Sean Pavone/iStock via Getty Images

The iShares MSCI Italy ETF (NYSEARCA:EWI) returned 30% in the 2023 calendar year and continues to offer both value and yield to investors. Despite positive recent performance and an enticing sticker price, the potential hindrances for EWI remain numerous. As a potential single country Europe play, I think EWI should remain a hold for now.

Economic and monetary hurdles to clear

Slower for longer tends to be the sentiment around the Eurozone and that doesn’t exclude region’s third largest economy, Italy. The country’s estimated GDP growth rate is expected to expand only +0.1% in 2024 to reach 0.7% compared with 0.6% in 2023.

Despite the lackluster economic projections, inflation is expected to experience a steep decline in 2024 dropping from an estimated 5.9% in 2023 to 2.0%. Diminished inflationary pressures aside, there are real question marks around whether economic growth can be realized; Italy has been delayed in disbursing funds from the European Recovery and Resilience Facility (RRF). The RRF is a pillar of the Eurozone’s crisis response to the COVID-19 crisis called “NextGenerationEU”. In the case of Italy, key economic advancement initiatives have been budgeted with expected funding from NextGenerationEU. There are guidelines around fundings, and large percentages are intended to be allocated to both green and digital transformation projects. These are requisite initiatives that would both help spur economic growth and help keep countries compliant with the evolving green regulatory apparatus in the EU. However, further funding is contingent upon completing agreed upon milestones. At present moment, Italy is not meeting those milestones. There is a scenario where Italy’s economic expansion is kneecapped by its inability to complete projects that would secure further investment.

There is also the wild card around when the ECB might cut interest rates. There is speculation that slowing inflation data around the Eurozone could lead to a rate cut as soon as June, or even April. However, a longer delay in rate cuts could further limit Italy’s progress. Even still, rate cuts could have their own set of consequences for the fund which I will touch on below.

Holdings

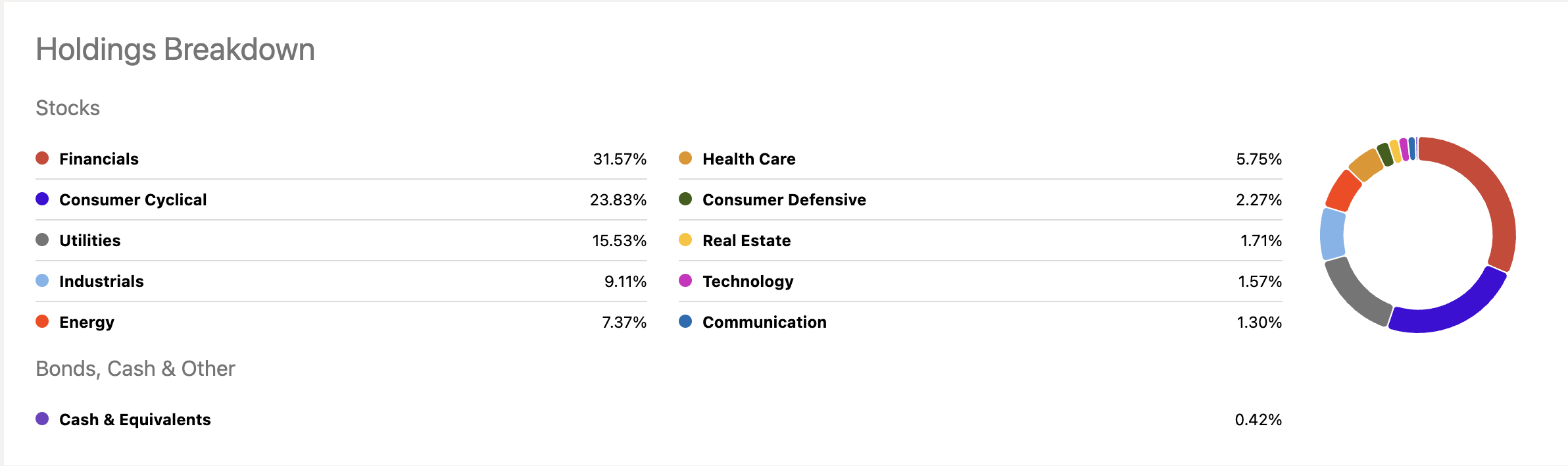

The iShares MSCI Italy ETF is a concentrated fund (~35 holdings) with around $425M in assets. The fund is heavy Financials (32%) and Consumer Cyclicals (24%), with sizable allocations to Utilities (16%) and Industrials (9%). Overall, this sector breakdown makes EWI a more defensive and value tilted fund.

Seeking Alpha

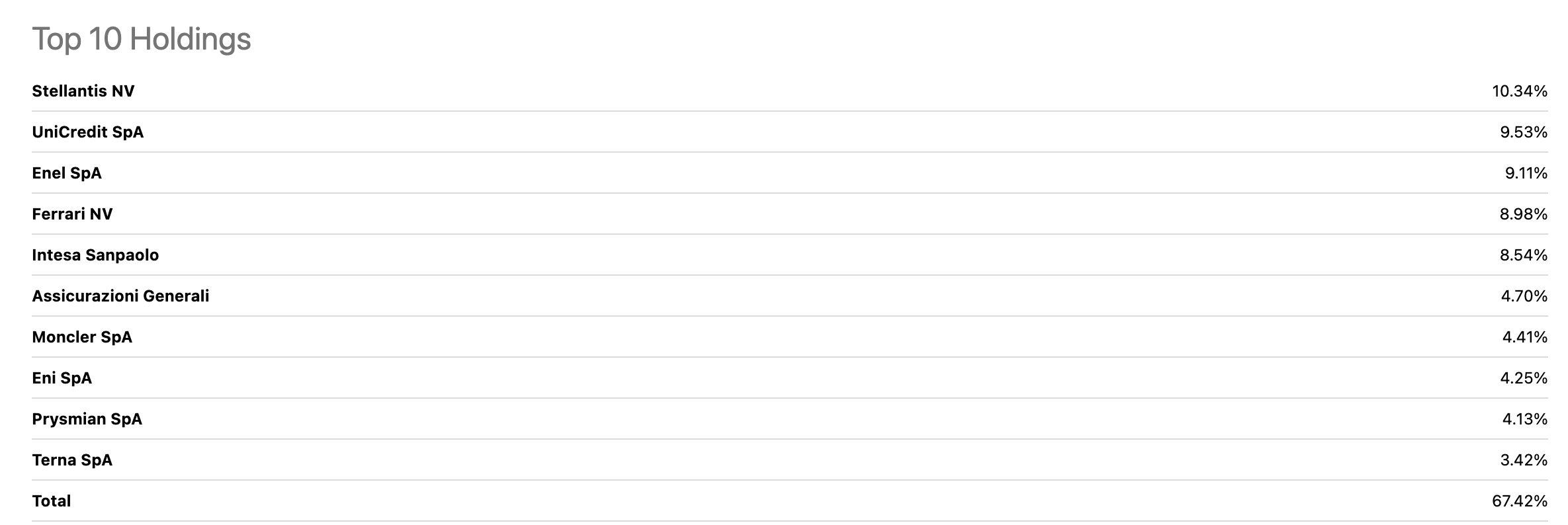

The top 10 holdings account for around 68% of the total assets, which is actually pretty diversified for a fund of 35 total holdings. About 10% of the fund is allocated to multinational automotive manufacturer Stellantis NV (STLA), with another ~10% to banking group UniCredit SpA (OTCPK:UNCFF).

Seeking Alpha

Favorable multiples in the Eurozone

I like EWI’s current value profile. It is trading at ~10x earnings, with a P/B ratio of 1.5. EWI is also offering a decent yield, with a TTM yield of 3.06%. The fund has consistently paid dividends for 18 years, while it hasn’t seen many periods of consecutive dividend growth, it currently holds a 3 year CAGR dividend growth rate of 33%. When compared to the broader western European peer universe, that is a notable characteristic.

|

EWI |

EWP |

EWQ |

EWG |

EWU |

|

|

iShares MSCI Italy ETF |

iShares MSCI Spain ETF |

iShares MSCI France ETF |

iShares MSCI Germany ETF |

iShares MSCI United Kingdom ETF |

|

| P/B | 1.5 | 1.4 | 2.1 | 1.6 | 1.8 |

| P/E | 10.4 | 10.8 | 17.9 | 13.5 | 13 |

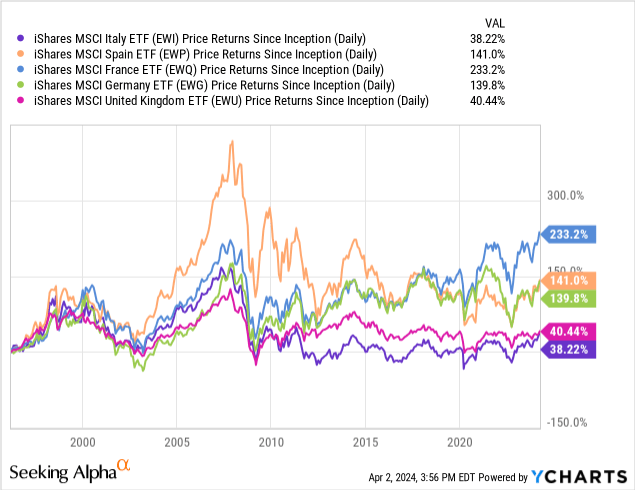

Return and risk

When comparing EWI to its peers, we see that its return profile has been underwhelming since inception. EWI has a daily price return of 38.22% since its inception in 1996.

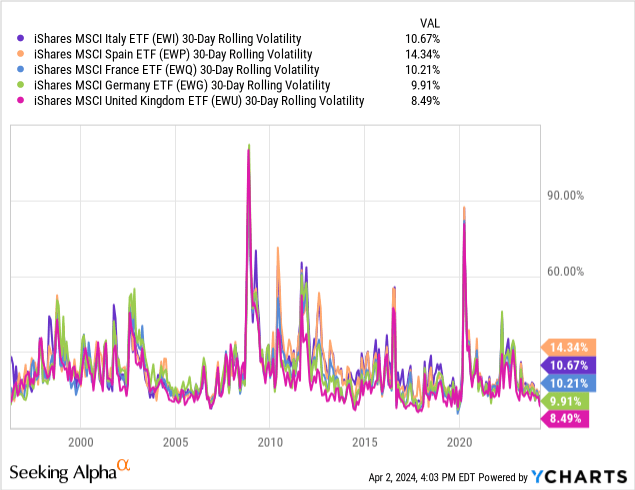

When evaluating the same universe along a few separate risk metrics we see that EWI is more middle of the pack, offering a 10.67% rolling volatility since inception. Given its longer-term return profile illustrated above, EWI would have less attractive risk-adjusted return relative to its European counterparts.

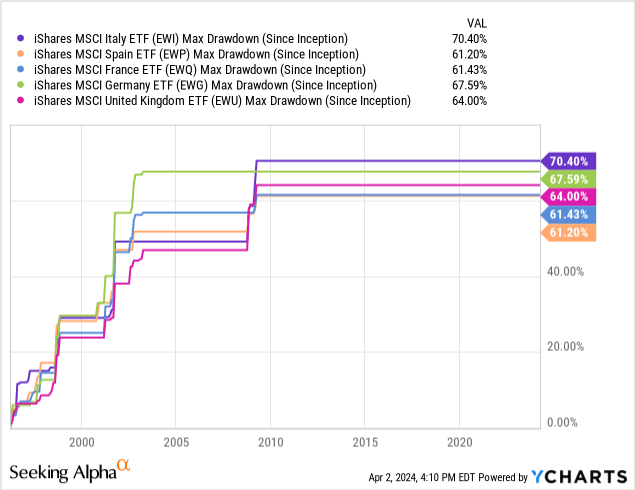

The same can be said in terms of downside protection. EWI also has offered less downside protection relative to the universe, though its max-drawdown within range of the others.

ECB rate cuts could add risk

In addition to the macro and fund characteristic risks outlined above, potential monetary policy changes could have an adverse effect on EWI. To reiterate, the main positive characteristic of EWI is its value profile. It is currently trading at a discount relative to the majority of western European single country ETFs and has a sector composition that is value-oriented (large allocation to financials and utilities). Value stocks tend to fare better than growth stocks in higher rate environments, as they are less impacted by higher discount rates for their future cash flows. This could be one contributing factor to EWI’s recent positive performance. However, given the stagnated economies of the Eurozone and the increasing calls for rate reductions, it seems likely that an interest rate regime shift is on the horizon. This financials heavy fund could suffer on the other side of an ECB rate cut.

Closing thoughts

EWI has performed well in the recent period though there are key vulnerabilities, namely: sluggish domestic growth projections, a less favorable risk-adjusted return profile, and a potential lower interest rate environment. I don’t see this as a time to hop on the EWI bandwagon, and would rather keep it a hold for now until we have more clarity.

Q2 2024 Earnings Call Transcript")