TERADAT SANTIVIVUT

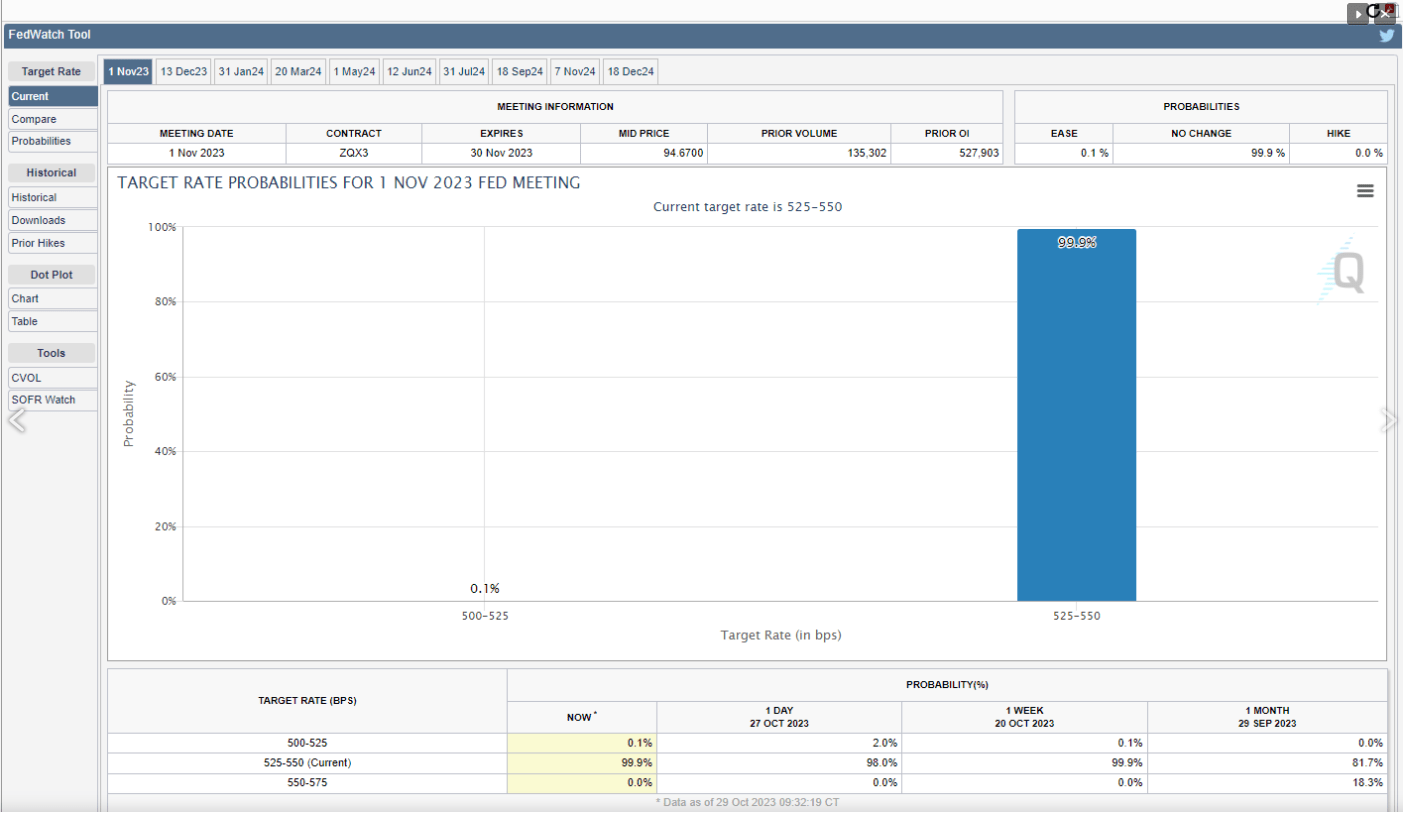

The first bar chart is the fed funds probability for Wednesday’s 11/1/23 FOMC meeting and what it’s telling readers is that there is a 99% chance that the FOMC will maintain the current fed funds rate of 5.25% – 5.50% for the next 6 weeks.

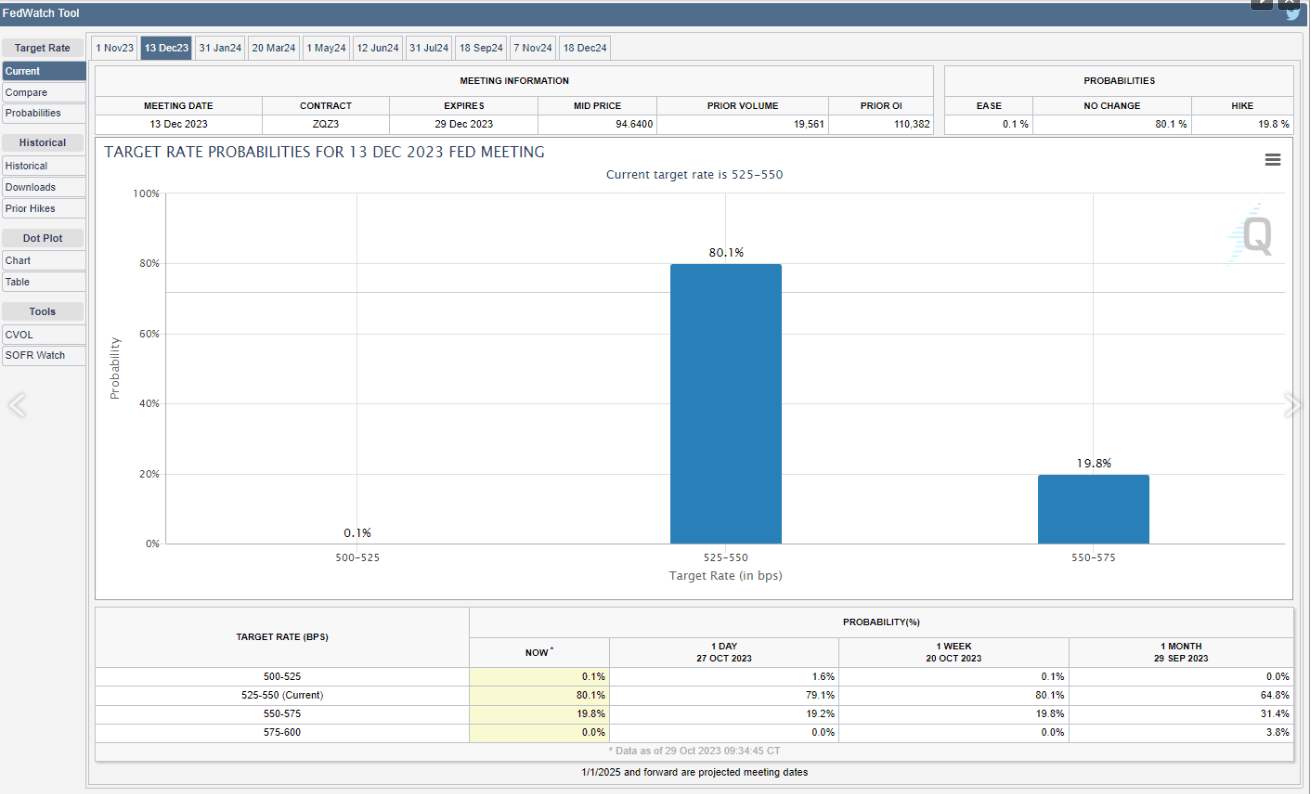

The second bar chart shows the probability for maintaining the fed funds at 5.25% – 5.5% at about 80% (as of Friday, October 27th) with a higher probability of about 20% of a 25 bps increase on December 13, 2023, or the next FOMC meeting after Wednesday’s.

Looking at the fed funds probability picture, it’s clear the Fed / FOMC is on hold for now. Let’s see if the FOMC statement, on 11/1/23, generates a rising probability of a 25-bp rise for the 12/13/23 meeting. (It’s still pretty likely that the Fed/FOMC or Powell would remain hawkish with this week’s statement. The bully pulpit and scaring the short end of the Treasury yield curve is still the easiest and cheapest form of monetary policy). However, I also think investors have to look at yields at the longer end of the curve, as there are some signs of the US economy weakening.

Let’s see if the probability changes for the 12/13/23 FOMC meeting for a potential rate hike, after Wednesday, 11/1/23’s meeting.

Oversold stock market:

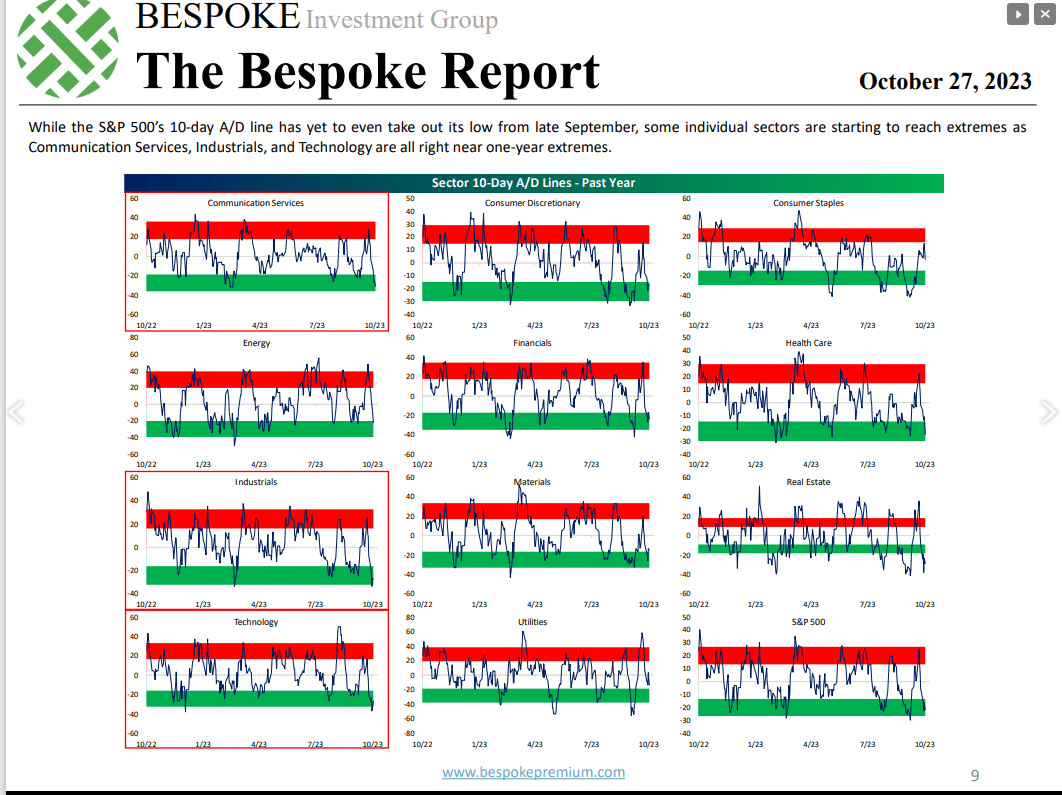

What’s a Fundamentalis blog post without a Bespoke chart ?

Every sector above is trading in “extreme oversold” levels except consumer staples.

Crude oil is weakening, but the dollar is still too strong.

This isn’t an easy market to navigate.

Apple (AAPL) Earnings, Thursday night, November 2nd, after the closing bell:

Apple reports after the bell Thursday night and they’ve experienced the typical year in terms of pre new product launch of the new Apple iPhone 15.

The September quarter is the fourth quarter of fiscal ’23, and it doesn’t look like the holiday quarter (fiscal Q1 ’24) will be any less robust than is typical for the iPhone giant, unless we see the onset of a nasty recession in Q4. However, in the calendar fourth quarter, 2018, when Jay Powell was raising the fed funds rate and the stock market was taking gas, Apple managed to just meet EPS and revenue consensus. The company did not manage their typical healthy “upside surprise” for the holiday quarter in Q4 ’18.

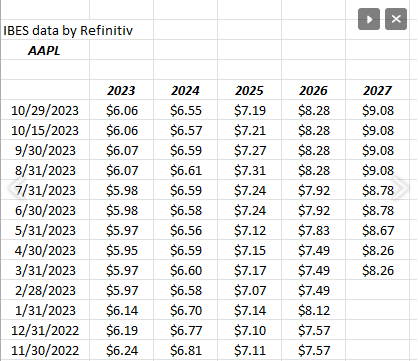

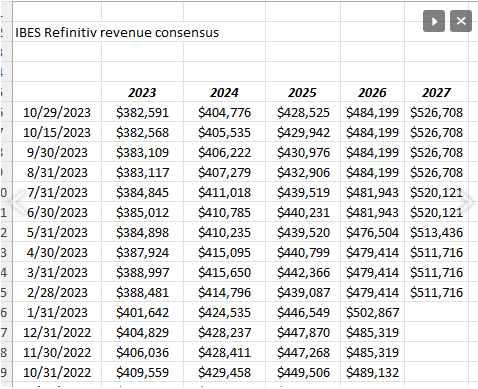

A look at Apple’s EPS and revenue revisions over the last year:

These revisions are sourced from IBES data by Refinitiv and show a gradual softening in EPS and revenue estimates over the last 12 months, not really that unusual for the 2nd year of an iPhone launch.

The key really is how well will the new iPhone and other Apple products sell in the holiday / Christmas quarter that has already started.

Apple is expecting -1% revenue growth and 8% EPS growth for the fiscal Q4 ’23 that will be reported Thursday night, but for the December quarter, revenue is expected to be up 5% and EPS is expected to grow 12% for the holiday quarter.

Here’s a history of Apple’s revenue for the key December quarter for the last 5 years:

- Dec ’23: $123.23 billion (estimate)

- Dec ’22: $117.154 billion (actual)

- Dec ’21: $123.9 billion (actual)

- Dec ’20: $111.4 billion (actual)

- Dec ’19: $91.8 billion (actual)

As readers can see, if Apple doesn’t lift guidance for the December quarter on Thursday night, there is a chance that total revenue growth for the last two years remains roughly flat with ’21, assuming the current consensus remains close to its current level.

Apple is trading at roughly 26x EPS for a hardware company that is expected to generate just 6% average EPS growth for the last quarter of ’23 and then the next two fiscal years. The services business of Apple is now 26% of total revenue – but the kicker is the services business packs a 70% gross margin, versus the iPhone and product segment, which has a 35% gross margin.

Multiple expansion is expected with Apple as services grows as a percentage of revenue. It’s probably why Morningstar kept a weak or no moat rating on Apple for so many years, i.e., waiting for services to grow as a percentage of total revenue.

Summary / conclusion: Once again, a Bespoke chart jumped out at me this weekend and showed the 11 sectors of the S&P 500 almost uniformly deeply oversold. Apple’s revenue has slowed (depending on where and how the December fiscal Q1 ’24 quarter turns out) but that deserves a longer look.

Take everything on this blog with substantial skepticism as it represents just one person’s opinion and past performance is no guarantee of future results. All the EPS and revenue data is sourced from IBES data by Refinitiv. Capital markets change quickly for both the good and bad. Readers should gauge their own comfort level with their portfolio volatility and adjust accordingly.

Thanks for reading.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Q2 2024 Earnings Call Transcript")