Perry Peine/iStock via Getty Images

Office REITs are in a battle for their lives, and their investors are faced with a conundrum in picking the winners in an increasingly Darwinistic space. The headwinds are clear; a Fed funds rate at a more than two-decade high and rising office vacancies as work-from-home becomes a perpetual feature of the post-pandemic world of work. Rolling layoffs have also afflicted US corporates as they come to terms with more expensive debt and the specter of a recession. These three factors have aggregated to form the perfect storm of headwinds for office REITs like Franklin Street Properties (NYSE:FSP). The $260 million REIT is the owner of Class B office properties across six states but with a concentration on Texas and Denver, Colorado.

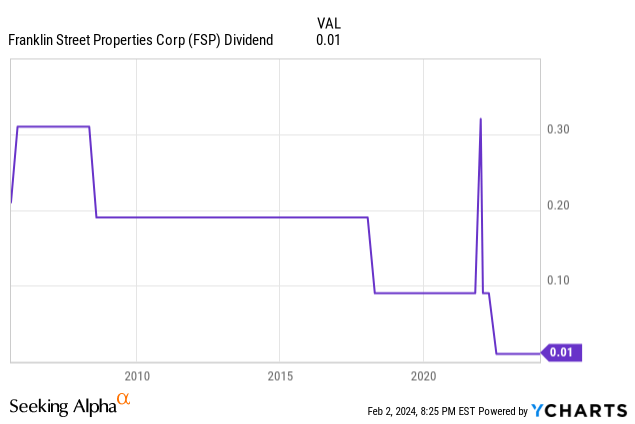

FSP is not an income play, the REIT last paid out a peppercorn $0.01 per share dividend, left unchanged sequentially and $0.04 annualized for a 1.7% forward dividend yield. Critically, the quarterly distribution was dipping even before the pandemic ushered in a brutal zeitgeist for office REITs. A dividend high of $0.31 per share in 2008 first dipped to $0.09 per share in 2018 and now sits at its lowest-ever level since FSP went public. The REIT represents a play on a possible reversion to a higher pre-pandemic valuation mean.

CME FedWatch Tool

Whilst a full reversion is unlikely with hybrid working set to become a perpetual part of US corporate working life, currently high-interest rates are abnormal for the level of debt in the economy. They will have to eventually come back down and 150 basis points worth of cuts forms the current market’s expectations for 2024 with the CME FedWatch Tool placing a 3.75% to 4.00% Fed funds rate as the most likely figure exiting 2024.

Revenue And Closing The Discount

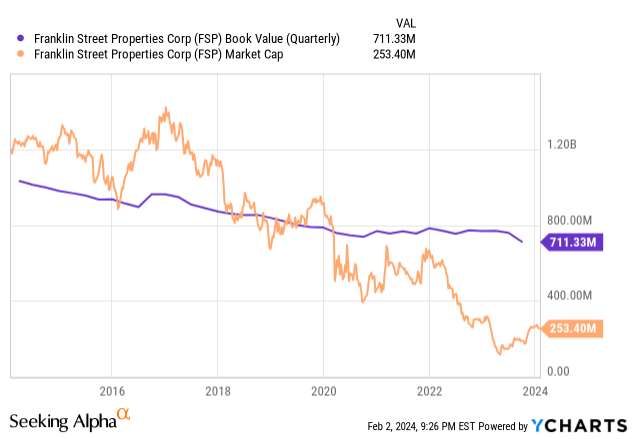

FSP’s book value came in at $711 million, around $6.88 per share, at the end of its fiscal 2023 third quarter. Book value per share dipped 60 cents versus its year-ago comp, with the figure under perpetual pressure for the last decade. However, the current gap between this figure and its market cap is at its greatest ever distance. To be clear, FSP simply closing this discount would mean a 180% upside on commons, currently trading for $2.46 per share. However, book value becomes a partially impaired metric against what’s currently a national office vacancy rate at a record 19.8%. Office sales are being completed at discounts.

Franklin Street Properties Fiscal 2023 Third Quarter Form 10-Q

FSP recorded total revenue of $36.9 million during its third quarter, down by $4 million from its year-ago comp but a small $510,000 beat on consensus estimates. GAAP net loss for the quarter at $45.68 million was a material deterioration from a year ago on the back of total expenses that were ahead of revenue by roughly $6 million. FSP also realized a $39.67 million loss on the sale of properties and impairment on held-for-sale assets.

Franklin Street Properties Fiscal 2023 Third Quarter Form 10-Q

The REIT reiterated during its earnings call that they’ll selectively chase dispositions to realize value from their properties. FSP’s portfolio consisted of 19 owned properties and a non-controlling stake in a consolidated REIT FSP Monument Circle. Both of these were spread across 6,206,460 rentable square feet and were down from 22 properties in the year-ago comp.

FFO Multiple, Debt Maturities, And Balance Sheet Health

FSP generated a third-quarter FFO of $0.07 per share, around $0.28 per share annualized. This means it’s currently trading at an 8.8x multiple to its annualized third-quarter FFO. Whilst low, there are other office REITs like Brandywine Realty (BDN) trading at a lower 4x multiple to FFO and offering a more substantive 13.6% dividend yield.

Franklin Street Properties Fiscal 2023 Third Quarter Supplemental

FSP held $73.5 million in cash and cash equivalents on its balance sheet as of the release of its earnings report. This is against what’s set to be $311 million of debt maturing this year. The REIT will have to continue to downsize its portfolio to address this upcoming wall of debt maturities, which will mean further pressure on revenue. Critically, FSP’s portfolio was only 74.8% leased at the end of the third quarter, down 80 basis points from 75.6% at the start of the fiscal year. This dip is set to continue when overlayed with what’s set to be continued revenue dips, GAAP net losses, and an extremely unfavorable debt maturity profile. FSP is also still expensive versus its other highly discombobulated peers. The lack of a dividend also adds to the conundrum. Hence, I’m rating FSP as a sell here, with the REIT set for more asset disposals at losses as it rushes to address debt above all else. I don’t think its maturities are an existential risk, though, but there could be more downside.

Q2 2024 Earnings Call Transcript")