eyegelb

Just over six weeks ago, I wrote on Fortuna Silver Mines (NYSE:FSM), noting that there was no margin of safety present for the stock which suggested elevated risk in chasing the stock above US$3.80. Since then, Fortuna Silver Mines (“Fortuna”) has suffered a ~20% drawdown, underperforming the Gold Miners Index (GDX) which has got off to a rough start to the year as well. The culprit for the stock’s underperformance is its underwhelming FY2024 guidance, with costs once again expected to come in well above the industry average. Worse, the Mexican Peso has remained under pressure, setting up another difficult year for reserve replacement as its dwindling San Jose Mine (the bulk of its silver exposure).

In this update, we’ll dig into the Q4/FY2023 results, the forward outlook, and where Fortuna’s updated low-risk buy zone lies.

Fortuna Silver Exploration – Company Website

Q4 & FY2023 Production

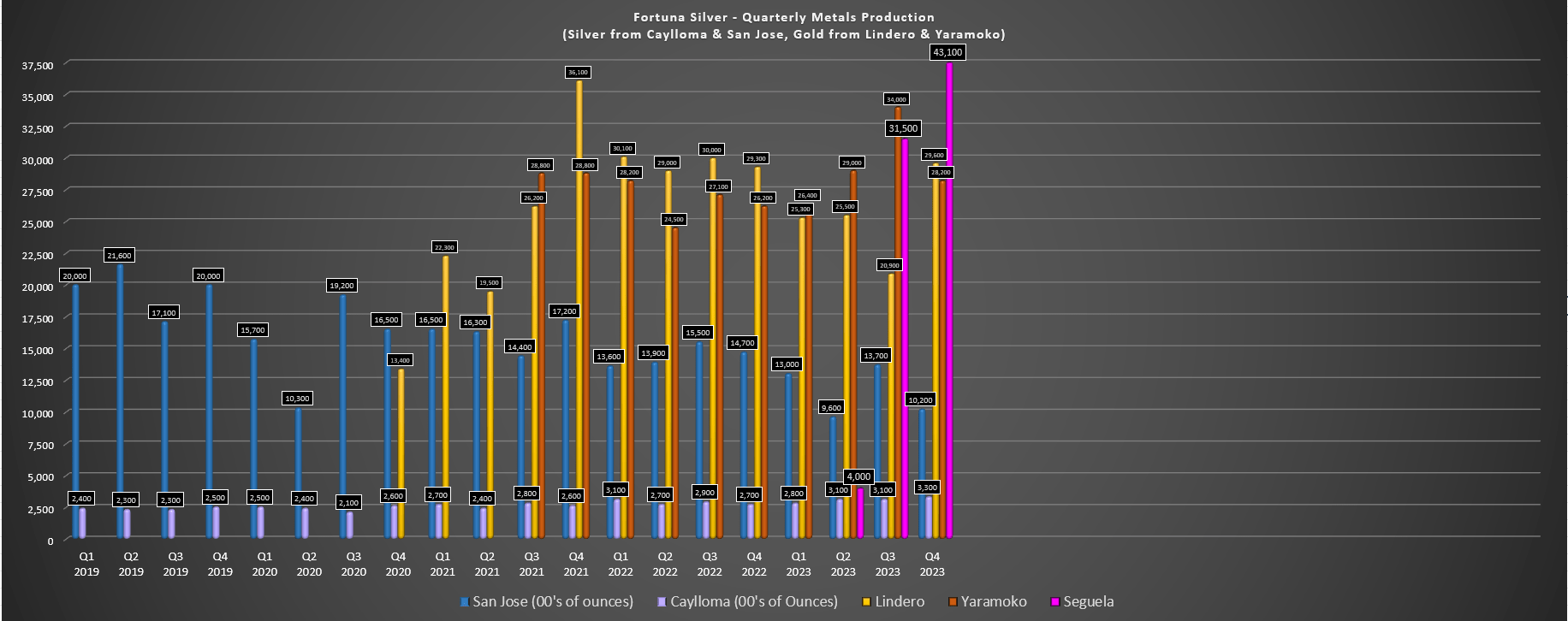

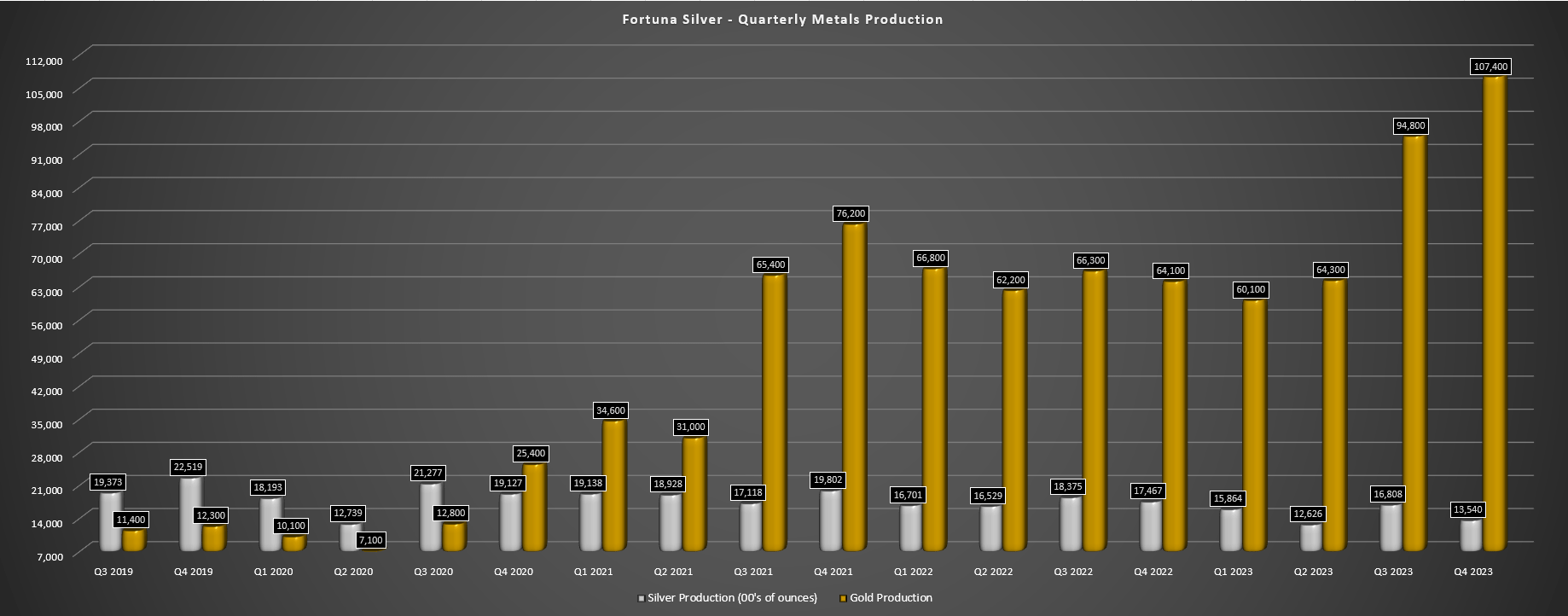

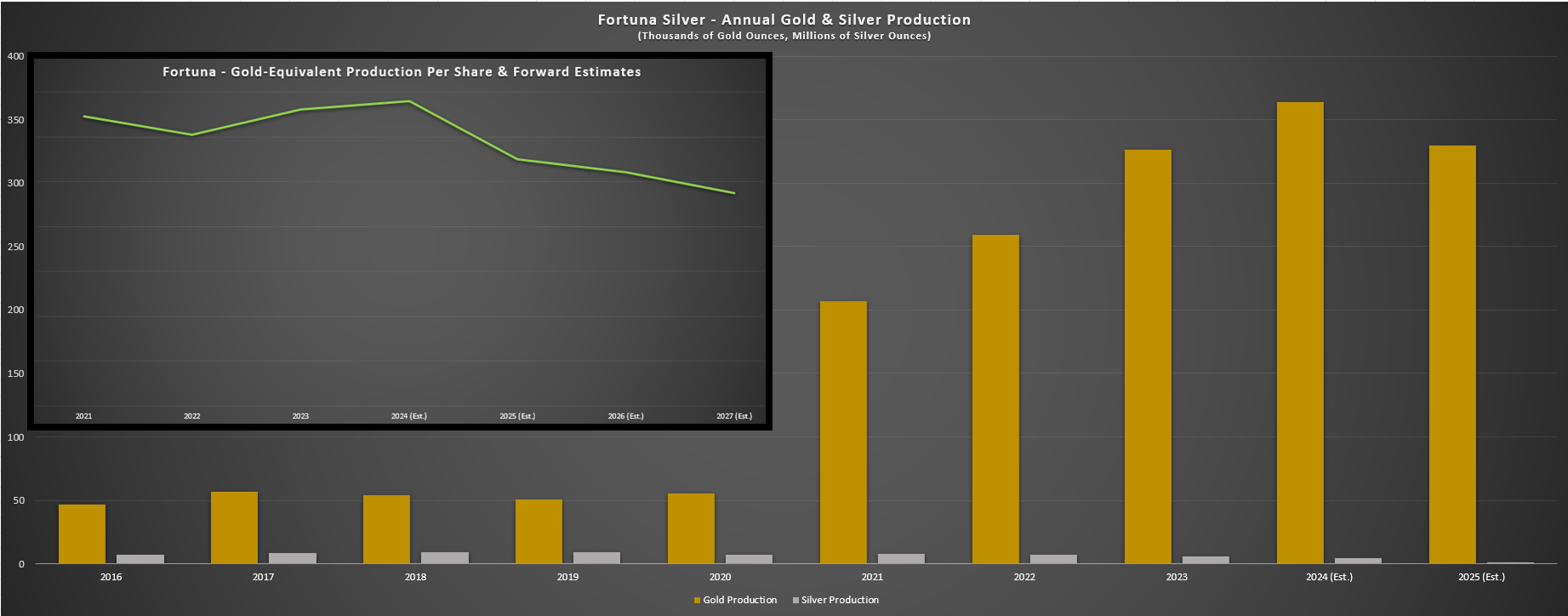

Fortuna released its preliminary Q4 and FY2023 results last week, reporting quarterly production of ~107,400 ounces of gold and ~1.35 million ounces of silver. This translated to a 19% decline in silver production, which was offset by a 13% increase in gold production, with the latter helped by the smooth ramp-up of its Seguela Mine in Cote d’Ivoire. Meanwhile, full-year production came in at ~326,600 ounces of gold and ~5.88 million ounces of silver, with gold production offsetting silver production which plunged 15% year-over-year on the back of an 8% decline last year as well. And with silver production expected to make up less than 5% of revenue in 2025, assuming San Jose heads offline, it’s certainly becoming more difficult to call Fortuna a silver play.

Fortuna Quarterly Metals Production – Company Filings, Author’s Chart Fortuna Quarterly Metals Production – Company Filings, Author’s Chart

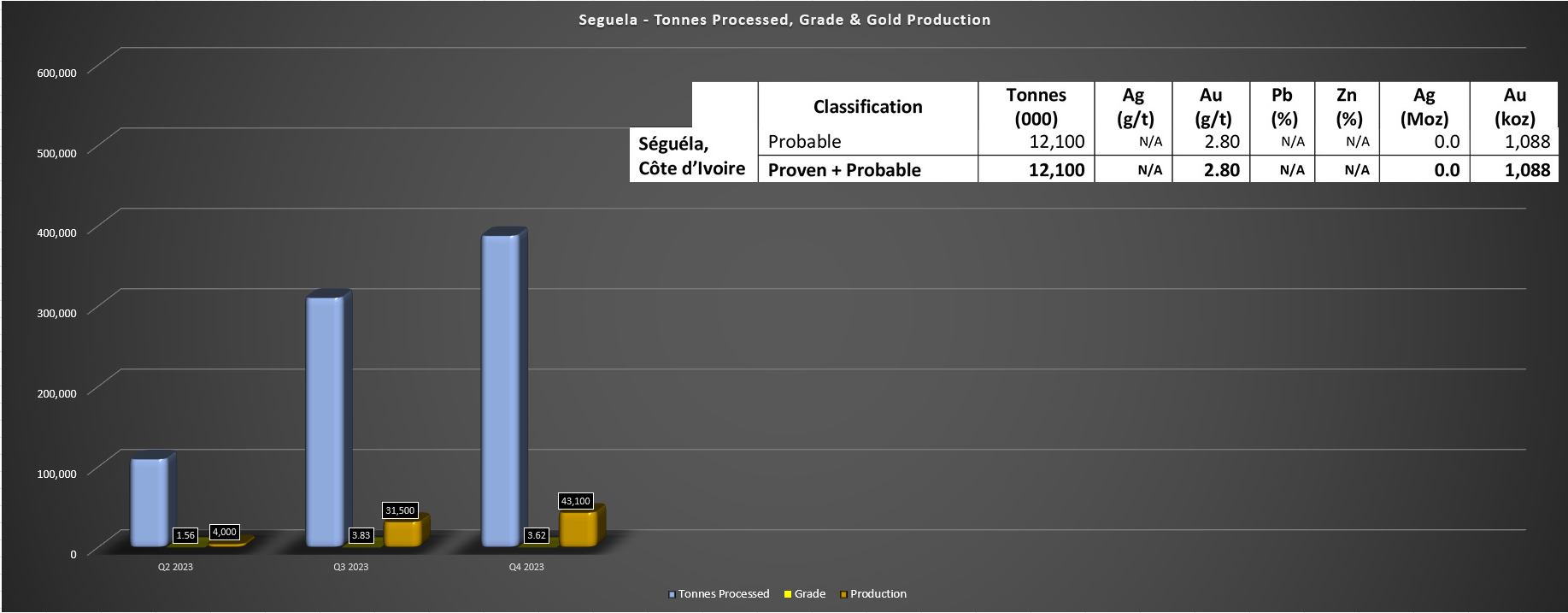

Digging into the results a little closer, we can see that Q4 was a blowout for Seguela, with ~43,100 ounces of gold producer, benefiting from mill throughput well above nameplate capacity (186 tonnes per hour vs. 154 tonnes per hour) and positive grade reconciliation. This was evidenced by ~387,600 tonnes being processed at an average grade of 3.62 grams per tonne of gold, with Q4 coming in above my estimates of 40,000 ounces of gold. That said, and as noted last year, grades were coming in well above life-of-mine grades (~2.80 grams per tonne of gold) with the benefit of an extremely low strip ratio, meaning that annualizing ~40,000 ounce peak production quarters over the mine life and assuming sub $900/oz all-in sustaining costs was likely to lead to disappointment. This has been confirmed by the 2024 guidance, which calls for higher stripping and production of ~132,000 ounces at the mid-point at costs of $1,170/oz.

Seguela Quarterly Operating Metrics – Company Filings, Author’s Chart

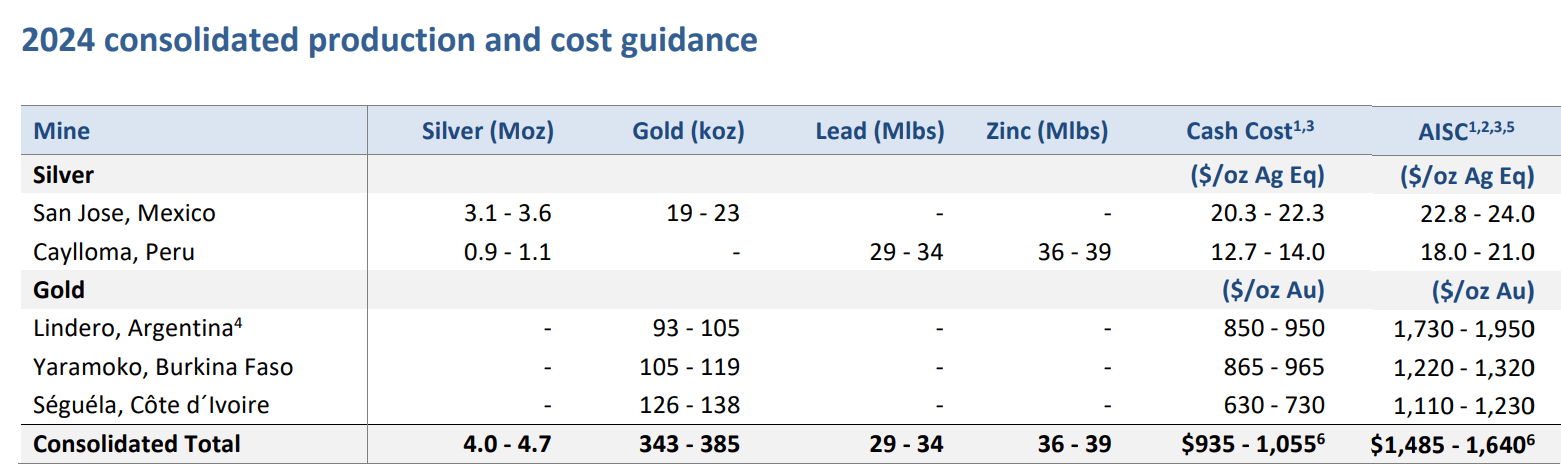

Moving to the company’s Yaramoko Mine in Burkina Faso, it was a solid year here as well, with production coming in above guidance at ~117,700 ounces of gold vs. a guidance midpoint of 99,000 ounces. This was helped by a strong Q4 with ~28,200 ounces produced (~110,400 tonnes at 7.16 grams per tonne of gold). Unfortunately, this was overshadowed by a weaker year at Lindero due to declining grades (in line with mine sequencing) with just ~101,200 ounces of gold produced (Q4 2023: ~29,600 ounces), and a much weaker year at San Jose with production of just ~1.02 million ounces of silver in Q4 and ~4.66 million ounces for the year. These metrics were well below planned levels on the back of lower grades and throughput, operational challenges in Q4, and the impact of a 15-day illegal blockade on operations. Unfortunately, 2024 won’t be any better at this asset, with guidance of 3.35 million ounces of silver production (+21,000 ounces of gold production) at ~$1,970/oz AISC.

2024 Outlook

Looking at the larger consolidated 2024 outlook, Fortuna has guided for production of 4.35 million ounces of silver and 364,000 ounces of gold at the mid-point, translating to a further increase in overall metals production. However, silver production is expected to take an additional 26% step down in 2024 (4.35 million ounces vs. 5.88 million ounces), offset by a ~10% increase in gold production with a full year of production from its new Seguela Mine. And while we will see a further increase in gold-equivalent production per share this year, this is not expected to last. In fact, gold-equivalent production per share should peak in 2024 with fewer ounces of gold and silver produced from San Jose and lower tonnage at Yaramoko post-2024. Hence, while Fortuna’s Seguela Mine is undoubtedly an upgrade to the portfolio, this is largely being offset by two short lives at Yaramoko and San Jose, which make up 100,000+ ounces of annual gold production and ~3.0+ million ounces of silver or ~140,000 gold-equivalent ounces [GEOs].

Fortuna 2024 Guidance – Company Website Fortuna – Annual Gold Silver Production, GEO Production Per Share & Forward Estimates – Company Filings, Author’s Chart

If these production numbers had come out with a more robust margin outlook, it might have been easier for the market to have digested the news. However, Fortuna’s cost guidance came in at $1,563/oz at the mid-point this year, over 10% above the expected FY2024 industry average of $1,410/oz. This is certainly not ideal, but should not be surprising to investors have looked at the mine plans of its legacy assets with declining grades at Lindero, declining production at Yaramoko, and the additional impact of a stronger Mexican Peso on its already low-margin silver operations in Mexico. In fact, other producers like Fresnillo (OTCPK:FNLPF) and Endeavour Silver (EXK) have been warning about cost pressures for most of 2023, which suggested an even worse year on deck in 2024 for San Jose if the Peso remained strong which has been the case.

The only good news is that Lindero’s costs are higher year-over-year because of investments in its leach pad expansion (expected to be completed in the H2-2024), and this is a minor drag on margins with all-in sustaining costs here expected to come in above $1,825/oz. That said, Yaramoko is partially offsetting this with a better than planned year, but we should see costs rise at Yaramoko in 2025 as it produces less gold and gets reduced leverage on fixed costs. Hence, I would still expect to see AISC near $1,400/oz in 2025 for Fortuna even if its higher cost San Jose mine does head offline, which has been a severe drag on performance. And while this will be an improvement, this will be offset by much lower production (fewer GEOs from Yaramoko and San Jose).

Recent Developments

Finally, as for recent developments, I had warned in previous updates that adding reserves at San Jose in 2024 would not be easy given the impact of rising cut-off grades with what looked to be a flat silver price which was up against general inflationary pressures and the additional impact of a stronger Mexican Peso. This would essentially erase Fortuna’s silver premium as it would result in an 80% decline in silver segment production, but I was cautiously optimistic that it might produce until Q1 2026 with minor reserve replacement. Unfortunately, even this estimate looks like it might have been too ambitious, with Fortuna stating that “the updated LOMP for 2024 is scheduled to exhaust reserves by the end of 2024 compared to mid-2025 as previously planned.”

Fortuna Silver Q3 2024 Commentary – Seeking Alpha Premium/PRO

Fortuna noted that the lower planned production can mostly be attributed to Mexican Peso strength, higher contractor costs for transportation, distribution, shotcrete, maintenance, and mining services, and higher labor costs and new labor reform mandates that took effect at the start of this year. The result is that closure is now expected in late 2024, with a team now in place to review and update a progressive mine closure/monitoring plan at a cost of ~$27 million. Some investors might argue that this development is a positive as it’s been a huge drag on costs and this is a fair point. That said, I would argue that the offset is that Fortuna could see further multiple compression from shedding the bulk of its silver segment, with predominantly West African gold producers with flat to declining production trading at much lower multiples (*) than 1.0x P/NAV where Fortuna sits today, especially with costs above the industry average.

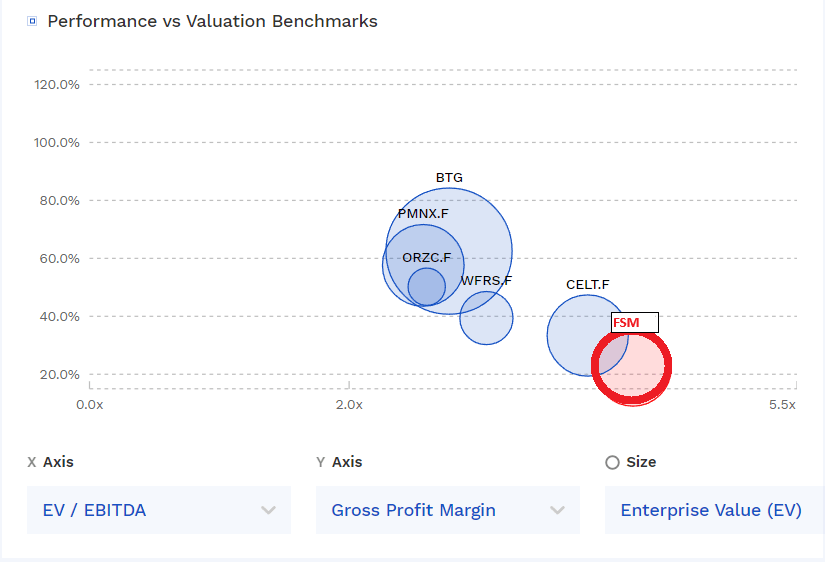

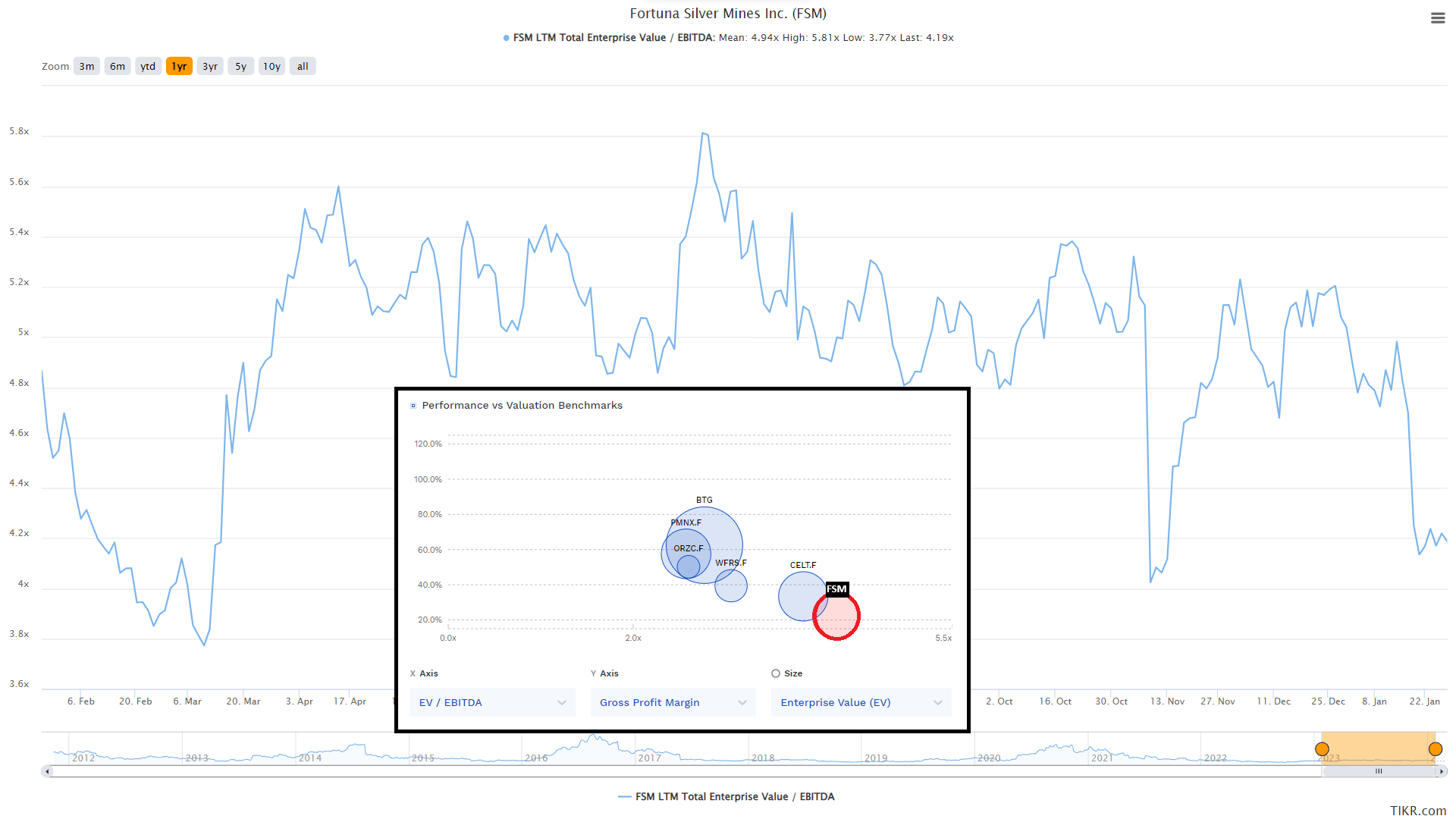

Fortuna Silver EV/EBITDA, Margins & Valuation vs. West African Producer Peers – FinBox

(*) A sample of West African gold producers is shown above, and we can see that Fortuna trades at one of the highest multiples despite much weaker margins and smaller scale than some of its peers, like Perseus Mining (OTCPK:PMNXF) and B2Gold (BTG). (*)

Valuation

Based on ~311 million fully diluted shares and a share price of US$3.10, Fortuna trades at a market cap of ~$970 million and an enterprise value of ~$1.09 billion. This has left Fortuna trading right near its estimated net asset value of ~$990 million, with San Jose now more of a liability than an asset with razor-thin margins this year with a 1-year mine life, offset by its expected closure costs. And while a 1.0x P/NAV multiple can easily be justified by a diversified and primarily Tier-1 jurisdiction operator with industry-leading margins like Alamos Gold (AGI) or Agnico Eagle (AEM), I think it’s a lot harder to assign this multiple to a high-cost producer with the bulk of its cash flow coming from West Africa and little to no silver exposure in its future as San Jose winds down (silver producers trade at a significant premium to gold producers). In fact, most predominantly African gold producers are trading at an average P/NAV multiple below 0.70x currently, and they have far better margins than Fortuna on balance.

Fortuna Silver Mines Valuation & Valuation vs. Peers – TIKR, FinBox

Using what I believe to be a more conservative multiple of 5.5x forward cash flow given its significant exposure to West Africa and 1.0x P/NAV and a 65/35% weighting (P/NAV vs. P/CF), I see an updated fair value for Fortuna of US$4.30. This fair value estimate points to a 39% upside from current levels, but I am looking for a minimum 40% discount to fair value to justify starting new positions in small-cap producers in Tier-2/Tier-3 ranked jurisdictions. And after applying this discount, Fortuna’s updated low-risk buy zone comes in at US$2.60 or lower, suggesting that the stock has still yet to move into a low-risk buy zone after its recent violent correction. Obviously, I could be wrong and the stock may end up finding a floor, but I prefer to buy at the right price or pass entirely, and when I can get a deeper discount to fair value in a larger producer with superior assets and Tier-1 exposure like B2Gold with a ~5.9% dividend yield, it’s hard to justify owning a name like Fortuna Silver.

Summary

Fortuna Silver had a solid year in 2023, beating guidance at its two operating gold mines in West Africa and enjoying a smooth ramp-up at Seguela while some other producers have had hiccups in the construction/ramp-up phase. That said, the company has delivered underwhelming 2024 guidance, it’s now looking more likely that San Jose is on its last legs (potentially erasing the bulk of its silver exposure starting in 2025 and a hit to gold production), and costs will remain above the industry average again. Plus, as I warned previously, Seguela would benefit from grades well above its LOM reserve grade in H2 2023, but costs were likely to normalize in 2024, with grades at or below 3.0 grams per tonne of gold and a higher strip ratio. Hence, there was no reason to think that 2024/2025 AISC would come in below $800/oz in line with the 2021 LOMP, especially with high double-digit additional inflationary pressures in the 2021-2023 period.

Given the shorter planned mine life at San Jose with a higher hurdle to adding new reserves and higher overall costs across the portfolio, Fortuna’s fair value has dropped vs. my previous estimates, and with other producers underperforming since October, Fortuna’s reward/risk setup is less compelling on a relative value basis. Hence, if I were looking to start a new position in Fortuna, I see the low-risk buy zone coming in closer to US$2.60. Hence, if I wanted to put capital to work today, my preference would be a larger producer like B2Gold with superior assets and Tier-1 exposure with a ~5.9% dividend yield.

Q2 2024 Earnings Call Transcript")