CalypsoArt

Fairfax Financial Holdings (TSX:FFH:CA) is a Toronto based global insurer, operating primarily in the Property and Casualty Insurance and Reinsurance business.

FFH released fiscal year 2023 results on February 15, which confirmed the strong operating performance of the underlying businesses. Earnings per share increased by 32% year on year, and book value by 25%.

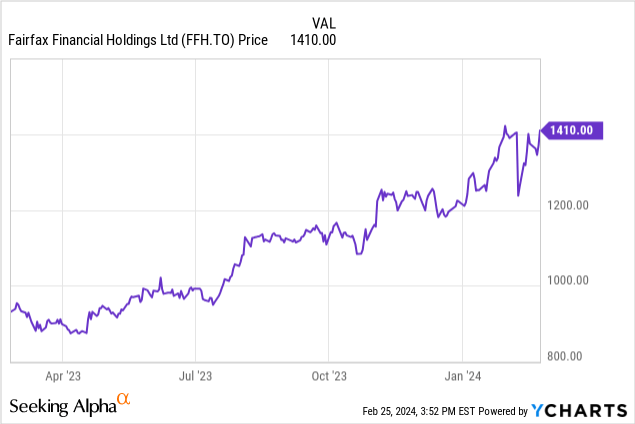

The stock performed well over the course of 2023, but dropped sharply prior to earnings following some accounting concerns. This 12% drop has been reversed following the results release, and FFH’s price has regained positive momentum.

This analysis follows up on an article I wrote prior to the earnings release, which took a deep dive into the underlying business, and outlined several key positive tailwinds which can be expected to drive continued performance. Below I will take a look at the FY23 earnings, and forward looking statements, which validate a positive outlook. I will also report on managements comments in the earnings call which included some detailed rebuttal of the accounting concerns.

The headline financial results

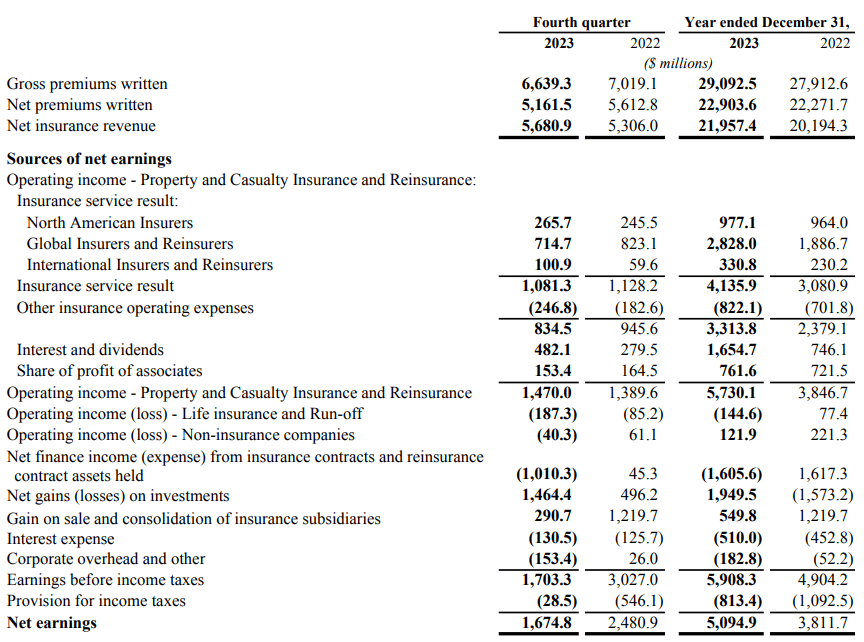

Q4 finished off a record year of performance for FFH, with key highlights as below.

- Net Earnings $5.1bn

- IFRS discounted pre-tax income of $5.9bn (see my previous article for a discussion in IFRS vs USGAAP accounting).

- All key Insurance and Reinsurance companies recorded underwriting profits, with a consolidated combined ratio of 93.2% generating $1.5bn of undiscounted underwriting profit.

- Gross premiums grew by 4.8% to $29.1bn

- Net premium growth was slower, at 3.5%. This reflects the increasing costs of reinsurance for the insurance parts of the business.

- Insurance float increased by 15% year on year, which creates good opportunities for growth in investment income.

- Investment income for the year doubled from $962m to $1.9bn, due to the growing float and higher equity valuations and investment yields especially from fixed income.

Full details are provided from the SEDAR filings.

SEDAR

Most of the operating companies saw growth in premiums, with some offset from Odyssey, the pure-play reinsurer. The release notes that group premiums would have grown by 6% without the impact of one large Quota Share reinsurance treaty, which was discontinued by Odyssey, implying 1.2% of gross premiums or roughly $350m in premiums. This is a very large impact from a single treaty, which from my experience could only relate to one of handful of contracts in the market. These tend to be high premium, low margin capital substitute contracts which are highly structured financing instruments. The impact on underwriting margins is likely to be minimal.

In terms of ongoing bottom line expectations, an increase of 6% by volume, plus improved margins of another 4% due to continued price momentum would not be unreasonable to see as the 2023 business earns out through 2024.

This implies 2024 net earnings growing by 10% to $5.5bn, assuming similar business performance to 2023.

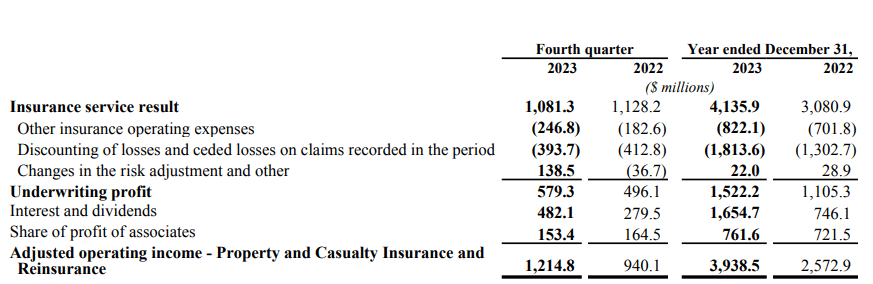

The critical point raised in my previous article is that the core businesses are firing on all cylinders, which can be seen in the table below.

SEDAR

The key metric here is the underwriting profit, increasing to $1.5bn, a 37% improvement in bottom line.

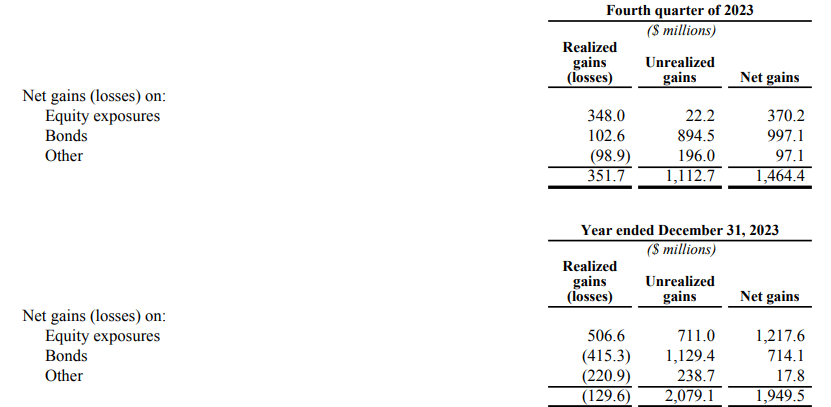

The investment performance is broken out below:

SEDAR

On the operating side, on December 23,2023, Fairfax doubled its stake in Gulf Insurance to a controlling 90% share, which created a pre-tax gain of $293m on the valuation of its prior share. Fairfax will also add a further $2.4bn of assets into its AUM following the transaction. The remaining 10% is subject to a tender offer to Kuwaiti shareholders, and Fairfax expects to complete the purchase of the remaining 10% during 2024.

Balance sheet actions included a year on year reduction in the debt to capital ratio from 23.7% to 23.1%, and a modest reduction in share count. Overall 2.5% of shares have been repurchased in 2022 and 2023.

Insights from the earnings call

The earnings call covered a lot of the operating result information discussed above.

Notable colour was added on a 89.5% combined ratio for Allied World, 91.9% for Brit, and 93.4% for Odyssey. The contribution of the reinsurance parts of these businesses was called out – which confirms the thesis of improved operating performance expected from this segment through the next 24 months discussed in my pre-earnings article.

In North America, performance was more muted, with Crum & Forster seeing results deteriorate to a 97.7% combined ratio due to a 2% contribution from unprecedented wildfires in Hawaii.

Discussion then moved onto the accounting issues raised in the short report.

Interested readers would be advised to read the entire transcript, but to summarise the main points raised by CFO Jenn Allen:

The main discussion was on the valuation of carried assets, and how these were carried out.

- Introduction stressing IFRS 17 accounting standards, and the controls in place.

- Digit Insurance – Valuation based on 2021 based on the asset price at the last 3rd party capital raise, updated by DCF valuation. The growth estimate of the business in India is a key driver here. Digit was profitable under both IFRS and Indian GAAP.

- Recipe – take private valuation was supported by an independent valuation conducted on the instructions of the Recipe BOD.

- EXCO – valued at 3x 2023 earnings.

- QUESS – has been subject to several valuation writedowns, currently valued below 16x EBITDA.

- Odyssey – details provided of the transaction, a partial sale at 1.7x book value, with proceeds used to buy back FFH shares at 0.9x book value (a compelling trade in my opinion). Fairfax call option included to allow them to buy back the Odyssey shares at a later date – no obligation to do so.

- IFRS17 implementation impact. As discussed in the previous article, the peer comparison was not reflective of the policy maturity profile of the liabilities of the Fairfax business, which has a major impact on IFRS capital modelling. Further colour of the fact that several peers used differing methodologies on discounting in the run up to IFRS17 implementation.

In my opinion, these comments dealt with each of the main accounting concerns comprehensively.

Outlook and valuation

As discussed above, I believe that the operating outlook for the (Re)insurance businesses are positive, especially in the reinsurance space, and I expect to see this come through into 2024 earnings and beyond, with growth in premiums, and also margins for at least the next 24 months.

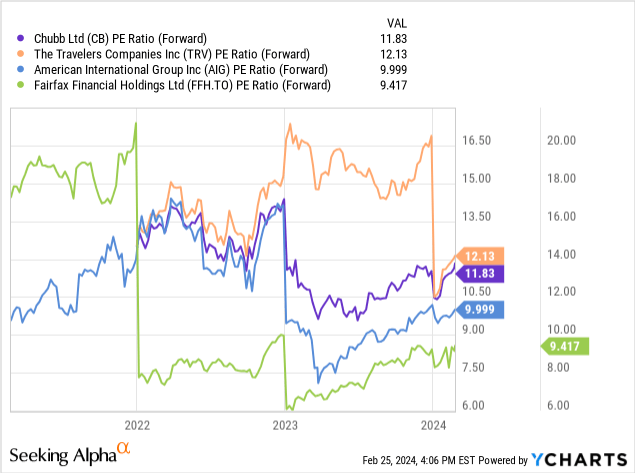

Despite the strong run up in price, FFH’s valuation to peers is at the low end. On a forward Price/earnings ratio, FFH trades at a 20% discount to Chubb (CB) and Travelers (TRV) and even below AIG (AIG).

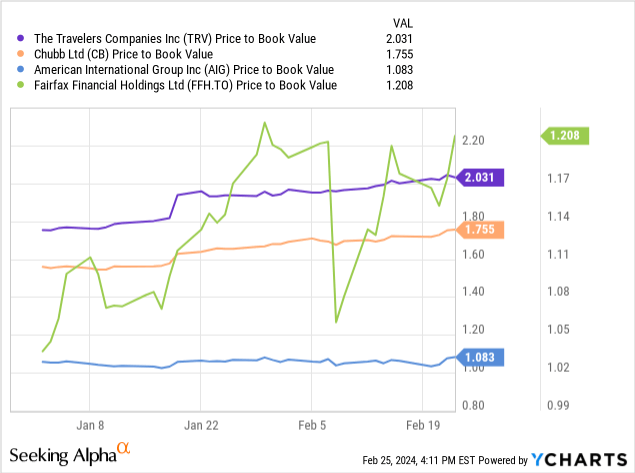

On a Price/book basis, the valuation gap is similar, although AIG is 20% below FFH on a price/book basis. (note the graph below seems to have a scaling issue with FFH – the Price to book is 1.2x, whereas the graph looks higher.)

After the Q4 results, I am upgrading FFH to a buy. I expect 2024 earnings growth of 10-15%, with some valuation upside. I doubt that FFH will close the valuation gap to industry darlings CB and TRV, but do see a 20% upside to the current price as realistic.

Risks to the thesis

In addition to the allegations of accounting manipulation, which I believe can be discounted, I see risks to the business performance as:

- Asset risk- The FFH asset base is not as diversified as most insurers.

- Climate and catastrophe risk- The risk of pricing gains being overtaken by loss trends.

- Inflation risk- As with climate and catastrophe risk, price increases are overtaken by inflation trends.

- Regulatory risk- OFSI investigation of accounting practices hampering the business.

- Reserving risk- Understatement of liabilities. This is mitigated by the active run-off management.

Summary

- FFH is performing well, as reinforced by Q4 results.

- The underlying businesses are benefitting from ongoing tailwinds.

- Double digit growth should be expected to continue.

- The share price has been volatile around a short thesis release which management has in my view de-bunked.

- Q4 results and the commentary cause me to rerate FFH as a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")