Sean Gallup

Thesis

As technology penetrates almost every aspect of life, fitness and the outdoors could not have escaped. For a company that started as a navigation device manufacturer, today Garmin (NYSE:GRMN) has evolved into a comprehensive solutions provider for all things outdoors. In this analysis, I will explore the company’s attributes, financial performance and offer a more in-depth look into its valuation.

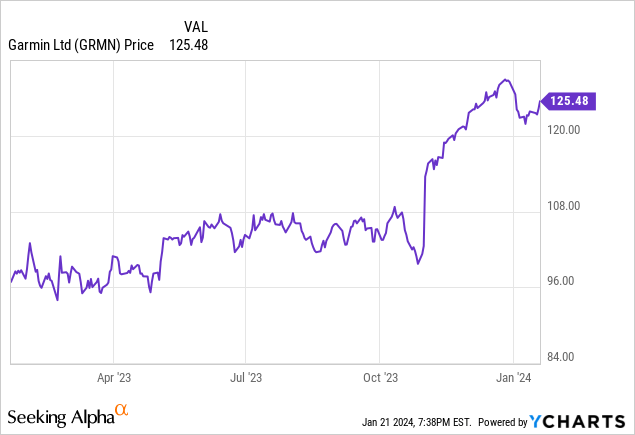

Over the past year, Garmin has recorded an impressive rally, gaining over 31% on a TTM basis. This comes after a large drop from all-time highs (yet to be reclaimed) in late 2021. Currently, GRMN trades at $125.48 per share ($24.01B market cap) and pays a 2.33% dividend yield.

A Proven-Yet-Evolving Model

For over 30 years now, Garmin has established a widely respectable brand, offering an ever-growing range of premium products centered around navigation, fitness, and the outdoors. Location technology, mainly incorporating the Global Positioning System (GPS) has been at the forefront of the Garmin brand; yet today the company offers much more than just navigation-oriented devices.

Garmin has become the brand of choice for a diverse group of customers, including runners, cyclists, off-road enthusiasts, hikers, boat owners, fishermen, and many more. In 2022, the company sold more than 15 million products globally, including sports watches, navigation hardware, satellite phones, navigation systems, and many more.

Industry Tailwinds

Even though Garmin is by no means solely focused on wearables, especially in segments like Marine or Aviation, still the smartwatches and other wearable devices the company offers represent a major chunk of total revenue, while also being the most visible and accessible products to the average consumer.

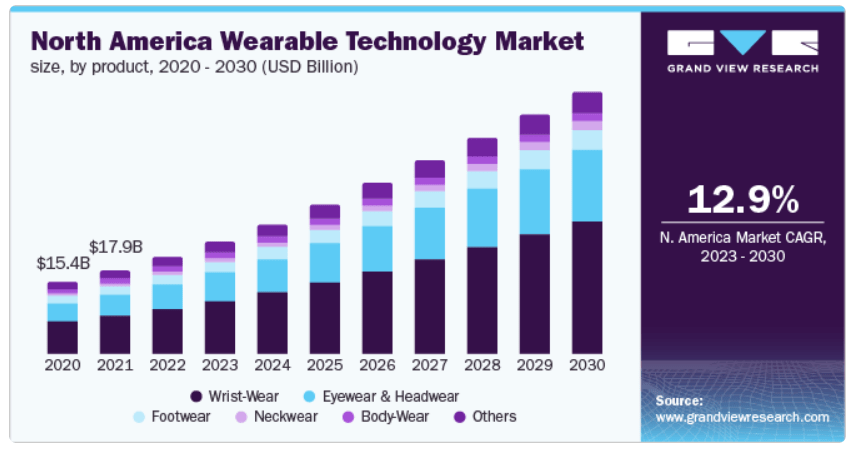

Having grown significantly over the past few years, as consumer adoption of wearables technology has dramatically increased, the wearables market is currently valued at $61B globally, with North America holding about a third of the global market share. The North American wearables market is expected to grow at a 12.9% CAGR (14.6% globally) through 2023, offering some rare, attractive growth prospects within the consumer discretionary sector.

grandviewresearch.com

More good news comes from the fact that, according to the same research approximately half of the overall revenue share is generated by wrist wearables, a subsection in which Garmin displays ample expertise and popularity.

Segment Performance

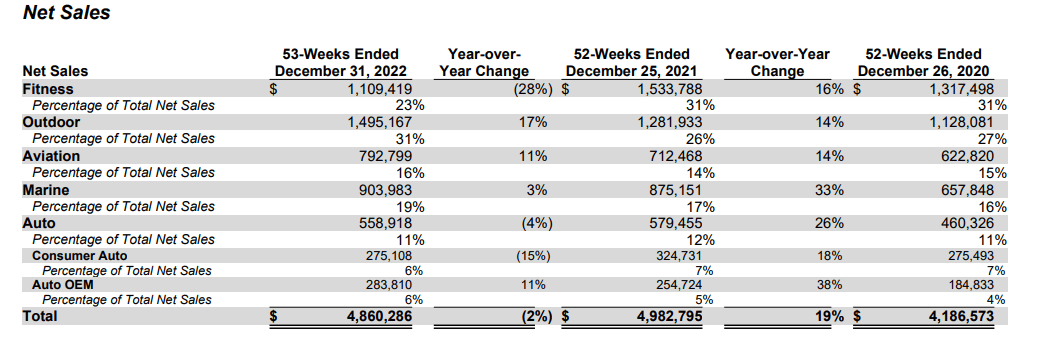

Product portfolio diversification has been the name of the game for Garmin for many years now, as all five major segments contribute significant chunks of revenue to the business. The outdoor segment has recently surpassed fitness as the higher contributor in terms of revenue, generating 31% of the company’s sales. Marine and aviation also contribute significant amounts, being the more mature and slow-growing segments for Garmin.

Garmin 10K – 2022

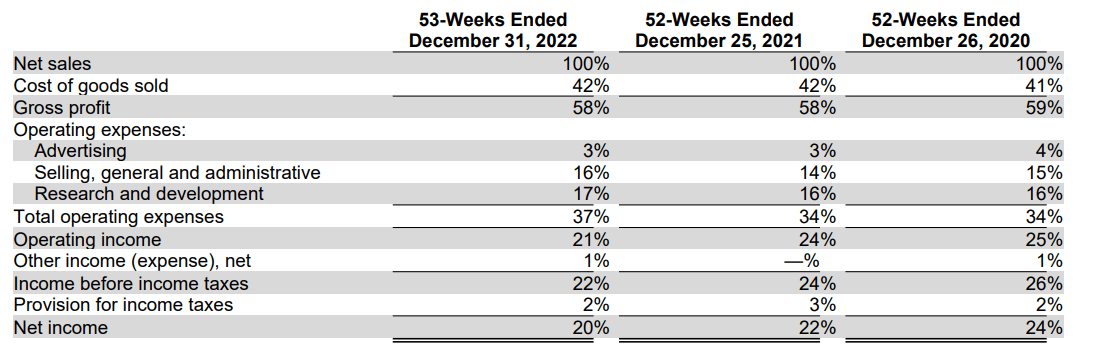

A key attribute that distinguishes the business in the industry, has been its operational efficiency and profitability. Holding a stable 42% gross margin indicates pricing power, while the 21% operating income speaks to the efficiency of running Garmin, a company that is familiar to millions of consumers around the world, yet it spends so little on advertising (3% of revenue). A 20% net margin, although somewhat decreased from the past couple of years is still rather impressive.

Garmin 10K – 2022

When it comes to assessing balance sheet strength we should note that Garmin holds virtually no debt and a sizable cash stockpile of $1.4B. Current and quick ratios of 3.13x and 1.83x also indicate very strong liquidity.

Q3 Results and Beyond

Garmin delivered overall strong results in Q3 2023, signaling that the break in growth for the 2022 fiscal year has been interrupted. Quarterly revenue grew 12% YoY, reaching $1.28B, while operating profits increased by 13% at $270M. The fitness segment remains the fastest growing, with quarterly revenue increasing by 26% YoY. The marine segment, however, recorded a 7% YoY decline for Q3 and is expected to remain flat for the entire year. Both operating and gross margins remained at high levels, with GAAP EPS increasing by 23% YoY.

For the next few years, analysts expect moderate growth in both revenue and EPS. Management’s guidance looks for $5.15B in revenue for 2023, while analysts are slightly more optimistic. Beyond that point, sales are expected to grow at high single digits, reaching $6.61B for the 2026 fiscal year, while EPS is forecasted at $7.53 per share in 2026, increasing at mid-single-digit rates in the mid-term.

Dividends to Boost Returns

Garmin’s profitability and cash flow production have allowed the company to pay a growing 2.33% dividend yield. GRMN’s dividends have grown at a 6.82% 5-year CAGR, as the company maintains a 56% payout ratio. Overall, Garmin can also be considered as potential a secondary addition to a dividend growth portfolio.

A High-Level Cash Flow Valuation Viewpoint

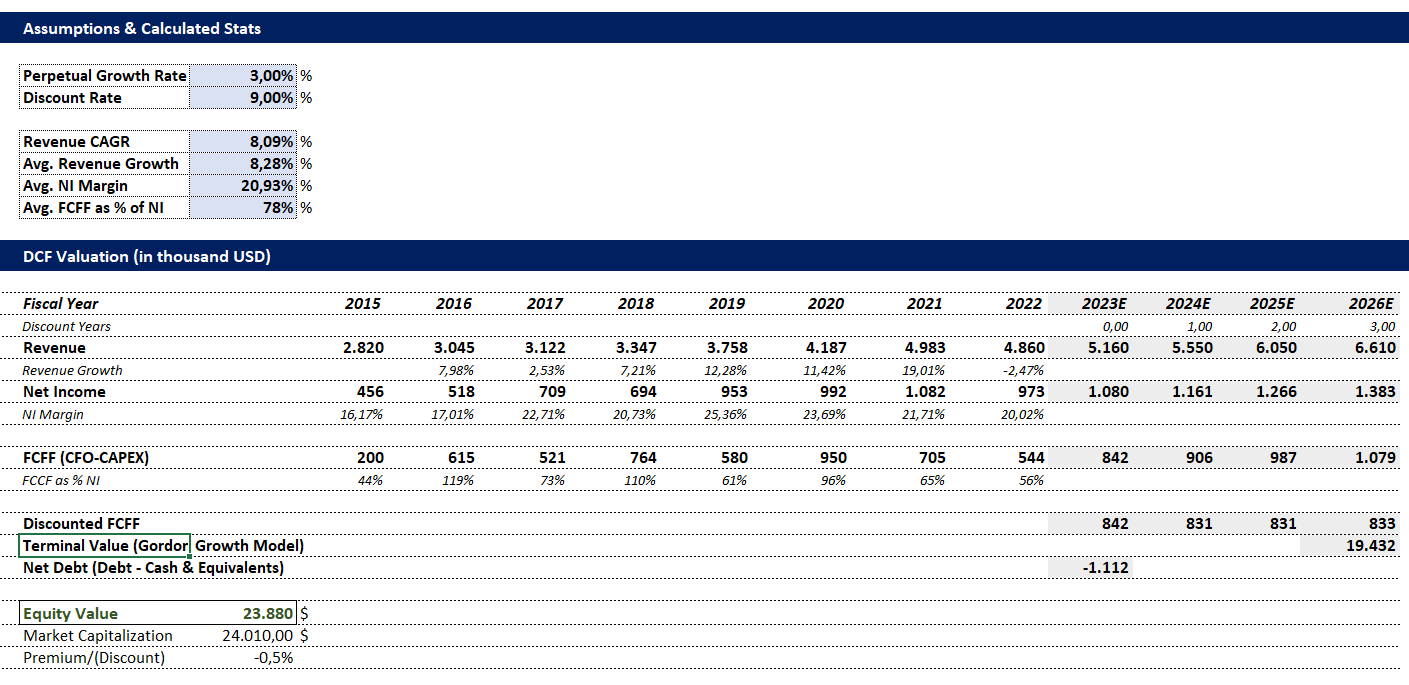

Considering that after decades of revenue growth and profitable operations, Garmin can be viewed as an established business with a long-term horizon ahead, a discounted cash flow valuation overview, can be helpful to provide a general outlook on the stock’s current valuation. Under some general assumptions for the perpetual growth and discount rates (consistent with broader industry expectations), a high-level DCF valuation of Garmin is provided in this segment.

Using analysts’ expectations regarding revenue growth over the next four years and the average net margin of 20.93% (2015-2022) Net Income was forecasted for the 2024-2026 period. As the company’s FCFF stands, on average at 78% of net income, Gamin should be expected to generate $842M of FCFF for the current fiscal year, increasing gradually to $1.08B in 2026. After that, using a perpetual growth rate of 3.0% and a discount rate of 9.0% the terminal value was calculated.

Discounting both the near-term expected cash flows and the terminal value, and also adjusting for Net Debt (which is negative due to very low leverage) to obtain equity value, an intrinsic $23.88B equity valuation is reached. Compared to the current market cap of $24.01B, this indicates that Garmin is currently fairly valued.

SA, Author’s Research

While a high-level DCF valuation like the one presented above can’t be held to high accuracy standards as many assumptions are subject to change, it still offers a broader outlook for the stock, which currently seems to be reasonably valued.

Despite the DCF value seeming on par with the stock’s current market capitalization, it is reasonable for value investors to seek a valuation discount of around 10% or even 20% to consider a stock particularly attractive, primarily due to the subjectivity and unpredictability of some input assumptions used in the model.

Different Valuation Indicators

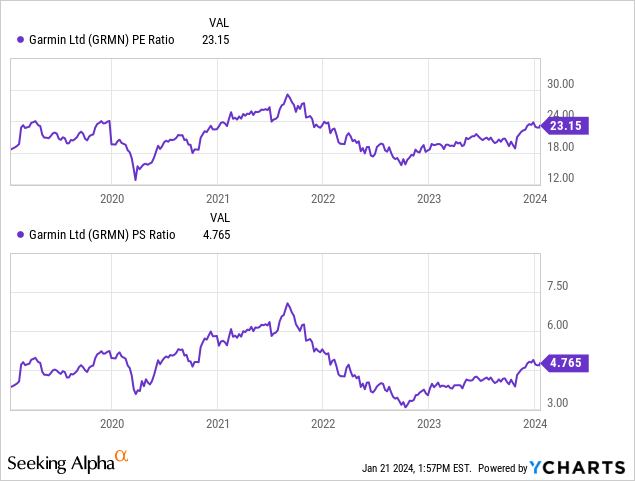

Even though a cash flow valuation can be a good overall proxy for a stock’s intrinsic value, a different viewpoint, regarding the GRMN’s valuation multiples is also warranted.

On that front, Garmin trades at a 23.15x P/E and a 4.77x P/S sales, with both generally considered pricey compared to the respective consumer discretionary sector averages of 14x and 0.9x. One thing to note, especially regarding the P/S ratio, is that given the company’s strong bottom-line profitability, the multiple actually overstates the stock’s “pricey-ness”, which is arguably not too extreme.

Compared to Garmin’s own P/S and P/S 5-year averages both multiples fall within the historic range, despite being slightly above their running averages.

Considering additional valuation metrics, GRMN trades at a 17.9x EV/EBITDA and a 2.8x P/B multiple.

Final Thoughts

After all things are considered, Garmin is a company financially set for the future. Strong profitability and a very healthy balance sheet complement a proven business model that provides consumers with a world-famous range of devices. The only caveat at this moment is obviously GRMN’s valuation, which many investors would like to see become less expensive before securing any noticeable long positions. Sharing that though, I would assign Garmin a reluctant Buy rating, for the time being.

Q2 2024 Earnings Call Transcript")