Yuichiro Chino/Moment via Getty Images

Investment Thesis

Fortinet (NASDAQ:FTNT) recently released its full-year FY23 results yesterday, showing improvement from the pivotal Q3 FY23 quarter, which cast a doubt on the cybersecurity company’s full-year performance. In the Q3 call, investors were quick to punish the stock last year, but management has made an active effort in the last 3 months to reinstill confidence in its investor base by participating in technology conferences such as the Wells Fargo TMT conference and the Barclays Global Technology Conference.

Based on management commentary from the recent earnings call and taking into account their forward-looking estimates from the full-year FY23 results published yesterday, I see upside in Fortinet and rate this as a BUY.

About Fortinet and its Journey into SASE

Before I review the latest earnings call, I think it is important to review Fortinet’s business model briefly and why SASE (Secure access service edge) is an important next chapter for the cybersecurity company. Fortinet was founded by the Xie brothers, Ken and Michael, and headquartered in Sunnyvale, CA, with the intention of selling on-premise cybersecurity hardware and virtual machine products such as firewalls and software-defined wide area networks (SD-WAN), virtual private networks (VPNs) etc. The company has shown resilience by weathering many business transformations, one of them being the transition from shifting reliance from hardware-product revenue to service revenue.

The company is in the midst of another transition at the moment as it moves to extend its reach of cybersecurity products in the SASE space as well as compete with some other large players such as Palo Alto (PANW) and Cisco (CSCO). In the Q3 FY23 earnings call, management expressed their disappointment with their own performance as product revenue declined slightly y/y while also setting mid- to long-term expectations that the company would be shifting “focus towards a faster-growing secured operation as SASE market over the next few quarters.”

Therefore, while reviewing their full-year FY23 performance, I think it is important to also review improvements in numbers and commentary from management.

Q4 & Full Year Results Walkthrough

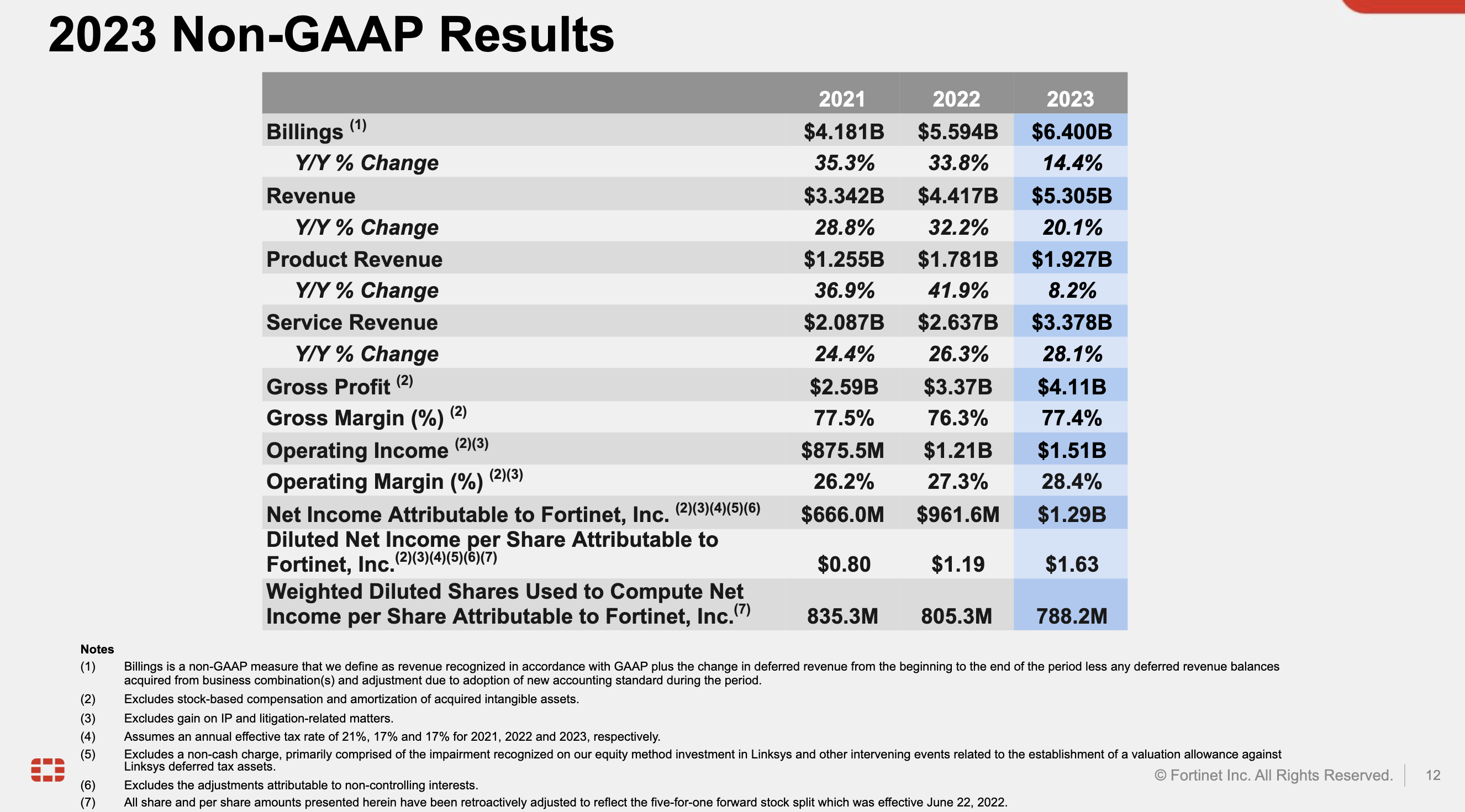

For the fourth quarter, Fortinet reported revenues of $1.42 billion, up 10.3% y/y and slightly beating consensus estimates by 0.7%. For the full year FY23, Fortinet’s revenue rose by 20% y/y over year to 5.3 billion, meeting the market’s expectations. Most of the growth in revenue was driven by its Services revenue segment, which accounted for 63.7% of the revenue, with the remainder coming from Product revenue. While Services revenue grew by a modest 20.1%, it was the Product revenue that saw the sharpest decline in three years, as can be seen below. I had noted earlier how management had expressed their disappointment at product revenue slowing more than their expectations. The slide below shows exactly the magnitude by which product revenue slowed.

FY23 Q4 investor presentation, Fortinet

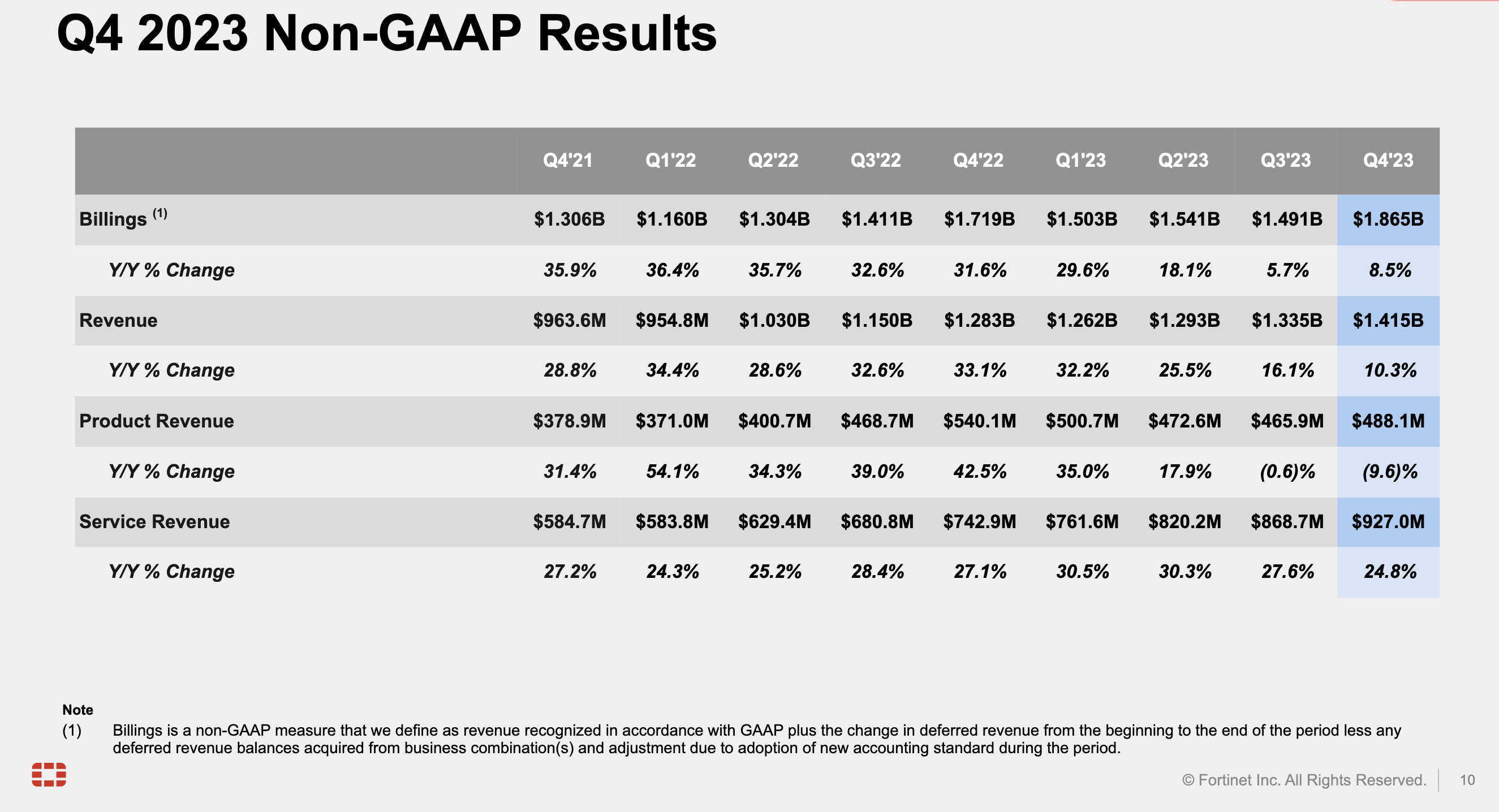

Full-year FY23 Billings grew 14.4% y/y, slower than revenue growth. However, much of the expectation of deceleration here was already laid by management last quarter, along with the mitigation strategies that management was working towards by working on their SASE product offerings. When I drill down on a q/q basis, I see that some of the billing growth has already picked up in Q4 FY23 after 6 straight sequential quarters of slowdown in their quarterly y/y Billings metric, as I see in the chart below.

FY23 Q4 investor presentation, Fortinet

These are some very early encouraging signs of the initial success the company is already seeing in its Billings. As the company rolls out more SASE products and upskills their sales and marketing team to get SASE-certified, Fortinet’s transition will take a few quarters. But on the Q4 earnings call, management provided more color on the trends they’re seeing in their Billings, which shows how critical Fortinet’s extension to SASE is. While Secure Networking accounts for the largest share of their Billings at 60%, Billings from SASE accounted for 21% of total Billings, which pleasantly surprised me. This was a welcome improvement, in my opinion, from the Q3 quarter. The next couple quarters may be slightly bumpy, in my opinion, but I have confidence that management will be able to successfully complete its transition to SASE by the end of the year. This was also previously reflected by management at the Barclays Technology conference late last year, where they mentioned:

Yes, we’re not guided into ’24 yet. So obviously, just some sort of indications of where we think, because people were concerned about what the future looks like always. I think from a billings perspective, what we said for 2024 was that we would expect the billings growth to return to double digits by the back half of next year.

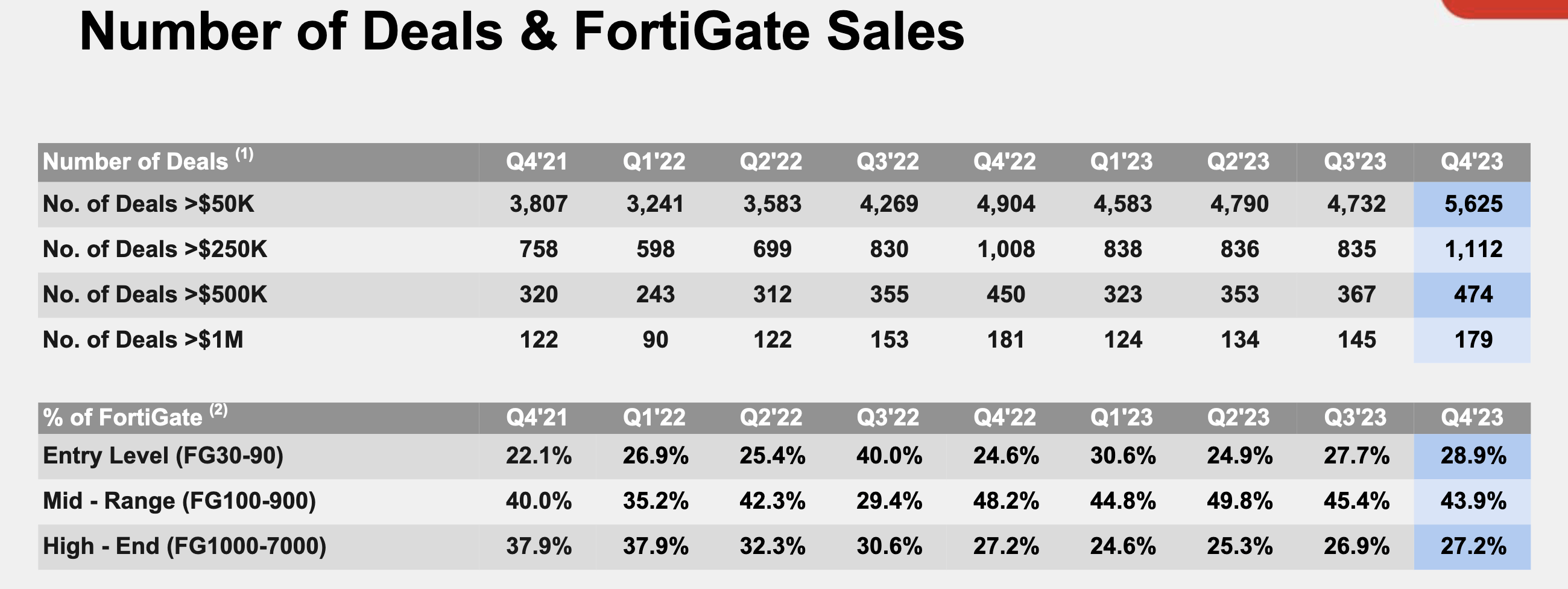

Another point in the earnings report that caught my attention was a development in Fortinet’s customer base. Usually, Fortinet has a good mix of customers, from SMBs to enterprises as well, but it’s more skewed towards SMBs. However, I noticed some good sequential improvement in their deals, especially in the larger deals, i.e., >$500k and >$1M. Moving forward, I would like to see more growth in this number so that Fortinet reduces its dependency on its SMB’s customer cohort. In my view, shifting its dependence to larger customers will allow Fortinet to expand its margins and keep expenses in line.

FY23 Q4 investor presentation, Fortinet

Moving over to profits. Fortinet achieved gross margins of 76.7%, in line with their long-term range of 76%-78%. Non-GAAP operating margins expanded by 1.1% to 28.4%. Although management did not directly allude to this, my guess here is that the large number of deals has started to show how effective Fortinet’s Sales and Marketing spend can be for the company. When specifically asked about this, Fortinet’s CFO mentioned that these large deals were actually not forecasted last year, possibly signaling that it may have helped in more than expected higher margins.

FY23 Q4 investor presentation, Fortinet

Valuation Models Suggest Strong Upside

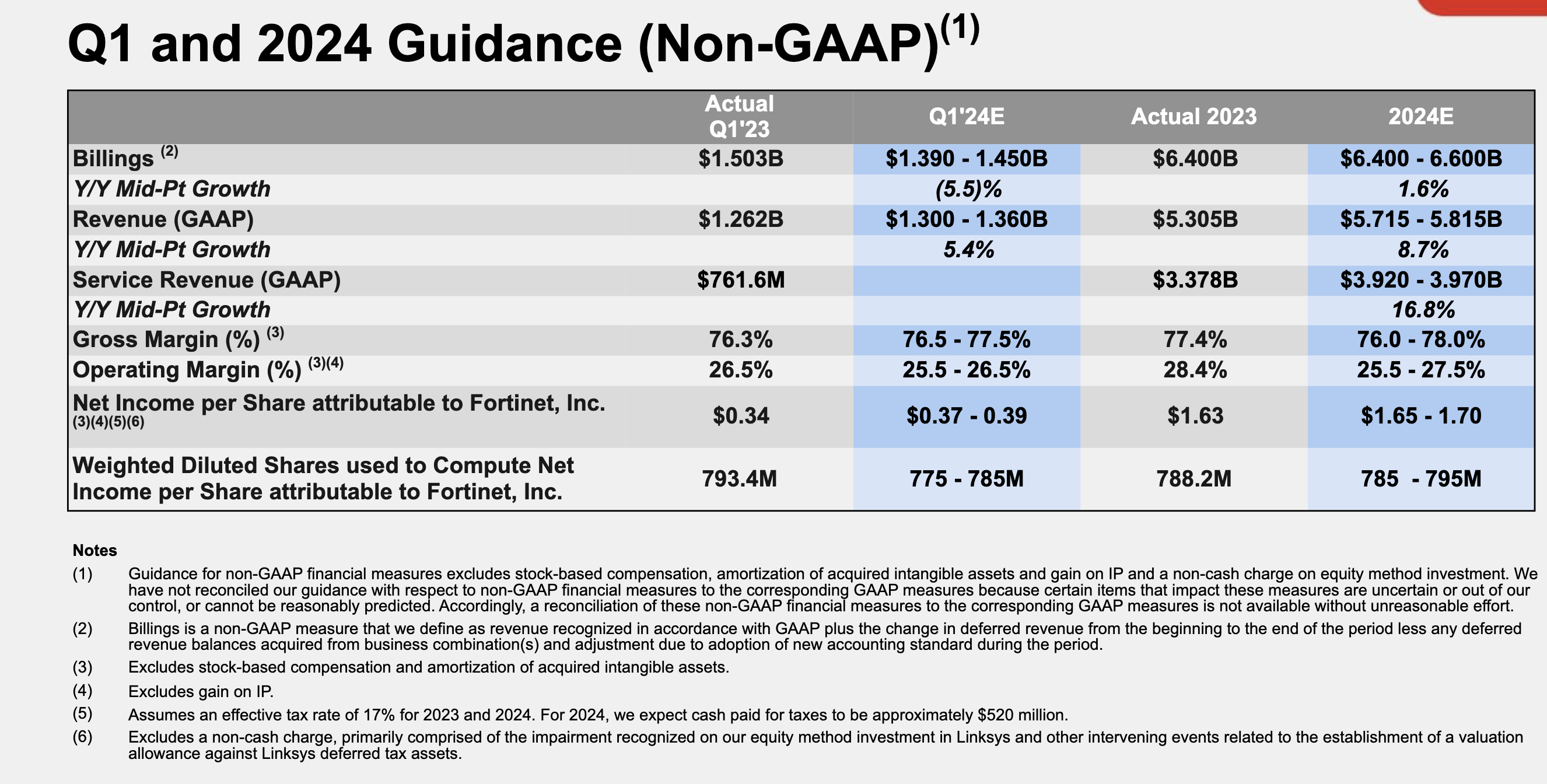

Management has issued guidance for FY24 which, in my opinion, was slightly tepid. However, I also think management is attempting to be conservative and temper expectations. I have attached the guidance below, which shows Billings are still growing but at a very slow pace.

FY23 Q4 investor presentation, Fortinet

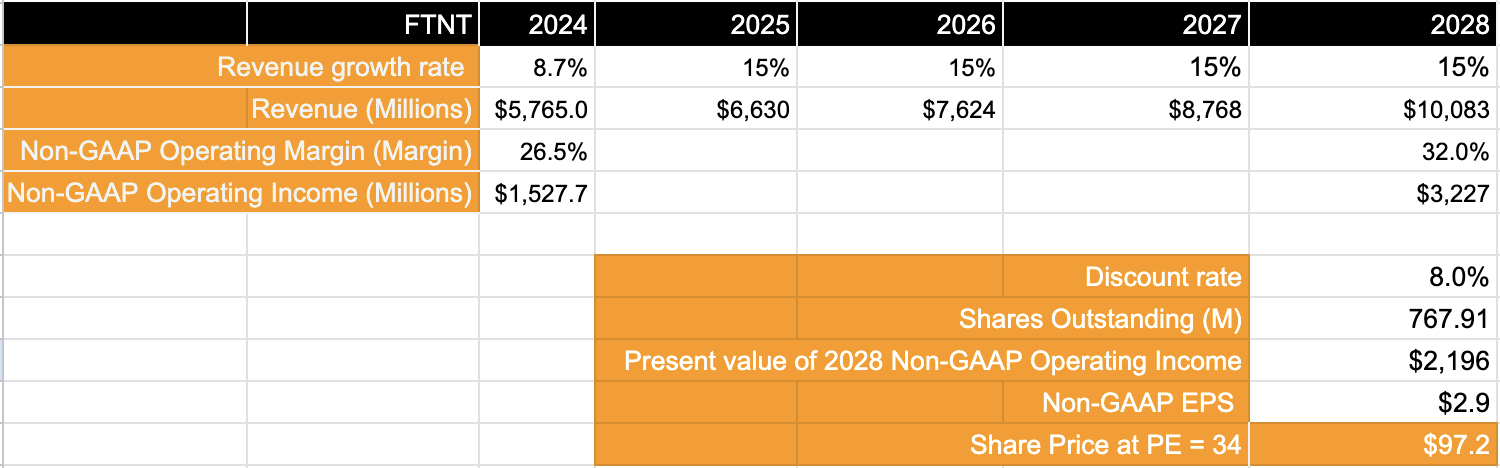

Given how management has already started executing on capturing market share in the SASE market, I am optimistic that Billings can continue to grow in the healthy double digits from FY25 onwards. Now, observing the company’s operational efficiency this year, I will continue to expect operating margins to continue to expand to my target of 32% in FY28, growing at a CAGR of ~20%. For such a growth rate, I value Fortinet at ~30%.

Author

Risks & Other Factors to Consider

Since Fortinet is in a period of transition, there is always the risk that the transition may fail or take longer than usual to complete. But with a history of having completed transitions earlier combined with the progress Fortinet has already started to make on its transition to SASE, I am optimistic about Fortinet’s transition. I will, however, pay close attention to management commentary throughout the year as they advise on trends that they are seeing in Billings. I had noted earlier how SASE contributed to ~21% of Billings in the FY23 report. I suspect Fortinet will use their current FY24 guidance as a base to build forward expectations through the year as they get through product cycles and participate in more technology conferences, where additional color can be expected to be shared on how their SASE market share is evolving. Additional headwinds from competition may further impact Fortinet’s ambitions to expand into SASE.

Since Fortinet is still in the business of selling hardware products, and with their hardware products not selling enough, the company’s balance sheet may carry more inventory than expected; this will worsen its working capital and put pressure on free cash.

Conclusion

In summary, I am optimistic about management’s transition to the SASE market. At the same time, management has shown efficiency in managing its expenses, increasing margins, and focusing on innovation. With these positive developments, I rate Fortinet as a BUY.

Q2 2024 Earnings Call Transcript")