izusek

Late last year, after seeing shares drop relative to the S&P 500, I decided to revisit GE HealthCare Technologies (NASDAQ:GEHC), an entity that was previously spun off from industrial conglomerate General Electric (GE) in early 2023. At that time, I reiterated my ‘strong buy’ rating, which is a rating I assigned companies that I believe should outperform, by a rather meaningful margin, the broader market for the foreseeable future. The company had, up to that point, continued to see attractive revenue growth. However, bottom-line results had been disappointing.

Despite those bottom-line issues, the picture is now looking up. Management has since come out with guidance for 2024 that sees profits and cash flows rising nicely. Add on top of this how cheap shares are relative to similar firms, and I do believe that additional strong upside is still on the table. To be clear, I don’t think we are looking at a doubling of the share price or anything like that. In fact, if we get another 10% or 15% upside compared to where we are today, a downgrade to a ‘buy’ rating would likely be on the table. But until that occurs, investors have every reason to be bullish.

The picture is improving

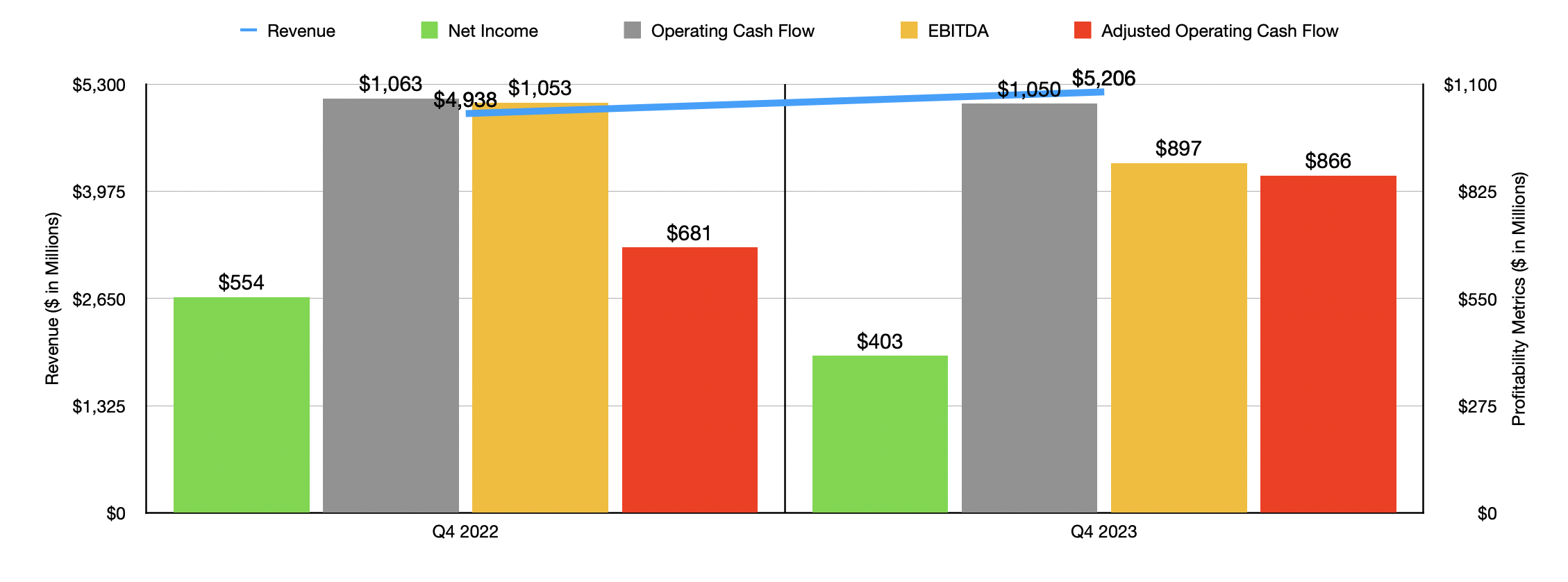

When I last wrote about GE HealthCare Technologies in early December of last year, we had data covering through the third quarter of the 2023 fiscal year. Today, that data now extends through the final quarter. So that might be a good place to start with. During that time, revenue for the business came in at $5.21 billion. That’s an increase of 5.4% over the $4.94 billion generated the same time one year earlier. Essentially, all of this upside was driven by organic means. Management attributed this to a combination of higher prices and increased volume. It’s always great to see both of these come into play in a positive way.

Author – SEC EDGAR Data

This doesn’t mean that every aspect of the company performed well. The best performer, by far, was the Pharmaceutical Diagnostics segment of the business. Revenue shot up 25%, or about 23% on an organic basis. For those not familiar, this unit focuses on supplying diagnostic agents to the radiology and nuclear medicine industries. These agents aid clinicians in the assessment of patients so as to ensure more precise diagnosis and the selection of more appropriate therapies for their respective conditions. But even with that strong increase, sales came out to only $591 million, or about 11.4% of the firm’s overall sales. Other parts of the company had more modest performance. The Patient Care Solutions and Imaging units of the company reported revenue increases of 5% and 4%, respectively, year over year. The only segment to see any weakness was the Ultrasound segment, which reported a 2% decline on an organic basis compared to one year earlier.

Although it’s great to see the increase in revenue, bottom-line results were not exactly great. Net income of $403 million fell short of the $554 million reported one year earlier. There were a few different cost categories where the company suffered. Selling, general, and administrative costs, all rose year over year. The business also reported an increase in interest expense from $59 million to $131 million. On top of this, while revenue rose 5.4%, research and development costs jumped 16.2%. Other profitability metrics mostly followed suit. Operating cash flow went from $1.06 billion to $1.05 billion. And EBITDA declined from $1.05 billion to $897 million. If we adjust for changes in working capital, we do get one exception, which would be adjusted operating cash flow. It managed to rise from $681 million to $866 million.

Author – SEC EDGAR Data

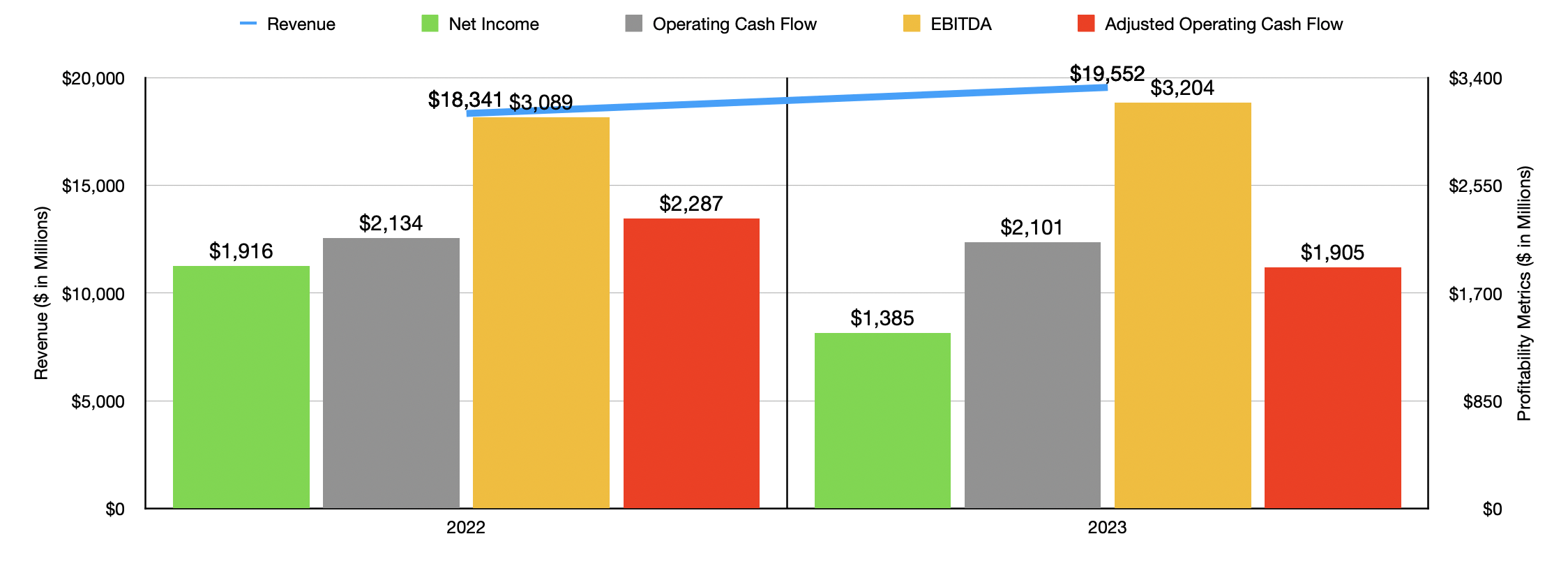

As you can see in the chart above, results for 2023 as a whole relative to 2022 showed that the final quarter of last year was not an anomaly. Revenue rose while profits fell. And with one exception, cash flows dropped on a year-over-year basis. I understand that investors would be unhappy with this. And that may help to explain why shares underperformed the market for a good portion of last year. However, when releasing results for the final quarter of 2023, management revealed guidance for 2024. Organic revenue is expected to rise by about 4%. If that comes to fruition, that should translate to roughly $20.33 billion. On top of this, margin expansion is expected to push earnings per share, on an adjusted basis, up to between $4.20 and $4.35. That compares to the $3.93 generated in 2023. That would translate to net profits rising from $1.80 billion on an adjusted basis to $1.96 billion. Meanwhile, based on current guidance, EBITDA should be somewhere around $3.45 billion. No guidance was given when it came to other profitability metrics. But if we assume that adjusted operating cash flow should rise at the same rate that EBITDA is anticipated to, then we should get a reading for 2024 of $2.05 billion.

Author – SEC EDGAR Data

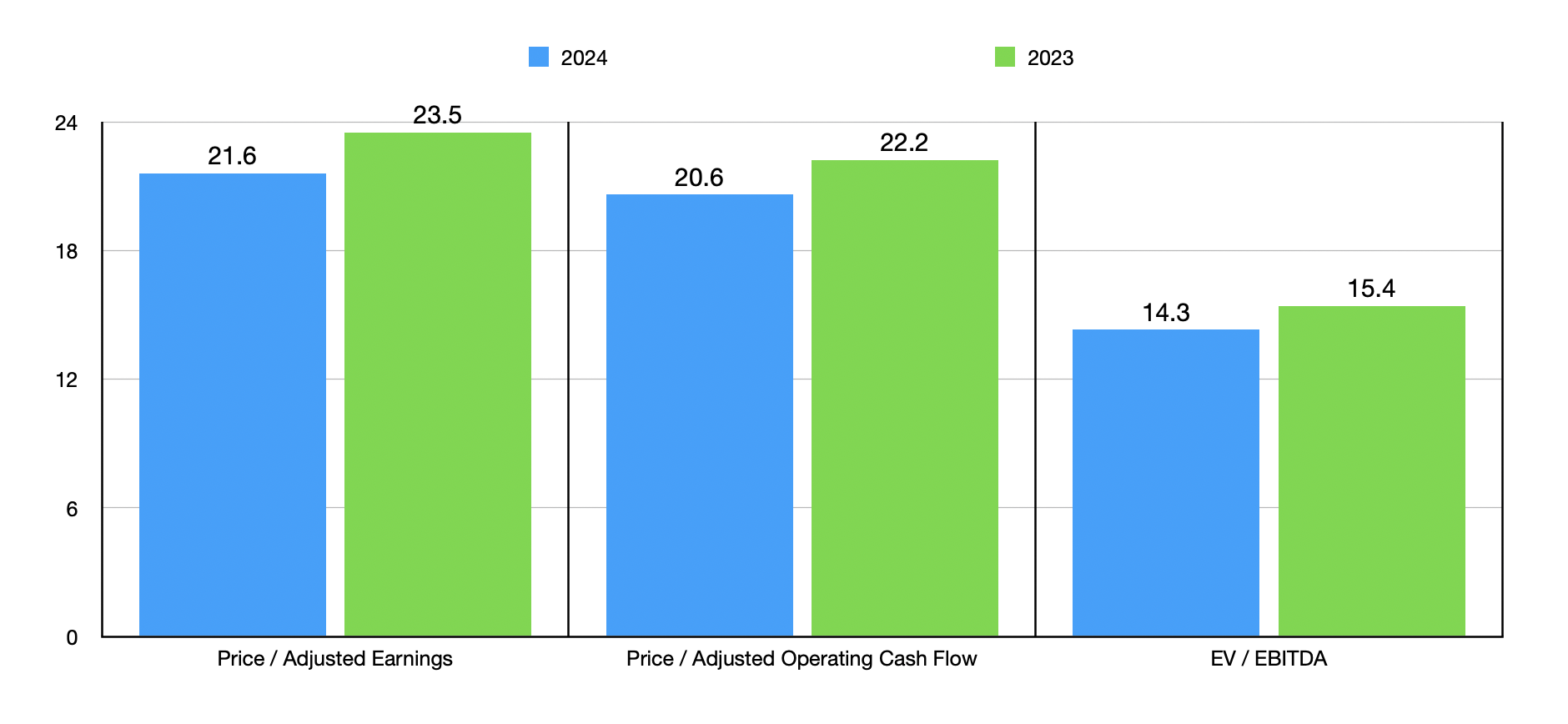

Taking these results, we can then value the company as shown in the chart above. As you can see, the stock does get cheaper on a forward basis. However, I wouldn’t say that shares, on their own, are the cheapest thing out there. But relative to similar players, they definitely are on the cheap end of the spectrum. In the table below, you can see how the stock stacks up against five similar firms. On both a price to earnings basis and on an EV to EBITDA basis, GE HealthCare Technologies ended up being the cheapest of the group. And when it comes to the price to operating cash flow approach, only one of the five companies was cheaper than it.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| GE HealthCare Technologies | 23.5 | 22.2 | 15.4 |

| Danaher (DHR) | 41.1 | 26.4 | 26.7 |

| Thermo Fisher Scientific (TMO) | 37.3 | 26.6 | 22.1 |

| Agilent Technologies (A) | 33.1 | 21.0 | 24.3 |

| Mettler-Toledo International (MTD) | 35.4 | 28.9 | 24.6 |

| Siemens Healthineers AG (OTCPK:SMMNY) | 41.3 | 26.8 | 15.7 |

A big question some might ask is what kind of upside, if any, shares of GE HealthCare Technologies might justify. To figure this out, I decided to look at two different scenarios for each of the three valuation metrics previously shown. In the table below, you can see the potential upside or downside for the stock if we assume that shares trade at the same trading multiples of the cheapest of the five companies I compared it to. And then you can also see how much upside or downside exists if we assume that shares trade at the average of the multiples for the same 5 firms. What we get is anywhere from downside of 5.4% to upside of 60.2%. This is a massive range, but it’s clear that there are some outliers here. For instance, the price to operating cash flow multiple and the EV to EBITDA multiple, both in the low scenario, seemed to be meaningful outliers. If we remove those from the equation, we’re looking at returns that are at least in the double digits.

Author – SEC EDGAR Data

Of course, this assumes that management only grows according to current guidance. This does not factor in any other potential opportunities that the company might jump on. And one thing that has been made clear over the past year is that the company is interested in different opportunities. In February of this year, the company entered into a strategic care alliance with an integrated health system known as OSF HealthCare. In short, the companies utilize the resources at their disposal to focus on achieving clinical and operational efficiencies, while also standardizing care delivery models and improving patient outcomes across the health system. And about a month before that, GE HealthCare Technologies announced its decision to acquire MIM Software, which provides AI enabled image analysis and workflow tools across spaces like oncology, urology, neurology, and cardiology. Unfortunately, the terms were not disclosed. What was disclosed is that, in addition to making interesting moves like this, the company continues to focus on improving its fundamental health. During the final quarter of last year, management bought back $850 million worth of debt. And in January of this year, they disclosed the repurchase of another $150 million of debt.

Takeaway

Operationally speaking, GE HealthCare Technologies might not be the best player in the world. Having said that, current guidance calls for massive improvements during 2024. Even if we assume bottom-line results don’t improve, shares look attractively priced relative to similar firms. Given this and given the prospect of additional upside through management’s actions such as asset purchases and debt repayment, and I believe that there are plenty of reasons to remain optimistic. If shares do end up rising another 10% or 15% without any meaningful reason, I probably will downgrade it. But even then, it would come in at a solid ‘buy’. Until then, the ‘strong buy’ rating still holds in my book.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")