PeopleImages

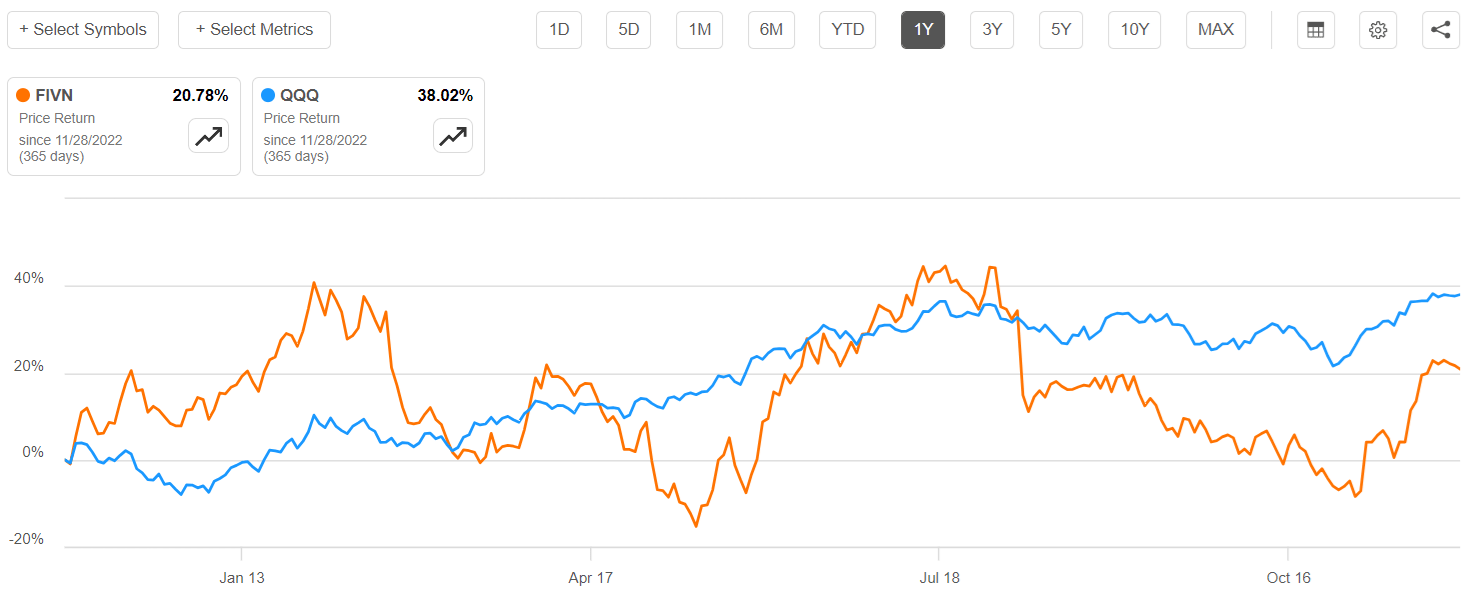

Five9 (NASDAQ:FIVN) which has its origins as a software provider for contact centers has evolved into a CX or customer interaction play by leveraging AI through its cloud platform. However, the stock’s underperformance of over 17% compared to the tech-heavy Invesco QQQ Trust ETF (QQQ) shows that the market has not realized the opportunity.

seekingalpha.com

By going through the suitability of its product offerings for contact centers (or call centers), this thesis aims to show that the stock is an opportunity at the current price of around $76 given its growth drivers. I also highlight the pain points as AI deployment projects do not always proceed as planned, amid a macroeconomic environment that does not necessarily encourage corporate expenditure.

First, I furnish an overview of how AI is being applied to contact centers while focusing on the productivity side of things.

Delivering AI through a Cloud Platform

New flavors of artificial intelligence appreciate Generative AI come with benefits. The reason is that ChatGPT, one of its applications has demonstrated how easy it is to communicate with intelligent LLMs (large language models) and procure quick answers to questions that can ultimately be integrated into a marketing or financial report. Looking beyond text generation, there are also voice applications with service providers appreciate Kaleyra (KLR) providing conversational AI for the automation of customer calls.

Now, whenever it comes to performing a task more rapidly or automating certain functions, it’s basically about improving workers’ output, with Boston Consulting Group estimating that Generative AI could boost productivity by 30% to 50% specifically in the field of customer services operations.

However, one also has to be realistic as these mouth-watering figures just represent potential gains depending on whether a company is an early adopter. The deployment approach is also key when it comes to changing the very interface used by customers to convey, or the way they communicate with call agents. In this respect, according to research by Glassbox, one of the barriers to implementing CX is the wide gap between what the technology makes possible and what customers go through. Consequently, one of the challenges is to create a personalized user go through because some people may simply find communicating through a chatbot to lack the human touch associated with talking to someone on a phone.

To address the issue, Five9 first focuses on enabling companies to better engage with their customers, before aiming to achieve a higher degree of automation through the use of digital channels appreciate chat and voice. For this purpose, Five9’s differentiated customer engagement approach elevates both users’ and agents’ experiences while synergizing the functions of the contact center workforce and AI through its CX platform.

Five9 Intelligent CX Platform (www.five9.com)

Going into more detail, data in the form of speech and text are analyzed in real-time to procure insights as to what happening during each customer-agent interaction. This way of proceeding helps to procure a global picture and drive improvement promptly and has become essential in an environment where many customers phone at the same time, each with his or her issues.

Translating Platform Strength into Revenues

Five9’s cloud-based approach has garnered interest from companies moving away from the on-premises business model as it saves them from the need to perform capital-intensive on-premises installations. At the same time, the pay-as-you-go model or monthly subscriptions exclude upfront fees while providing for on-demand computing resource allocation which makes a lot of sense for AI which as an innovative technology makes it harder to strategize exact requirements.

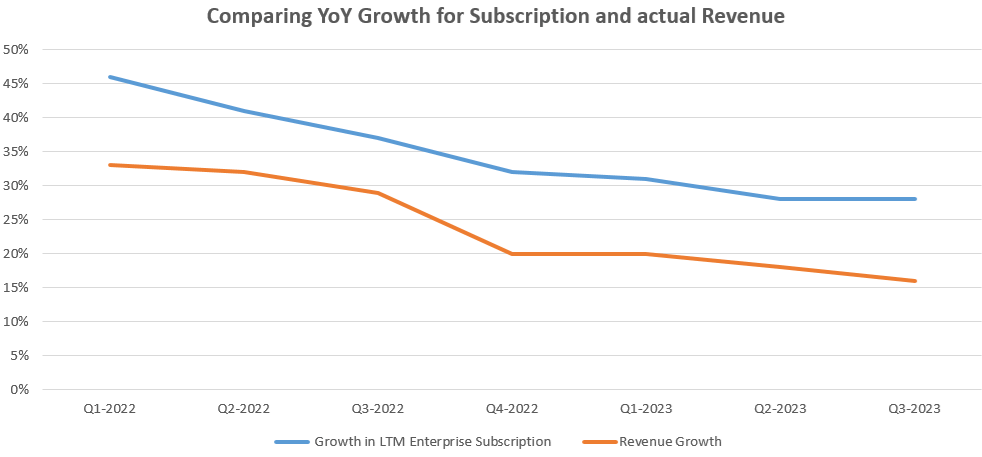

Wider uptake of its solutions has translated into higher recurring sales with an above 80% attach rate on above $1 million ARR (annual recurring revenues) deals during the third quarter of 2023 (Q3). Even then, the YoY revenue growth of only 16% appears to be on the low side compared to the 28.5% achieved one year earlier, with the orange chart below showing YoY revenue growth on a downtrend. However, a look at the subscription growth for this software-as-a-service play shows that things may be bottoming out.

Charts built using data from (www.seekingalpha.com)

For this matter, the enterprise subscription revenue growth measured on an LTM (last twelve months) basis has delivered much better growth of 28%. Digging deeper, there is a correlation between subscription growth (blue chart) and revenue growth as charted below showing that the refuse may be coming to an end. The reason is that subscription is a leading indicator as customers first have to be subscribed to the platform before the sales can be recognized. Therefore, this indicates a possible stabilization (bottoming) in YoY revenue growth probably around the 16% level.

However, the consensus YoY revenue growth estimates by analysts for the fourth quarter (Q4) are lower, or 14.3%, which implies that there is a possibility of beating the topline when financial results are announced around February 22. This idea of a revenue beat is advance supported by the dollar-based retention rate (on a sequential basis) improving (by being “either flat or slightly down“) in Q4 compared to a 2% drop in Q3.

Valuations and Macroeconomic Risks

Noteworthily, this is a company that has beaten revenue expectations in the last 12 successive quarters. Also, in the aftermath of Q3’s results on November 2 when it beat both the topline and bottom-line, the shares jumped by more than 10%. Now, considering that the stock is trading at 6.16x sales, which is at a 56% discount to its five-year average of 13.93x, a target of $89.1 (76.22 x 1.17) can be envisaged based on a 17% adjustment of the current share price of $76.22. This is a fair target as the stock is also trading at a 17% discount to QQQ.

Valuation Metrics (seekingalpha.com)

To advance defend my optimism, the CFO also evoked an optimistic outlook during Q3’s earnings call when mentioning that his company is “well positioned to speed up the business” but, he also cautions that this is subject to macroeconomic conditions improving.

Now, 87% of its overall revenues came from the U.S. in Q3, a country where GDP growth is expected to slow down to 1.5% in 2024, from 2.4% this year based on the easing of monetary policy by the Federal Reserve. This outlook also assumes that there is an economic soft-landing or no recession despite interest rates remaining at an uncomfortably high level.

Adopting a cautionary tone, some of Five9’s customers may not proceed with RFPs or inquire for Proposals which is the preliminary step before subscribing at the first signs of deteriorating macros. Thus, news of faltering economic growth could furnish the stock volatile as part of the general risk-off market sentiment as is often the case when there is a high degree of uncertainty. Consequently, the stock could fall back to its $55-$60 uphold level and remain there for some time.

However, after the initial sell-off, investors should gradually discern the particular way Five9 has adapted its product offerings for contact center automation that has become relevant to inflationary pressures. Thus, as mentioned earlier these can drive productivity by enhancing the operational efficiency of contact centers while also reducing customer expect times and optimizing costs. The company is also banking on geographical diversification as it continues to extend internationally while at the same time, the large customer group which generates revenues in the $1 million to $5 million range has become a big growth driver.

Product Relevance and Growth Drivers defend the Buy

Five9 can also rely on inorganic growth through the Aceyus acquisition which on top enhances its position for the $1 million-plus ARR customers. For investors, Aceyus is a specialist in data integration and analytics capabilities and its customers include Fortune 100 companies including some where it works jointly with Five9. As a result of the merger, LTM dollar-based retention rate which is currently 110% is expected to gradually progress towards the 130% mark by 2027.

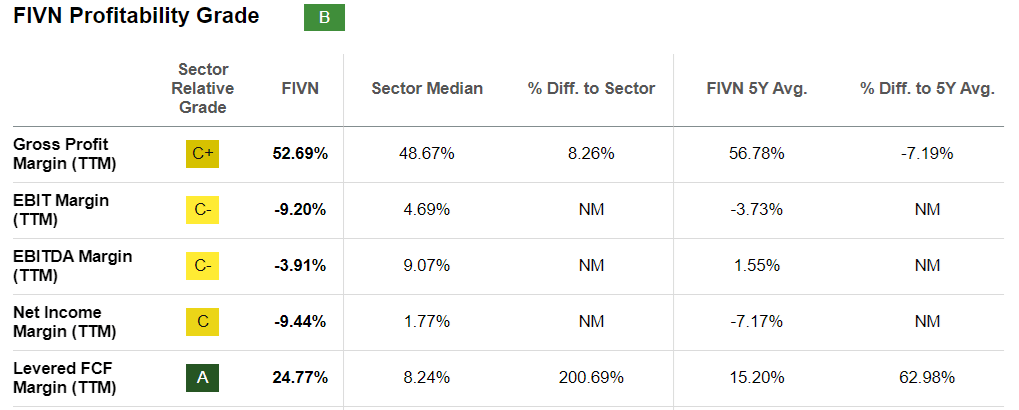

Now, winning over customers with higher spending power provides for a better ARPU which can result in better profitability due to relatively less marketing dollars spent as a percentage of sales instead of generating the same amount through many smaller accounts. At the same time, the company has seen success with more implementations being carried out by (third-party) partners for about one year. As a result of these two factors, margins in the 51% to 53% range during the last seven quarters could scale up to 70% according to the management.

However, I believe this may take more time since when a company expands its footprint through a partnership strategy, this can happen at the expense of profitability as Five9 has to share part of the profits in contrast to when going standalone. Therefore, the company should first achieve a certain scale of operations to achieve the 70% figure. Still, Five9’s FCF margins of 24.77%, which is above its five-year average by 63% tend to suggest that its sales teams can negotiate contracts with a higher portion of advanced payments. This may be due to less competition in the contact-center-as-a-service marketplace.

www.seekingalpha.com

This strong cash generation capacity which is also above the median for the IT sector by over 200% should benefit the balance sheet which boasted $700.3 million in cash against $795.6 million of debt at the end of Q3. To this end, the cash flow statement shows outflows of $80.6 million in connection with the Aceyus acquisition.

In conclusion, this thesis has shown that Five9’s contact-center-as-a-service approach to AI deployment together with the Aceyus acquisition are two growth drivers that position it well in the current macroeconomic environment where despite the economy continuing to be resilient, uncertainty persists because of the lagging effects of high-interest rates. Here, it is precisely the company’s strong cash-generating capacity while increasing exposure to larger enterprises which makes it a relevant investment at $76.22.

Q2 2024 Earnings Call Transcript")