bjdlzx

Investment Thesis

Oil and gas continue to be a cornerstone of the global economy, yet the stocks are very undervalued despite higher oil prices. I think overall a lot of oil stocks continued to be neglected due to low institutional interest as they are reluctant to invest in fossil fuels. Thus, this lack of appetite creates bargains for investors who like oil stocks in today’s market. GeoPark Limited (NYSE:GPRK) is a solid choice in my opinion due to its high profit margins, solid growth potential, and cheap valuation. I expect the company to continue to grow as it develops more wells and invests in the proper infrastructure to take advantage of high oil prices.

A Latin American Oil Producer

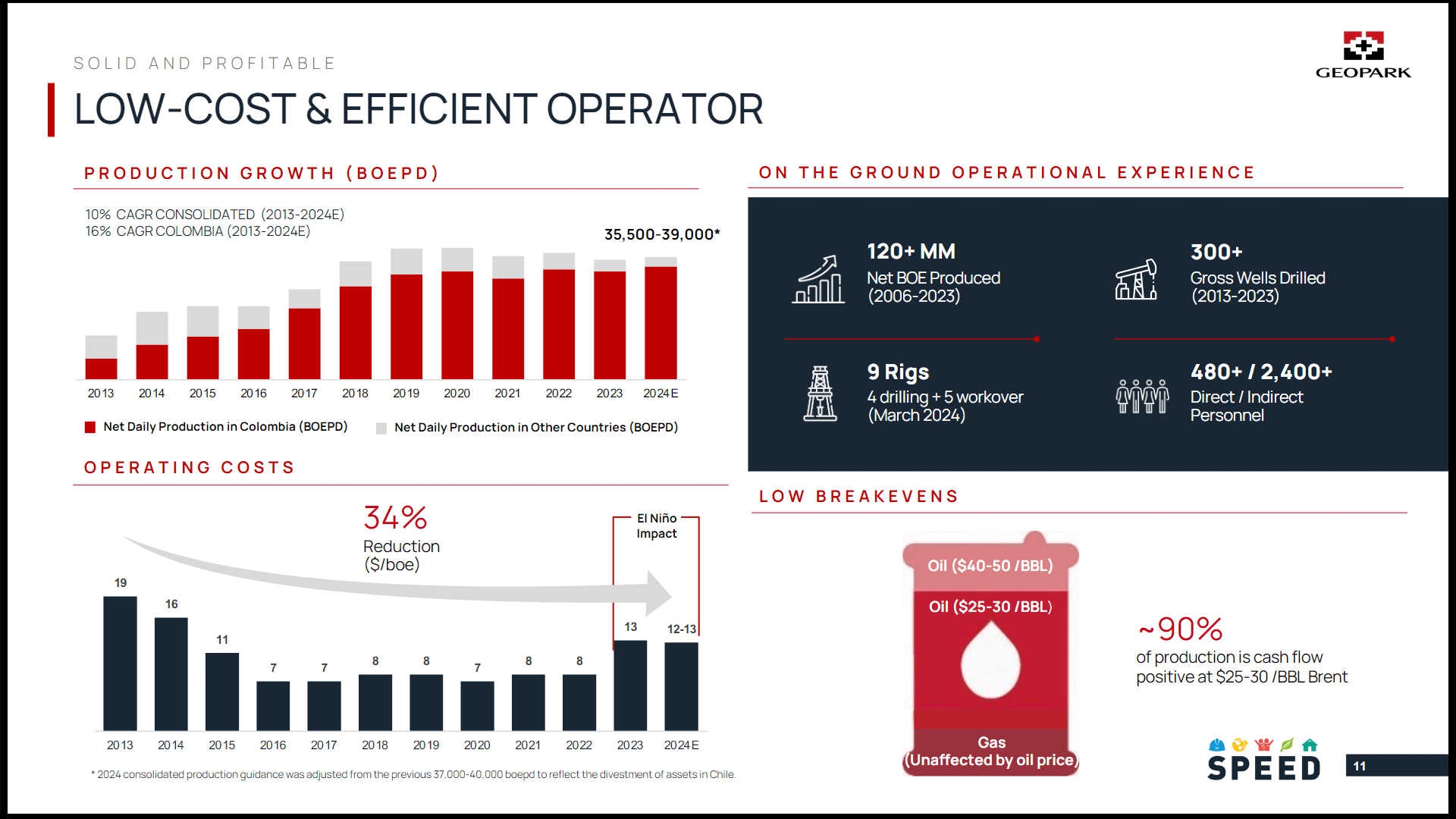

The company is an oil E&P company with operations across Latin America. They have a strong track record of unlocking value through their assets and sport a 10% CAGR of oil and gas production from 2013 to today. Most of their wells are very profitable at current spot prices, so as long as oil prices stay high, the company should continue to deliver tremendous earnings.

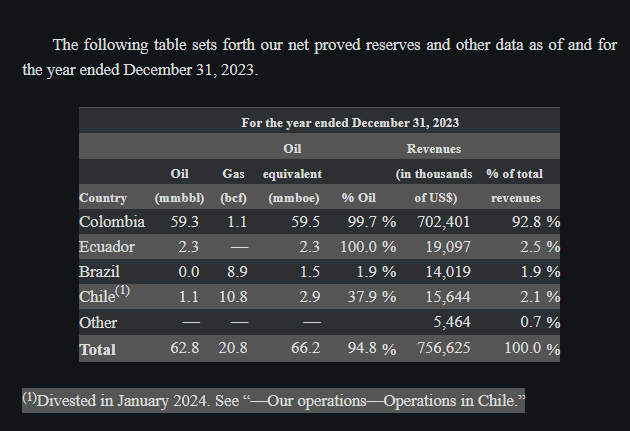

For the year 2023, most of their revenues come from Colombia. The majority of revenues comes from oil production, and the company has “working and/or economic interests in 34 hydrocarbon blocks, 33 of which are onshore blocks, including 10 in production as of December 31, 2023” (Annual Report, Page 39).

Annual Report

I feel Colombian oil stocks are some of the cheapest securities on the market today. GeoPark in particular has a proven track record of growing oil production, healthy amount of developed and undeveloped reserves to tap into, and stable cash flow. Management has been disciplined in capital allocation with generous dividends and developed strong partnerships with leading refineries like Ecopetrol (EC) and Petrobras (PBR).

Also, being the main operator of their oil assets allows them to control production costs to stay competitive. The annual report mentions on page 41,

As of the date of this annual report, we are and intend to continue to be the operator of a majority of the blocks and concessions in which we have working interests. Operating the majority of our blocks and concessions gives us the flexibility to allocate our capital and resources opportunistically and efficiently within a diversified asset portfolio.

Having control of their working interests has made them extremely profitable, with 5Y average EBITDA margins of 50%, and a 5Y average return on total capital of 20%. Assuming the company continues to benefit from being the owner operator, I expect high oil prices to continue to allow profit margins to remain high.

Oil Prices Should Remain High

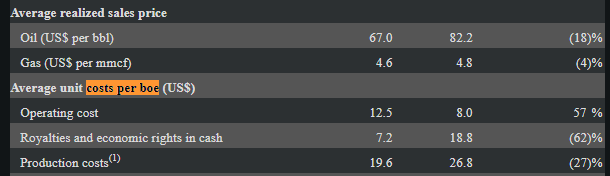

Probably the most important driver of oil stocks is oil prices in my opinion, and I believe oil prices should remain high for the next year or two. I see continued geopolitical instability from Russia, production cuts from OPEC, and sustained demand to keep prices relatively high. For the next year or two I expect oil prices to remain in the range of $60-$90 a barrel, giving investors of GeoPark sustained profitability as their costs of producing a barrel are around $20 per barrel.

Annual Report, Page 94

The EIA forecasts high spot prices for the rest of 2024,

The Brent crude oil spot price will average $90 per barrel in the second quarter of 2024, $2/b more than our March STEO, and average $89/b in 2024. This increase reflects our expectation of strong global oil inventory draws during this quarter and ongoing geopolitical risks.

Some will notice that operating costs have increased a bit and may wonder if that trend should continue. Management comments that an “increase in energy costs occurred in 2023 due to a drought that affected the energy matrix in Colombia as a result of decreased availability of hydroelectric power” (Annual Report, Page 90). However, the increase in operating cost was more than offset by a decrease in royalties, so overall the production costs are demonstrably lower. I feel that even with modest cost increases the company still generates large cash flows and that high oil prices are more than enough to offset any cost pressures. The company continues to drill well after well to take advantage of high oil prices, which should grow profits further. In their earnings call they mention,

We invested $200 million in capital expenditures during 2023 to drill 48 gross wells resulting in a 2P reserve replacement ratio of 110% and average production annually of 36,500 barrels of oil per day equivalent.

Given their historical record of successful investments increasing oil production, I feel that their investment team is very skilled in finding and developing the right reserves. The company sports very high production efficiency, growing 2P reserves, and plans to drill more wells. I expect oil production to increase and earnings and cash flows to follow so long as oil prices remain high.

Investor Presentation

Stable Cash Flows Lead To Sustainable Growth

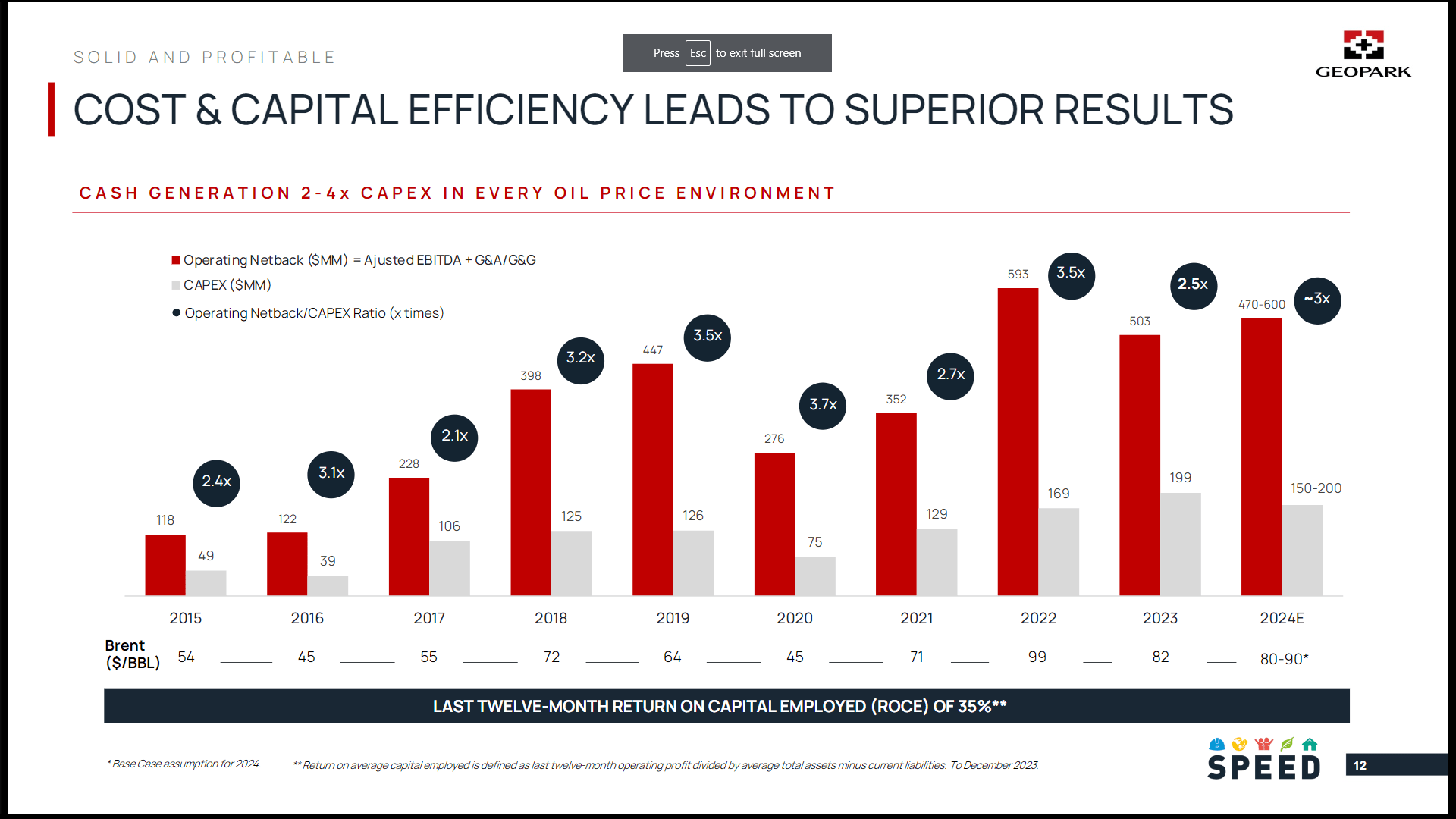

Cash flows are the highlight of this company, growing from $26 million in 2015 to $300 million in 2023. I’m surprised to note that the company remained cash flow positive in 2020, during the peak of the pandemic when oil prices went negative. Thus, I believe their hedging program and cash flows are incredibly resilient and make this stock more attractive as the company has a proven track record of weathering intense storms.

With growing cash flows comes the increased ability to reinvest in the business, driving sustainable growth. I like how management has been disciplined in keeping their capex below cash flow, so the dividends they pay seem well covered. Capex has risen from $75 million in 2020 to $200 million in 2023, signaling management’s confidence in growing the business organically. Many of these investments went to drilling high ROI wells, with an expected operating netback/capex ratio of over 3x for 2024.

Investor Presentation

As long as oil prices stay high, I think the ROCEs and returns on capex are extremely attractive, and stable cash flows allow the company to plant the seeds for sustainable growth. Therefore, I feel that the growth potential of GeoPark is very valuable, as every dollar that is reinvested has very high returns on capital employed.

Finally, the company’s strong balance sheet allows them to grow safely without much risk to shareholders. The company sports a current ratio of over 1, and a strong Debt/EBITDA of 1.23x ($533 million/$433 million). Most of the debt is long-term and refers to a $500 million bond that matures in 2027. I am confident they can reduce their leverage profile given their strong free cash flow. If money gets tight all they have to do is reduce capex spending for a year or two and they should be able to strengthen the balance sheet even further. All in all, it looks to me the company is in control of their growth, profitability, and leverage.

Valuation – $15 Fair Value

Assuming oil stays at relatively high prices, I think revenues will stay above a floor of $700 million annually going forward. This is slightly below TTM revenues of $756 million which makes a floor of $700 million very conservative.

Apply a 5Y average EBITDA margin of 50% gets me annual EBITDA of $350 million. Multiply by a conservative multiple of 3.5x EBITDA (which is below the sector median of 6x) gets me an enterprise value of $1.23 billion. Subtract net debt of 400 million gets me a market cap of $830 million. Divide by shares outstanding of 55 million gets me $15 per share fair value.

I feel comfortable with my conservative estimates, and as long as oil prices remain in a comfortably high range of $70-90 a barrel the company may substantially outperform my expectations. The company also pays a nice 5.34% dividend yield, and trades at 5.5x free cash flow.

Management gives us some hints of its stock being undervalued in their earnings call,

As part of our disciplined capital allocation process, our own shares are currently offer a unique opportunity for repurchase, which is why we announced our intention to commence a modified Dutch auction tender to buy up to $50 million of GeoPark shares, following our view that the current market value of GeoPark does not properly reflect the intrinsic net value of our assets.

Going forward, I expect some buybacks to drive shareholder value, as prices do not seem to reflect the company’s future growth potential and oil asset base. At 3x FWD earnings the stock is very cheap and should give investors good returns from here.

Risks

Oil stocks face risks stemming from the future price movements of oil directed by supply and demand. If demand plummets or the market is glutted with oversupply, price declines in oil could lead to shares underperforming. Investors should keep an eye on the price of oil to see if any economic shocks could put pressure on the fundamental performance of GeoPark.

As most of their revenues come from Colombia, royalties are unusually high as Colombia derives a large portion of their GDP from oil exports. So, if the Colombian government raises taxes and royalties, it could hurt future profitability of GeoPark.

Colombia’s president Gustavo Petro is urging a transition to green energy, which could put oil companies at risk as they are in a politically unfavorable position. He seems very adamant on getting rid of fossil fuels in his country, but so far, the impact seems to be relatively insignificant, as GeoPark still reports strong profits.

In the long term, the company may struggle to replenish reserves as they start to run out. Management has to keep exploring and producing from new wells in order to keep growth going, and this depends on the success of their exploration efforts, which can be highly variable. Also, the company discloses that they have a few key clients on page 8 of their annual report,

During 2023, the oil and gas production was sold to three clients which concentrate 96% of the Colombian subsidiaries’ revenue (accounting for 89% of the consolidated revenue).

Any loss of a customer could materially hurt revenues, as three clients make up a lot of sales for GeoPark. I feel more customer diversification would be appreciated for investors going forward.

Buy GeoPark

I see a lot of cheap oil stocks in Colombia, and GeoPark was very attractive given its track record of successful exploration, production, and profitability. With oil prices remaining at relative highs, I see opportunity for buying Colombian oil stocks. Their assets are incredibly productive and GeoPark has plenty of reserves to fuel growth. At 3x FWD earnings and over a 5% dividend yield, it is clearly cheap and investors who like oil stocks should consider buying GeoPark.

Q2 2024 Earnings Call Transcript")