davelogan/iStock via Getty Images

FirstEnergy (NYSE:FE) is a holding company for ten electric utility companies in the Midwest and Mid-Atlantic. Collectively they serve over 6.2 million customers in Ohio, Pennsylvania, West Virginia, Maryland, New Jersey, and New York. The company was incorporated in 1996 and became a wholly regulated utility in 2016. It is currently head quartered in Akron, Ohio. Some of the familiar subsidiaries include Monongahela Power, The Cleveland Electric Illuminating Company, Jersey Central Power & Light, Metropolitan Edison, Toledo Edison and Ohio Edison. The total generating capacity of the company is 3,580 megawatts (following the sale of some generation assets), and the current market cap is $20.76 billion, making it the fifteenth largest US electric utility. Since peak demand exceeds generating capacity on occasion, FirstEnergy must make up the difference by buying electricity in the wholesale market. Standard & Poor’s rates FirstEnergy as BBB-, or lower investment grade.

Share Price History (Seeking Alpha Charting)

The recent high for the stock was February 2020, when shares reached $52.23. In July of that year they dropped precipitously from $42.14 to $29.00 over the course of a week, a change of 31.2%. This happened when news broke of a bribery scandal involving FirstEnergy, with $60 million and a legislative bill that “halved the renewable power that utilities were required to buy, eliminated energy efficiency laws, and handed a billion dollars to the state’s two nuclear power plants…” In 2021, FE entered into a deferred prosecution agreement (DPA) over three years as outlined in the 2022 Annual Report, contingent on the company’s continued cooperation with the US Attorney, with a penalty of $230 million (about $0.40 per share) and disclosure of any and all payments benefiting public officials. There are two more payments to be made, one for $45.0 million in 2024 ($0.08 per share) and another for $25.0 million in 2025 ($0.04 per share). However it appears the story is not over yet with investigations underway by the state and individual investors.

Before the scandal, FirstEnergy had three nuclear plants: Perry and Davis-Besse (both in Ohio) and Beaver Valley (in Pennsylvania). These were part of First Energy Solutions, the unregulated portion of FirstEnergy. After the controversy with the payoffs, First Energy Solutions declared bankruptcy and re-emerged as Energy Harbor, a company now completely unrelated to FirstEnergy, and with the nuclear plants as its assets. FirstEnergy had claimed that “renewable energy and cheaper fuels had made both nuclear plants unprofitable.”

An Uneven History of Dividend Payments

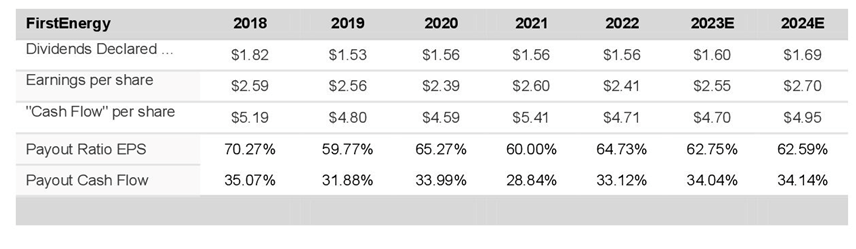

Even before the bribery scandal came to light in 2020, the dividend history was uneven. If you are buying this stock for dividend income, you should not expect consistency. The yield is a somewhat attractive 4.53% and the quarterly dividend was just increased in November to $0.41 from $0.39 per share. However the dividend was $0.39 per quarter from February 2020 to August 2023, a stretch of three and a half years. It was in July 2021 when the company agreed to pay a $230 million dollar fine to settle its bribery case, so this may have limited dividend growth. Before this the dividend was cut from $0.55 to $0.36 in February 2014, and stayed fixed at this rate through February 2019 when it was increased to $0.38 per quarter.

Despite the inconsistent dividend, the payout ratio has remained an acceptable 60.0-70.27% of earnings and 28.84% to 35.07% based on cash flow. The targeted payout ratio is 60.0-70.0%. With pension and investment funds now litigating against FirstEnergy, I would say that any future dividend increases are uncertain and may not be as high as the most recent 5.0% increase, although the company does say it plans to increase the dividend in line with 6.0-8.0% earnings growth. The quarterly dividend payable for March 1 was recently announced as $0.41.

Payout Ratio Over Time (Author Calculated and Value Line)

The current yield for FirstEnergy is 4.53%. It compares favorably with peers like American Electric Power (AEP) at 4.38%, Duke Energy (DUK) at 4.19%, Pinnacle West (PNW) at 4.95%, Consolidated Edison (ED) at 3.61%, and Southern Company (SO) at 4.0%.

Shares are Undervalued, Mathematically

In the third quarter 2023, FirstEnergy had operating earnings per share of $0.88 versus $0.79 in the third quarter 2022. Part of this gain was from tax benefits and lower labor costs. Operating earnings consensus for the year was narrowed to $2.49 to $2.59 per share. The company has a 6.0% to 8% annual earnings growth target.

GAAP earnings per share were $1.99 in 2020, $2.35 in 2021, and $0.71 in 2022. Operating earnings were $2.39 in 2020, $2.60 in 2021, and $2.41 in 2022. Of course, part of the difference was one-time fines paid.

In order to value FirstEnergy shares I have used a P/E ratio derived from comparable utilities and a discounted cash flow. Utility shares have been attractively valued of late, partly because of the rise in the federal funds rate. Six month treasuries are currently paying 5.32%, well above the average utility dividend yield of 4.0%. As Morningstar noted, this is the first time treasury yields have exceeded utility dividends since 2008-2009, and the 16.0 overall P/E ratio for the sector is the lowest it has been since 2009. Information from Duff and Phelps Research showed that “utilities were the worst-performing sector in the S&P 500, dropping 15.5% YTD through October 31, 2023, while the broader S&P 500 rose 10.7% during the same time period.” This has made valuations more attractive, but of course now in December, a portion of this trend has been reversed.

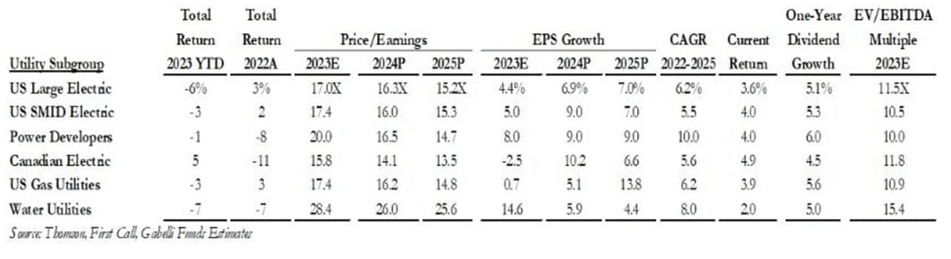

Gabelli Funds provides a semi-annual survey of utility P/E ratios by segment whether electric, gas, or blended. In the company’s Utilities Mid-Year Update it reported that “electric utility valuation multiples have declined from 23x forward earnings in early 2020 to 17x 2023 and 16x 2024 earnings estimates.” The most recent table of multiples if provided below.

Gabelli Research Utility Survey (Gabelli Funds)

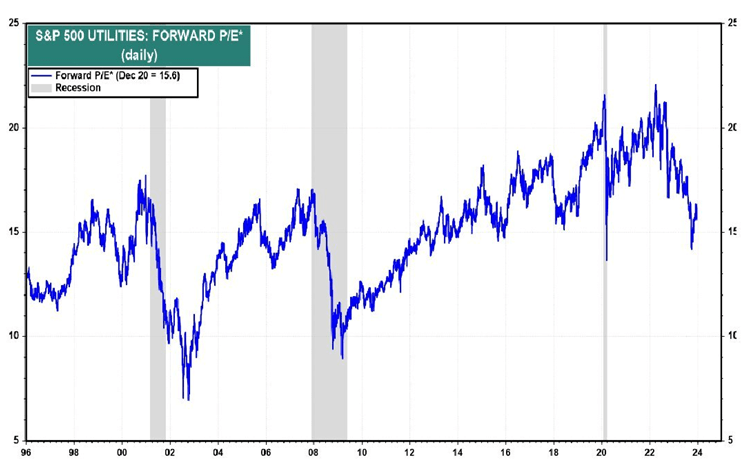

I also consulted Yardeni Research, which provides price/earnings data on utilities as well as other industries. The current forward P/E ratio reported by Yardeni for the S&P 500 utilities is 15.6 as of December 20th. Using the 2024 projected EPS of $2.70 with the 15.6 P/E ratio, the fair value of FirstEnergy’s shares would be $42.14.

S&P 500 Utility Multiples (Yardeni Research)

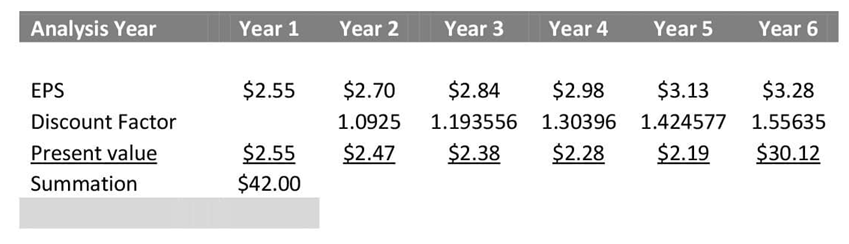

As I typically do, I have also done a five-year discounted cash flow to value FirstEnergy shares. The company has projected an earnings growth rate of 6.0-8.0% moving forward, however, after recent issues I am skeptical about this and have estimated a lower rate of 5.0%. I began the discounted cash flow with the consensus earnings midpoint of $2.55 for this year and $2.70 for next year. For the discount rate, I used 9.25%, just below the average annual return of the S&P 500, which is about 9.8%. The justification is that this is a fully regulated electric utility, so in theory lower risk. The reversion rate used in this analysis was 7.0%, 225 basis points below the discount rate.

Discounted Cash Flow (Author Calculated)

The numbers produced by these two methods indicate a fair value of $42.00 to $42.14, a very tight range, so mathematically anything below $42.00 would be a buy. The current share price is $36.23, so shares are about 14.0% undervalued, but there are other considerations besides just the price.

The Change to Renewables

All US utilities are subject to two regulatory acts that will guide the transition to a carbon free energy profile. Probably the most important is the Inflation Reduction Act, which has incentives for utilities to move away from coal power generation. It requires a 40.0% reduction in emissions by 2030, based on a 2005 benchmark, and net-zero emissions by 2050. There are significant tax credits for renewable power generation (by solar, wind, hydro and geothermal) and $2.0 billion in loans to update transmission infrastructure. Also important is the Bipartisan Infrastructure Law which was passed in 2022. It will provide billions in grant funds to “upgrade our power infrastructure, by building thousands of miles of new, resilient transmission lines to facilitate the expansion of renewables.”

Currently FirstEnergy has three coal fired plants and a hydro facility. It used to have three nuclear facilities that would have technically qualified as “clean energy” but they are now owned by Energy Harbor (OTC:ENGH). These were the Davis-Besse Nuclear Power Station with 894 megawatt generating capability, the Perry Nuclear Power Plant with 3500 megawatts, and Beaver Valley with 1,815 megawatts. Energy Harbor will now use these facilities to sell power on the open market. First Energy had planned to close them in 2018.

One renewable project being pursued by FirstEnergy right now is offshore wind power generation. This project is off the coast of New Jersey and will produce 7,500 megawatts of power when completed in 2035. It is being developed under FirstEnergy subsidiary Jersey Central Power & Light. The total cost of the project is $1.1 billion and it will be paid for by New Jersey retail electric customers. Another FirstEnergy renewable project is currently being hooked up to the grid: two solar farms in southern Pennsylvania that will together generate 200 megawatts of power. FirstEnergy is also completing a solar project in West Virginia.

Long-Term Debt is on the High Side

First Energy had $21.2 billion in long-term debt as of the end of 2022, or 66.6% of total capitalization and 45.9% of total assets. In 2021, long-term debt was $22.2 billion, or 71.9% of total capitalization and 48.9% of total assets, so the ratios improved in 2022. In 2020, long-term debt was $22.1 billion and 75.4% of total capitalization and 49.7% of total assets. The volume of long-term debt is definitely headed in the right direction, but it is elevated when compared to most utilities.

According to Edison Electric Institute FirstEnergy “completed a sale in May 2022 of a 20% ownership interest in FirstEnergy Transmission for $2.4 billion…(and) used proceeds from its asset sales and equity issuances to pay down $2.4 billion of parent company debt.” In 2023, the company sold another 30% interest in FirstEnergy Transmission for $3.5 billion to Brookfield Super-Core Infrastructure Partners, again to pay down debt.

Generally Favorable Regulatory Environment

FirstEnergy’s average electric rate in 2022 was $0.1193 per Kilowatt hour, placing it in the middle of electric rates charged by US utilities. Peers like NextEra (NEE) charged $0.1220, AES Corporation (AES) was $0.1186, Duke Energy (DUK) averaged $0.1044, Evergy (EVRG) was $0.1097, Dominion Energy (D) was $0.1117, and Southern Company (SO) was $0.1229. Consolidated Edison (ED) was one of the most expensive in the country at $0.2643.

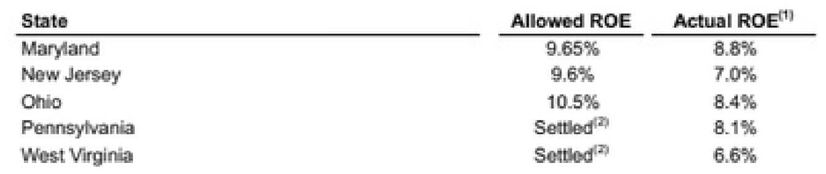

I believe FirstEnergy generally operates in a generally favorable regulatory environment. The rate base was $26.0 billion in 2022 with 7.0% annual rate base growth estimated through 2024 and 2025. Each of the states in which FirstEnergy operates – Pennsylvania, Maryland, West Virginia, New Jersey, New York, and Ohio – have utility boards with governor appointed members. They vary in size from three in West Virginia to seven in New York, but appointed members tend to be more balanced with the interests of the public and the utility. Elected utility board members can often be more customer-oriented as their tenure is election dependent. According to FirstEnergy “A favorable outcome was recently concluded in the Maryland rate case, while settlement talks are still underway in West Virginia and New Jersey. Base rate cases will likely be filed in Ohio and Pennsylvania next year.” That said, there have been complaints about regulatory lag in Ohio, with decisions on rate appeals taking a long time to be resolved.

According to Edison Electric Institute, the average awarded ROE for electric utilities in 2022 was 9.47%, up slightly from 9.40% from 2021. Regulatory lag (the time to get an approval) averaged around 8.01 months. Allowed return on equity for FirstEnergy’s subsidiaries are about equal to these reported averages.

Return on Equity (2022 Annual Report)

Risks to Outlook

The first risk that comes to mind for FirstEnergy is legal risk. There are still investor and mutual fund lawsuits to come and these have recently unearthed more documents to use in litigation (CALPERS is among those involved). So the story is not yet over from the 2020 scandal and shareholder loss of value. Another consideration is that many utilities have experienced declines in earnings due to warmer weather and that was certainly the case in 2022-23 with record warm temperatures in Ohio and in Pennsylvania. Finally the long-term debt of FirstEnergy is at rather high ratios when compared to other utilities. It is timely that the Federal Reserve plans to lower rates in 2024, although we don’t know when or by how much.

Conclusion

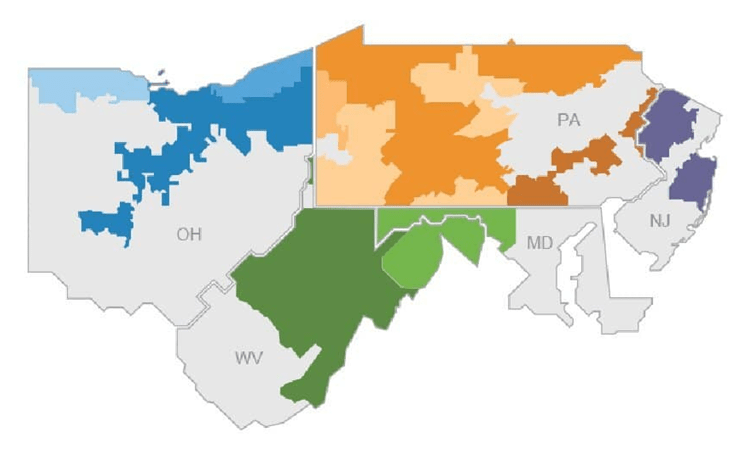

FirstEnergy reminds me of a house that needs renovating. There are good bones, with the utility’s territory of Ohio, Pennsylvania, New Jersey, West Virginia, Maryland and New York (see below). These are areas with established, dense populations that will continue to demand energy. But there are changes that need to be made and there’s still some uncertainty as to what surprises you may get if you buy shares. Among those needed changes are that FirstEnergy should have higher generating capacity and it should be further along in its transition to renewable energy. If I were a perspective investor, I would wait until all the likely lawsuits have concluded, despite what seems an attractive valuation today. In the plus column, however, Brian Tierney, a 23-year veteran of American electric Power, took over as CEO earlier this year. Maybe shares will look better in a couple years.

FirstEnergy Market Area (2023 investor Presentation)

Q2 2024 Earnings Call Transcript")