paulbranding

Forward Air Corp. (NASDAQ:FWRD) has recently become an even larger conglomerate with its acquisition of Omni Logistics. In general, this may be seen as a good sign for company growth, but concerns have arisen regarding the large debt required to finance the merger and the loss of ownership control for Forward Air shareholders. While the skepticism of this merger is high, the company should generate some potential synergies for this merger. Economies of scale and increased service offerings to customers should generate growth as well as savings long-term if integrated well. Whether these synergies will outpace the cost of the acquisition remains to be seen and does pose a risk long term to the company’s balance sheet.

Growth has seen a recent decline compared to 2022 for Forward Air. This can be attributed not only to supply chain issues due to the geopolitical environment but also to reduced consumer spending that has an impact on shipping needs for retailers and e-commerce companies. Operating expenses have increased as the company has grown, which is to be expected for a logistics company such as itself. As the economy continues to grow, I expect a rebound in Forward Air’s top-line financials as demand for delivered products continues to rise.

When considering these current stories about Forward Air, we need to determine which news topics will have a long-term and ongoing effect on the company and its share price. Forward Air is still positioned well to take advantage of its large-scale and leading execution service within the LTL industry. The stock has seen a recent downward trend due to global political instability and declining revenues. Global political instability in the Red Sea is hard to forecast for improvement but the truckload weight should rebound in 2024 as the need for logistics increases as the economy continues to expand. On the balance sheet, Forward Air did take on massive debt to acquire Omni Logistics. This does pose a risk long term, especially if the synergies mentioned do not pan out or if any complications arise from the integration of these two companies. If the companies successfully merge and take advantage of economies of scale the stock could be positioned to finally return greater value to shareholders moving forward.

While current news stories, good or bad can sway our opinion about investing in a company, it’s good to analyze the fundamentals of the company and to see where it’s been in the past and in which direction it’s heading.

This article will focus on the long-term fundamentals of the company, which tend to give us a better picture of the company as a viable investment. I also analyze the value of the company versus the price and help you to determine if Forward Air is currently trading at a bargain price. I provide various situations which help estimate the company’s future returns. In closing, I will tell you my personal opinion about whether I’m interested in taking a position in this company and why.

Snapshot of the Company

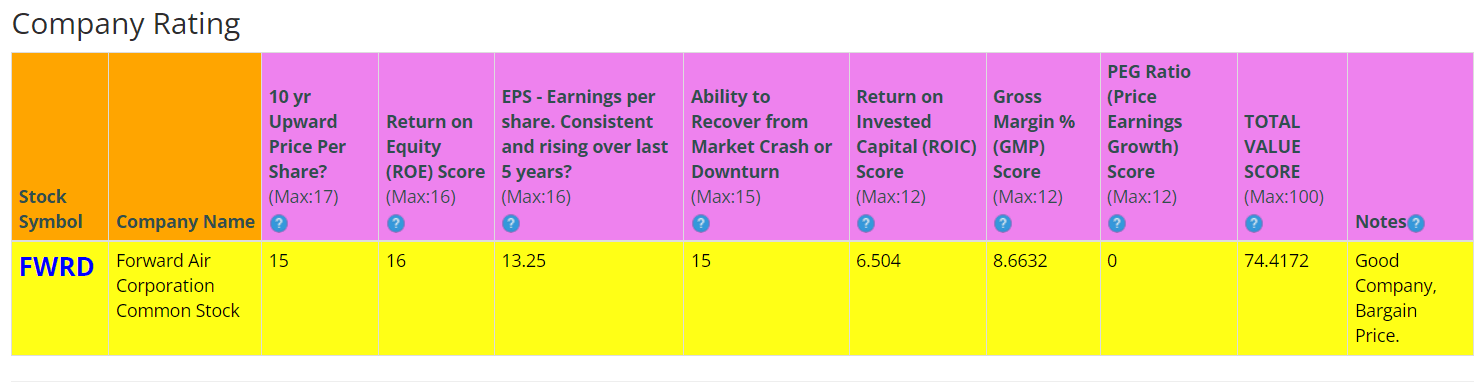

A fast way for me to get an overall understanding of the condition of the business is to use the BTMA Stock Analyzer’s company rating score. Forward Air shows a rating score of 74.4 out of 100. In summary, Forward Air has strong fundamentals with some concerns in the ROIC and Gross Margin categories.

Before jumping to conclusions, we’ll have to look closer into individual categories to see what’s going on.

BTMA Stock Analyzer

(Source: BTMA Stock Analyzer )

Fundamentals

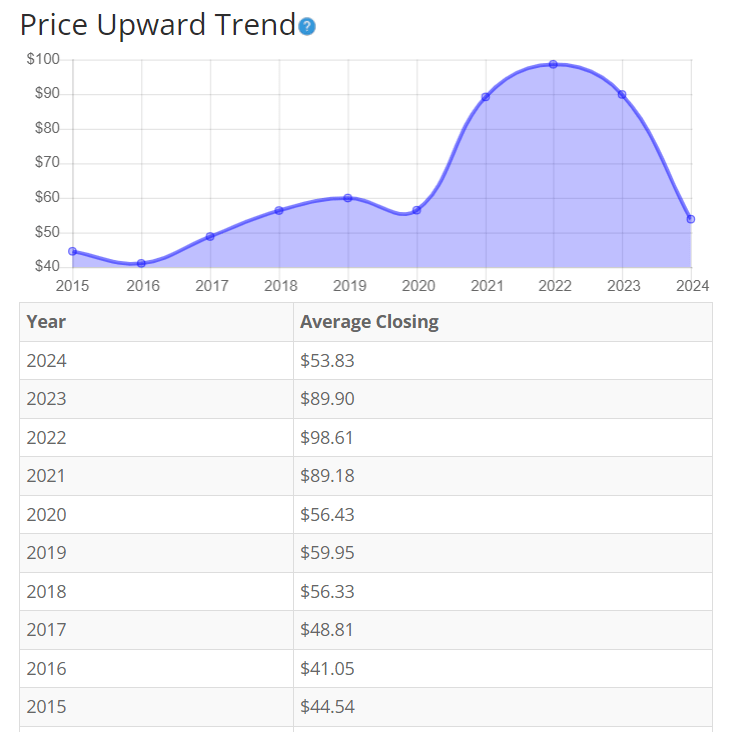

The share price has been in decline since 2022 highs. Much of this decline has been from the negative reaction to its announced merger with Omni Logistics. Combine that negative press with the global instability through the Red Sea and consumer spending declines and the reason for a stock price decline becomes clear. The current revenue generated in 2023 is lower compared to its best year in 2022. Overall, the share price average has grown by about 20.9% over the past 10 years, or a Compound Annual Growth Rate of 2.12%. At today’s stock price, Forward Air is trading near a 10-year low.

BTMA Stock Analyzer

(Source: BTMA Stock Analyzer – Price Per Share History)

Earnings

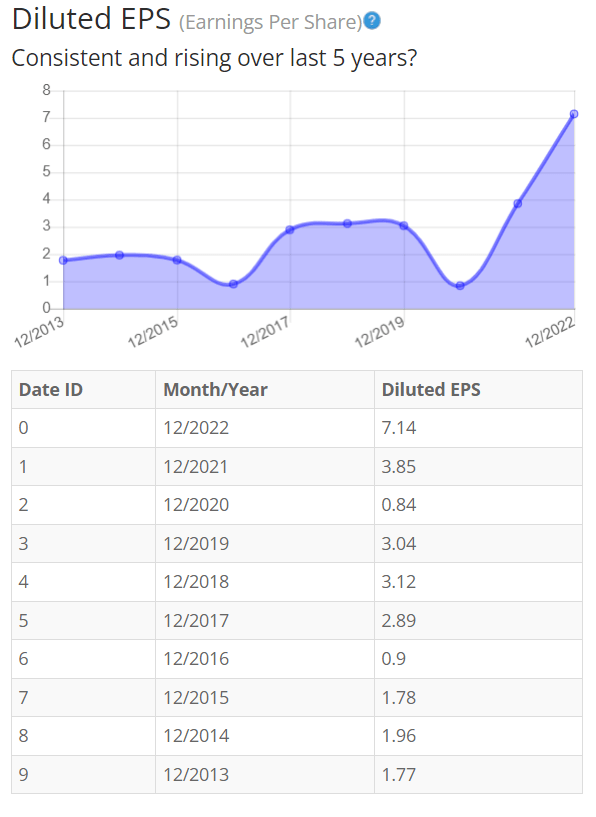

Earnings were relatively static until the large rise in 2022 due to increased prices for logistics travel due to supply chain shortages. I expect earnings to show a declining trend like the price per share due to declining revenue in the recent year of 2023. As the merger begins to integrate and economies of scale are taken advantage of, I could see a major rebound in earnings per share.

BTMA Stock Analyzer

(Source: BTMA Stock Analyzer – EPS History)

Since earnings and price per share don’t always give the whole picture, it’s good to look at other factors like the gross margins, return on equity, and return on invested capital.

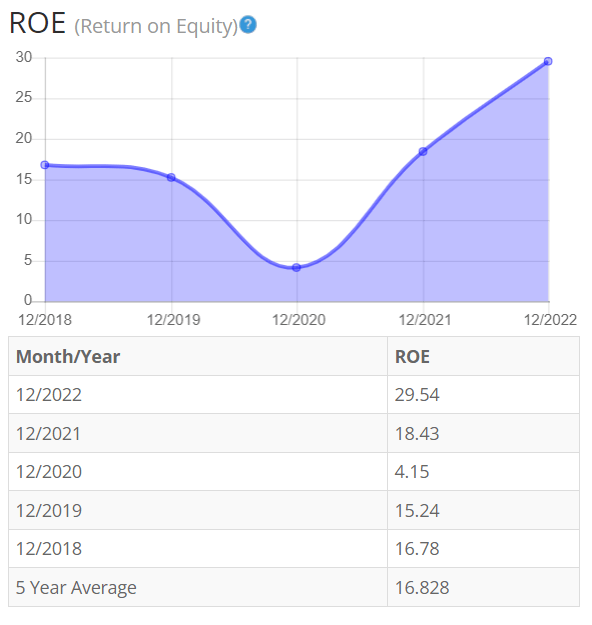

Return on Equity

The return on equity has followed the trend of earnings due to a large increase in revenue in 2022. In the short term, I expect a similar ROE decline due to all the macro factors stated earlier impacting the company’s performance. I will note an outlier year in 2020 most likely saw a large decline due to COVID-19. If we remove that year the company does show a very steady return on equity even for changing economic conditions. For return on equity (ROE), I look for a 5-year average of 16% or more. So, Forward Air exceeds this requirement.

BTMA Stock Analyzer

(Source: BTMA Stock Analyzer – ROE History)

Let’s compare the ROE of this company to its industry. The average ROE of 110 transportation companies is 22.06%.

Therefore, Forward Air’s 5-year average of 16.8% is below its peers. Although in 2022 they have exceeded this metric.

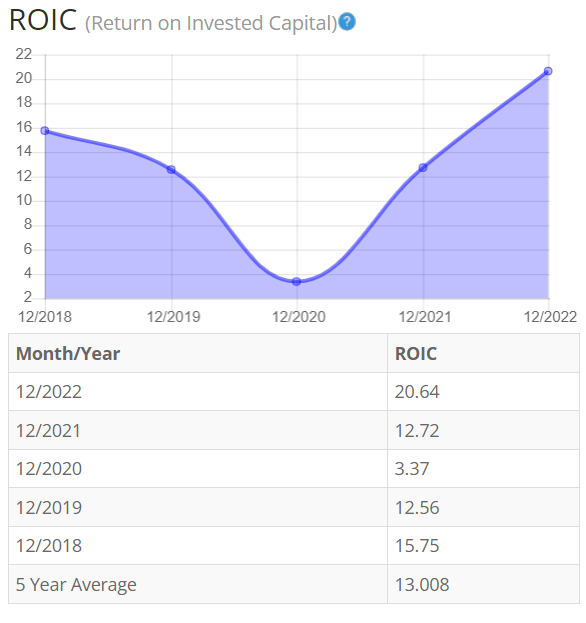

Return on Invested Capital

The return on invested capital saw a sharp rise in 2022 like previous charts. The company has increased capital expenditure after 2020 and has maintained that level for the past three years. At least for 2021 and 2022 the company returned greater if not similar levels to previous returns before COVID. This is a very good metric for a logistics company that must maintain its competitive advantage through continued investment back into the business. I again expect a slight decline in 2023 and beyond due to short-term impacts on the growth side. For return on invested capital (ROIC), I also look for a 5-year average of 16% or more. So, Forward Air does not exceed this but would if we removed the outlier year.

BTMA Stock Analyzer

(Source: BTMA Stock Analyzer – Return on Invested Capital History)

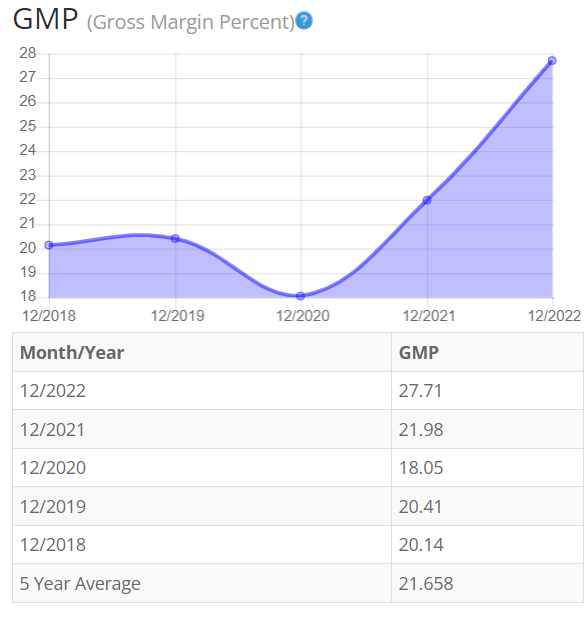

Gross Margin Percent

The gross margin percentage (GMP) has remained stable over the last 5 years. Even during COVID, Forward Air maintained a healthy margin for its business. I anticipate the surge seen in 2022 will most likely reduce to its nominal levels in 2023 and beyond. As economies of scale are leveraged after the merger, we should see gross margin improvement or at least operation cost improvement. If no cost reductions are realized, merger integration would be considered a struggle for the company. I typically look for companies with a gross margin percent consistently above 30%. So, Forward Air is below this criterion.

BTMA Stock Analyzer

(Source: BTMA Stock Analyzer – Gross Margin Percent History)

Financial Stability

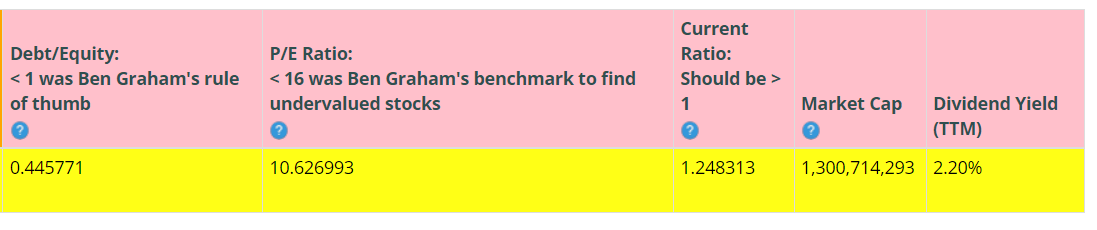

Looking at other fundamentals involving the balance sheet, we can see that the debt-to-equity is less than one. This is a good level for debt to equity. Keep in mind that this current value does not consider the recent debt load taken on due to the merger.

Forward Air’s Current Ratio of 1.28 indicates it can pay off short-term debt with its current assets.

Ideally, we’d want to see a Current Ratio of more than 1, so Forward Air exceeds this amount.

Forward Air shows a mixed bag when looking at its fundamentals. The company recently took on a large acquisition which is somewhat risky with the amount they paid for Omni Logistics. Revenue has declined and this will directly decline a lot of the fundamentals in 2023 and beyond into 2024. Long term I do think the merger can position this company for long-term growth if they can achieve their synergies and economies of scale.

Forward Air currently pays a dividend of around 2.2%.

BTMA Stock Analyzer

(Source: BTMA Stock Analyzer – Misc. Fundamentals)

This analysis wouldn’t be complete without considering the value of the company vs. share price.

Value Vs. Price

The company’s Price-Earnings Ratio of 10.62 indicates that Forward Air is underpriced when comparing Forward Air’s Ratio to a long-term market average PE Ratio of 15.

The 10-year and 5-year average PE Ratio of FWRD has typically been 24.3 and 23.3, respectively. This also indicates that FWRD could be currently trading at a low price when comparing to its average historical PE Ratio range.

BTMA Stock Analyzer

(Source: BTMA Stock Analyzer – Stock Value)

The Estimated Value of the Stock is $84.74, versus the current stock price of $43.49. This indicates that Forward Air is currently selling below its value.

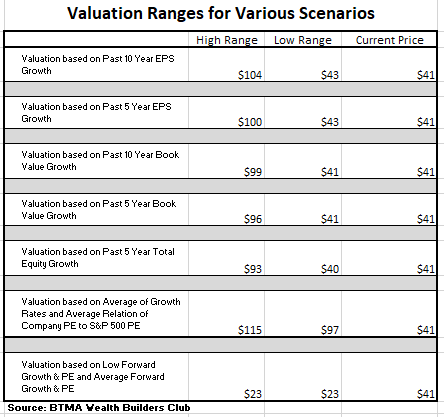

For more detailed valuation purposes, I will be using a conservative diluted EPS of 3.85. I’ve used various past averages of growth rates and PE Ratios to calculate different scenarios of valuation ranges from low to average values. The valuations compare growth rates of EPS, Book Value, and Total Equity.

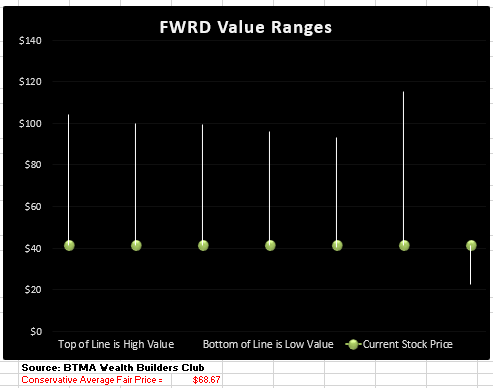

In the table below, you can see the different scenarios, and in the chart, you will see vertical valuation lines that correspond to the table valuation ranges. The dots on the lines represent the current stock price. If the dot is towards the bottom of the valuation range, this would indicate that the stock is undervalued. If the dot is near the top of the valuation line, this would show an overvalued stock.

BTMA Wealth Builders Club

BTMA Wealth Builders Club

(Source: BTMA Wealth Builders Club )

According to this valuation analysis, FWRD is undervalued according to all categories except the last category (Valuation Based on Low and Average Forward Growth & PE).

This analysis shows an average valuation of around $68.67 per share versus its current price of about $41. This again indicates that FWRD is significantly undervalued.

Summarizing the Fundamentals

After analyzing the fundamentals of Forward Air, I believe this company has a solid chance to capitalize on its recent merger long-term. Overall, the fundamentals (EPS, ROE, ROIC, Gross Margins) are either at a satisfactory level or have been trending towards a satisfactory level. However, these fundamentals could see a decline into 2024 due to declining revenues from the company.

If the synergies of the merger are realized, the growth will have a drastic impact on the stock and fundamentals of the company. The company does retain a healthy ROIC even during economic downturns, proving that Forward Air does have some resilience. I will be looking for gross margin improvements and operating cost improvements as Omni Logistics gets integrated into the company. I would see a high-risk scenario if cost improvements were not realized due to them being the easiest to capture synergistically.

Forward Air Vs. The S&P 500

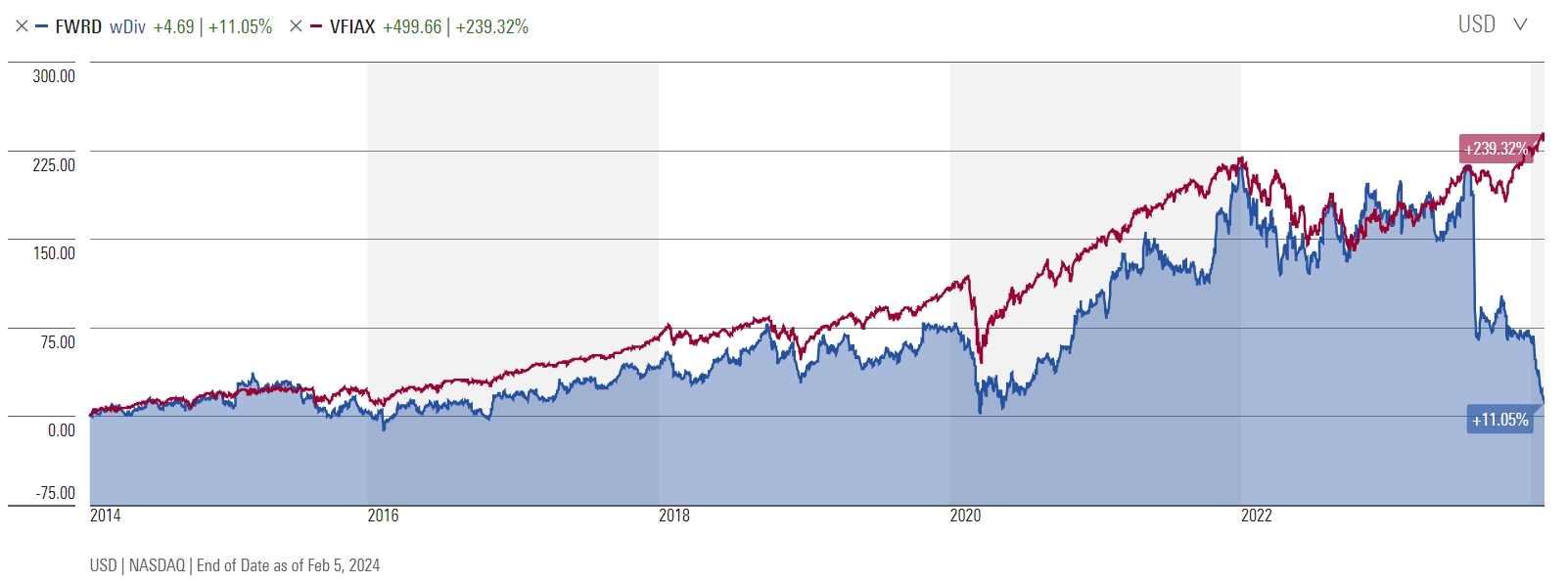

Now, let’s see how Forward Air compares versus the US stock market benchmark S&P 500 over the past 10 years. From the chart below, we can see that Forward Air has not performed greater than the overall market. Although its current return level compared to the market is considerably lower than its previous gaps. This indicates that the stock could be extremely undervalued at this time. The company is also primed for growth as it just recently merged with Omni Logistics.

Therefore, even though Forward Air typically doesn’t outperform the S&P 500, now could be a great opportunity to buy at an ultra-low price and to capitalize on future growth and price gains.

Morningstar

Forward-Looking Conclusion

Over the next five years, the analysts that follow this company are expecting it to grow earnings at an average annual rate of 13.16%.

In addition, the average one-year price target for this stock is $67.50, which is about a 55% increase in a year.

The Expected Annual Compounding Rate of Return is 19.25%.

If you invest today, with analysts’ forecasts, you might expect about 10% (low growth) to 13% (average growth) per year long-term.

Here is an alternative scenario based on FWRD’s past earnings growth. During the past 10 and 5-year periods, the average EPS growth rate was about 5.5% and 8.7%, respectively.

But when considering cash flow growth over the past 10 and 5 years, the average growth has been 12.5% and 9.3%, respectively. Therefore, when considering all of these return possibilities, our average annual return could likely be around 11%.

Does Forward Air Pass My Checklist?

- Company Rating 70+ out of 100? Yes (74.4)

- Share Price Compound Annual Growth Rate > 12%? No (2.12%)

- Earnings history mostly increasing? Yes

- ROE (5-year average 16% or greater)? Yes (16.8%)

- ROIC (5-year average 16% or greater)? No (13%)

- Gross Margin % (5-year average > 30%)? No (21.6%)

- Debt-to-Equity (less than 1)? Yes

- Current Ratio (greater than 1)? Yes

- Outperformed S&P 500 during most of the past 10 years? No

- Do I think this company will continue to successfully sell their same main product/service for the next 10 years? Yes

Forward Air scored 6/10 or 60%. Therefore, Forward Air shows some solid fundamentals but also some risk that should be carefully considered before entering a position.

Is Forward Air currently selling at a bargain price?

- Price Earnings less than 16? Yes (10.6)

- Average Valuation greater than the Current Stock Price? Yes (Value $68.67 >$41 Stock Price)

Forward Air is a mixed bag. Geopolitical headaches, declining revenue, and a large merger dragged down the perception of the company’s overall balance sheet. All these factors have contributed to the price per share decline and risk level of this company in the short and long term. Fundamentals overall tend to show good promise. Most fundamentals are at satisfactory levels or are trending upward.

I believe that the stock has declined not necessarily on just fundamentals. It appears that the stock has been battered in an overly pessimistic nature. This has sunken the share price near a 10-year low. However, almost every valuation indicator shows that this stock is greatly undervalued.

If the recent merger turns out to be mildly successful, this stock could soar and give investors great returns. I don’t see LTL logistics declining anytime soon as e-commerce companies continue to grow. The economies of scale and synergies that Forward Air can achieve will set them up to beat out the fragmented logistics market on price and capture more market share. If the merger is not successful, the company could take further stock losses in the long term, but I believe a short-term recovery is in order due to being oversold.

From my analysis, it seems clear that the stock is greatly undervalued, and the long-term fundamentals are strong enough that I would be willing to take on some of the additional risks and concerns of this company. The stock price might continue to fall lower, but it’s approaching the territory where it really makes sense to take a position in Forward Air and to ride out the storm.

Q2 2024 Earnings Call Transcript")