PATRICK T. FALLON/AFP via Getty Images

The world is moving to more radically decarbonize, and energy storage will form a critical part of this zeitgeist, however, renewables come with an intermittency that reduces their ability to fully replace traditional fossil fuel alternatives. This backdrop is set to play out over the next decade and beyond. It’s a critical macrotrend and Fluence Energy (NASDAQ:FLNC) forms a pick-and-shovel play on the ramping rollout of solar and wind energy. The company offers battery-based energy storage products to utilities, developers, and industrial and commercial customers and was formed in 2017 as a joint venture between German technology giant Siemens (OTCPK:SIEGY) and US utility company AES Corporation (AES).

Fluenceenergy.com

The common shares started trading on the NASDAQ in 2021 but have dipped 21% from their IPO price for a $3.96 billion market cap. This places FLNC as an emerging leader in the energy storage space that’s a mix of well-established but floundering players like Stem, Inc. (STEM) and speculative upstarts chasing different battery chemistries to the conventional lithium-ion technology like Eos Energy (EOSE). There are a few tailwinds to highlight here, from lithium prices that have collapsed over the last year on market concerns around slowing EV adoption to growing government mandates for certain industries to adopt aggressive carbon reduction targets. However, volatile lithium prices also form a core risk for FLNC, as lithium plays a huge part in the company’s cost base.

Revenue, Gross Margins, And Profitability

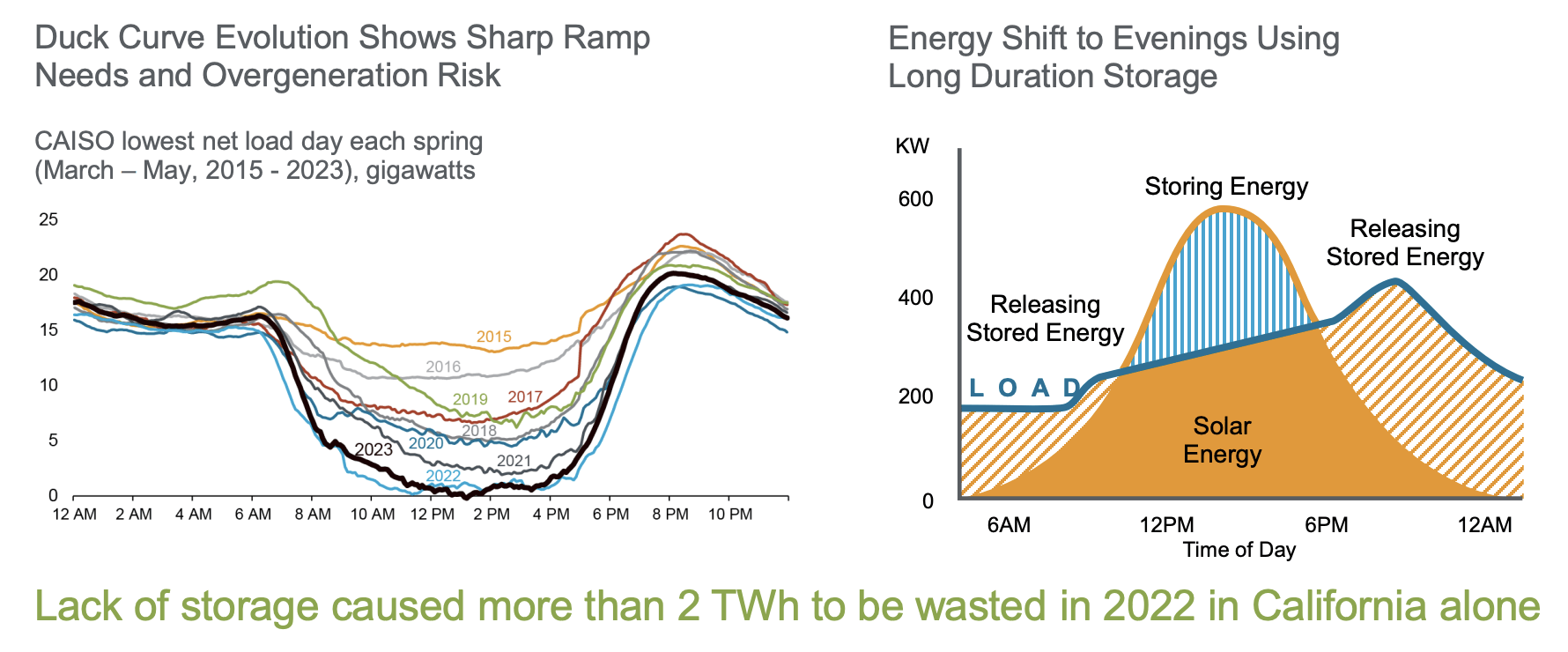

ESS Tech November 2023 Investor Presentation

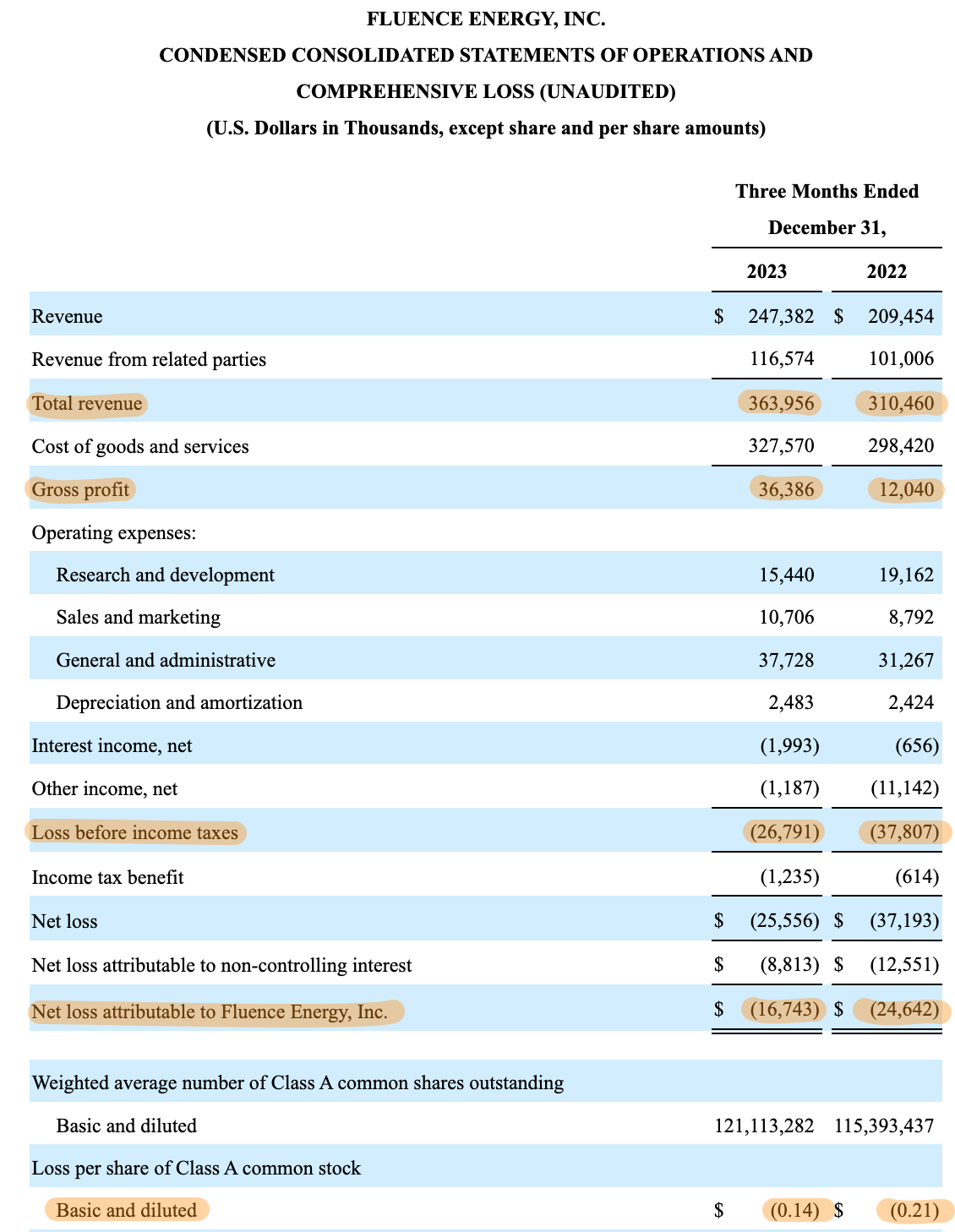

The solar duck curve highlights why there will be a perpetual wall of structural demand for energy storage, with batteries critical to addressing the timing mismatch between peak demand and solar electricity generation. FLNC generated $364 million in revenue for its most recent fiscal 2024 first quarter, up 17.2% from its year-ago comp, with its GAAP gross profit coming in at $36.39 million. This was up 200% from its year-ago comp, with double-digit gross margins at 10% also increasing 606 basis points from the year-ago figure. Net loss for the quarter came in at $16.7 million, down markedly from $37.8 million a year ago. This was a 6 cents per share year-over-year improvement.

Fluence Energy Fiscal 2024 First Quarter Form 10-Q

At the end of the first quarter, the company’s contracted backlog stood at roughly $3.7 billion, up $800 million from a $2.9 billion backlog at the end of its fiscal 2023. This growing backlog reflects the ramping adoption of renewables in the US, where utility-scale electricity generation from wind and solar grew to 13.7% in 2022 and is forecasted to account for 18% of total energy generation in 2024. This continued pull-up of renewables as a percent of utility-scale electricity generation is FLNC’s main investment pitch against what’s currently still losses from operations.

US Energy Information Administration

The risk of disruption to this macro story seems minimal, with 90% of new interconnection requests having been renewables and/or storage since 2019. This is creating a material total addressable market for Fluence and will form a backstop for revenue growth for years to come, with energy storage set to become at least a $56 billion market opportunity by 2027. The US Energy Information Administration expects roughly 20.8 gigawatts of battery storage capacity to be added from 2023 to 2025, growing to 30 gigawatts by 2025.

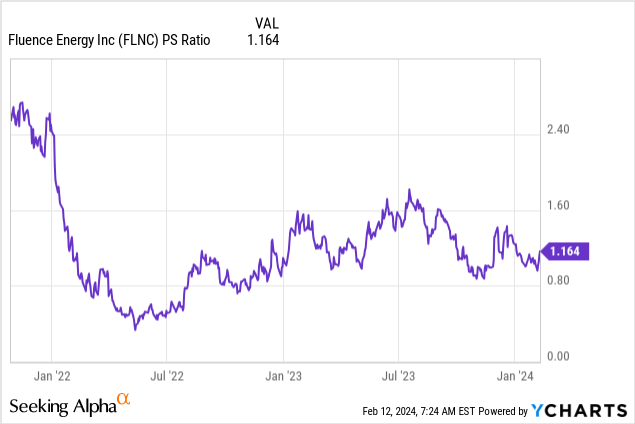

The current price-to-sales multiple of 1.16x is reasonable against FLNC’s growing TAM and is also in line with peer energy storage company Stem which is trading at a 1.15x multiple. FLNC has seen some price weakness in response to a secondary offering of 18 million common shares back in December. However, FLNC is not issuing any new shares, as the offering was Siemens and AES reducing their stake. Both firms owned over 60% of the common shares outstanding. The bigger fall in December was sparked by a lawsuit from Diablo, an owner of a battery energy storage project that had used FLNC, with Diablo pursuing at least $229 million plus damages. The court filing references overheating batteries and the batteries needing to be occasionally removed from the service. The lawsuit should be immaterial to its future financial performance as it has not slowed down growth, with FLNC surpassing 20 GWh of deployed and contracted storage systems globally in January. Critically, lithium-ion batteries will always come with the risk of overheating, with Tesla’s (TSLA) utility-scale batteries seeing overheating issues. Higher base interest rates for longer will also keep a lid on investor sentiment towards the commons, with a possible resurgence of inflation likely to spark downside volatility.

Fluence Energy Fiscal 2024 First Quarter Presentation

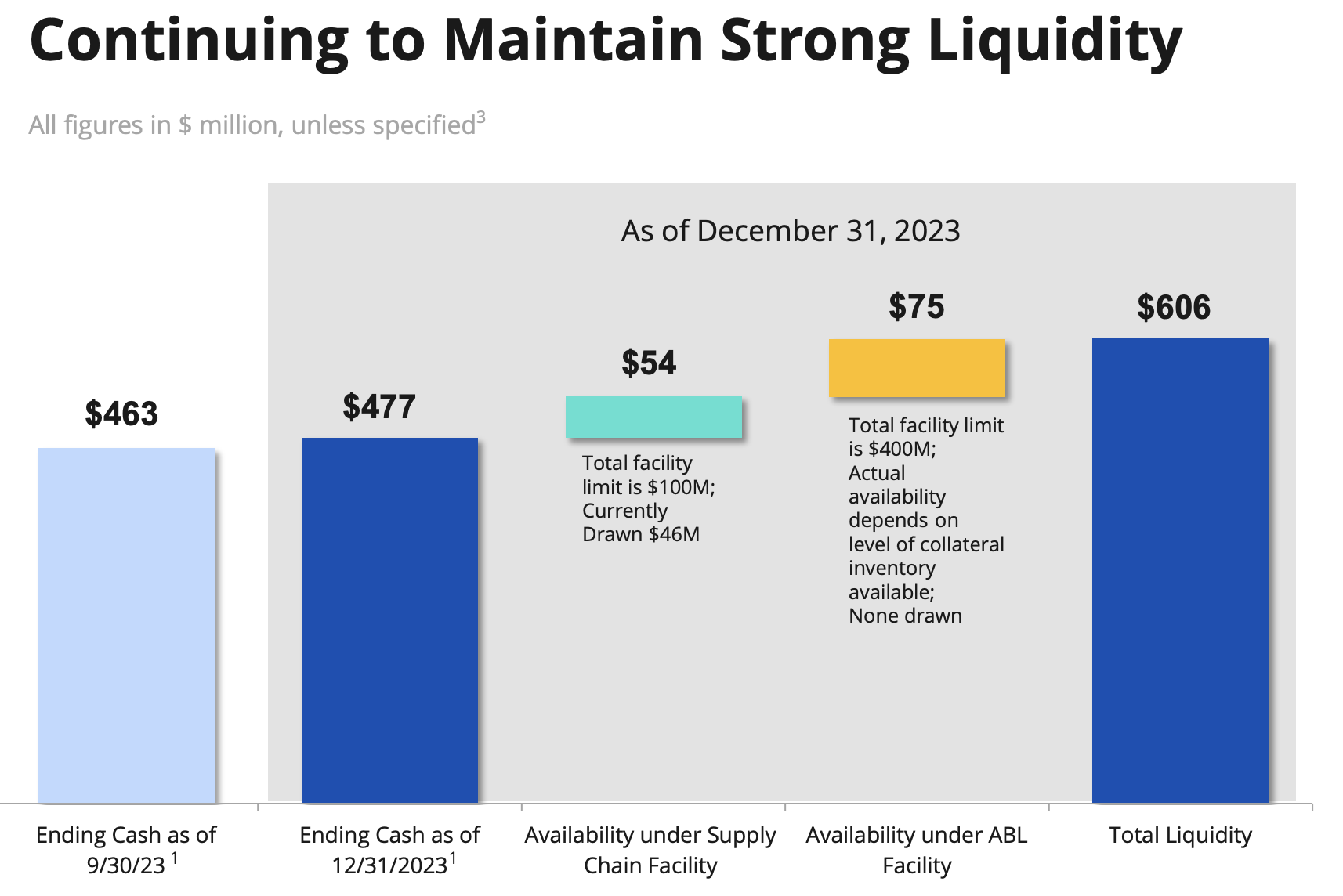

Lithium-ion is likely to remain the dominant technology for short-duration BESS, but the market is seeing an increasing amount of competing but early-stage technology like zinc and gravity-based batteries. These are however for longer-duration solutions. Overall, FLNC’s strong liquidity profile at $606 million at the end of the first quarter helps partially de-risk its investment proposition. The ticker is a play on a wider macrotrend with revenue and contracted backlog set for strong long-term growth. Profitability will be more volatile, and I’m rating this as a hold.

Q2 2024 Earnings Call Transcript")