stocknshares

As the market navigates through the uncertainties of 2023, investors are increasingly looking for stocks that offer a compelling blend of growth potential, resilience, and value. In the current landscape, First Citizens BancShares (NASDAQ:FCNCA) (OTCPK:FCNCB) emerges as a candidate worth serious consideration for your 2024 portfolio.

A Southeast Powerhouse with Strategic Acquisitions

FCNCA is a leading regional bank headquartered in North Carolina. The bank has been led by the Holding family for more than 100 years, including the current Chairman and CEO Frank Holding Jr.

A detailed summary of the bank’s history is available on the First Citizens BancShares website. Some excerpts are below:

- 1898 Founded in North Carolina- “Our company was founded as the Bank of Smithfield with just $10,000 of capital. We were Johnston County’s sole bank and served primarily agricultural customers. Steady growth quickly became our hallmark.”

- 1935 R.P. Holding Leads the Way ” After 17 years of astute leadership, R.P. Holding was elected president and chairman of First-Citizens Bank & Trust Company. The bank’s branch network stretched beyond Smithfield to Raleigh and into Eastern North Carolina.”

- 1957 The Holding Legacy Continues- “Upon the death of R.P. Holding, leadership passed to his three sons, the second generation of Holdings, who were all under 32 years old-Chairman Robert Holding, Jr. (standing), President Lewis R. Holding (right) and Vice President Frank B. Holding (left).”

- 1994 Expanding to New States- “First Citizens began operating our first-ever branches outside of our home state of North Carolina when we acquired a bank based in West Virginia.”

- 2022 Growing Our Footprint- “Our merger with CIT marked a major milestone for First Citizens and established us as a top 20 US bank based on asset size. Joining forces enables us to serve a broader spectrum of businesses and individuals, while offering even more convenience, scale and value.”

The bank has a strong footprint across the Southeast, and boasts a long history of organic growth and strategic acquisitions. Between 1971 and 2020, there were about twenty small acquisitions. Many of these acquisitions were FDIC-assisted deals. Frank Holding Jr. has managed to steadily expand the First Citizens franchise in a highly cost-effective manner by acquiring failed banks.

Two recent large deals were much larger than usual- the acquisition of CIT Group in 2022 which roughly doubled the company size and Silicon Valley Bank (SVB) in 2023 which doubled its size yet again. These acquisitions have significantly reshaped the bank’s landscape and future trajectory. It is now a top twenty bank with about $210 billion in assets.

CIT Acquisition: Expands Reach and Diversifies Revenue Stream

The acquisition of CIT, a national leader in lending to middle-market businesses, significantly expanded FCNCA’s reach beyond its traditional Southeast footprint. CIT provides access to new markets, customer segments, and revenue streams, including commercial banking, lending, and leasing. The CIT integration initially caused some earnings headwinds, but the long-term potential, cross-selling opportunities and cost synergies are quite valuable.

SVB Acquisition: Tapping into the Tech Boom

In March, 2023, the FDIC announced that FCNCA won a bid to purchase Silicon Valley Bridge Bank and SVB Private Bank when SVB entered FDIC receivership on March 12. Silicon Valley Bridge Bank is the US operations of SVB excluding the investment bank.

The FDIC likes dealing with First Citizens bank. As part of the acquisition, the FDIC received equity appreciation rights in First Citizens common stock with a value of $500 million. First Citizens and the FDIC also entered into a “loss-share transaction” where the FDIC absorbs part of the loss on the commercial loans purchased from the SVB Bridge Bank.

SVB’s failure occurred because the previous management completely mishandled the underlying bank portfolio. They invested strong deposit growth into longer duration securities that caused the bank to have large unrealized loss positions when interest rates rose rapidly in 2022 and early 2023, and this led to the shutdown of the bank by the FDIC.

But the underlying business of SVB is still quite valuable. SVB was a premier bank serving the technology industry and the innovation economy. It has greatly benefited FCNCA’s diversification efforts. SVB’s expertise in technology banking, coupled with its strong presence in key growth markets like California, positions FCNCA to capitalize on the growing tech sector. This strategic move aligns very well with the bank’s focus on high-growth markets and specialty banking businesses. I believe that even better times for the SVB franchise may occur under the strong leadership of First Citizens management team.

Valuation Advantages Compared to Peers

Despite its attractive acquisition history and growth prospects, FCNCA currently trades at a discount compared to its regional bank peers. The Seeking Alpha Financial page has the forward P/E Non-GAAP TTM of 8.06 compared to the sector Median of 10.49. The P/E GAAP TTM is only 1.87, but that is somewhat distorted by the recent SVB acquisition. The shares trade at 1.03 times tangible book value which is a 14% discount to its sector peers, but I believe its total return potential is better than its peers.

Key Drivers for 2024 Growth

Several factors suggest FCNCA is poised for a strong performance in 2024:

- Continued integration of CIT and SVB: The cross-selling and cost synergy opportunities from these acquisitions are expected to materialize in 2024, boosting profitability and efficiency.

- Unique Family Ownership Structure: The Holding family owns about 20% of the shares and more than 50% of the voting shares. Under the family’s leadership, the bank has consistently produced above average growth in the most important metrics for investors- tangible book value, revenue per share and earnings per share.

- Strong regional economy: The Southeast, FCNCA’s core market, is one of the fastest-growing regions in the US, providing a solid foundation for organic growth.

- Improvements to SVB management: The previous SVB business model had a weakness because it generated far more in deposits than loans, which caused the underlying securities portfolio to be way too large. Technology companies tend to generate a lot of cash and often do not need to borrow much. Apple is a good example, sitting on $60 billion in cash compared to about $10 million in loans.

- Under First Citizen’s management, there is now much more capacity to generate high quality loans to provide balance for the large deposits. This is largely due to the acquisition of CIT in 2020. CIT actually had the opposite problem, because it tended to provide more loans than it could generate in deposits. Pairing the SVB business with the CIT business is a very good match.

- Focus on specialty banking: FCNCA’s strengths in areas like wealth management, commercial banking, and technology banking are expected to outperform as these segments experience increased demand.

- Thinking long term: The Holding family has continuously led First Citizens Bank for over 100 years. The management team clearly thinks and invests for the long term.

Potential Risks and Considerations

While FCNCA offers promising long term opportunities, it’s important to acknowledge some potential risks:

- Economic slowdown: A broader economic downturn could negatively impact loan demand and bank profitability. There is also some credit risk in SVB’s early stage loans, but these are currently less than 2% of First Citizens total loans.

- Execution challenges: Integrating large acquisitions like CIT and SVB can be complex and it may take longer than expected to realize the full potential benefits.

- Key Person Risk: The Holding family has led First Citizens for over 100 years and has helped the bank expand nationally. If the Holding family should ever decide to sell off a lot of their FCNCA shares, it could lead to some underperformance. Another risk is that some of the key SVB executives may decide to leave the bank.

- Competition: After SVB failed, some employees defected to other banks. The franchise was also split from the international business, and First Citizens did not acquire the investment bank. Because of this, SVB has more competition than before. The banking industry is highly competitive, and FCNCA faces some stiff competition from established players and new entrants. But I believe that the innovation community will want to see SVB rebuild its former franchise, especially because of First Citizens strong management team.

- Interest Rate Risk: If interest rates trend a lot lower, this could reduce the net interest income benefit earned from the balance sheet assets inherited from SVB.

Overall, FCNCA’s strategic acquisitions, attractive valuation, strong regional footprint, and focus on high-growth segments make it a compelling investment proposition for 2024. While risks exist, the potential rewards appear to outweigh them for investors seeking a well-rounded, growth-oriented bank stock with a strong track record and promising future prospects.

Additional Points to Consider

- Dividend policy: FCNCA offers a modest dividend yield of about 0.5%. It is really more of a total return investment. But it can be a good holding in a taxable account, especially for those in a higher tax bracket.

- Management team: FCNCA has a strong and experienced management team with a proven track record of success.

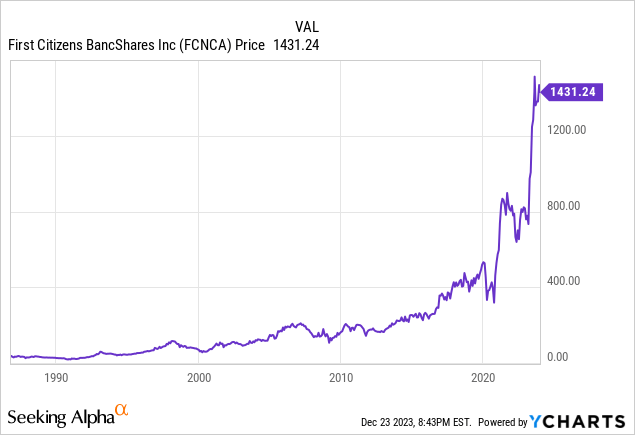

- Technical analysis: While not a guarantee of future performance, technical indicators suggest a potential breakout to all time highs for FCNCA in 2024. Its long term chart is a thing of beauty, and shows consistently good long term performance.

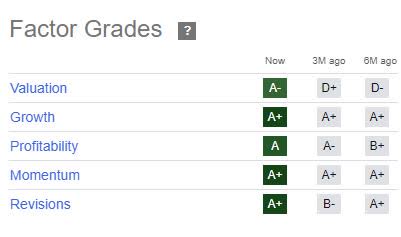

The Seeking Alpha Quant Model Loves FCNCA

I have come to respect the opinions of the Seeking Alpha Quant Model, especially when it gives a “Strong Buy”. Its backtested strategy has beaten the S&P 500 every year since 2011. https://seekingalpha.com/performance/quant

FCNCA currently has a Strong buy rating with a nearly perfect score of 4.92 out of 5. It currently scores at least an A in all five factor categories- Valuation, Growth, Profitability, Momentum and Revisions. In the Financials sector, it is ranked 13 out of 696 stocks. In the Diversified Banks industry group, it is ranked 4 out of 67.

FCNCA Seeking Alpha Quant Ratings (Seeking Alpha)

Two Different Share Classes of Common Stock

First Citizens has two share classes of common stock outstanding. FCNCA are the Class A shares which have one vote per share. FCNCB are the Class B shares which have 16 votes per share. Aside from the voting rights difference, both share classes have the same economic interest, including dividend payments.

The Class B shares normally trade at a significant discount to the A shares, in spite of their greater voting power. The last close on December 22 was $1,431.24 for the A shares and $1,269.98 for the B shares. Why is that? There are several reasons.

- Class B shares trade over the counter. Class A shares are listed on the NASDAQ.

- The average 90 day trading volume for the A shares is 67,928 shares. For the B shares, the average volume is only 112 shares. (Source: Yahoo Finance). On some days, there is no volume in the B’s at all, and quite often the volume is exactly 100 shares.

- Bid-Asked Spread: The spread on the A shares is often only one or two dollars. The spread on the B shares is usually ten dollars or higher, with very limited size on the bid and asked.

- There are stock options available for FCNCA, but not for FCNCB.

Future Long Term Catalyst: Possible Addition to S&P 500

IF FCNCA continues growing, at some point it may become a candidate for the S&P 500. This is probably unlikely in the short term, because the Holding family controls so much of the float and more than 50% of the voting rights. But things could change in the future.

At some point, the Holding family may want to sell off some of their holdings. That would increase the trading float of the stock, which could make it more likely that FCNCA could be added to the S&P 500. They could also authorize a stock split to bring in more retail investors.

Summary

For a long term investor, that does not expect to trade the stock for awhile, I would definitely recommend buying the B shares over the A shares. The exception where the A shares may be preferable might be for institutional investors who need to hold large size, or more active traders who wants to use options to hedge or plan to swing trade the stock.

At the current time, the Holding family controls most of the B shares and controls more than 50% of the voting rights. Because of this, the B shares trade at a discount because the voting rights are not seen as especially valuable. But that can change over time. At some point, the Holding family may want to reduce their holdings, when the additional voting rights of the B shares may be seen by the market as more valuable.

By carefully considering some of the factors above, you can make an informed decision about whether FCNCA or FCNCB deserves a place in your 2024 portfolio. With its solid balance sheet, strong management, attractive valuation, and promising growth prospects, I believe that FCNCB in particular has the potential to be a significant wealth driver for long-term investors.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2024 Long/Short Pick investment competition, which runs through December 31. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")