Sezeryadigar

Co-authored by Treading Softly.

There is a belief that is pervasive within the entire Western mindset: “Everything happens for a reason.” Even the unreligious will often exclaim when something bad happens; there is a reason behind it that a greater force, whether it be Karma or a deity or just some law of thermodynamics, will cause an event to occur, potentially for their benefit. While I understand the mindset, I disagree when it comes to the market. Many believe the market is efficient. There are many ways to produce efficiencies within a closed system, but there are still impacts from external forces.

There’s another popular saying that says that “theories are great in theory, but they rarely work in reality” – part of this is because of the human condition. People are naturally inclined to be selfish, greedy, and lazy. Looking for the easiest way to get rich without doing any work. When you add humanity into the mixture of many theories, they just destroy the entire working premise because humanity has a way of mucking things up.

Looking at income investing, When a company is heavily oversold because of human emotion or lack of understanding, even though the company itself is financially sound or stable, I refer to these incidents as causing “accidental high yielders.” These are companies whose yields are exceptionally high compared to normal, simply because of a singular event that people misunderstood or blew out of proportion.

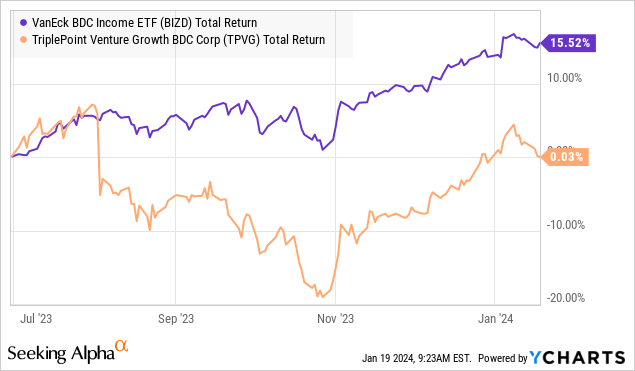

Today, I want to look at one specific business development company, or BDC, that saw a massive overselling in the middle of last year, causing it to underperform the overall BDC sector. This is a time frame when so many other BDCs are enjoying a Goldilocks period where they have low fixed costs and high interest rates, which means that their earnings are elevated. Why would I be looking at this extra high-yielding BDC? Because I see it as an accidental high yielder, which means I can earn both strong income and capital gains when it recovers.

Let’s dive in!

Beaten Down, But Strong Outlook

TriplePoint Venture Growth (NYSE:TPVG), yielding 14.6%, is a BDC that specializes in companies that are funded by venture capital. TPVG will step in and provide a debt investment when a company is being prepared for an IPO. Getting a debt investment allows the venture capitalists who bought in early to avoid diluting their equity at a point where they are expecting to finally realize their gains.

TPVG will provide debt and accept a smaller amount of equity, often in the form of warrants. This allows the borrower to get the capital it needs to sustain its business while it goes through the IPO process or it is shopped around to potential buyers.

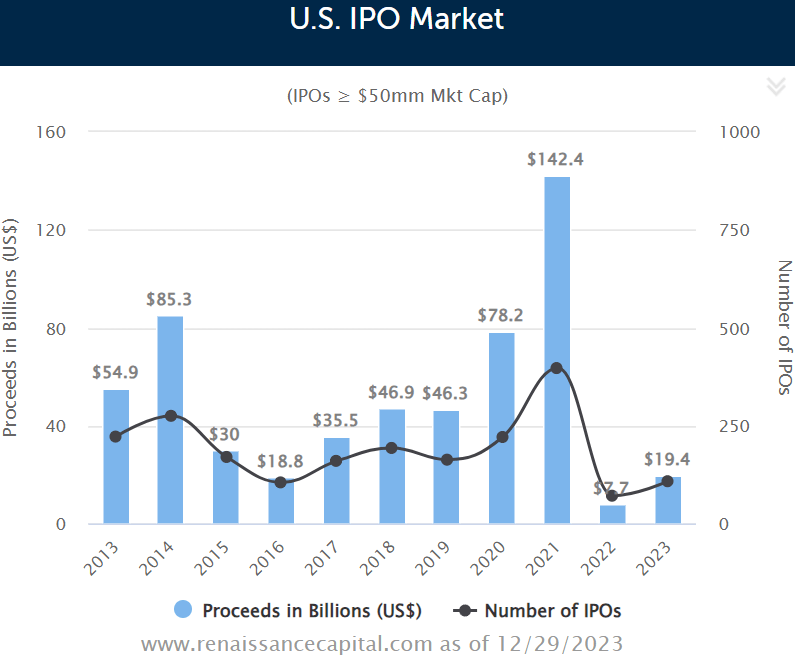

It has been a tough couple of years for companies that are backed by venture capital. IPOs were very low in 2022 and 2023 as companies were unwilling to take the risk of flopping an IPO. Source.

RenaissanceCapital Website

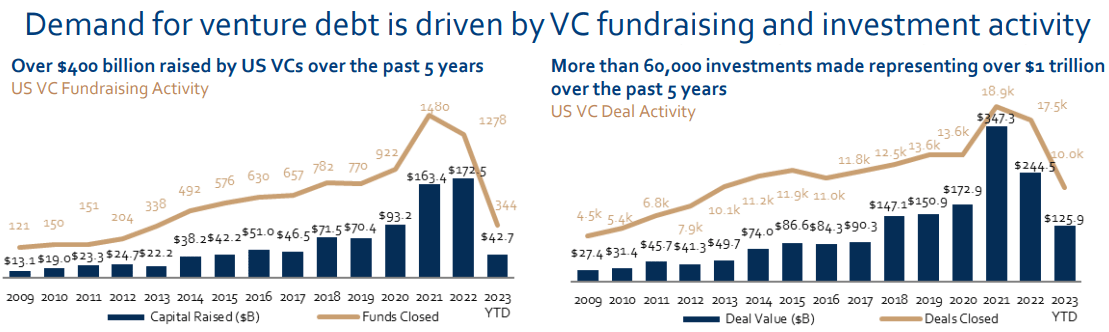

Additionally, venture capital raised and venture deals closed declined dramatically in 2023. Source.

TPVG Q3 2023 Presentation

The failure of Silicon Valley Bank (OTCPK:SIVBQ), a bank that catered to venture capitalists and startups didn’t help the sector. This led to a few consequences for TPVG:

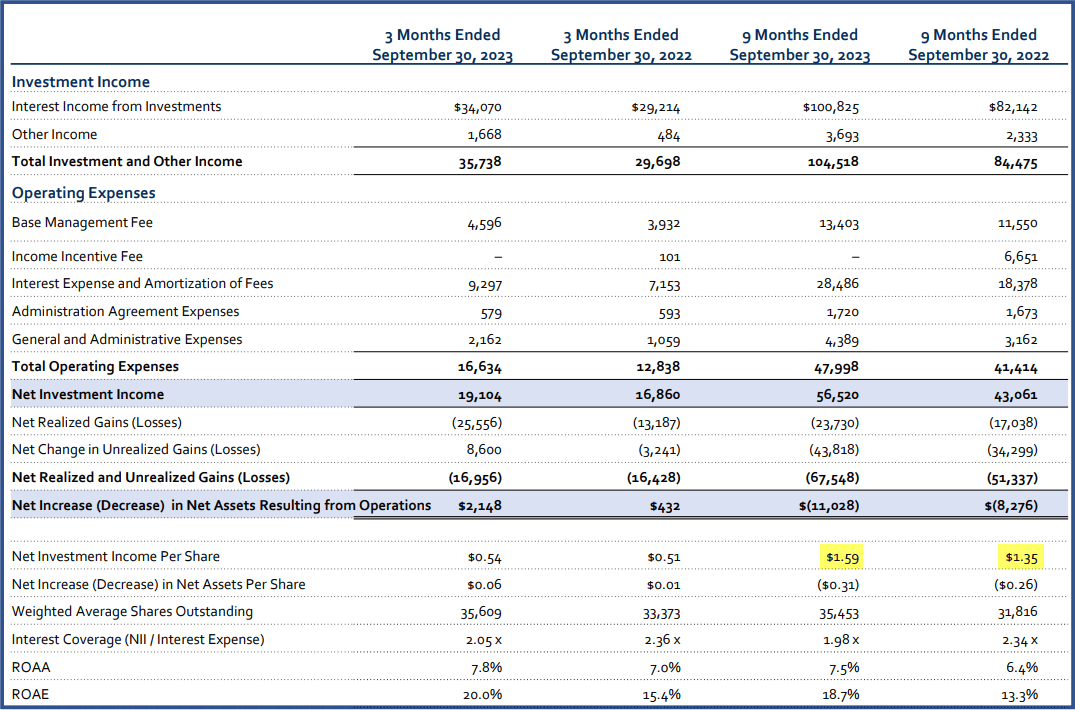

1: Demand for their services increased. TPVG saw higher net investment income and was able to achieve higher spreads and higher yields on its new investments in 2023. NII per share climbed 17% year-over-year as of Q3.

TPVG Q3 2023 Presentation

So why is TPVG’s share price down?

2: Several borrowers filed for bankruptcy. Venture capitalists tightened their belts, and with that came the willingness to make the tough decisions about which companies to back up and which to cut off.

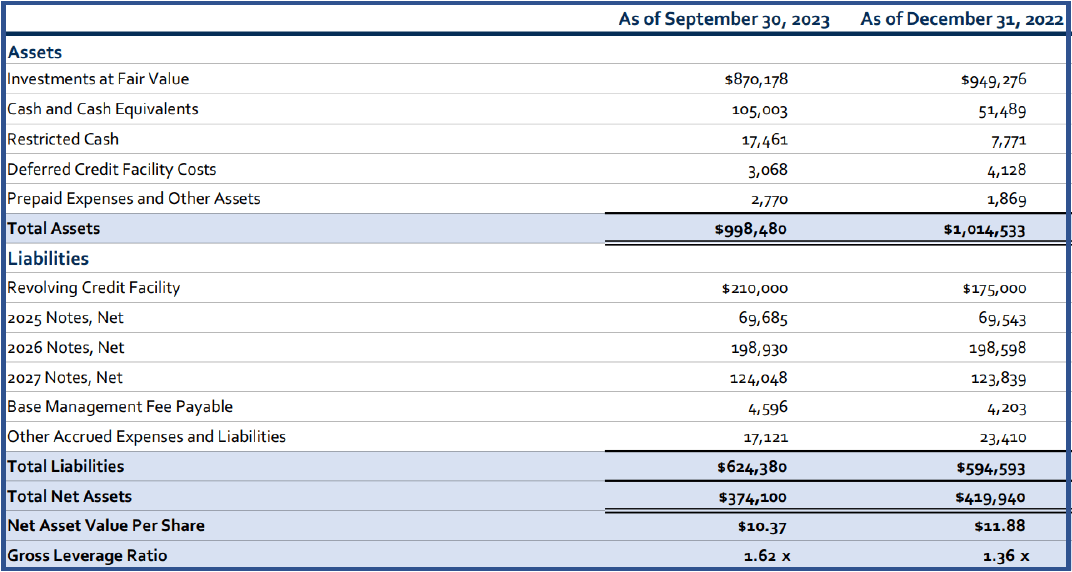

These bankruptcies impacted TPVG in Q2 and Q3, driving NAV down to $10.37/share.

TPVG Q3 2023 Presentation

This leads to a very interesting situation where 2023 was a very strong year in terms of cash flow, but a very difficult one in terms of NAV for TPVG.

With two quarters that saw bankruptcies, the natural fear for investors is that there will be more in the future. That fear is understandable, given two back-to-back quarters with sizable declines in NAV. However, it is very common for bankruptcies to come in waves. The companies that filed for bankruptcy were all dealing with the same macro issues: high interest rates and a difficult capital-raising environment. Anytime there is a significant shift in macro conditions, there are companies that will adapt and survive and those that will fail. The failures tend to all happen in relatively quick succession.

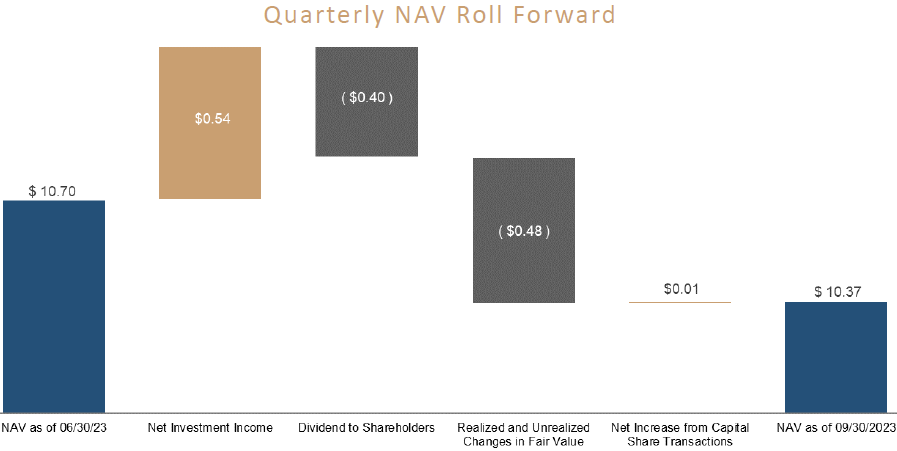

So, a BDC like TPVG can be faced with large losses when these bankruptcies happen in one quarter. From Q2 to Q3, TPVG wrote off $0.48 in NAV losses. However, TPVG also saw a $0.14 increase in NAV from excess cash flows.

TPVG Q3 2023 Presentation

The losses from bankruptcy are one-time, while net investment income is recurring. In time, the excess cash flows will mitigate the decline in NAV. With TPVG’s current cash flow, NAV will climb unless there are more bankruptcies.

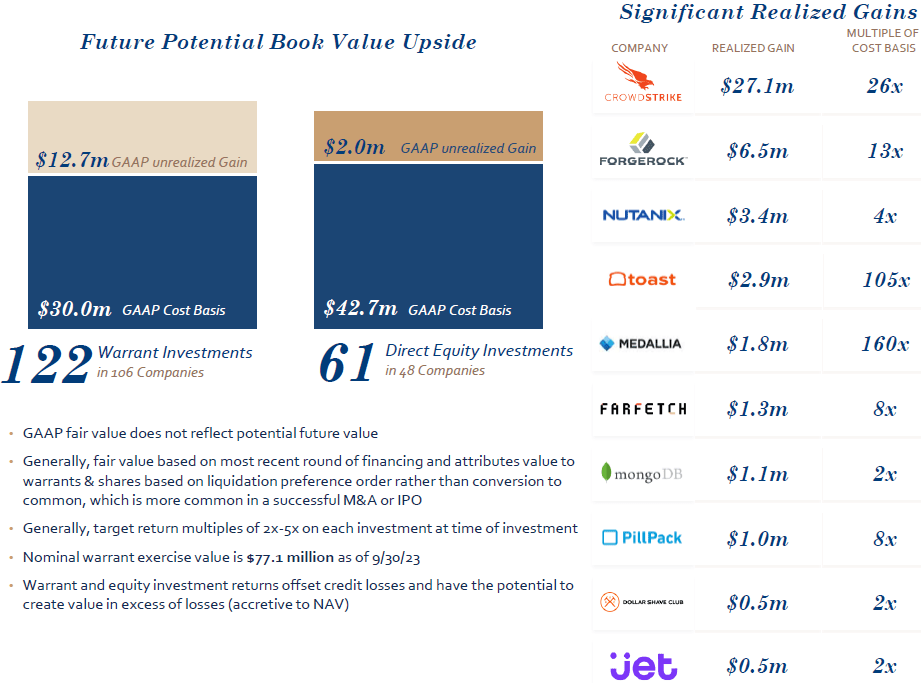

TPVG also has a significant number of warrants and common equity positions that are capable of producing a substantial upside in NAV.

TPVG Q3 2023 Presentation

Like with bankruptcies, positive liquidity events also tend to happen in spurts. The gains from these will offset the credit losses from the difficult times. We expect that the gains will likely be much larger than the losses.

It has been a tough year for TPVG in terms of book value and share price, and we see this as an opportunity to buy a great BDC at a low price. The cash flow that TPVG is producing remains well in excess of the dividend, and that will help rebuild NAV and bring leverage back into a normal range. It will likely take a few quiet quarters, with no significant bankruptcies in their portfolio for the market to warm back up to them. In the meantime, we can buy at a great price and collect an excellent yield.

Conclusion

With TriplePoint Venture Growth, you enjoy an elevated yield simply because of other people’s misunderstandings. Most disagreements that we have with other people or especially our loved ones, are produced because of misunderstandings and assumptions. Many investors simply assume that they understand what is going to drive the market, and they trade accordingly without doing any deeper thought or research.

Today, we’ve looked closer at TPVG and understood what is happening under the surface, providing us the insight needed to enjoy a position offering 14% yields.

When it comes to retirement, you no longer have the expectations of a workplace or boss towering over you. Hopefully, that provides a freeing feeling to explore life without as many burdens. Don’t burden yourself with the assumptions of the market; instead, dig and understand for yourself. You can find amazing income opportunities by cutting through the noise and seeing the facts. Those opportunities provide the income that you so desperately need to pay your bills and enjoy retirement on your terms.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Q2 2024 Earnings Call Transcript")