tifonimages

Overview

Freeport-McMoRan (NYSE:FCX) is one the largest copper mining companies in the world and it is very focused on copper specifically while many larger mining companies often have a more diversified production profile between base metals.

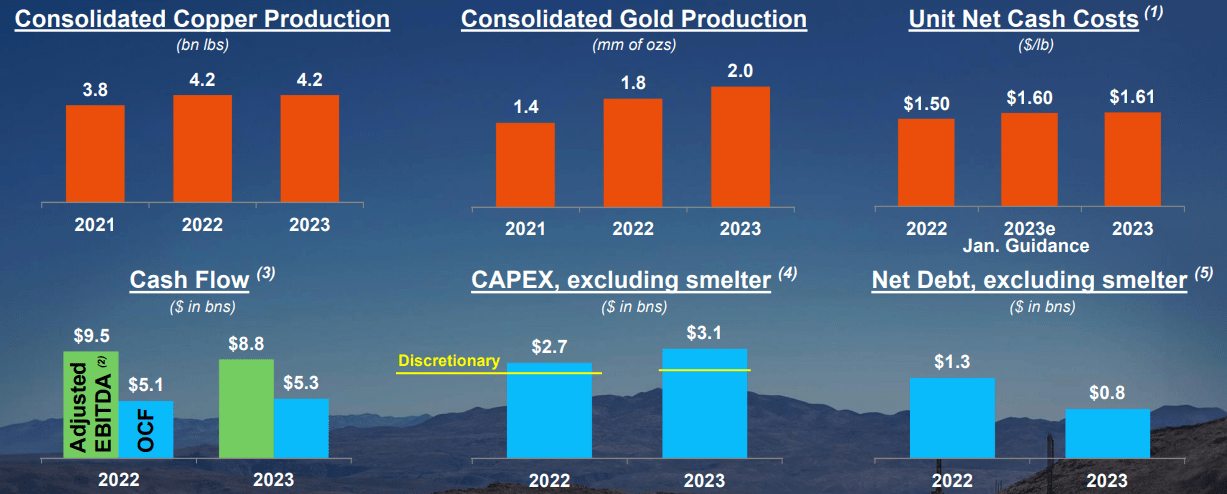

Figure 1 – Source: FCX Q4-23 Presentation

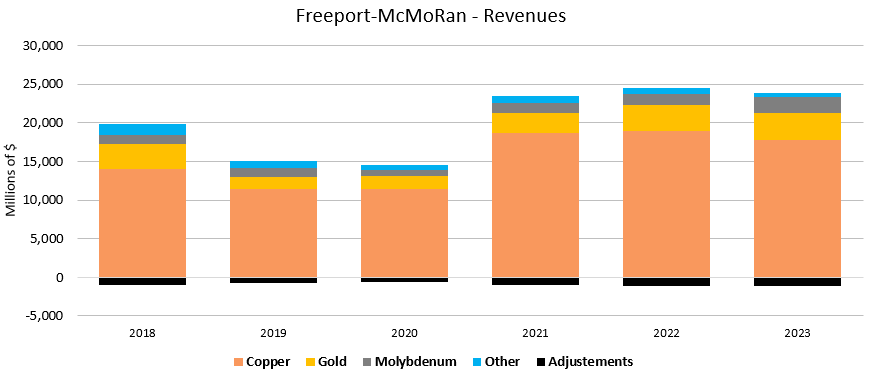

Figure 2 – Source: FCX 10Ks

Copper revenues have over the last few years been around 75-80% of total revenues for FCX, the company also has material amounts of gold and molybdenum (“moly”) sales.

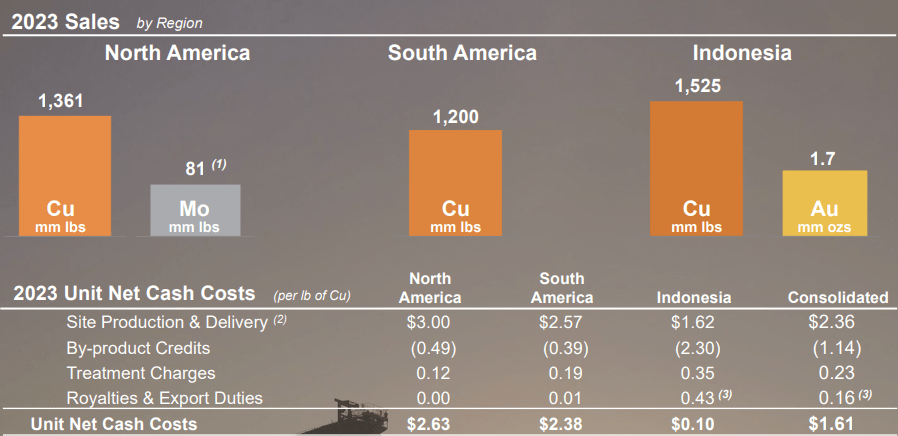

While FCX is more concentrated with its commodity exposure, it is relatively well diversified between North America, South America, and Indonesia when it comes to copper production.

Figure 3 – Source: FCX Q4-23 Presentation

With that said, even if production is relatively diversified, the costs are so low in Indonesia that the majority of operating income has come from there lately. In 2023, as much as 76% of operating income came from Indonesia.

So, in the current copper price environment, FCX is relatively concentrated geographically as well. However, if we do envision a higher copper price environment, which I suspect many that invest in FCX do, the geographical contribution to operating income will be more diversified.

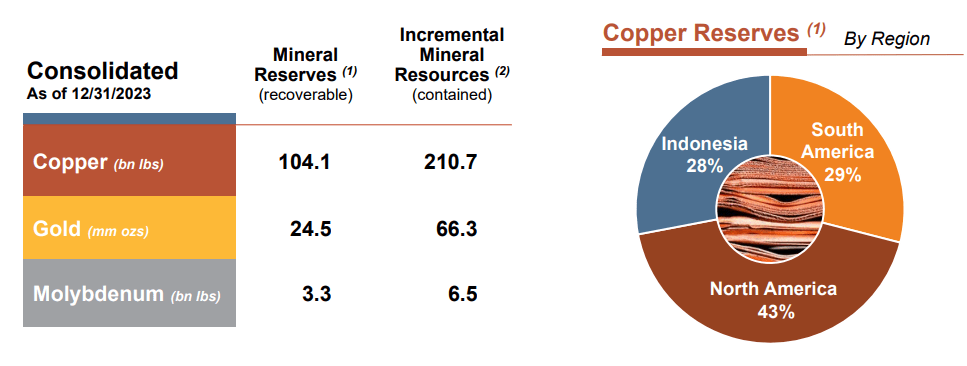

The company also has very substantial copper reserves of 104.1Blbs on a consolidated level between the regions, which is enough to support current operation for about 25 years. There is also a very large amount of copper resources on top of that.

Figure 4 – Source: FCX Q4-23 Presentation

Financials

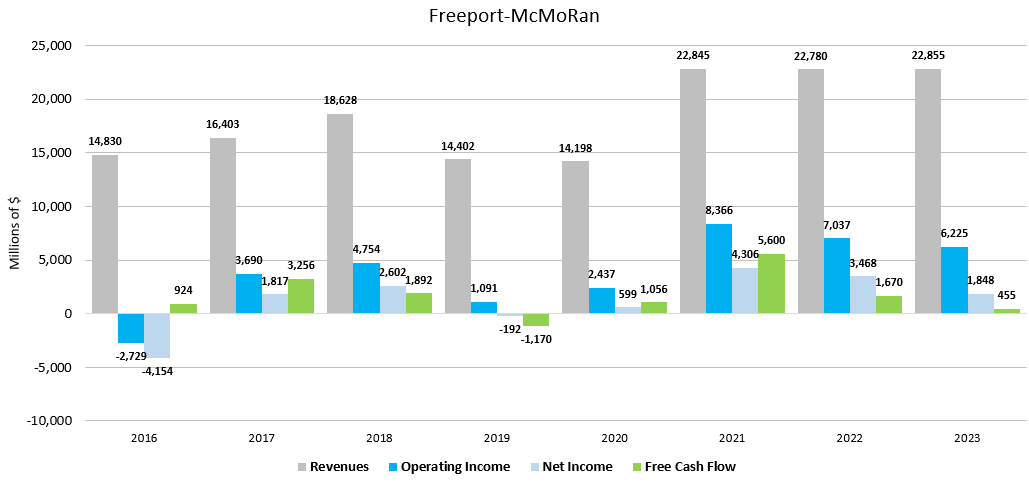

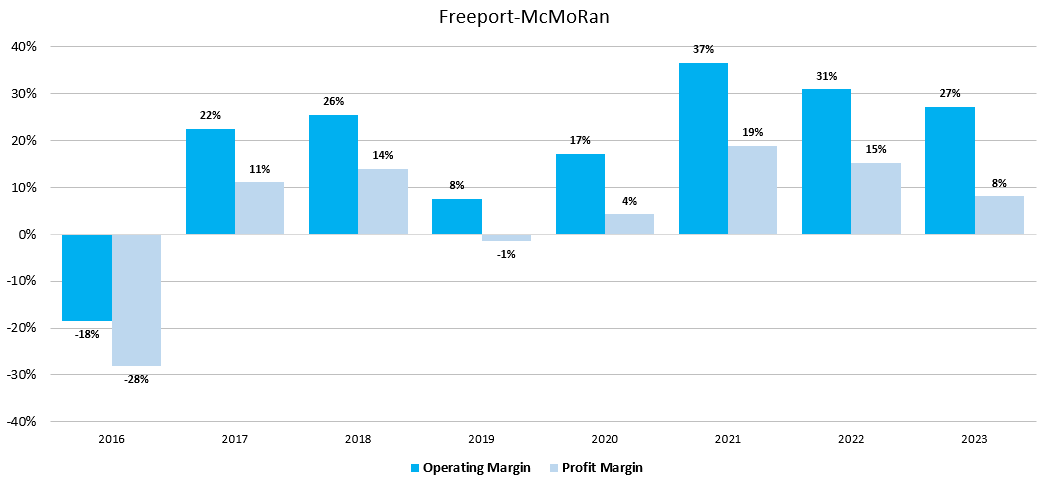

FCX has performed well operationally lately, which has led to strong financial results. Total revenues have been around $23B over the last 3 years and we have seen a very healthy operating margin of around 30% during that period. The company has, despite some rather substantial capital investments, had a positive free cash flow in 7 out of the last 8 years.

Figure 5 – Source: FCX 10Ks

Figure 6 – Source: FCX 10Ks

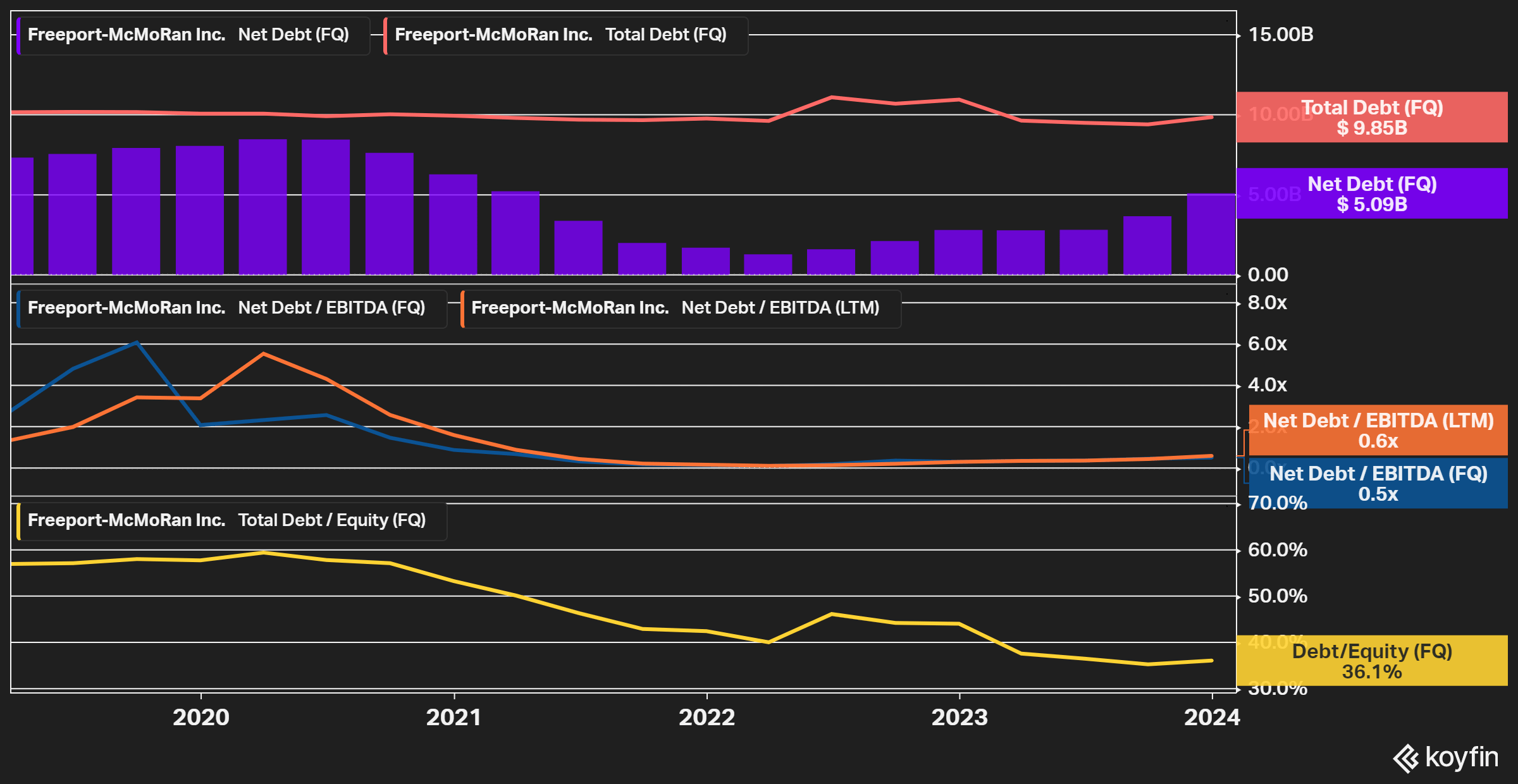

The good financial results have allowed the company to deleverage, where the net debt has gone from over $8B 4 years ago to around $5B now. The net debt to last twelve months’ EBITDA is a very manageable 0.6 and the debt-to-equity ratio is at 0.36.

Figure 7 – Source: Koyfin

Over the last few years, the company has made some minor buybacks and pays a quarterly base and variable dividend. The dividend is estimated to be $0.60 per share in 2024, which equates to a dividend yield of 1.3% using the latest share price.

Guidance & Valuation

FCX has provided sales guidance for the next few years, copper sales are expected to go from 4.1Blbs in 2023 to 4.3Blbs in 2026. So, we are looking at a relatively modest increase in copper sales from 2023 to 2026. The moly sales are expected to increase by 11% and gold sales are expected to decrease by 12% using the same period.

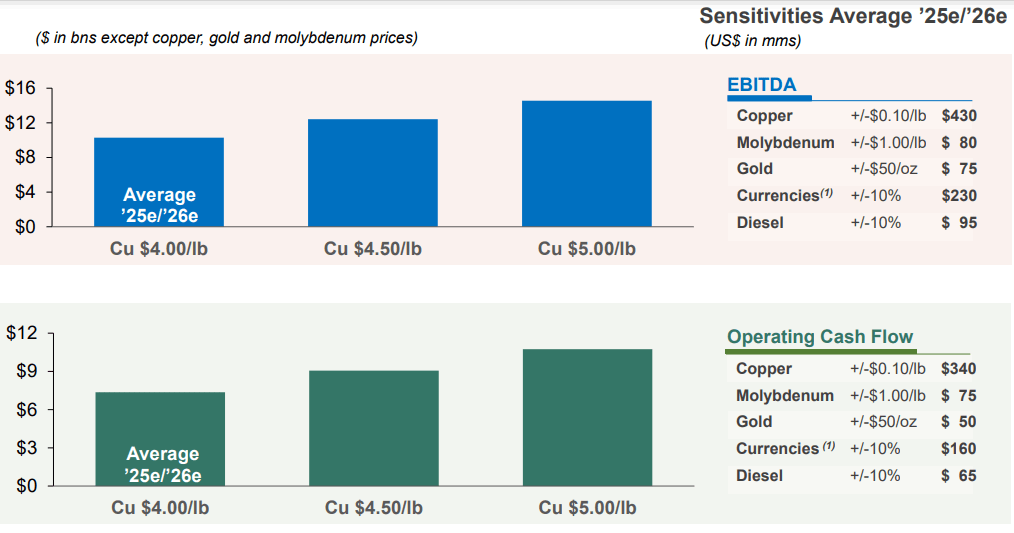

Figure 8 – Source: FCX Q4-23 Presentation

The above figure illustrates the sensitivity to various commodity prices during 2025-2026, where the company is expected to generate an operating cash flow around $7.5B with a copper price of $4.0/lb. If we subtract the 2025 capex guidance figure of 3.8B, we are talking about a free cash flow of $3.7B, which translates to a free cash flow yield of around 5%, using the enterprise value. The free cash flow yield increases to about 10%, with a copper price of $5/lb.

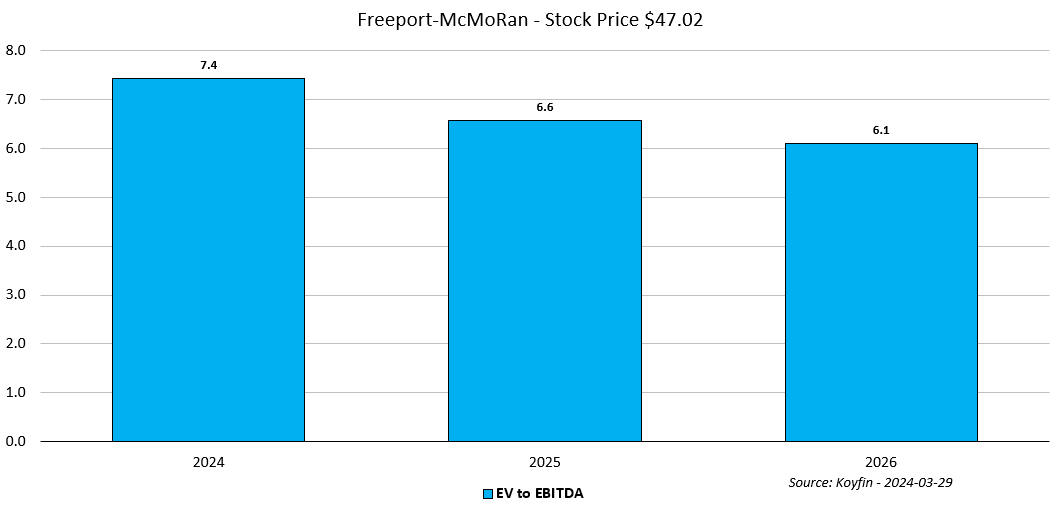

If we use the latest estimates from Koyfin, the EV to EBITDA isn’t overly attractive at 7.4 for 2024, but the valuation multiple is expected to improve in the coming years. The copper price has been relatively strong over the last month, but we haven’t seen many upward revisions to estimated EBITDA recently. So, if the current copper price persists or increases going forward, the estimates used in the chart below could slightly be conservative.

Figure 9 – Source: Koyfin

Conclusion

Freeport-McMoRan is a large high-margin copper producer, which has had a strong performance lately as we have seen the price of copper improve.

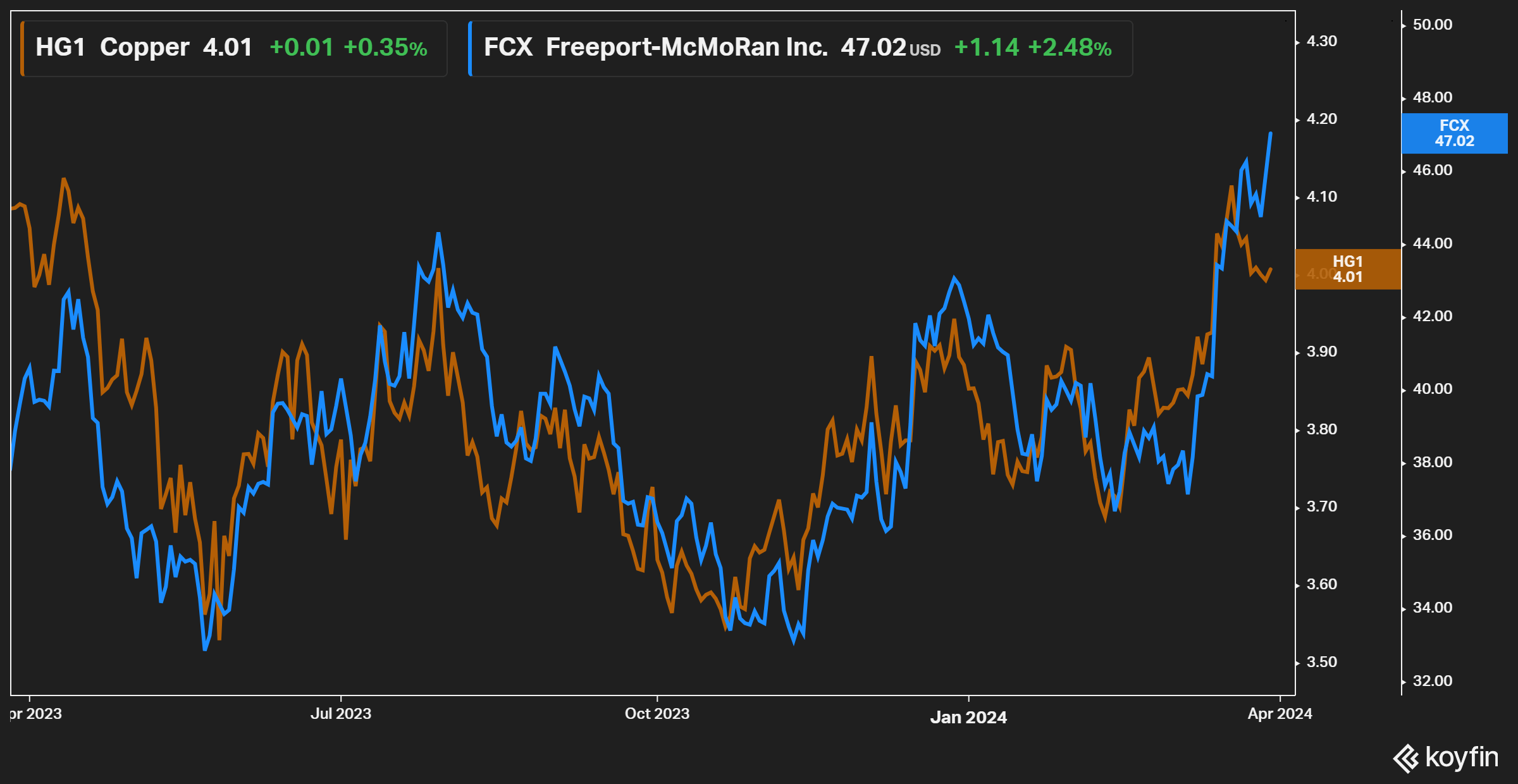

Figure 10 – Source: Koyfin

The valuation for FCX is relatively attractive if we look a couple of years out and assume a copper price in the $4-5/lb range, which I don’t think is an overly aggressive price assumption in the medium term. However, at the current copper price and based on production and margins in 2024, I do think FCX is more fairly valued.

So, I am neutral on the stock here and would need to see a significant pullback to buy the stock. However, it is worth keeping in mind that FCX is relatively unique in its size, good margin, and concentrated exposure to copper production. So, if the copper mining industry catches more of generalist’s interest, I do think FCX is very likely to attract investment flows and do well.

One concern with FCX is the large exposure to Indonesia, which makes the company more impacted by local geopolitical risk considerations. The company has, however, managed local challenges well over time. Also, the superior grades and low operating costs at the Grasberg minerals district in Indonesia is what allows the company to stay profitable even during more adverse copper price environments.

Q2 2024 Earnings Call Transcript")