Andrew Merry/Moment via Getty Images

Over the past few years, housing affordability has been thrust into the limelight as home values continue to appreciate. While beneficial for homeowners, increasing home prices leave future generations and first-time buyers in a difficult position. The changing tide serves as a serious multidecade tailwind for multifamily investors. Renting continues to gain traction as a long-term living option. As a result, multifamily development increased coming out of the pandemic and “built for rent” communities continue to gain popularity. As new development begins to slow, established landlords in primary markets are well positioned to capitalize on population and income growth.

Investors looking to capitalize on these tailwinds often find themselves in a difficult position. Buying an investment property and managing tenants is a difficult and time intensive business. There are costs and risks associated with being a landlord which makes the gig unattractive. Unless you have a passion for painting walls and collecting rent, these duties are better left to a property manager. However, property managers are expensive and can quickly eat into our returns. With that, the spotlight moves to apartment REITs!

Real estate investment trusts offer an opportunity to invest in high quality real estate while benefiting from the advantages of owning shares of stock. Investors benefit from a scalable investment, daily liquidity, and consistent financial reporting. Going deeper, we are removing liability and duties from our own schedules and offloading these responsibilities on professionals who leverage their scale to succeed.

Today, we are going to follow up on our previous coverage of Essex Property Trust (NYSE:ESS), a Dividend Aristocrat REIT. We will discuss tailwinds that stand to benefit multifamily investors.

Who is Essex Property Trust?

With a dynamic portfolio of properties, we help both residents and investors thrive. Located in the coastal markets of Southern California, Northern California, and the Seattle metropolitan area, our ever-growing collection of apartment buildings and commercial spaces maintains the highest level of excellence through communities unlike any other.

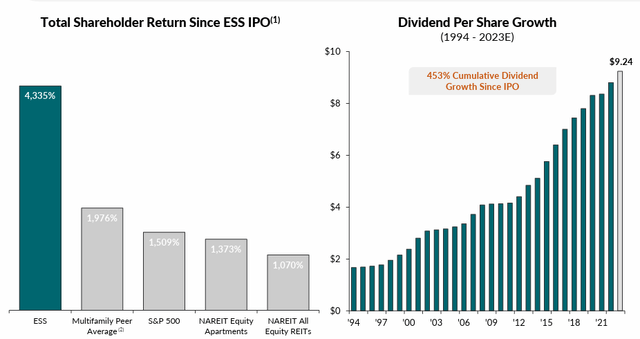

Essex is a multifamily REIT that develops, acquires, and owns apartments across the West Coast. ESS is a member of the S&P500 and one of the largest equity REITs operating in the residential space. Essex focuses exclusively on California and Seattle, sticking to these core geographies. These markets have benefitted from macro tailwinds such as wage and population growth. ESS has been an active developer in these markets for decades. ESS is also a Dividend Aristocrat having raised its dividend for 29 consecutive years. Even more impressive is the 13.8% dividend compound annual growth rate since IPO in June 1994. ESS is rated investment grade by S&P (BBB+) and Moody’s (Baa1).

ESS

ESS owns and operates a best-in-class portfolio of high-quality apartment properties. ESS generates 83% of net operating income in California with the remaining 17% coming from Seattle. Markets within Southern and Northern California are heavily diversified but focus on dense population centers with high paying jobs.

ESS

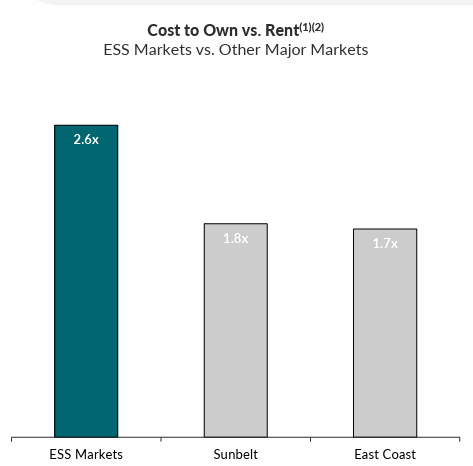

Looking within each of these markets, we see that Essex owns 11,124 units in Los Angeles, 12,525 units in Seattle, and 10,523 units in Santa Clara. The median household income across all markets in the portfolio is $119,000, significantly higher than the national average of $74,580. Most importantly, Essex notes that these markets are notoriously unaffordable in terms of homeownership. Essex notes that across active markets, the cost to own a home is 2.6x the cost to rent.

ESS

The individual assets owned by Essex are exceptional as well. Essex owns a variety of multifamily assets including high rise, midrise, and garden-style apartments. Let’s dive deeper into a typical asset owned by Essex.

Essex owns Forestview, a garden style apartment complex located at 650 Duvall Ave N E, Renton, WA. Renton is a submarket of Seattle with strong demographics which has received interest from institutional investors. Renton is located less than an hour’s drive southeast of Seattle’s Central Business District. A closer look at the submarket will show dense multifamily development throughout.

Bing Maps

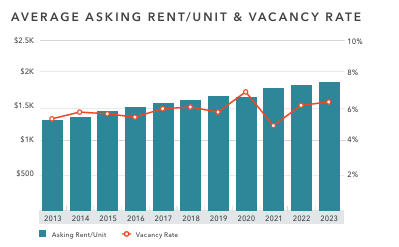

The multifamily heavy submarket benefits from proximity to major employers in the tech and aerospace sectors, such as Boeing (BA). For institutional investors, this means a population of highly compensated employees who are potential tenants. The strong tenant base has supported the growth of rent in the market. According to Kidder Matthews, Seattle apartment rents continue to grow aggressively.

ESS

Balance Sheet & Valuation

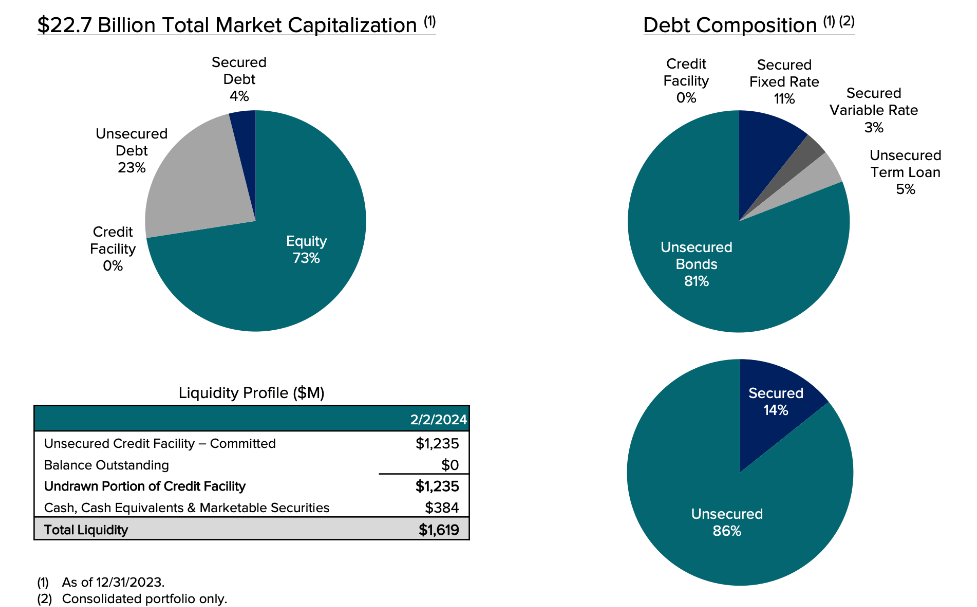

Essex is one of the largest multifamily landlords in the United States. The firm’s balance sheet is strong with low leverage with a debt to asset ratio of 34% and holding primarily unsecured, fixed rate debt. As of year-end, Essex has nearly $1.7 billion in available liquidity across their revolving line of credit and cash holdings. Essex’s net debt to EBITDA ratio was 5.4x as of year-end.

ESS

Essex will be refinancing roughly 25% of their debt over the next three years. The interest rate on the new debt will likely be higher than the maturing debt. Same store rent growth will likely compensate for the negative impact to cash flow given the degree to which rents have risen. Essex reported year end same store rent growth of 4.4%, which translated to NOI growth of 4.3%. Thankfully, rising rents have translated to bottom line growth.

As we mentioned, Essex has averaged 13.8% annual dividend growth since IPO. Quick math will tell you 2023 NOI growth in not sufficient to support a large dividend increase, especially considering the slow in new development across the United States. ESS is anticipated to announce their dividend increase soon. I would expect a modest increase to $2.40 per quarter, an increase of 3.9%.

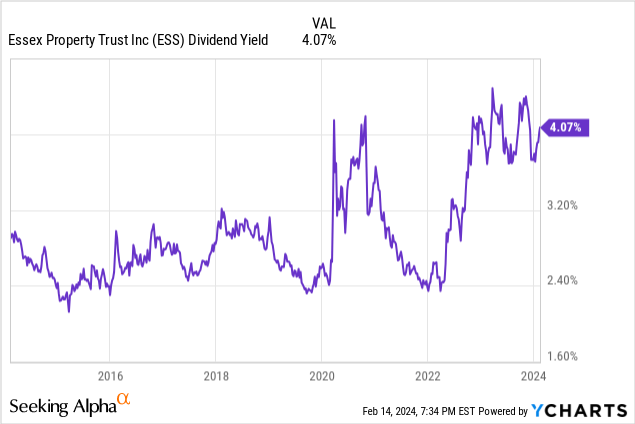

Even still, opportunity knocks as ESS shares have the highest yield in recent memory. As of writing, Essex yields over 4%, a rarity for an investment grade apartment REIT. Given the quality of the underlying assets and the stable NOI growth, Essex remains healthy and well positioned to continue growing the dividend.

Tailwinds

Factors such as inflation, wage growth, housing costs, and employment, continue to shape the housing market differently for each generation. As housing costs rise, retirees and current owners benefit as their net worth grows. On the opposite side, younger generations have found themselves unable to enter a housing market which continues to run away from them. Inflation is driving up building costs, which in turn increases the costs of new deliveries. Employment numbers remain surprisingly strong, so there is no shortage of highly compensated workers who are looking to buy the few homes that do reach the market. The commonality between these various drivers is a benefit to the owner of high-quality apartments.

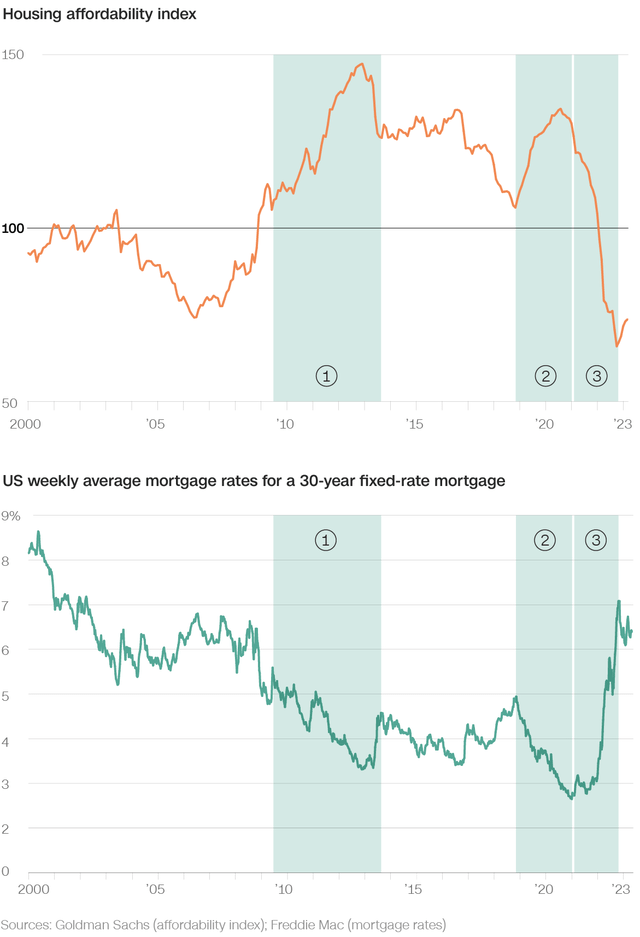

Long term trends continue to point towards housing becoming increasingly unaffordable. Housing affordability remains at the lowest levels in nearly 30 years. Coming out of the pandemic, affordability plummeted, falling below what is considered affordable by the Goldman Sachs US Housing Affordability Index for the first time in over a decade. The index is derived from three metrics: household income, home prices, and mortgage rates. Rising incomes have been unable to offset increasing mortgage rates and rising home prices. Despite expectations that high interest rates would cause home prices to fall, it appears to have limited supply to the point that home prices continue to rise.

CNN

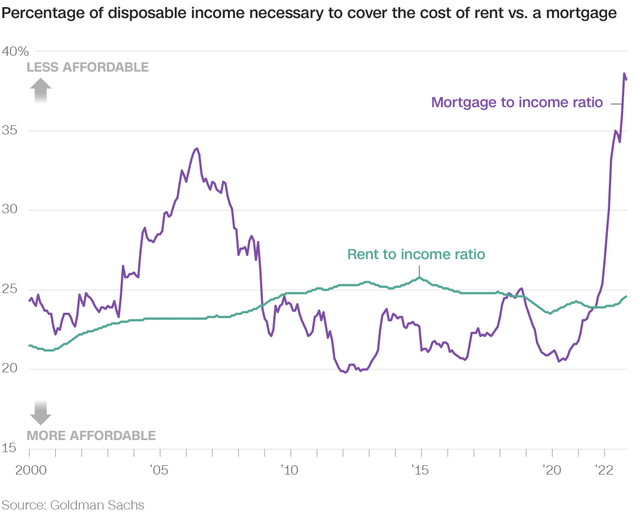

Although rents have also increased, the cost has trailed homeownership significantly. Historically, renting has been cheaper than owning a home. The zero-interest rate policy coming out of the Great Financial Crisis upended the physics of the housing industry. Low mortgage rates meant home ownership was now more affordable on a relative basis than renting. Rising rates have caused this landscape to change dramatically. Now, renting is more affordable than ownership by a wider margin than any point in the past 25 years.

CNN

As the Federal Reserve remains determined to hold rates higher for longer, housing affordability will inevitably continue to suffer. Higher rates will keep mortgage payments elevated and otherwise qualified families will not be able to buy a home. Those families will be forced to turn to an alternative living situation to meet their needs. For ESS, this means an increasing supply of qualified tenants who may have otherwise qualified for a mortgage. This profile of tenant is high quality and will most likely deliver rent on time consistently.

Conclusion

Apartment REITs alleviate a significant amount of responsibility for investors. Without having to prepare leases, perform maintenance, evict delinquent tenants, or perform other time-intensive and expensive tasks, investors can reduce their risk and improve their quality of life. Even better, ESS or similar apartment REITs can benefit from the development of high-quality assets in strong markets. As the tailwinds for multifamily investment continue to blow, ESS remains one of the best ways to capitalize on the opportunity. Currently yielding over 4.0%, this is a unique opportunity to invest in a rare REIT Dividend Aristocrat.

Q2 2024 Earnings Call Transcript")