If you are looking at AGNC, enticed by its huge dividend yield, you would probably be better off with dividend growth stock Rexford Industrial.

If you are a dividend investor, you probably care a great deal about dividend yields. That’s basically the big attraction when it comes to AGNC Investment (AGNC 0.21%) and its huge 15% yield. When comparing that to the relatively modest 3.7% yield on offer from Rexford Industrial (REXR -0.42%), you might be tempted to pass on Rexford. There’s an important difference here on the dividend front that you shouldn’t ignore and it’ll likely make Rexford a better long-term dividend stock for most investors.

AGNC vs. Rexford: Business model

AGNC Investment is a mortgage real estate investment trust (REIT). That means it buys mortgages that have been packed into bond-like securities, providing shareholders with direct exposure to the mortgage market. This is not an easy business and AGNC’s value is tied to the publicly traded mortgage bonds it buys. In many ways, it is more like a mutual fund than a typical REIT.

Rexford is a typical REIT. It buys physical properties and leases them out to tenants. In this case, Rexford is highly focused on the industrial property type and geographically on the Southern California market. That concentration increases risk, but Southern California is the largest and usually best-positioned industrial market in the United States. Rents are buttressed by a lack of property, strict zoning laws, and the trend of industrial assets being converted to housing.

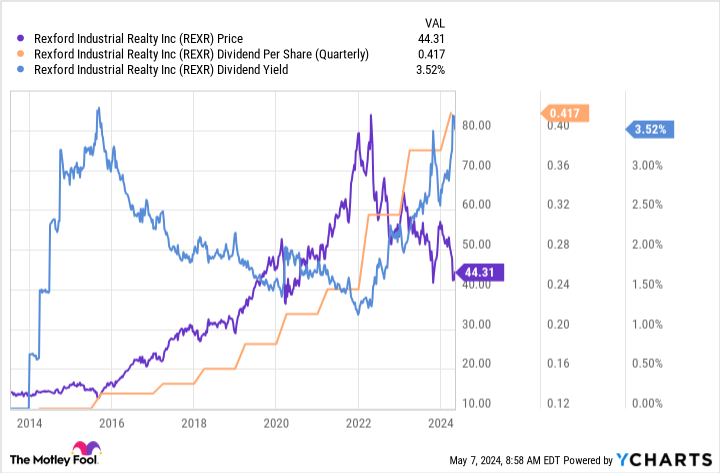

AGNC vs. Rexford: Dividend history

This is where things get interesting. AGNC’s dividend has been extremely volatile over time. As the chart below highlights, it rose sharply and then, for over a decade, it has been in general decline. The stock price has followed along for the ride. That trend could absolutely change, but if you are trying to live off of the income your portfolio generates, you would have been left with less income and a huge capital loss if you bought AGNC. Notably, its yield has been high, usually in the double digits, over the entire span. If you are considering investing in AGNC today, you have to ask whether given that terrible dividend history, the risk is worth the reward. For most, it probably won’t be.

Rexford’s dividend track record is drastically different. It has boosted its payout annually for 11 years. And the dividend has increased by a huge 16% annualized over the past decade. That’s an incredible growth rate for a REIT, but it isn’t as big an anomaly as it may seem. The most recent dividend hike was roughly 10%. Being a big player in a niche market with structural advantages has clearly worked out well for Rexford and its shareholders. But the yield is far lower — currently around 3.7% — because the stock price has risen along with the dividend payment over time.

AGNC vs. Rexford: Yield or yield on purchase price

But what about that huge yield from AGNC Investment? Clearly, you can’t go in counting on that yield to last. What’s interesting here is that Rexford’s yield is just a small fraction of AGNC’s today. But what if you had bought Rexford at the highest price in 2013, when the quarterly dividend per share was $0.12? At that point your yield on purchase price, based on a $14.15 stock price, would have been 3.3%, which is close to where the yield is today.

If you had held that stock until today, however, the quarterly dividend would now be $0.4175 per share. That equates to a yield on purchase price of 11.8%! That’s not too far off from AGNC’s yield. Of course, there’s no way to guarantee that Rexford continues to increase its dividend in the future like it has in the past. However, if you are looking to live off of your dividends in retirement, Rexford’s story should be far more compelling than that of regular dividend-cutter AGNC.

Not a bad REIT, just not for dividend investors

The rub here is that AGNC isn’t necessarily a bad investment. It’s just meant for institutional investors that use an asset allocation model and focus on total return (which assumes dividend reinvestment) over dividend yield. Even though it has a huge yield, it’s just not appropriate for most dividend investors. Rexford, meanwhile, despite a relatively low yield, has turned out to be a much better dividend stock to own. But here’s the really interesting thing: Rexford’s yield is actually historically high today, suggesting the stock is currently on sale. In other words, now might be a good time to buy it.

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Rexford Industrial Realty. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")