Love Employee/iStock via Getty Images

Genmab (GMAB) is a leading contender in the biotech industry, demanding attention from investors for its innovative technology, robust pipeline, and strategic collaborations. In my previous Genmab article (6/9/22), I discussed how the company’s antibody technology, broad portfolio, and impressive list of collaborations would continue to yield significant growth. Fast forward to today, we can say that Genmab has produced impressive growth grades, but the share price has returned to the same levels as when I wrote my last article. Despite reporting strong growth, the DARZALEX litigation has put a dark cloud over the ticker and DARZALEX sales falling short of some analysts’ expectations in Q3 have weighed on the share price. However, I am still incredibly bullish on GMAB thanks to three positive trends heading into 2024.

I intend to provide some background on Genmab and review three positive trends GMAB investors should monitor throughout 2024. In addition, I discuss some downside risks that investors need to keep an eye on. Finally, I laid out my plan for my GMAB position in 2024.

Background On Genmab

Genmab’s focus is on the development of monoclonal antibodies, which are engineered molecules designed to target specific proteins involved in disease processes. Over the years, the company has established itself as a monoclonal antibody powerhouse, forming strategic collaborations with big pharma and leading biotech companies to develop cutting-edge products.

At the core of Genmab’s success lies its state-of-the-art platform technology. The company utilizes unique technologies called DuoBody, HexaBody, DuoHexaBody, and HexElect. These proprietary platforms enable the creation of next-gen antibodies that have advantages over traditional monoclonal antibodies. These developments in versatility open up new possibilities for therapeutic interventions, allowing for more precise and effective treatment stratagems.

#1 – Epcoritamab’s Growth

Epcoritamab Genmab’s groundbreaking bispecific antibody co-developed with AbbVie (ABBV) adults with relapsed or refractory diffuse large B-cell lymphoma (DLBCL) who have undergone two or more lines of systemic therapy. Notably, Genmab’s financial performance for the first nine months of 2023 reflects the company’s growing success. Revenue increased by an impressive 26% compared to the same period in 2022, reaching DKK 11,796M. The company attributes this remarkable growth to the regulatory approvals in Japan and Europe for EPKINLY/TEPKINLY (epcoritamab). Genmab’s assumed commercial lead for EPKINLY in Japan signifies a strong foothold in this vital market. Notably, this marks a significant milestone as it represents the first Genmab-owned medicine available outside of the U.S., expanding therapeutic options for patients in these regions. Moreover, Epcoritamab has secured approvals in Canada and the UK.

Genmab Epcoritamab (Genmab)

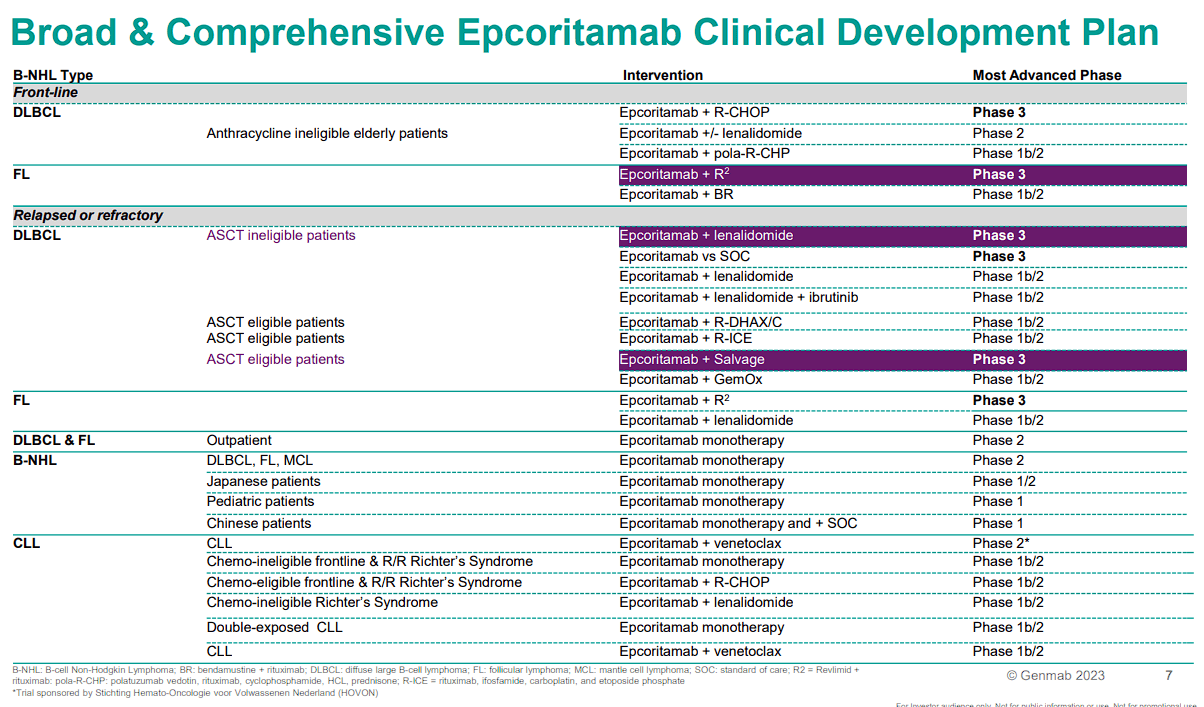

Genmab’s near-term success is going to be linked to epcoritamab growth over 2024 and their effort to continue the collaboration with AbbVie to investigate epcoritamab as a cornerstone therapy across various B-cell malignancies.

Genmab Epcoritamab Development (Genmab)

Therefore, investors should keep a close eye on epcoritamab’s commercial trajectory and pipeline programs.

#2 – DARZALEX Growth

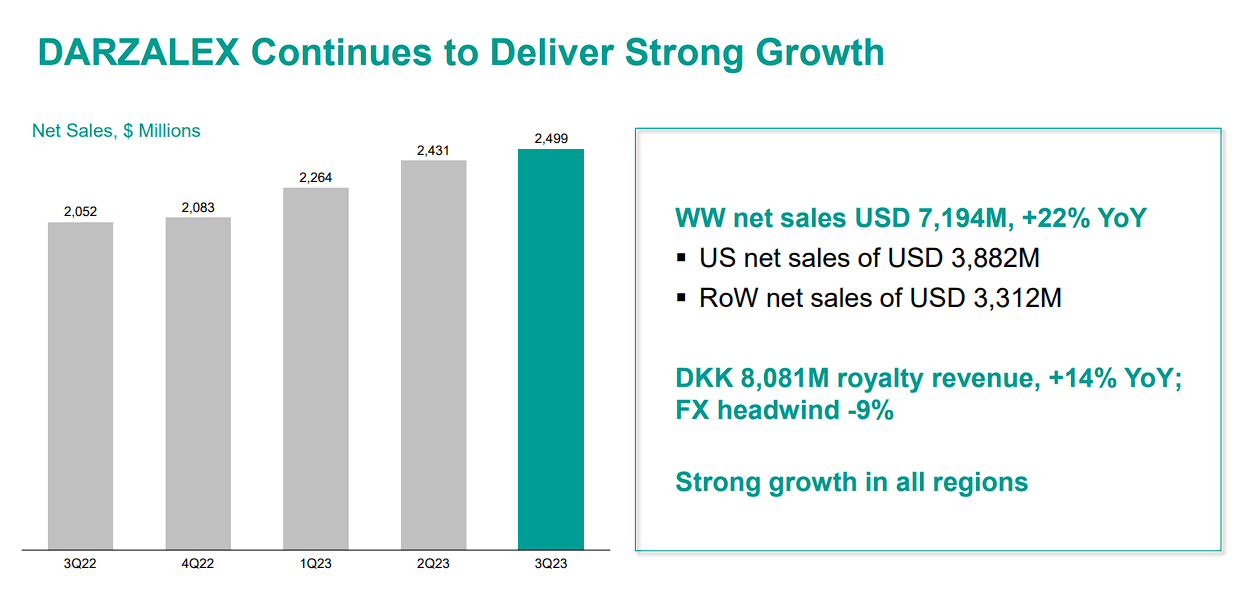

DARZALEX, Genmab’s flagship product, has continued to be a substantial revenue driver recording sequential sales growth with ~$2.5B for Q3 of 2023 and reaching nearly $7.2B for the first three quarters of 2023. DARZALEX is currently the ticker’s rudder, so growth should continue to support GMAB’s performance. However, waning growth and concerns over royalty their battle with Genmab’s partner, Johnson & Johnson (JNJ), over DARZALEX licensing and royalties.

Genmab DARZALEX Growth (Genmab)

Furthermore, investors should monitor DARZALEX’s clinical programs that could add to the product’s commercial potential. Recently, Johnson & Johnson (JNJ) has reported positive results for a Phase III study of Darzalex Faspro in combination with the traditional VRd regimen, which reduced the risk of disease progression or death by 58% when matched to the standard of care. At the four-year mark, 84.3% of patients receiving Darzalex Faspro with VRd were still alive without disease progression, versus 67.7% in the VRd-only group. So, Darzalex has the potential to grow in the coming years as more label expansions enhance its commercial potential.

Johnson & Johnson DARZALEX Phase III Programs (Johnson & Johnson)

Although Genmab’s relationship with Johnson & Johnson is not perfect, the company needs their partner to continue to maximize DARALEX’s clinical and commercial potential.

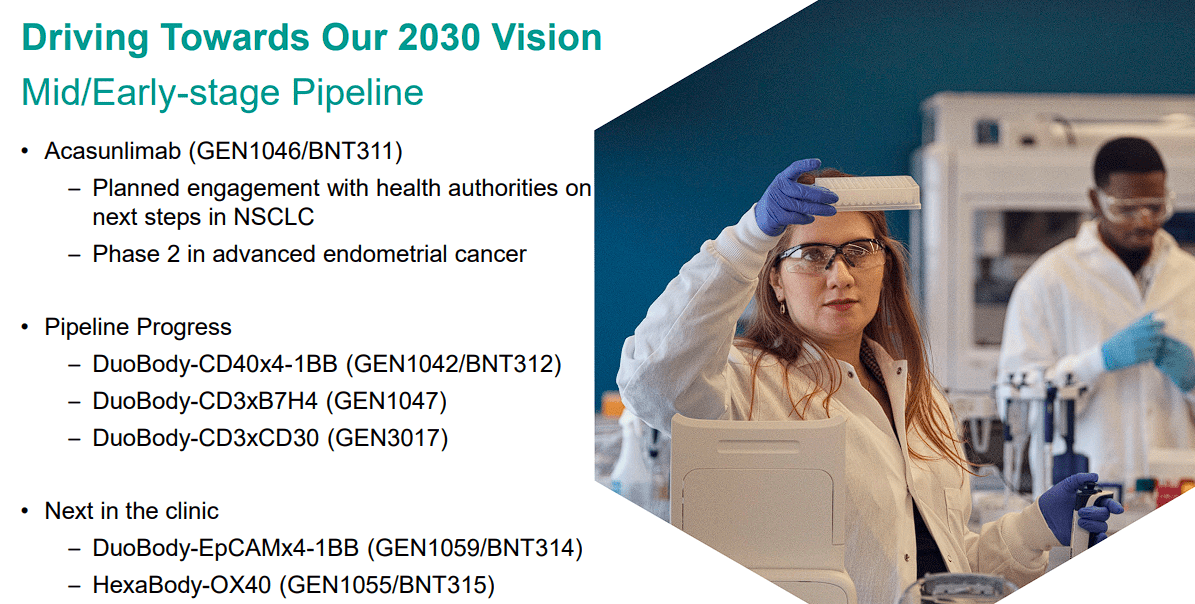

#3 – Advancing The Pipeline

Genmab’s robust discovery engine holds plenty of value with 19 candidates in active clinical development, showcasing an exceptional hit rate. The company’s emphasis on the significance of DuoBody and HexaBody tech has provided them with a unique toolkit to address specific disease targets effectively, positioning Genmab at the pole position of antibody innovation.

I like the compelling narrative around GEN1046, a collaborative venture with BioNTech (BNTX), revealing promising results in combination with checkpoint inhibitors for non-small cell lung cancer (NSCLC). Simultaneously, Tivdak, developed in partnership with Seagen (SGEN), demonstrated positive outcomes in the innovative 301 trial for cervical cancer, hitting the primary endpoint of overall survival (OSS).

Genmab Early & Mid-Stage Pipeline (Genmab)

The company’s $3.9B in cash has allowed them to invest in their development as total OpEx swelled by 42% for the first three quarters of 2023. The company has confidence in pushing their pipeline forward on all fronts thanks to their forecasts of sustained growth, with an increased bottom end for revenue.

An increase in approved products should translate into their earnings, or at least lessen their dependency on DARZALEX and bolster their long-term outlook. As a result, it is almost imperative that the company keeps the pedal down in the lab and the clinic.

The Impact

I believe Genmab’s 2024 performance will be dependent on their ability to safeguard the positive trends in innovation, development, and partnership revenue. Indeed, some of these trends are out of the company’s control. Thankfully, the company has a sturdy financial foundation, broad portfolio, and industry-leading tech for their long-term performance goals and be a trailblazer in the biotech realm. Genmab’s financial strategy revolves around continued investment in promising programs, leveraging existing platforms, and maintaining a disciplined approach to ensure resources are allocated effectively.

Certainly, the company’s efforts and financial commitment to their pipeline will have an impact on their earnings growth.

Genmab Annual EPS Estimates (Seeking Alpha)

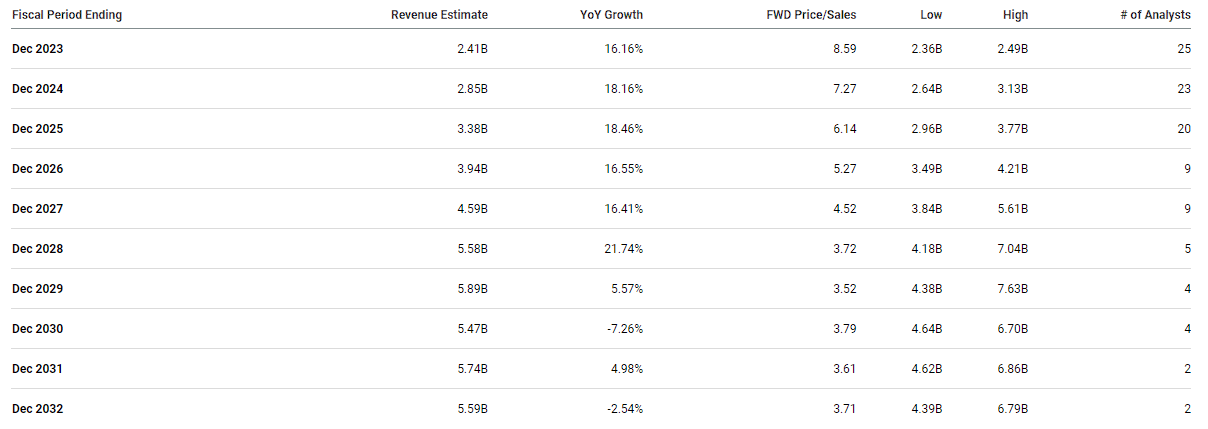

On the other hand, the Street expects Genmab to report solid double-digit growth and double their revenue in the next few years.

Genmab Annual Revenue Estimates (Seeking Alpha)

Therefore, I remain optimistic about the potential of Genmab’s pipeline, particularly with EPCORE and other late-stage programs ultimately allowing the company to become less dependent on DARZALEX.

Risks To Consider

While Genmab has achieved outstanding success, investors need to recognize the inherent risks associated with drug development and the volatility of the biotech arena. Some key risks include clinical trial outcomes, market competition, regulatory challenges, IP risks, and market dynamics. These risks could have a significant impact on the company’s operations and long-term outlook. Even though Genmab is an established company with strong fundamentals, one of the risks listed above could challenge or derail the company.

Considering these risks, I am keeping my GMAB conviction level at 4 out of 5.

My Plan

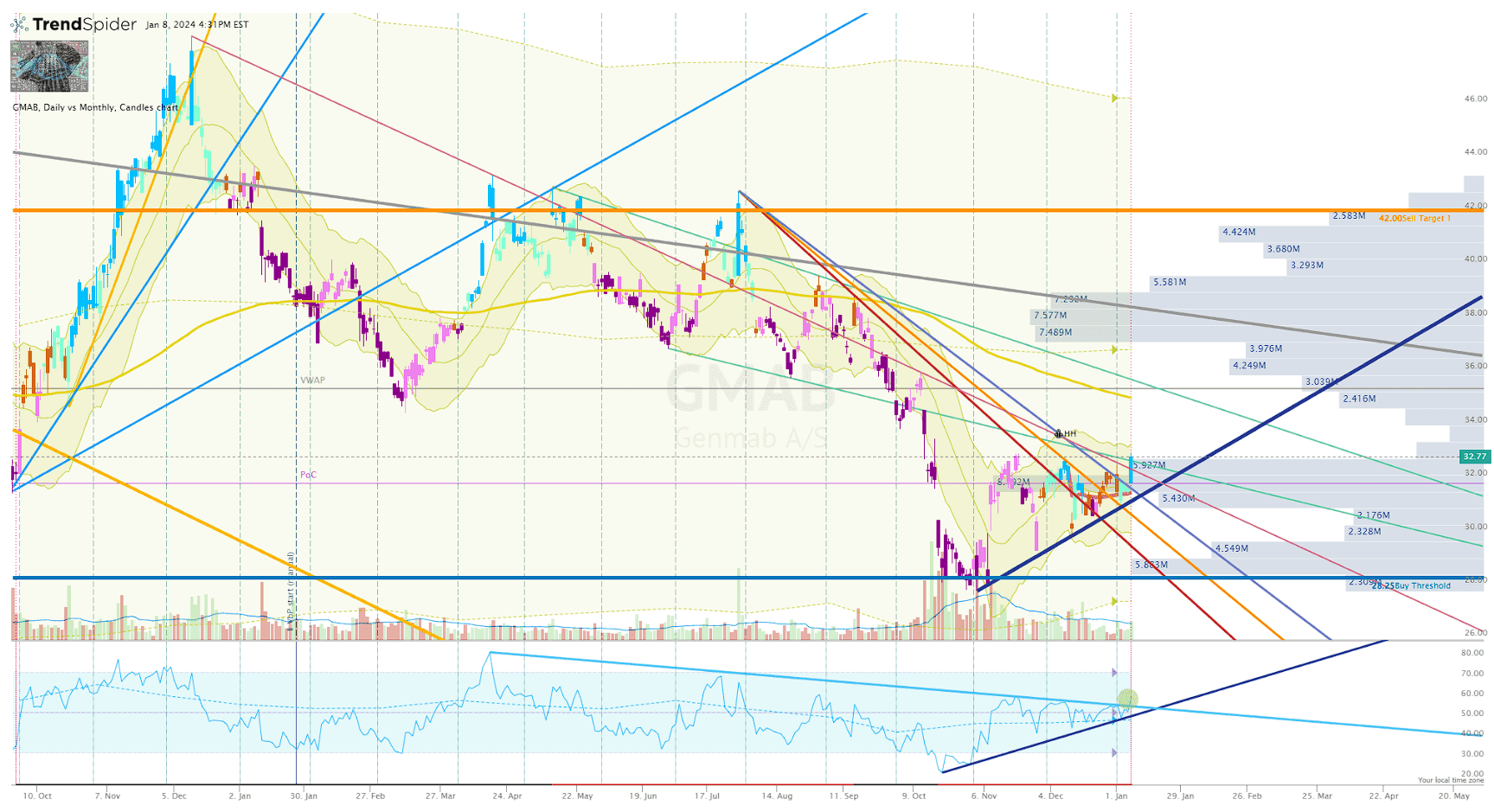

Despite GMAB being a “Top Pick” in the Compounding Healthcare “Bioreactor” growth portfolio, my position was dormant for almost the entire calendar year of 2023 due to the ticker trading above my Buy Threshold ($28.25) and the unknown impact from the DARZALEX litigation. Now, GMAB is back to trading above my Buy Threshold and is showing a solid setup on the Daily Chart.

GMAB Daily Chart (Trendspider)

My methods necessitate that I wait for the share price to return to my Buy Threshold before clicking the buy button, however, it appears as if I may be risking GMAB moving higher. The share price is easily chewing through downtrend rays from the July 2023 high, and the RSI just broke out of a pennant pattern. Plus, the ticker is currently bullish on the Go-No-Go indicator… so, there is a strong likelihood that GMAB will be trading above my Buy Threshold for a prolonged period of time, and might never return. Therefore, I am going to wait to see if the company’s Q4/2023 earnings report justifies updating my Buy Threshold and Targets to suit their current fundamentals and the ticker’s technical analysis. Until then, I am going to remain vigilant and will place a small buy order around my Buy Threshold, just in case the market wants to retest the 2023-lows.

Long-term, I still plan on maintaining a GMAB position for the foreseeable future and will continue to trade the ticker to grow a “house money” position for a long-term investment.

Q2 2024 Earnings Call Transcript")