Vera Tikhonova

Overview

My thesis is that while Ford (NYSE:F) stock can be considered cheap at the moment with good profitability and strong forward operational intentions, its weak growth in revenues and margins means it isn’t a strong contender in a long-term focused portfolio. There are better options to consider that indicate longer-term, high-price returns from presently undervalued stocks. Nevertheless, the short-to-medium-term upside could be around 40% based on my analysis.

Operations & Results

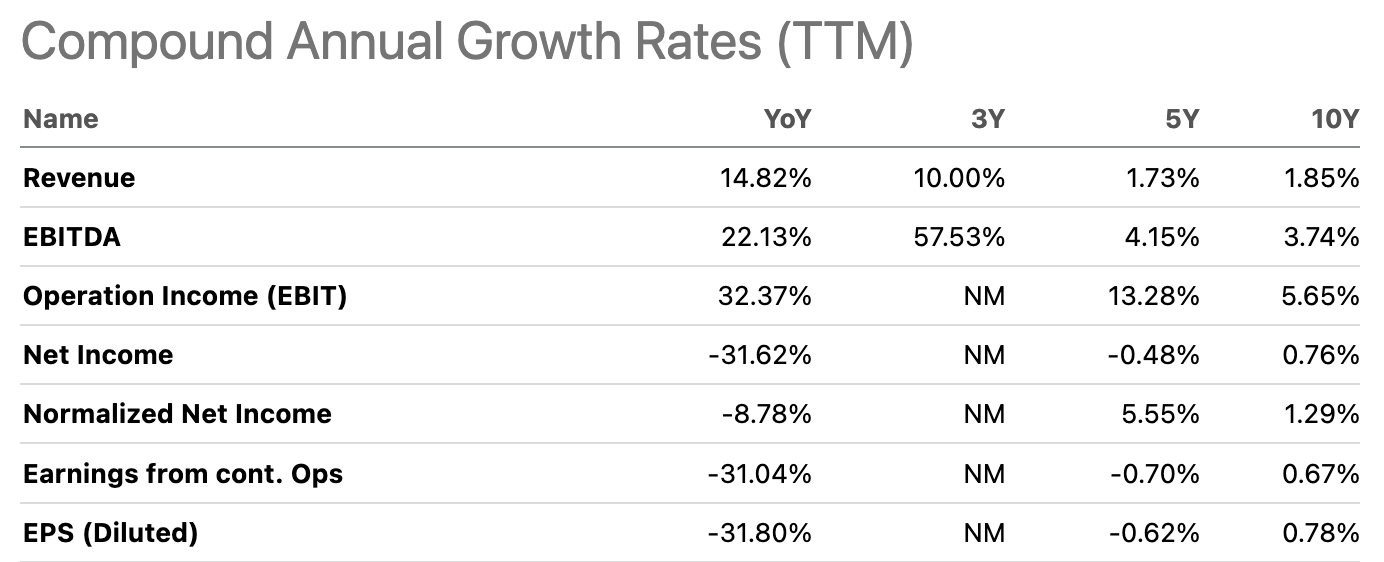

The company has reported incredibly strong compound annual revenue growth rates recently compared to historically, but the firm’s net income compound annual growth rates are much less ideal:

Seeking Alpha

EBIT growth includes an anticipated full-year 2023 EBIT of approximately $10.25 billion, including $1.7 billion in ‘strike-related lost profits’, interrupting high-margin SUV and truck earnings. In addition, recently, operations have been divided into three segments: Ford Blue (gas and hybrid), Ford Model e (electric vehicles), and Ford Pro (commercial products and services).

Ford Q3 2023 Results

Ford Blue delivered $1.7 billion in Q3 EBIT, which is a 17% Y/Y increase. It introduced gas and hybrid versions of the 2024 F-150 pickup, described as ‘the most connected and technologically capable F-150 yet’. The hybrid segment of the business is particularly strong right now, jumping 40% in Q3, primarily as a result of F-150 and Maverick trucks.

Q3 wholesales of Ford Model e’s first-generation electric cars jumped 44%, and revenue increased 26%. However, notably, a loss of $1.3 billion for the segment can be explained by heavy investment in the new technology, competing effectively, and navigating the market dynamics.

Ford’s software-enabled services have also seen a 50% Y/Y increase, approaching 600,000 subscribers in Q3 2023. In addition, Peter Stern, previously from Apple (AAPL), is establishing Ford Integrated Services, working in value-added services from high-tech.

Kumar Galhotra has been named COO, making a sequence of organizational changes to support Ford+ and a highly efficient, cost-reducing, and quality-improving business model.

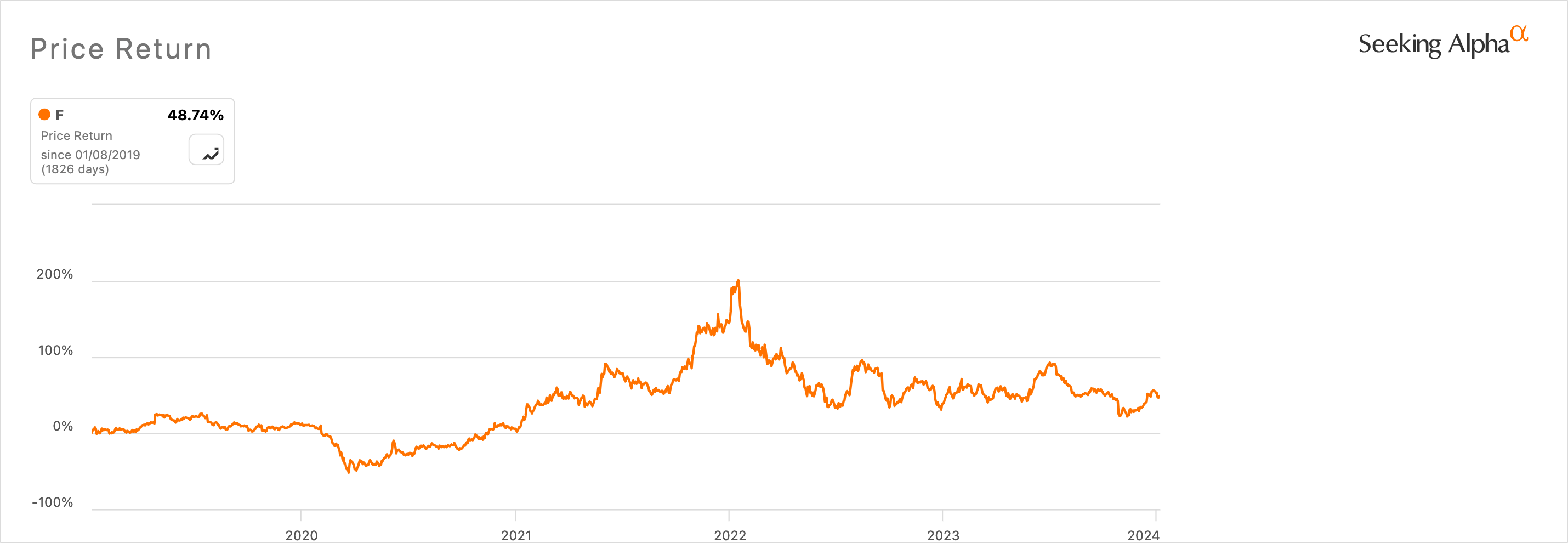

The shares could be considered mispriced when looking at the previous high in 2022 and considering the firm’s success in operations and strategies to tackle green-energy trends in automotive, but this is a significantly risky position and one I don’t think is a good long-term investment but rather could be considered a medium-term trade based on value:

Seeking Alpha

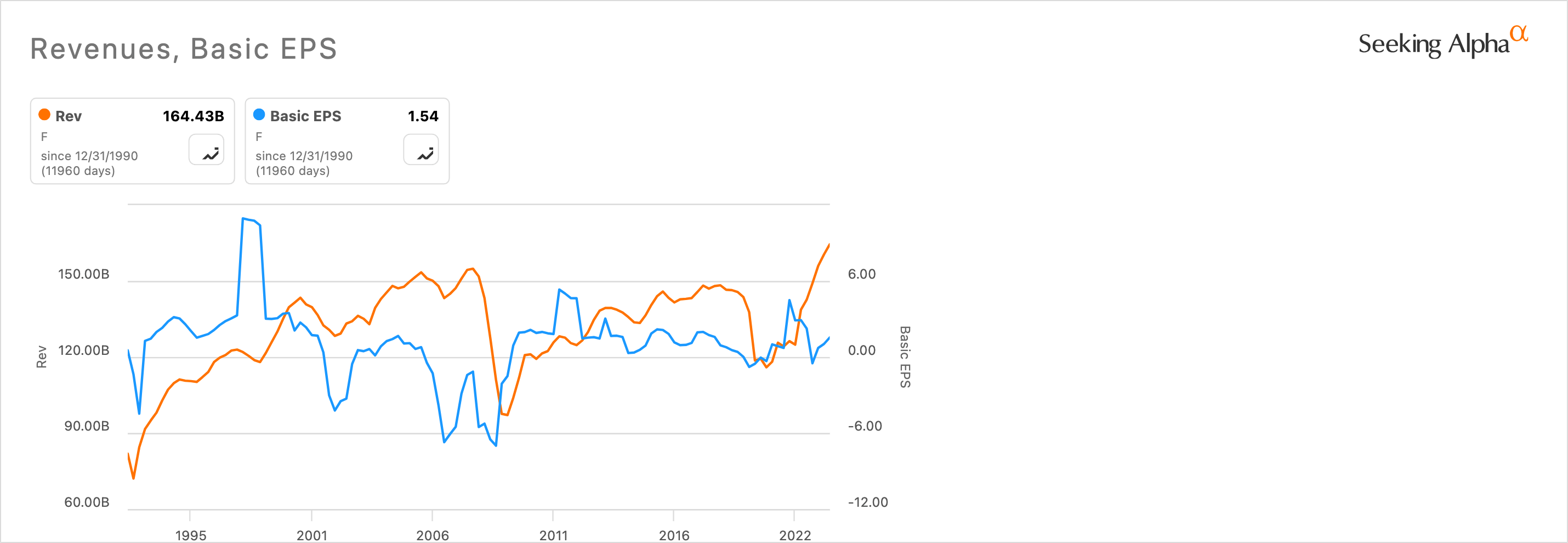

This becomes more apparent to me when analyzing the company’s long-term revenue growth, which is quite slow, and considering its long-term EPS growth, which is relatively flat:

Author, Using Seeking Alpha

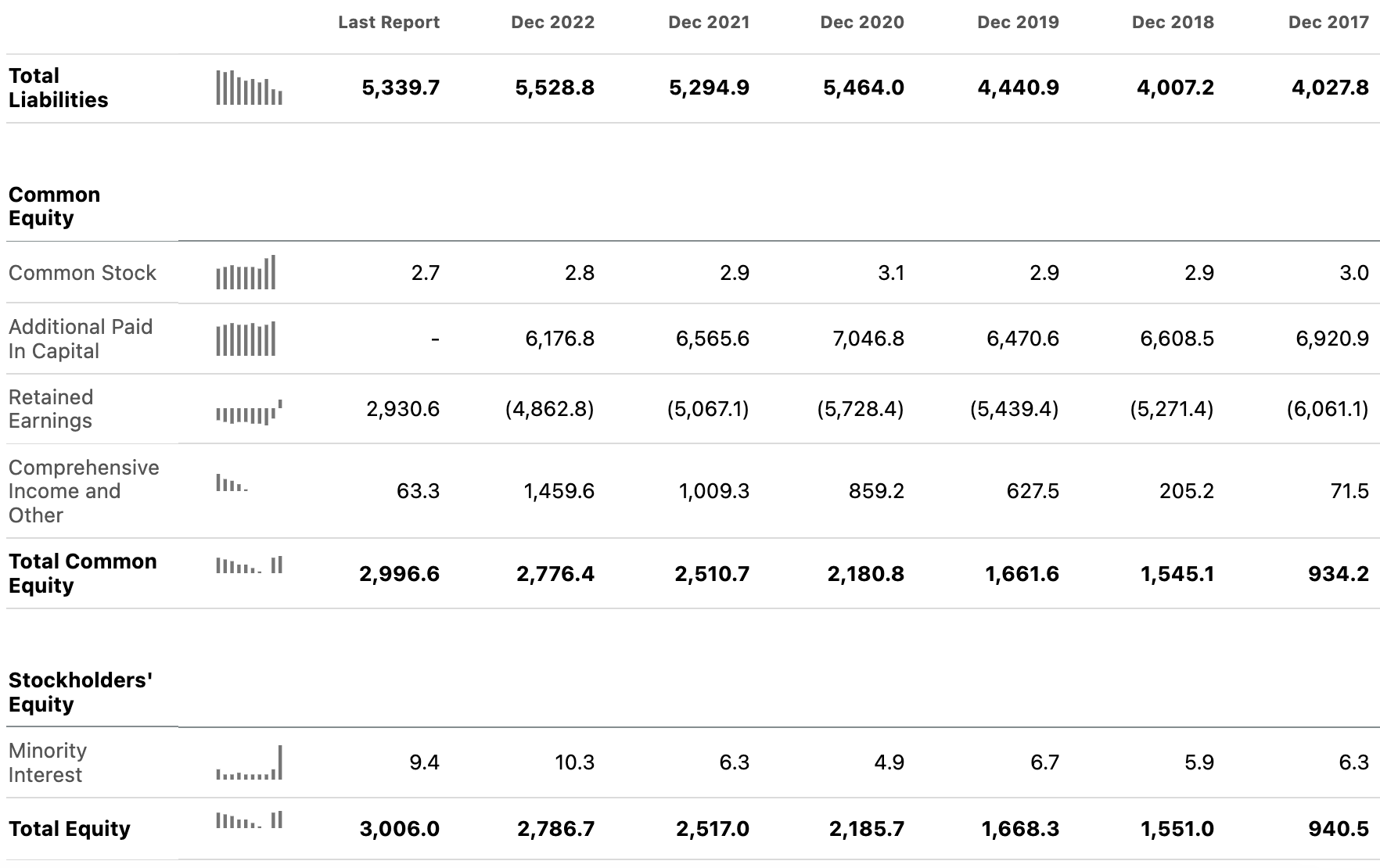

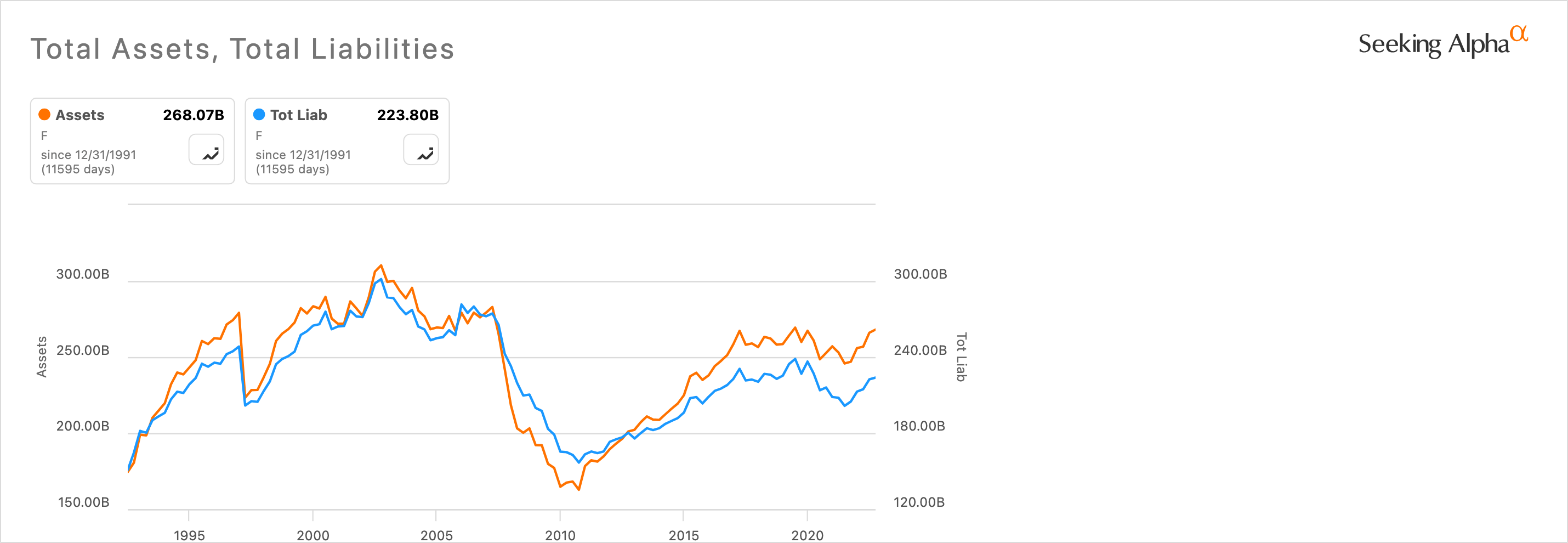

Also, the firm’s balance sheet is stable in relation to past reports but not good at large, with a massive 83.48% of assets balanced by liabilities and an equity-to-asset ratio of 0.17. This is further cause for concern when considering investing in the stock and represents a note of caution on my part for buying Ford shares based on ‘good value’:

Seeking Alpha

The fact the company is increasing its assets at a quicker rate than liabilities recently is a positive sign when considering whether Ford will be financially prepared to compete at the level it may need to. Financing advanced technology for the changing automobile landscape may require more borrowing:

Author, Using Seeking Alpha

Valuation

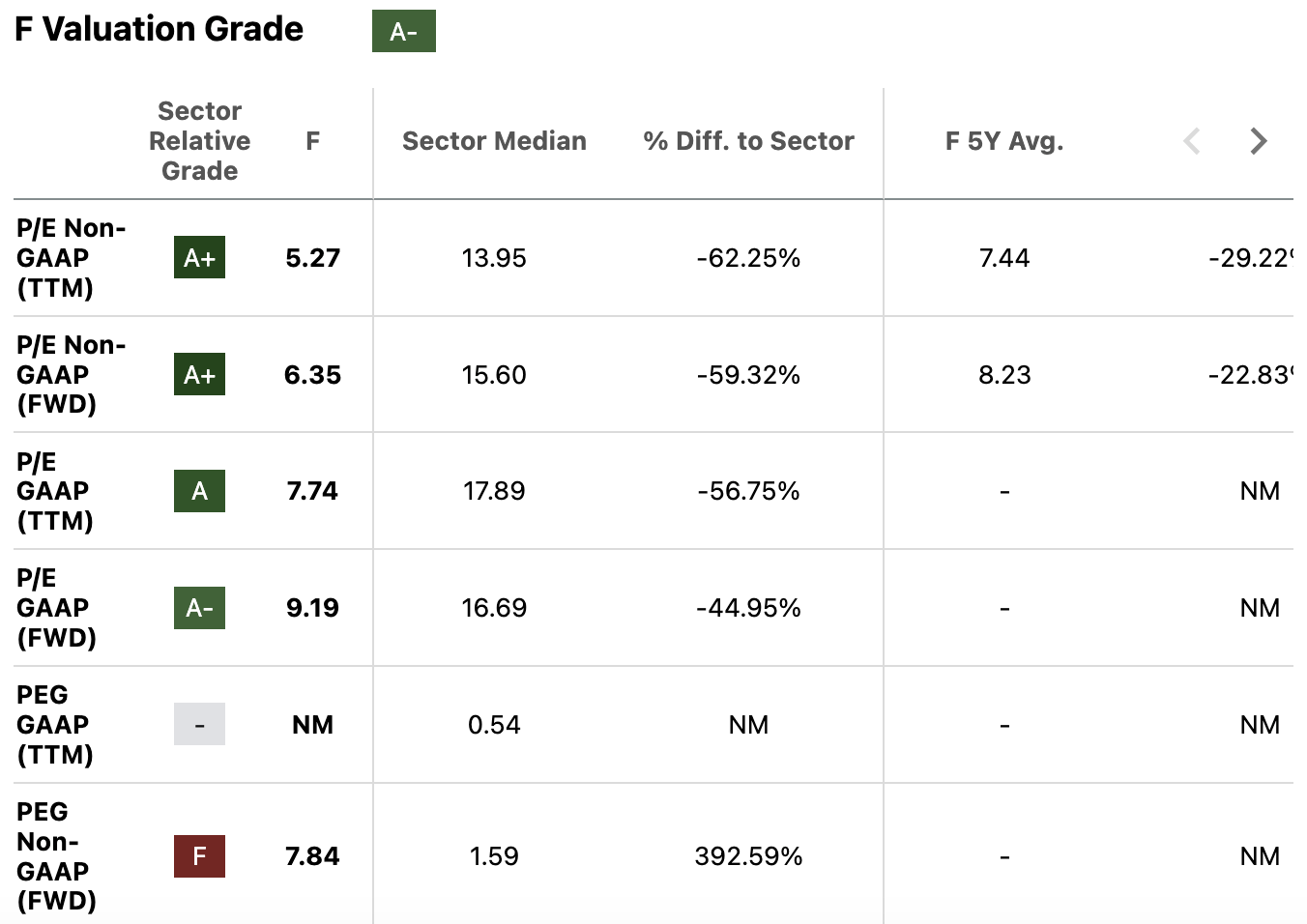

The firm is undeniably cheap on almost all of its valuation metrics, other than one, which, to me, is the key indicator of why the stock is not a good investment:

Seeking Alpha

With a P/E GAAP TTM ratio of around 8 and a forward ratio of around 9, the stock looks favorable from a pure value investment standpoint, but introducing a PEG Non-GAAP FWD ratio of 7.8 makes the case evident that the long-term earnings growth of the stock is its critical weakness.

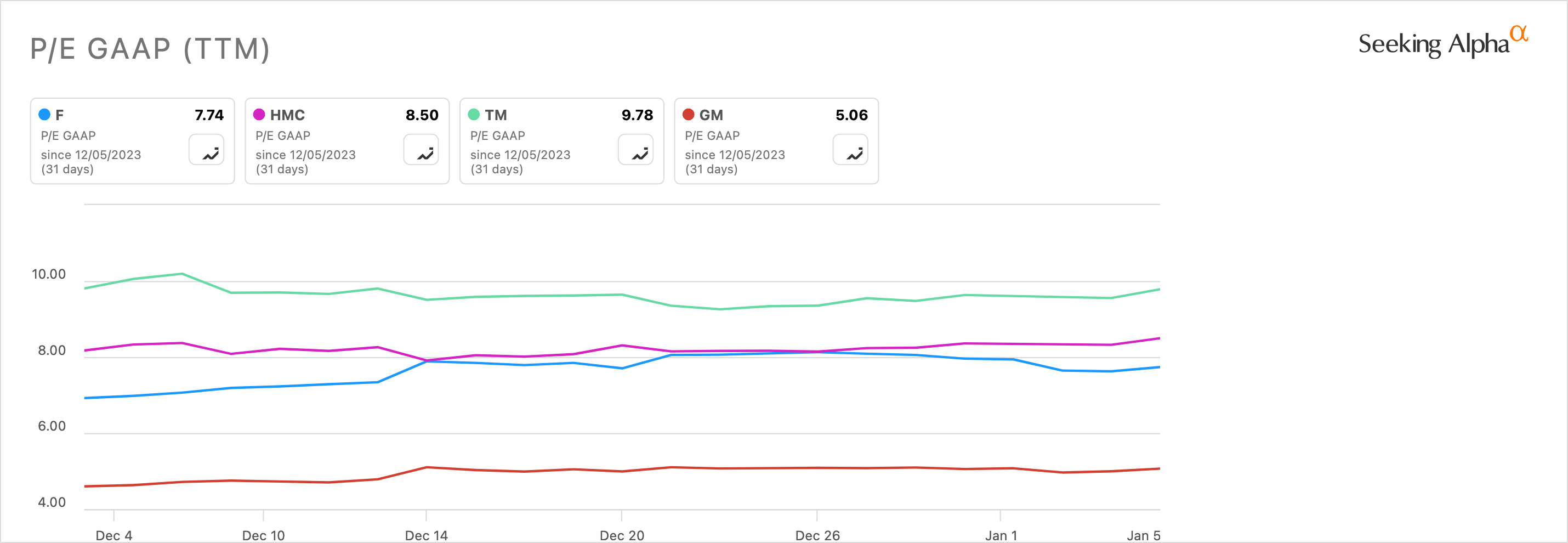

However, comparing the firm against four of its popular peers on its P/E GAAP TTM ratio leads it to look average on this metric in some regards:

Author, Using Seeking Alpha

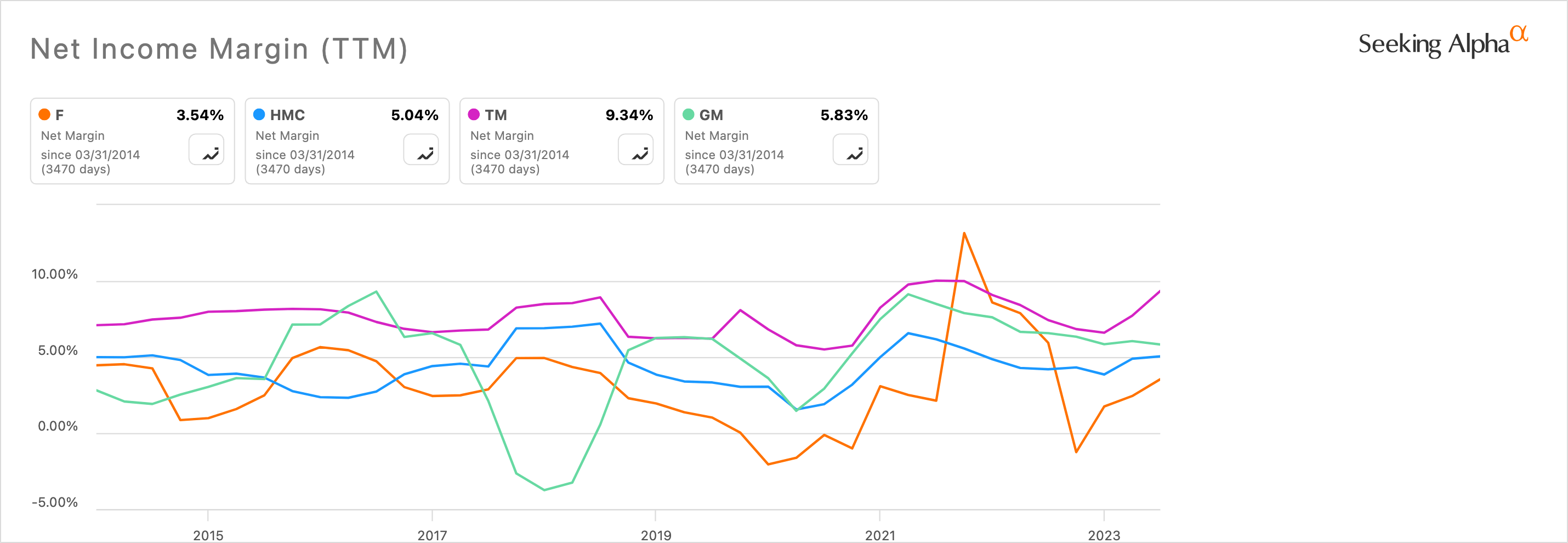

In addition, if I compare Ford’s margin growth against these three peers, we can see not only that the company has the worst net margins of the four but also that the firm’s profitability growth problem is common among the four peers over a 10-year period:

Author, Using Seeking Alpha

The income of Ford’s vehicles varies by model, and larger vehicles are generally more profitable. While the company could hone in on high-profitability vehicles, it likely also wants to maintain portfolio breadth to maintain its brand and saturated presence in automotive offerings. Arguably, a narrower, higher profitability product portfolio would be better for shareholders.

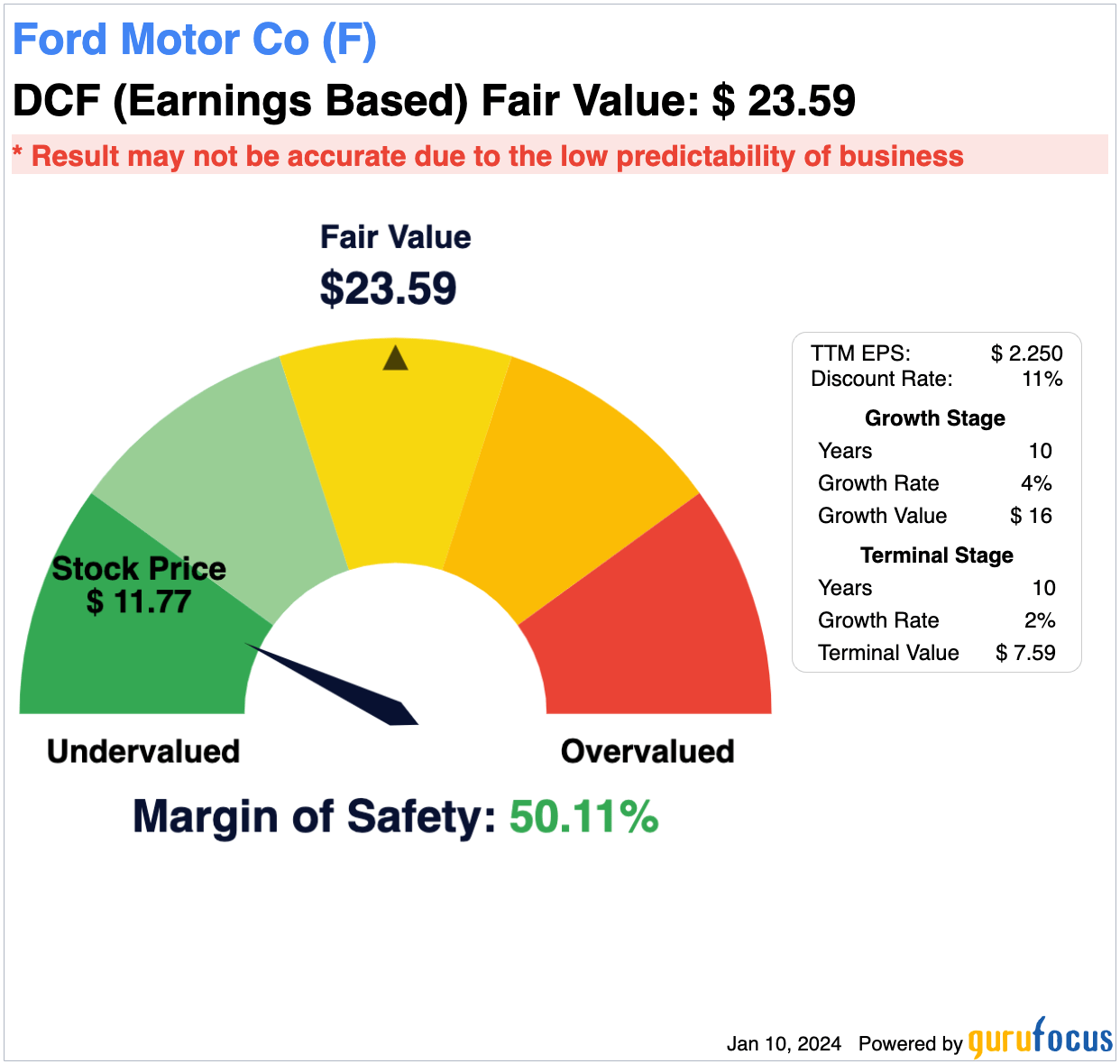

Based on an EPS without NRI discounted cash flow analysis, the company could be seen as around 50% below fair value based on an optimistic 4% 10-year growth stage and a 2% 10-year terminal stage. However, I think this suggests that the company will see increased earnings power through a more streamlined portfolio also honed in on EVs to keep up with changing demand.

Author, Using GuruFocus

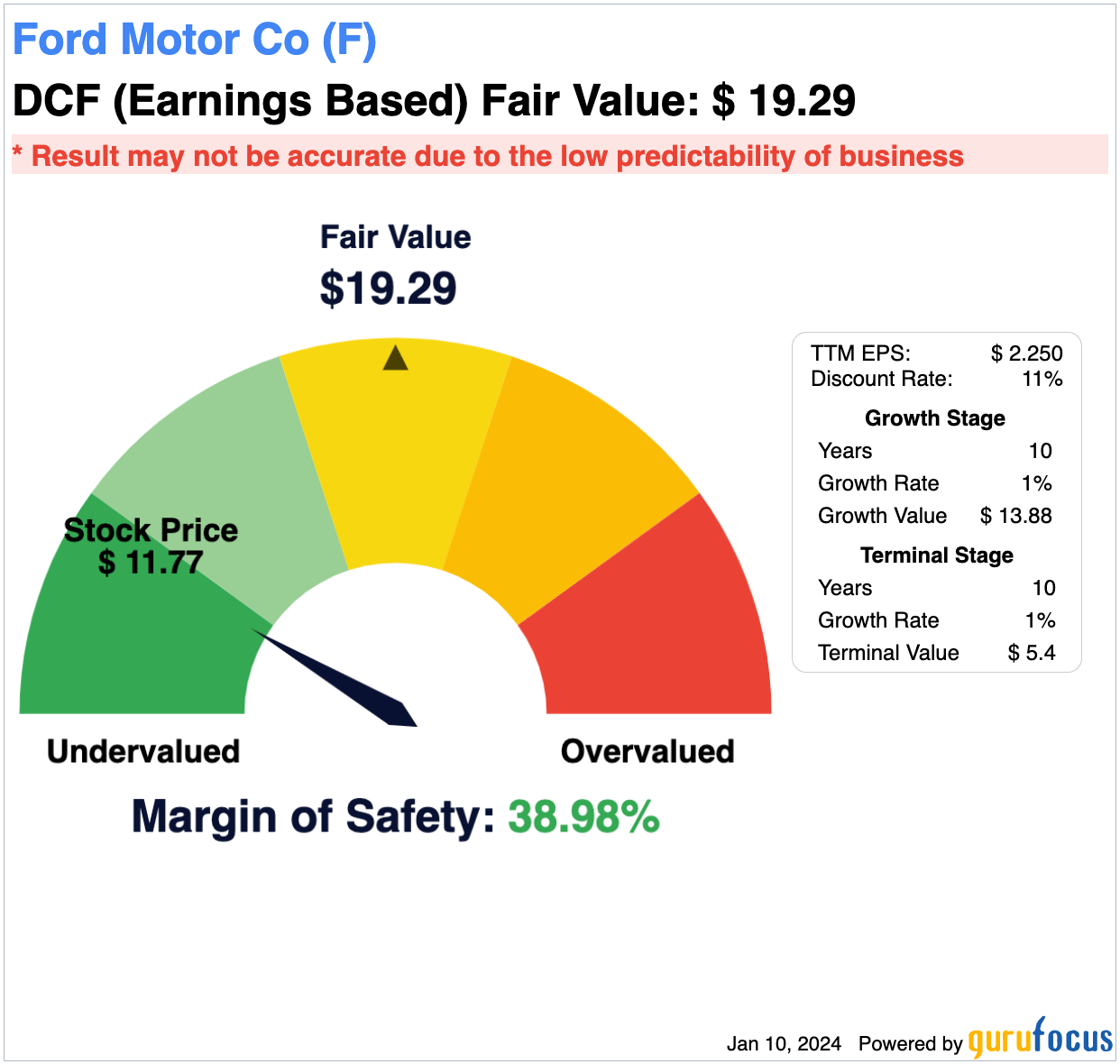

More realistically, the growth rate might look much slower, considering the relative all-time flatness in EPS growth exposed in the chart above. A mere 1% growth rate in EPS as an average over 20 years seems more in line with historical trends. Therefore, the fair value may be considered around $19 in my opinion, providing a margin of safety of around 40%. That indeed is a strong short-term value investment, but the prime issue I see with the stock is not its price but rather its long-term horizon potential, which I think evidently falls short. For example, even if the stock price rises 40% to ‘fair value’ in the next few years, that doesn’t mean it is going to grow at above index rates annually over the next two decades.

Author, Using GuruFocus

Company Positives

Ford is a great company, and it is very popular and has very well-made cars. The company is also collaborating with Tesla (TSLA) for EV charging, making its electric vehicles compatible with Tesla Superchargers. This is a strong move, in my opinion, and will work in favor of Ford as the economy shifts completely to electric cars in due course.

Its $9.2 billion conditional loan from the U.S. Department of Energy to build three battery plants supports its forward operational strategies, including a goal of 2 million EVs produced annually by 2026.

If Ford can successfully position itself as a top choice in the EV market over the long term, it could have a good price return in the next decade. That could mean that buying the stock now could pay off long term, and a Buy thesis would be supported by Ford continuing to be the leader in EV trucks as the market scales, for example, and honing their portfolio around these high-margin large vehicles and disposing of segments of the business not correlated to this.

Largest Risk

However, every automobile company is making shifts similar to this based on regulatory pressures and market trends. The real leaders in EVs will be heavily innovative and likely have moats in the battery charging segments, including supply, where Tesla will shine more than Ford. I think this is a very difficult time for traditional car manufacturers, and the shift to fully electric could cause declines in companies that aren’t technologically sophisticated enough to capture market interest.

This industry is going through the biggest technology-led transformation we’ve ever seen and some companies, new and old, are going to be left behind – John Lawler, Ford CFO.

I think Ford will see considerable success in the future, but whether the stock will achieve above-index returns does not seem likely to me. At the moment, I’m not convinced enough to put it in my portfolio.

Conclusion

Ford seems undervalued, but that’s not enough to make it a compelling investment, in my opinion. Its operations and financials show promise for the future, but the results are not guaranteed. Despite the potential undervaluation, I think there are other companies to invest in that provide more likely long-term upside than Ford, which is why my analyst rating is a Hold.

Q2 2024 Earnings Call Transcript")