confident that this fund’s net assets will hold up than I am many others because of its substantial foreign holdings. However, we should not get complacent at any time and should ensure that all of the assets in our portfolio are maintaining the performance that we expect.

Valuation

As of April 18, 2024 (the most recent date for which data is currently available), the PGIM Global High Yield Fund has a net asset value of $12.72 but the shares only trade at $11.26 each. This gives the fund’s shares an 11.48% discount on net asset value at the current price. This is a very large discount that is quite a bit larger than the 8.35% discount that the shares have averaged over the past month. As such, the current entry price appears to be a very reasonable price at which to add this fund to your portfolio if you wish to own it.

Conclusion

In conclusion, the PGIM Global High Yield Fund is a closed-end fund that invests in speculative-grade securities issued by entities that are located all over the world. This is an attractive proposition right now considering the threats that the U.S. dollar is facing due to the strained financial situation of the American government and the desire for diversification that has been expressed by some foreign central banks. This fund is one of the few ways to obtain exposure to foreign bonds without having a significant asset base and its yield is higher than index funds or exchange-traded funds. The fact that it trades at a discount is another benefit.

Overall, this fund will probably prove to be a winner over the long term but of course, it could suffer some short-term weakness if today’s interest-rate environment causes an economic shock.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")