John Lamparski/Getty Images Entertainment

This article was coproduced with Wolf Report.

The legendary investor Sam Zell passed away a few months ago, and he’s missed by many, and I feel fortunate to have had the chance to become friends with him.

In 2021, I wrote The Intelligent REIT Investor Guide, and I was honored that Mr. Zell provided me with this testimonial:

“The simple genius of public REITs is that they turn bricks and mortar into transparent and predictable liquid assets. Since they tend to pay high dividends, REITs can serve as a terrific addition to an investment portfolio. Thomas’ book helps break down this asset class for the average person, making REITs more understandable, and therefore more accessible, to everyone.”

Sam Zell, American billionaire businessman and philanthropist (worth $5.3 billion according to Forbes).

Mr. Zell was once nicknamed “the grave dancer” for his strategy of profiting from distressed real estate, and he once cautioned:

“He who dances closest to the graves always has to be careful he doesn’t fall in.”

Now, over the years I learned a lot from Mr. Zell, which is why I decided to tribute my latest book (REITs For Dummies) to the mastermind. Here’s an excerpt from this dedication:

“The book is dedicated to legendary tycoon Sam Zell (1941-2023) …he was nicknamed the “gravedancer” for snatching up distressed properties at wide discounts, and he inspired so many others to try to follow in his ever-impressive footsteps.”

Mr. Zell created three real estate investment trusts, or REITs, including Equity Residential (NYSE:EQR), Equity Lifestyle (ELS), and Equity Office, which Zell sold to Blackstone (BX) in 2006.

Today, we decided to focus on Equity Residential and why we view this REIT as a very solid pick for the valuation-conscious but conservative dividend investor looking for A-rated safety.

Why?

Because EQR is indeed A-rated, has a 4.3%+ yield at today’s price, and comes with a decent 3-5% growth estimate on an annual forward basis.

Again, a lot to like just when talking about fundamentals – and things get better from here onward.

In this article, we mean to update our thesis on the company and show you why we consider this company a very solid overall play.

There’s a reason why this company is down.

There are also very clear reasons why we own more and higher stakes in other multifamily and residential REITs, but this company still has a lot going for it.

That is especially true at this valuation.

Let us show you what we mean.

Source: Brad Thomas

Equity Residential – and what we like about it

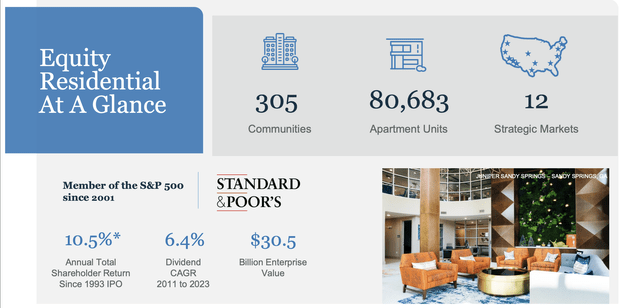

So, first of all – as you can see below, EQR owns 305 communities in 12 strategic markets.

EQR IR

EQR has exposure to the west and east coast, as opposed to the currently more attractive sunbelt or sun states (i.e., MAA and CPT).

Equity Residential is primarily a Washington, Seattle, San-Fran, and Southern Cali REIT in terms of exposure, though it has other areas growing as well.

The challenges with these areas should not be unknown to anyone at this particular point.

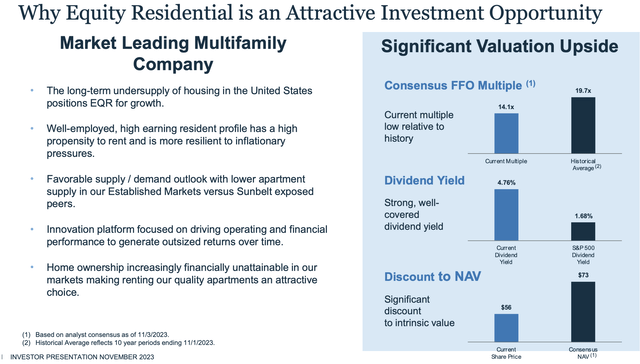

The fact that the company is undervalued relative to historicals – well, that’s something that hasn’t gone unnoticed by the company, either. In fact, they present it as one of the primary investment reasons for this company.

EQR IR

So, the company itself is very aware of what valuation-related upside it has going for itself, even if that upside isn’t really as high as it was back in November.

The overall macro picture in the U.S. is very complex, but there is an overall undersupply of housing and living solutions, which means that current trends, especially with current interest rates, actually do favor rental housing above other options.

Like other of its peers, EQR caters primarily to fairly affluent customers, and demand here is continuing to be relatively strong.

Other than that, this is primarily a supply/demand play, and the company’s fundamentals here look good.

In EQR’s established markets, there’s less than one unit of new supply forecasted relative to each new projected job – which means that the fundamentals for this company are very good going forward.

EQR presents that the numbers for Sunbelt are actually exceeding new units for each new job, implying a long-term potential of oversupply.

We say this is valid – but we would also be careful with these claims of upside because EQR’s home markets need to come to grips with the fact that job growth and appeal are likely to be lower than in the aforementioned sun belt and other states.

Still, as we have said in other articles, we do view the panic about coastal markets as overplayed, and we do view the punishment as overdone.

So we’re happy to invest, as long as the price is “good” or okay.

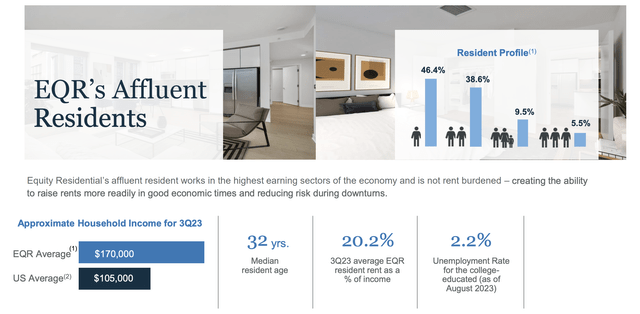

Here’s the typical resident of an EQR rental property.

EQR IR

We see similarities among many of this company’s residents, as it’s very typical for exactly this demography to look for this sort of situation.

And with job creation, for the time being, remaining good, the downside for the company’s earnings and AFFO remain somewhat limited, at least as we see it.

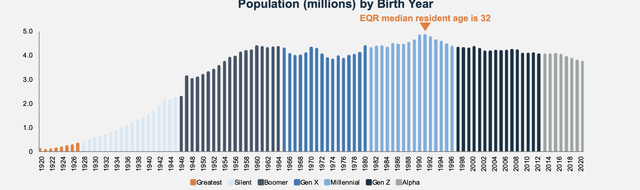

Demographic trends continue to support a long-term demand picture, for a few reasons.

Millennials are more likely to keep renting longer due to the sheer cost of family ownership and overall lifestyle preferences.

EQR IR

Marriage ages are far higher, and the median age for the first child is up almost 30% in less than 30 years.

The company has only token exposure to areas that other REITs in this sector consider to be their core areas, such as Dallas and Austin.

Over 25% of the company’s NOI comes from SoCAL, another 11% from Seattle, and 16% from San Fran.

That’s almost 50% of NOI, and another 16% from D.C, 14% from NYC and 11% from Boston.

That means that EQR actually has exposure to many geographies that some companies, especially offices, are looking to vacate.

The core question investors should be asking themselves is if they believe in a resurgence in these geographies, and that they will remain fundamentally appealing areas to live and work in.

If you believe that to be the case, we will argue there is very little reason to doubt EQR – because it’s among the market leaders in these segments geographically.

The “new” fact to consider is what has happened in these markets, and what value or discount you would assign to this.

The company has a strong, near-96% physical occupancy and the company has managed a renewal rate increase of 5.5%, a. new lease change of 0.5%, with a blended a 1.6% as of Q3 2023.

Not the best increase, but considering where the company operates, we’ll call it “good enough.”

There also doesn’t seem to be any worry about delinquencies – bad debt is improving, at least compared to the company’s historical trends.

EQR, unlike other players, does have a backlog of evictions that are not yet finished, and this is a different factor compared to its competition – because un-evicted tenants do still count towards the physical occupancy.

This is perhaps, aside from the geographical issue, the one risk we would consider very significant to this company.

Not something that EQR cannot solve, but something that’s going to weigh on earnings for some time. But don’t just take our word for it – take EQR’s.

Much like last year, we expect 2024 to continue to show improvement. We also expect the pace of this improvement to be dependent on the speed of the court systems, primarily in Southern California, where delinquency remains highest to quickly process evictions, which is a hard thing to predict. As a result, our guidance assumes that 2024 remains another transition year for bad debt and that we don’t get all the way back to pre-pandemic levels.

(Source: Robert Garachana, Q4 2023 Earnings Call.)

According to several news outlets, there is now talk of an “eviction cliff,” and current eviction cases are higher than the pre-pandemic level, though not as high as post-GFC.

Overall, looking at Q4 2023, we would not say this is a reason not to invest in EQR, but it is a reason to be perhaps a bit wary of the valuation.

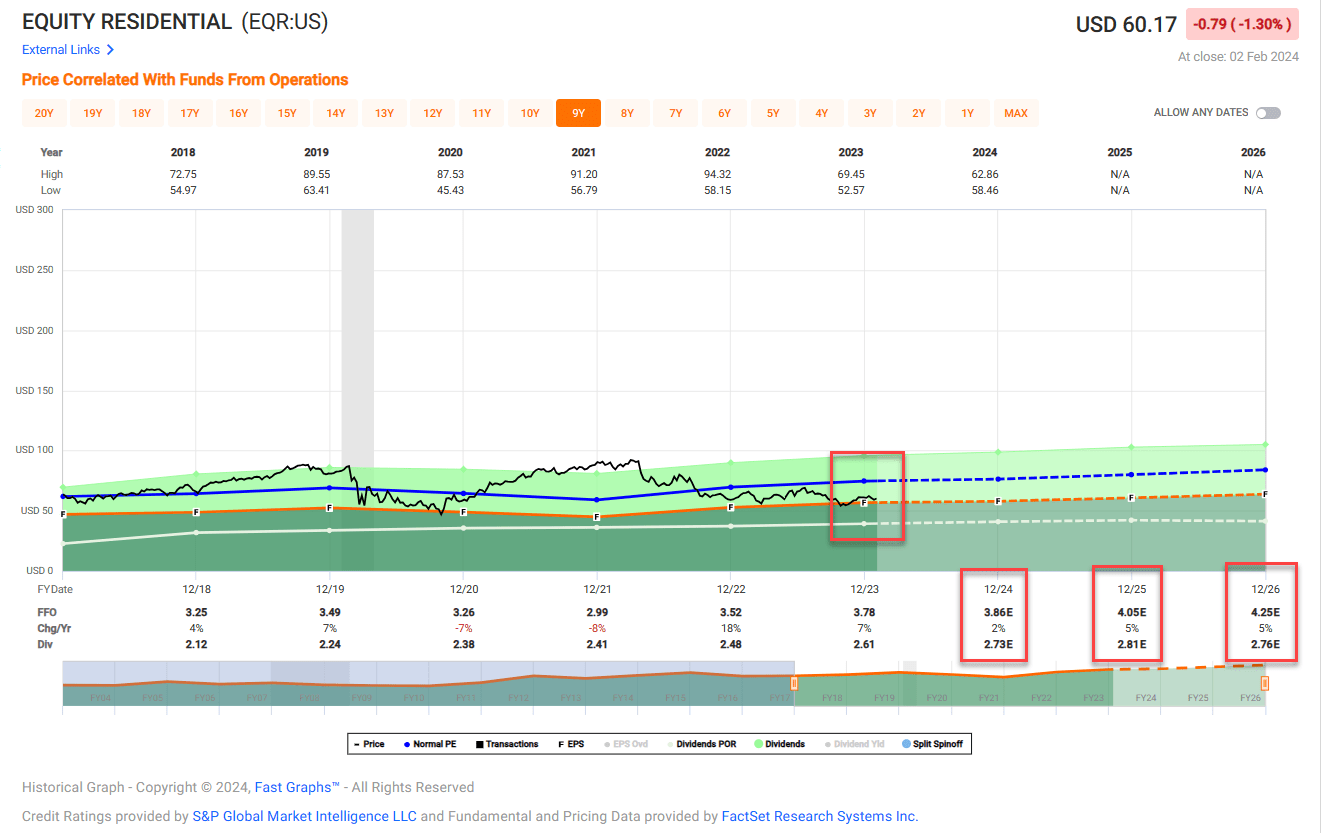

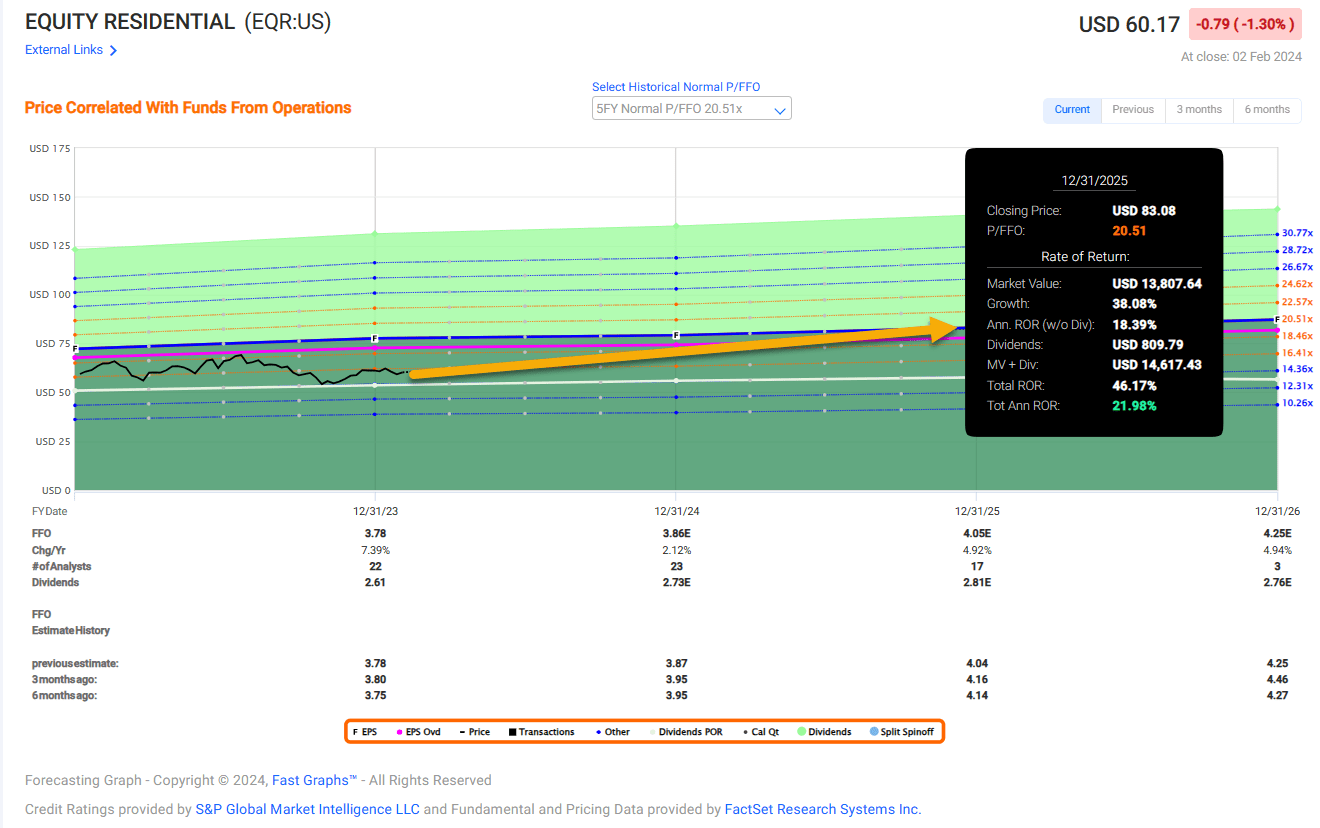

Valuation – plenty of upside here

EQR is attractively valued here.

The company’s typical 5-year average comes to around 20-22x P/FFO, which is the range for most premium Residential REITs, of which EQR is one.

The company’s A-credit and other fundamental characteristics make other considerations almost impossible.

We do not consider EQR’s 5-year premium to be valid.

Due to the lower quality of the company’s tenancy, meaning the evictions and the exposure to lower-appeal states and geographies (a description we consider to be justified – but feel free to disagree), we would go to 18-19x P/FFO, at most, rather than to the 20-24x P/FFO that we would consider valid in other companies.

This valuation means that the company has an upside to, at most, around 14% annually with the current forecast, and a price target, or PT, of around $77/share, which also will be our updated share price for EQR.

With this share price, we believe we’re taking into consideration the trouble and challenges that the company is presented with, without being irrationally negative on what is, in the end, a great business.

Because we don’t see a likelihood of a dividend cut, of a severe drop in FFO or earnings/NOI, of any real serious downturn – that’s why we remain positive on this company’s potential.

S&P Global analysts give the company from $58 to a high of around $87, but with an average of $69.5 – which is a considerable distance from $77, but we maintain that while there is risk in the coastal markets, it’s not as high as some would have you believe, and we maintain that this investment is one of the more solid ones you can make.

Is it more solid than investing in MAA or CPT here?

No.

EQR is a bolt-on purchase to positions we already own (i.e., MAA and CPT).

If you’re not yet fully invested in either MAA or CPT, then we would say that you might want to look closer at those two here, particularly CPT, which not only has an almost similar yield, but a better growth profile, A-rating and better history of hitting targets alongside only trivial non-attractive sunbelt exposure.

The same is actually true for MAA, which also has a better yield.

So again, every investment needs to justify itself in context.

EQR is a great REIT.

We consider it a “BUY.”

We’re not scared of coastal market investment, neither office/industrial nor this type. But it’s all about knowing value.

FAST Graphs

Thesis

- Equity Residential is by far the best-rated and most qualitative, high-yielding non-sunbelt multifamily residential out there. It offers A-rating, and aside from this also a 4.35% yield with a prospect for DGR proven by history, as well as an upside with growth of 2-4% for the next few years.

- This makes its current valuation of 16x to FFO an attractive potential, if not as attractive as when it traded closer to 15x and offered almost a 20% annualized upside per year to the normalized premium.

- We consider EQR a “BUY” here, but we would not go higher than a $77/share PT, which comes to a 13-14% annualized upside with yield included to an 18x normalized P/FFO. It’s a good price, not a great one, but worthy of a “BUY” rating nonetheless.

FAST Graphs

Q2 2024 Earnings Call Transcript")