Teka77

FedEx (NYSE:FDX) has been one of the companies I have been following for years due to their big fleet of freighter airplanes providing somewhat of an indicator on strength on the air freight market. I have never covered the stock before, but as it was part of my watchlist I have seen it fall post earnings many times, and the most recent quarterly report was no exception. In this report, I will be briefly discussing the results and more importantly I will assess whether the recent share decline in FedEx share prices offers a compelling entry point.

FedEx Misses On Top And Bottomline In A Challenging Market

The fact that FedEx stock plummeted might not be a total surprise as the company produced a $230 million or roughly 1% miss on estimates and core earnings per share of $3.99 missed estimates by $0.21. The earnings miss comes after four quarters of beating EPS estimates but the top line miss marked the seventh consecutive revenue miss.

FedEx

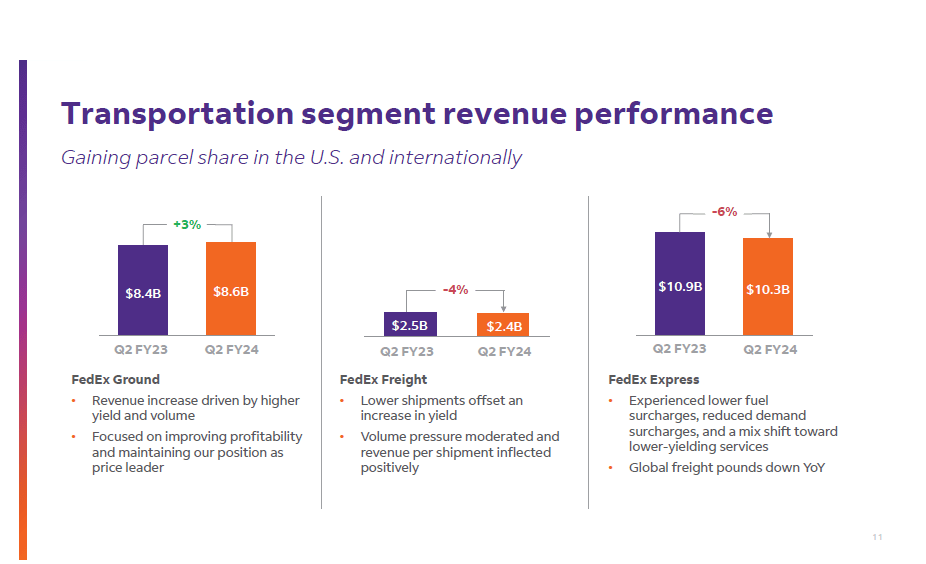

Revenues of $20.89 billion fell 2.8% with revenues impacted by an array of factors. FedEx Ground saw 3% higher revenues driven by better yield and volume. FedEx Freight saw a 6.5% decrease in priority shipments and 1.6% decline in Economy shipments for a total decline of 5% in shipments resulting in a 4% reduction in revenues. The dampening on the revenue decline was primarily driven by a ~1% improvement in revenue for priority shipments. FedEx Express saw its revenues decline 6% driven by lower US domestic volumes while International domestic volumes were down 2.2% while International Export volumes were up 2.4%, but this was not enough to offset the 3.5% decline in domestic volumes which has a 47% share in the total package volumes. Furthermore, the domestic revenues per package was down from $22.61 to $22.55 and international export revenue per package was down from $54.93 to $52.76.

So, the story of FedEx is that of volume and pricing challenges. FedEx Express at this point looks most challenged, but that’s driven by a normalization of capacity and unit revenues driving down demand surcharges out of Asia while product mix is shifting from priority flows to economy flows. Additionally, fuel surcharges are lower and USPS is requiring more volume to be moved over ground than air and FedEx Express is working on rejigging its network to facilitate e-commerce demands, which to a lesser extent would favor the existing hub-to-spoke model. It’s not the case that the air network will be transformed to point-to-point network, but via a Tricolor network set up the company will optimize utilization of its own assets by flying the traditional hub-spoke model with high margin volumes. This is known as the Purple network. The company also will build a network to decongest hubs and have better density in its network, which would likely be more like a point-to-point operation for priority deliveries and finally capacity of partners would be used as a flexible capacity layer.

FedEx

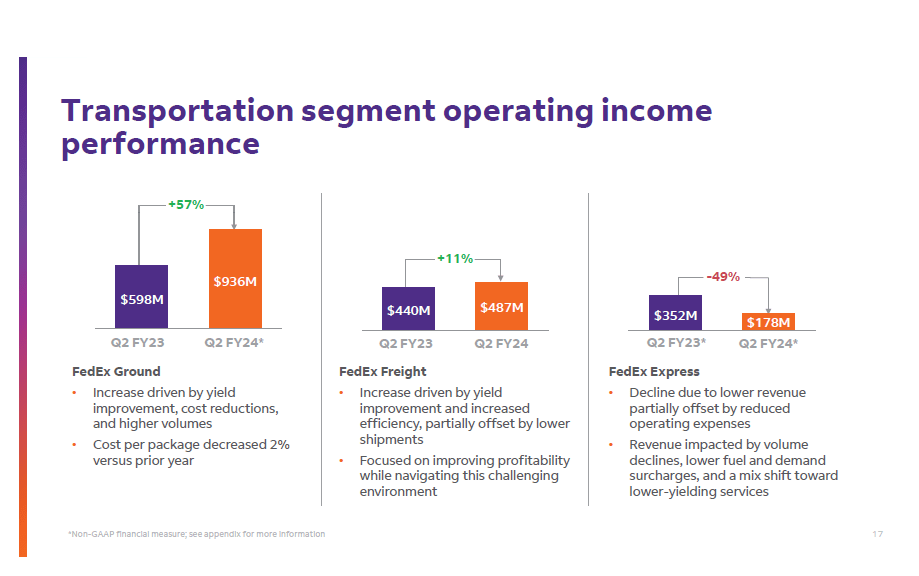

On 2.8% lower revenues, FedEx achieved 9% higher operating income driven by the significantly better results at FedEx Ground, which more than offset the decline at FedEx Express. The significant improvement in consolidated income to $1.276 billion can be attributed to the DRIVE cost optimization program which yielded >$415 million in Q2 costs savings.

The reality is that FedEx is facing a challenging environment right now due to lower volumes driven by macroeconomic uncertainty all while the normalization in capacity and unit revenues has been ongoing for a while. With low volumes and low fuel prices we also see those surcharges falling off and reduce the top line and all of that happens while FedEx is reinventing its air network. However, at the same time we are also seeing the positive impact from the DRIVE cost reduction program

Guidance Update Reflects Topline Pressures

FedEx

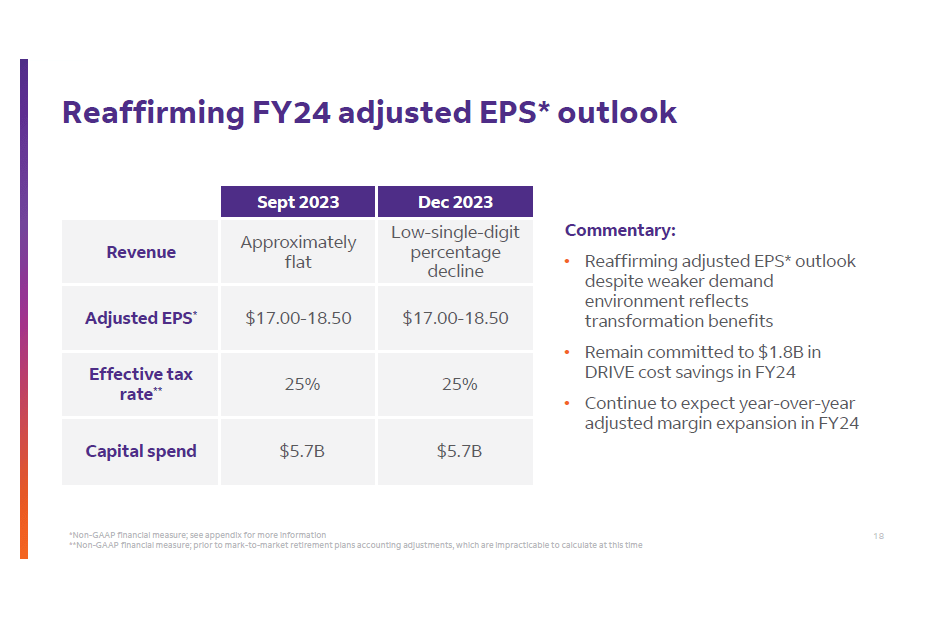

The guidance update pretty much reflects what we saw in Q2 as well: The DRIVE cost savings should flow positively in the company’s financial results yielding higher profits on lower revenues. It’s not much to get excited about but very meaningful given how many businesses in freight and logistics depend on volume improvements and lower revenue has a tendency to significantly erode profitability and the DRIVE program is offsetting some of those volume pressures.

FedEx Stock: Hold With Upside

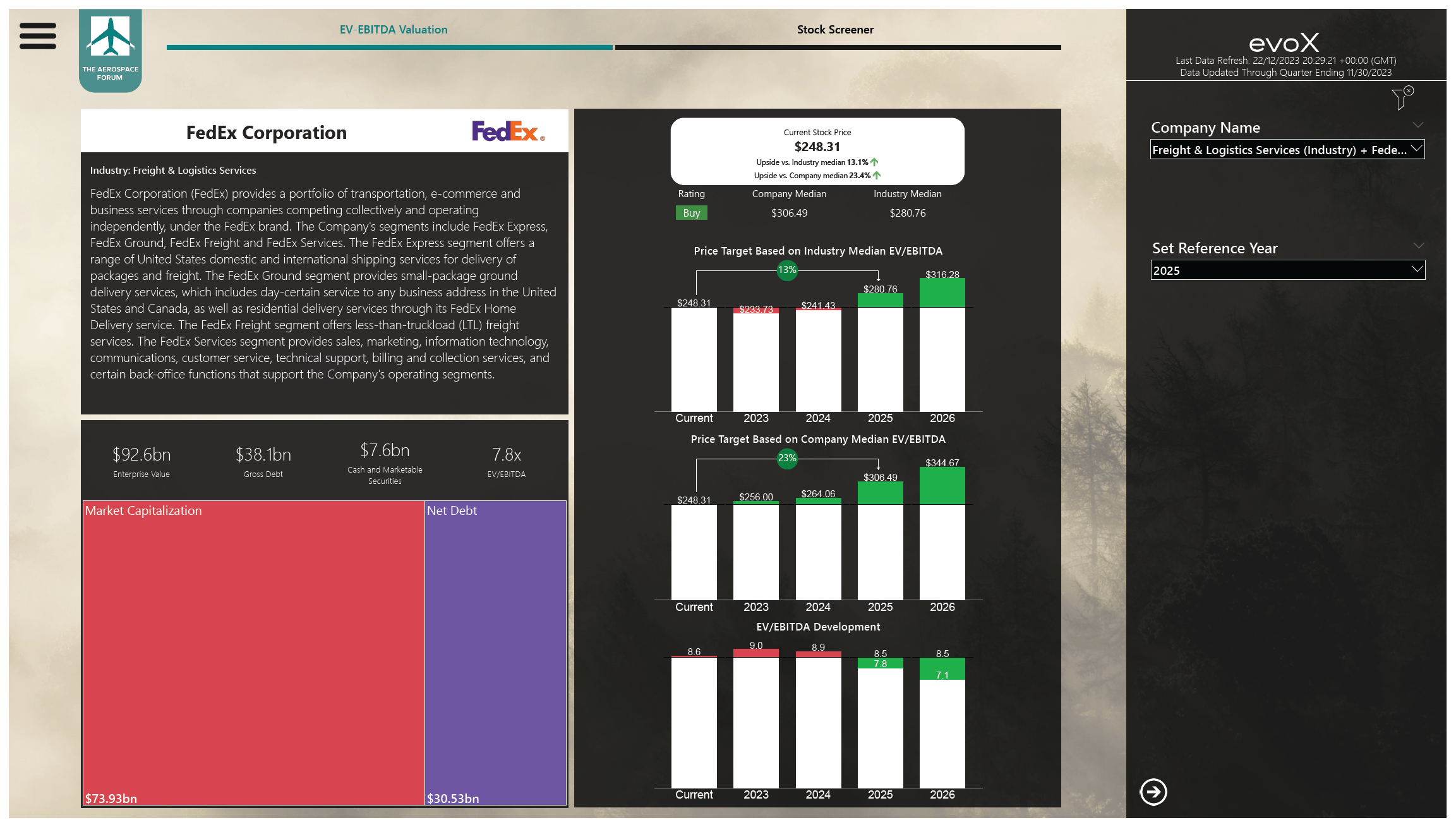

Stock price valuation for FedEx using evoX Stock Screener (The Aerospace Forum)

Processing the forward projections and balance sheet data for FedEx shows that with FY25 earnings in mind, FedEx has around 13% upside based on the industry median EV/EBITDA and 23% based on the company’s media EV/EBITDA. While upside does exist, based on the three-year alpha value FedEx stock is a hold and I believe that’s an appropriate rating given the macroeconomic uncertainty which currently is translating in lower volumes. At the same time, I think it’s important to point out that upside continues to exist and the reduction in share price as seen recently is more than reasonable. The stock went as low as $245 which comes pretty close to valuing 2024 earnings at industry median EV/EBITDA. I would assign a Buy rating with a $293.70 price target which is obtained by averaging the company median and the peer group median EV/EBITDA and coincides with Wall Street price target of $293.63.

What Are The Risks For FedEx?

While I do have a Buy rating for FedEx stock, there certainly are challenges. The decline in volumes and pressures seen at FedEx Express certainly are somewhat concerning even though the company is executing well on its cost reduction program. Additionally, Amazon (AMZN) has restarted its shipping service earlier this year, which is in direct competition to FedEx. So, just building a bullish thesis centered on e-commerce growth won’t cut it.

Conclusion: FedEx Stock Is A Buy On DRIVE Execution

Following the FedEx Q2 FY24 earnings report, I’m marking the stock a Hold. The company is facing a tough environment with lower volumes and shifts in mix. The positive is the ongoing cost savings from the DRIVE program. FedEx has qualified as a buy driven by its long-term alpha value, would we have used a three-year alpha value the company would be a Hold. So, you could make a case for the stock being a hold or a buy. I’m initiating with a buy rating and will keep an eye on the macroeconomic environment and the impact on volumes and unit revenues as well as the progress on the DRIVE cost reduction effort.

Q2 2024 Earnings Call Transcript")