stocklapse/E+ via Getty Images

Summary

Investing in Brazil is frustrating, the nation has all the ingredients to grow into a developed nation, and anyone who has been to Sao Paulo feels and sees a dynamic modern growth engine. However, in my view, the country consistently shoots itself in the foot via dysfunctional political and institutional decision making i.e. populism and corruption. Thus, Brazil is more a medium-term trade idea vs a long-term compounder. The iShares MSCI Brazil ETF (NYSEARCA:EWZ) is a reasonable vehicle to trade Brazil.

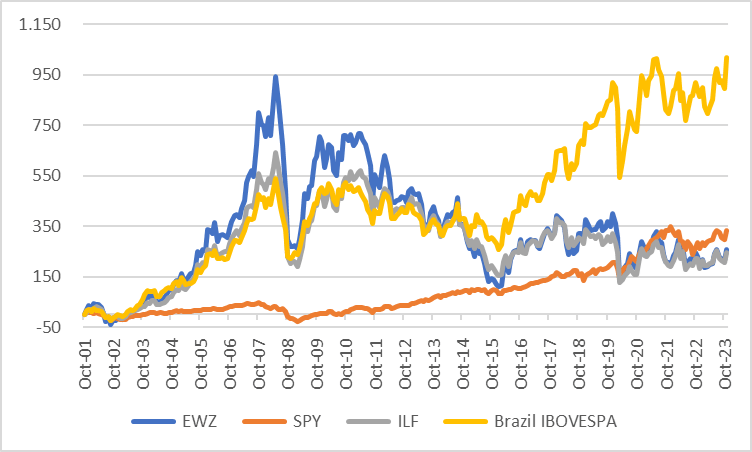

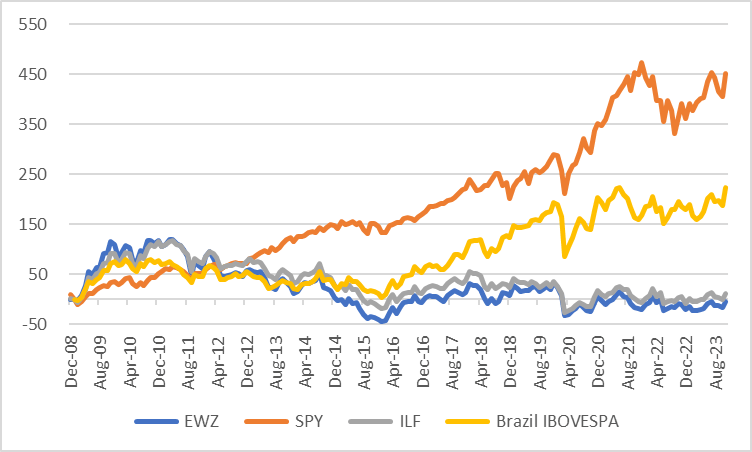

Performance

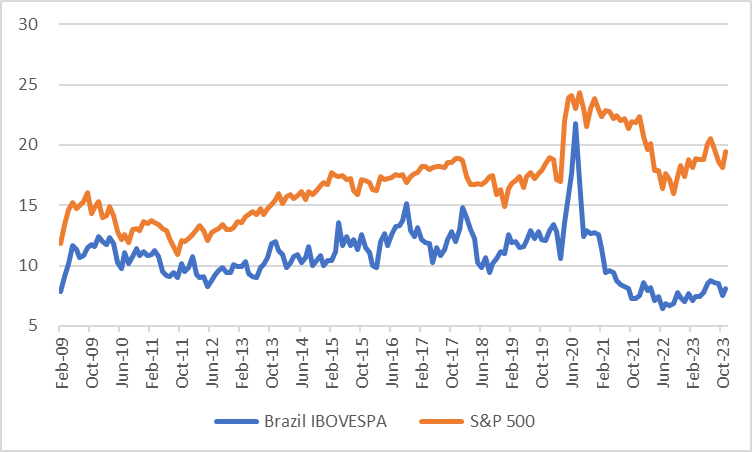

As can be seen in the charts, the EWZ had a massive return up to 2008 and has given most of it back by 2023. The main detractor has been the currency. When I lived in Brazil the BRL was volatile, the currency peg broke in 1999, with the BRL climbing from $1 to $3.5 at the start of Lula’s first term in 2003 and then back to $1.5 pre-GFC in 2008. Since then, the BRL has continued to be volatile and generally lost vs the USD to the $5 range today. This currency devaluation has sapped the USD returns as can be seen when one compares the EWZ vs the Bovespa Index.

EWZ vs Bovespa (Created by author with data from Capital IQ) EWZ vs Bovespa (Created by author with data from Capital IQ)

The Trade Balance

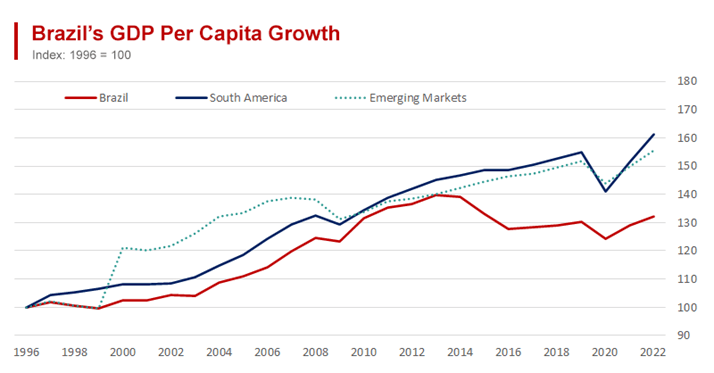

Brazil is not China or India, it has rarely seen more than 3% GDP growth and this impacts overall stock market returns. In my view, the reason for poor growth is primarily due to dysfunctional institutions from the government to the justice system. Brazil is a rich nation with a poor population that can be wooed by populism that has created a renter or client economy i.e., where the government attempts to supply benefits for the poor that winds up handicapping growth and results in a vicious cycle of institutional overspending, overtaxing, protectionism, and inefficiency.

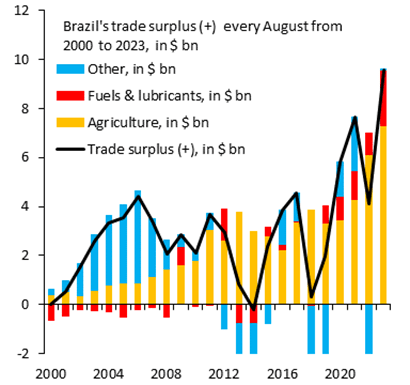

Key to the strength of the BRL and potential GDP growth is the trade balance. Brazil is experiencing a second commodity boom, this time led by agriculture. Which when combined with low valuations may result in positive returns into 2024.

Brazil GDP Growth (Image from World.economics.com)

Brazil Trade Balance (Image from RobinBrooksIIF on X)

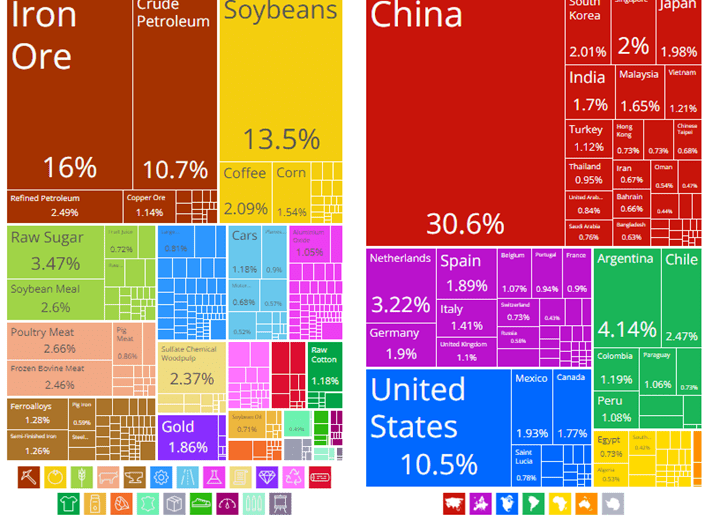

Brazil Exports (Image from OEC.World)

Historic Valuation

The Bovespa has traded north of 10x PE in the last 20yrs, this is despite the level that local risk-free or bench market interest rates were. From 2021 to the present this multiple has declined to 8x as the market incorporated a refuse in EPS and a dramatic boost in SELIC rates, the Central Bank equivalent of the Fed Funds rate, from 2% to 14% to combat inflation. Those rates are now being reduced and could return to an 8% level, while EPS are slated to rebound 30% in YE24. This, plus reasonable GDP growth, should drive valuation up to 10x in my view.

Bovespa PE Ratio (Created by author with data from Capital IQ)

EWZ Growth and Valuation

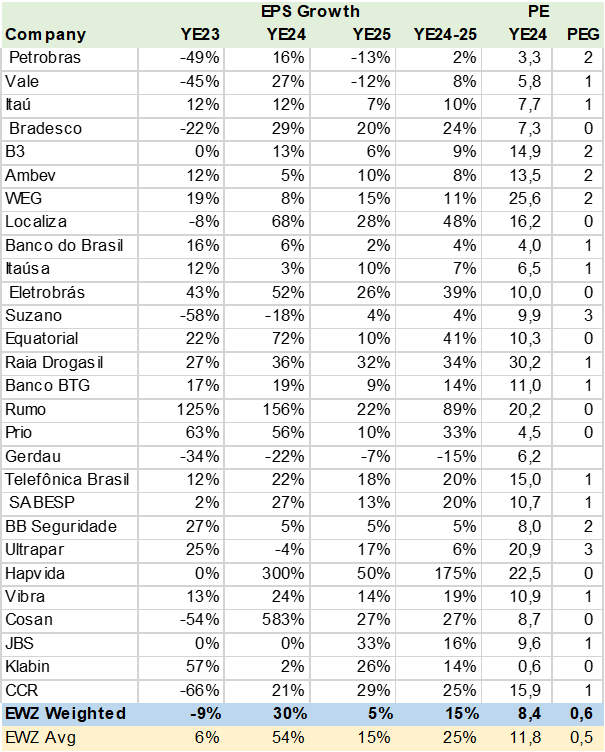

Using consensus estimates for the EWZ portfolio I calculated weighted EPS growth of 15% in the YE24-25 period vs. a PE of 8x or a PEG of .6x, which I would classify as cheap. Note that the simple average or equal-weighted portfolio has far higher EPS growth due to Petrobras’s (PBR) declining EPS estimates.

EWZ Consensus EPS Growth (Created by author with data from Capital IQ)

Portfolio Upside

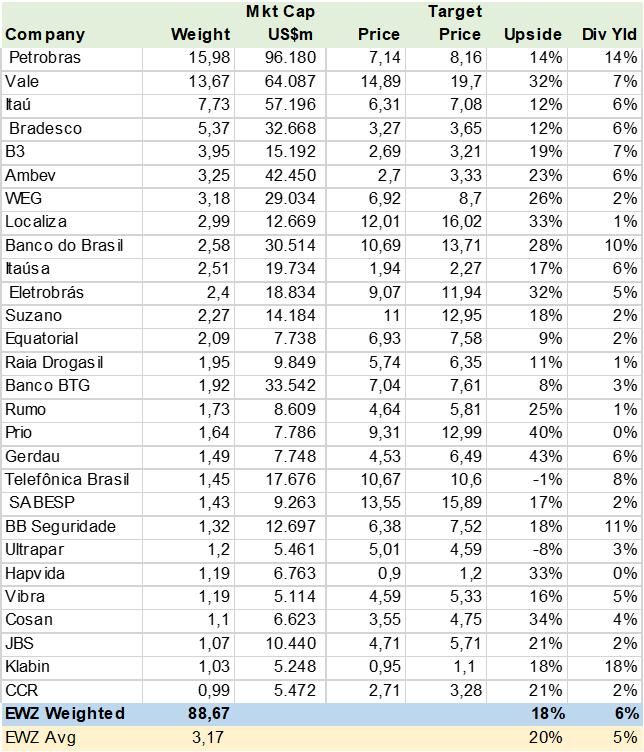

I calculated that the EWZ holding could have an 18% upside to the end of 2024 on the consensus price targets. In addition, the estimated dividend yield of 6% is also attractive. Some interesting outliers, with ADRs are Banco do Brasil and Sabesp (SBS), which is being privatized as I write this article.

EWZ Consensus Price Target (Created by author with data from Capital IQ)

Conclusion

I rate the EWZ a BUY. The Brazil ETF should benefit from the country’s rate cut cycle, EPS growth recovery, and strong trade surplus that supports the currency. Consensus price targets point to an 18% upside with an additional 6% dividend yield trading at a PE of 8x for year-end 2024.

Q2 2024 Earnings Call Transcript")