Robert Way

Investment summary

My recommendation for Ermenegildo Zegna (NYSE:ZGN) is a buy rating. I believe the medium-term guide for 10% sales CAGR and adj. EBIT 20% CAGR is plausible as the business shifts towards targeting loyal and high-spending customers and shifts away from its wholesale strategy. While the near-term (FY24) performance is going to be volatile due to these changes and a weak Chinese spending backdrop, these temporal headwinds should ease eventually.

Business Overview

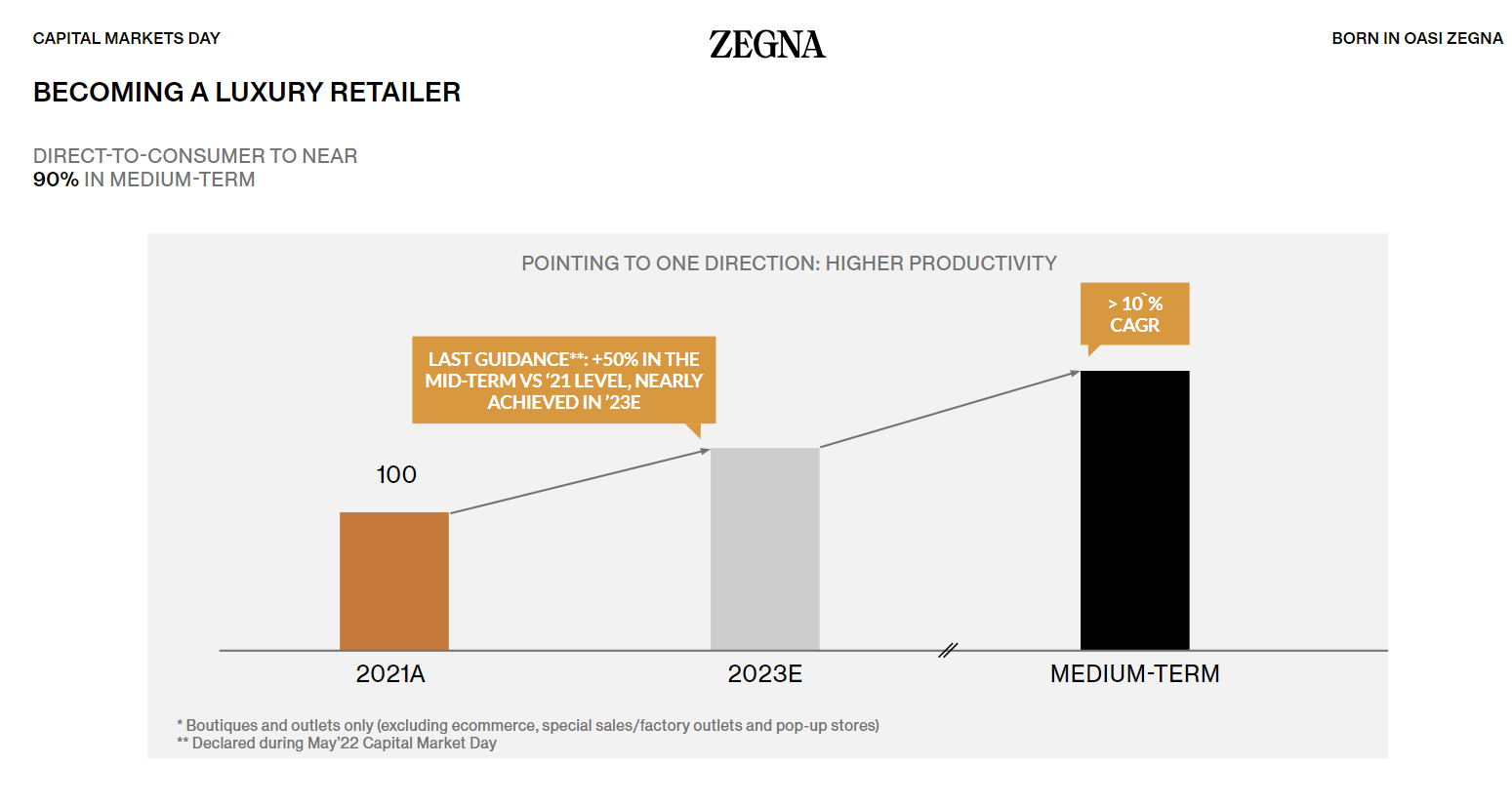

ZGN is an apparel retail operator that manufactures and sells products such as blazers, suits, shoes, and other accessories for men. The key brands that ZGN owns and operates are Zegna and Thom Browne. ZGN derives most of its revenue from across the globe: 43% from APAC, 35% from EMEA< 20% from NA, and the remainder from Latin America and others. The single largest revenue-contributing country is China (31% of total revenue). ZGN reported its FY23 results 3 days ago, where it saw EUR1.905 billion in sales, in line with consensus expectations (note that ZGN already reported its sales figure on Jan’31, so there is not a major surprise here). This represents a constant currency growth rate of 29.7%. As a result, reported EBITDA saw 32% growth from EUR321 million to EUR423 million, with margins sustained at >20% level (22.2% for FY23 from 21.3% in FY22). With the strong performance, management reiterated the medium-term targets announced at its capital market days (December 2023): More than 10% sales CAGR over the medium term and (ii) ~20% adj EBIT CAGR. Below, I discuss my views on the ZGN outlook that make me believe this guidance is achievable.

ZGN

Zegna brand outlook

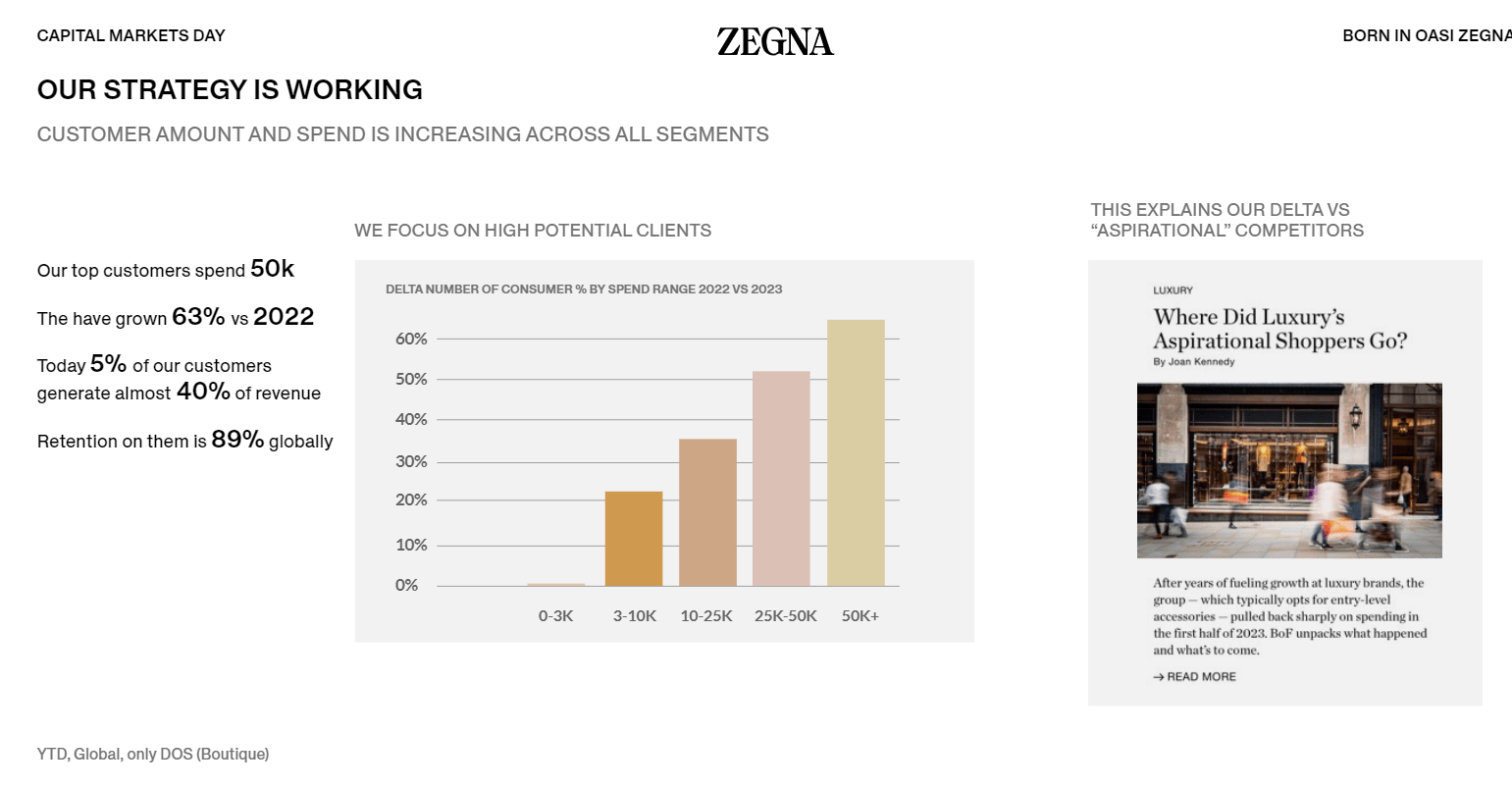

The key focus is on the Zegna brand (85% of total revenue), and I am very positive about the outlook as management continues to position the brand towards the high-end consumer cohort. The distinctive aspect here that makes it more attractive is that the Zegna brand is reducing its exposure to the aspirational segment. This is extremely important, in my view, because ZGN will have more resources to focus on a more loyal (more recurring purchases, and thus, lower customer acquisition cost [CAC]) and affluent cohort mix (a larger budget to spend, and thus, a higher customer lifetime value [CLTV]). From a CLTV-CAC perspective, the unit economics are definitely much better than the typical customer. Management has walked the talk so far as it has moved away from entry-level product lines such as ZZegna, and the financial figures speak for themselves, wherein high-end customers (>EUR50k spend/year) grew 63% vs. 2022, with the top 5% of customers representing 40% of sales (3Q23 earnings call).

ZGN

Thom Browne brand outlook

The Thom Browne brand is most likely going to be a drag on the business’s overall growth, but I see the decline as a strategic-self-inflicted one that should yield positive medium- to long-term results. At the recent earnings call, management announced that it has decided to accelerate the planned rationalization of the wholesale division at Thom Browne, and this is huge because it represents ~52% of the brand’s revenues in FY23, from 52% to 40%. This 10% represents ~EUR43 million in FY23, which is about 2.3% of FY23 revenues. I believe this is the right strategic move because of the tough wholesale environment (competition for loyalty is key to success in the current climate), including online, and it also frees up resources for ZGN to allocate to its retail expansion plan.

However, while the topline will be pressured by this shift, I don’t think the impact will see a 100% flow through to the bottom line, as ZGN should see gross margin benefits (wholesale has a lower margin). I believe driving gross margin expansion is a key focus of management given that they only started to disclose the gross margin metric in FY23, and they did see 210bp gross margin expansion in FY23 to 64.3%.

And in the meantime, we have to stay tuned to our people in stores. They are our first ambassadors. We will continue to streamline our wholesale doors, if anything, even more aggressively than initially planned.

Obviously, it challenging wholesale market around the globe, but at the same time, wholesale remains a great channel. I’m here in Saks, where Saks hosts a fantastic event for VACs and celebrities with an exclusive collection in Los Angeles of accessories and clothing. 4FQ23 earnings

China outlook

Given the contribution of China to ZGN’s revenue, it cannot be left unlooked for, and unfortunately, the consumer demand environment is not looking good at the moment. I am expecting China sales to remain weak for three reasons: (1) the overall weak macro backdrop; (2) a tough base of comp vs. FY23, which saw 25.5% constant currency growth; and (3) the lack of aspirational brand ZZegna revenue contribution given the branding shift. The good news is that all three of these are temporal issues. Fundamentally, the management strategy for a one-brand strategy is working, so as ZGN continues to execute on this strategy and the macro backdrop eventually recovers, growth should come back online.

Secondly, we are seeing some higher than expected volatility in Asia, mainly in Greater China and mainly for Thom Browne. For Zegna, the trend in the region largely reflects the one brand strategy and we see signs confirming that we are moving into the right direction, even if the strategy has yet to be fully completed. 4FQ23 earnings

Valuation

Redfox Capital Ideas

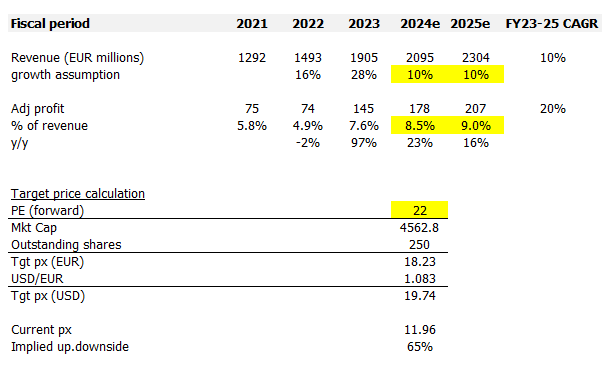

I model ZGN using a forward PE approach, and using my assumptions, I believe ZGN is worth ~$20. For revenue-modeled ZGN, I used the low point of the medium-term growth outlook (10%), and I used the low point because FY24 is going to be a year of transition, so while I assumed 10% growth for both years, reported growth could be lower for FY24 and higher for FY25. Depending on how much transition impact ZGN is going to experience in FY24, it would impact the CAGR growth rates between FY23 and FY25. For adj profit (adj earnings), I am using management’s 20% adj EBIT growth CAGR as a benchmark as well, which I think makes sense as the shift away from wholesale and focus on a loyal and high-spending customer base (which has higher unit economics) should drive margin expansion, leading to earnings seeing faster-than-revenue growth.

While I see ZGN’s recent performance through a positive lens, I can understand why the share price fell as well, because FY24 is going to be a volatile year given the transition and tough comparable performance in FY23. Especially with the Chinese market demand backdrop still weak, investors are going to take a risk-adverse approach. As such, it is unlikely that the market will revalue ZGN’s multiple back to its historical average anytime soon, but it doesn’t matter because even a slight upgrade in multiple to 22x (-1 standard deviation of ZGN forward PE bend since it got listed) makes the upside material. I don’t think it is demanding to assume 22x, given that it traded at that level just a few weeks ago.

Risk

FY24 transitional headwinds could be more pronounced than I expected if: (1) China demand slows further; (2) the shift away from wholesale causes other wholesale retailers to leave as well. Also, while the focus on a loyal and high-spending customer strategy is sound (shifting away from the aspirational brand ZZegna), this also means that ZGN revenue is going to get more concentrated. If the global economy worsens, ZGN might not have any lower-priced products to take advantage of any trade-down motion.

Conclusion

My view for ZGN is a buy rating. The company’s strategic shift towards a loyal, high-spending clientele and away from wholesale channels positions it for sustainable growth. While near-term headwinds exist due to these changes and a weak Chinese market, they are temporary. While the stock price may remain volatile in the short term, a slight multiple expansion can unlock attractive upside potential.

Q2 2024 Earnings Call Transcript")